Session 8: Rough Volatility

Course: Advanced Volatility Modeling¶

Learning Objectives¶

Understand fractional Brownian motion and the Hurst parameter

Explore the empirical evidence for rough volatility

Implement the rough Bergomi model

Connect rough volatility to realized volatility behavior

1. Motivation: Volatility is Rough¶

1.1 Classical vs Rough Volatility¶

Classical SV (Heston): Volatility driven by standard Brownian motion (H = 0.5)

Rough Volatility (Gatheral et al., 2018): Volatility driven by fractional Brownian motion with

1.2 Key Empirical Finding¶

with across many assets!

Source

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from scipy import stats

import warnings

warnings.filterwarnings('ignore')

plt.style.use('seaborn-v0_8-whitegrid')

plt.rcParams['figure.figsize'] = (12, 6)

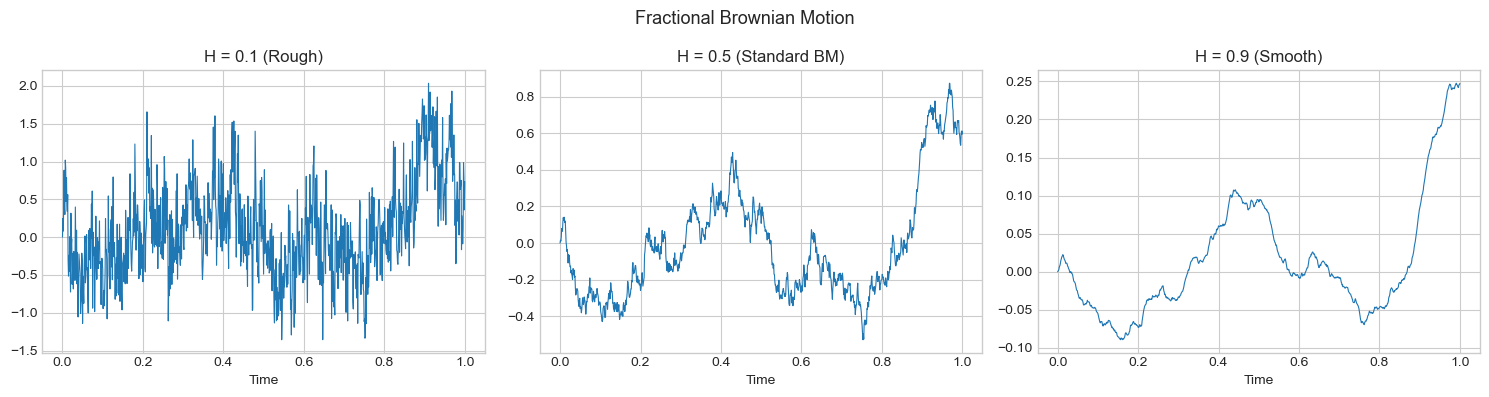

np.random.seed(42)2. Fractional Brownian Motion¶

2.1 Definition¶

fBM with Hurst parameter :

| H value | Property |

|---|---|

| H < 0.5 | Rough, anti-persistent |

| H = 0.5 | Standard Brownian motion |

| H > 0.5 | Smooth, persistent |

Source

def simulate_fbm_cholesky(n, H, T=1, seed=None):

"""Simulate fBM using Cholesky decomposition."""

if seed is not None:

np.random.seed(seed)

dt = T / n

t = np.linspace(0, T, n + 1)

# Build covariance matrix

cov = np.zeros((n, n))

for i in range(n):

for j in range(n):

ti, tj = (i + 1) * dt, (j + 1) * dt

cov[i, j] = 0.5 * (ti**(2*H) + tj**(2*H) - abs(ti - tj)**(2*H))

L = np.linalg.cholesky(cov + 1e-10 * np.eye(n))

Z = np.random.standard_normal(n)

W_H = np.zeros(n + 1)

W_H[1:] = L @ Z

return t, W_H

# Compare different H values

fig, axes = plt.subplots(1, 3, figsize=(15, 4))

for ax, H in zip(axes, [0.1, 0.5, 0.9]):

t, W = simulate_fbm_cholesky(1000, H, seed=42)

ax.plot(t, W, linewidth=0.8)

ax.set_title(f'H = {H} ({"Rough" if H < 0.5 else "Standard BM" if H == 0.5 else "Smooth"})')

ax.set_xlabel('Time')

plt.suptitle('Fractional Brownian Motion', fontsize=13)

plt.tight_layout()

plt.show()

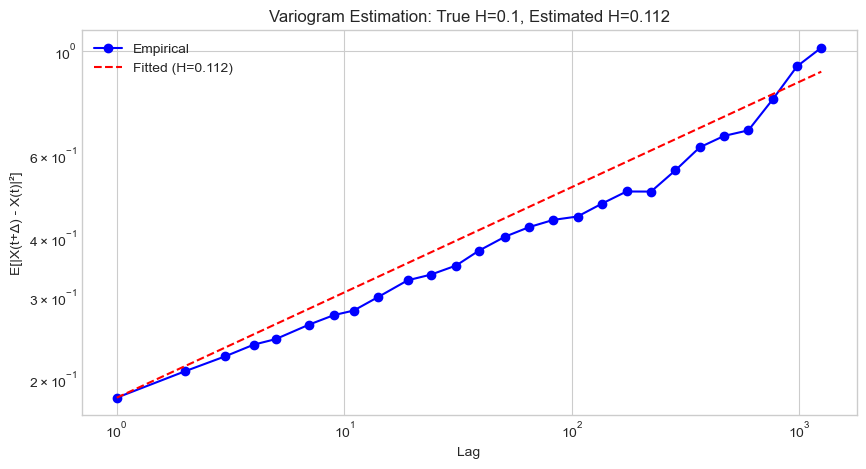

3. Estimating the Hurst Parameter¶

Source

def estimate_hurst_variogram(x, q=2, max_lag=None):

"""Estimate Hurst parameter using variogram method."""

n = len(x)

if max_lag is None:

max_lag = n // 4

lags = np.unique(np.logspace(0, np.log10(max_lag), 30).astype(int))

m_q = [np.mean(np.abs(x[lag:] - x[:-lag])**q) for lag in lags]

# Log-log regression

slope, _ = np.polyfit(np.log(lags), np.log(m_q), 1)

H = slope / q

return H, lags, np.array(m_q)

# Test on simulated fBM

true_H = 0.1

t, W_rough = simulate_fbm_cholesky(5000, true_H, seed=42)

H_est, lags, m_q = estimate_hurst_variogram(W_rough, q=2)

fig, ax = plt.subplots(figsize=(10, 5))

ax.loglog(lags, m_q, 'bo-', label='Empirical')

ax.loglog(lags, m_q[0] * (lags/lags[0])**(2*H_est), 'r--',

label=f'Fitted (H={H_est:.3f})')

ax.set_xlabel('Lag')

ax.set_ylabel('E[|X(t+Δ) - X(t)|²]')

ax.set_title(f'Variogram Estimation: True H={true_H}, Estimated H={H_est:.3f}')

ax.legend()

plt.show()

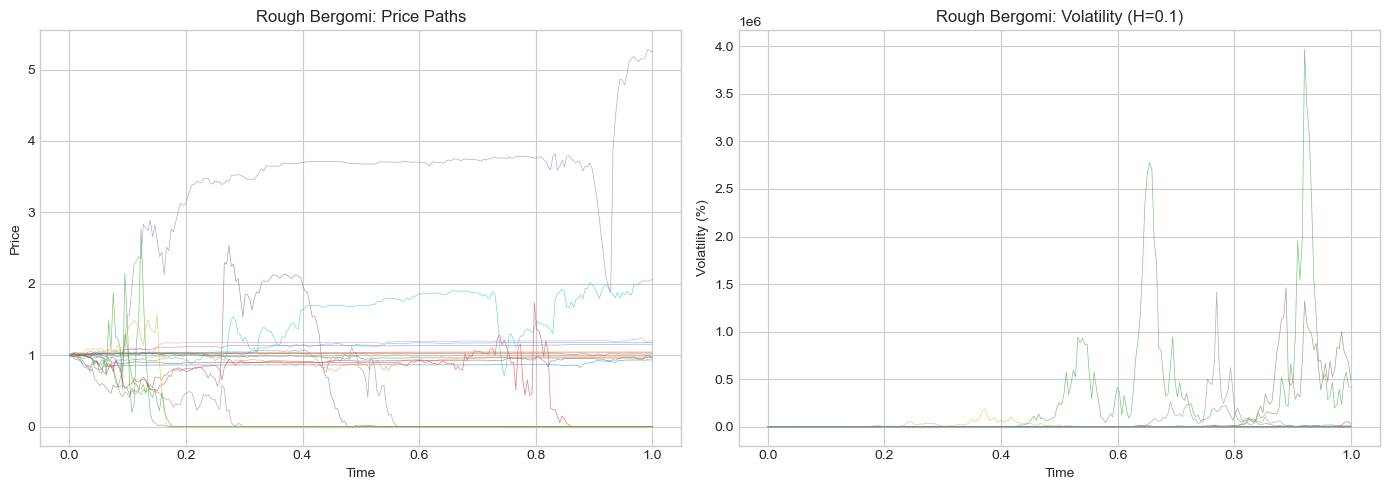

4. The Rough Bergomi Model¶

4.1 Model Specification (Bayer, Friz & Gatheral, 2016)¶

where:

is fractional Brownian motion with

is the forward variance curve

controls vol-of-vol

Source

def simulate_rough_bergomi(n_paths, n_steps, T, H, eta, rho, xi0, S0=1, seed=None):

"""

Simulate the rough Bergomi model.

Parameters

----------

n_paths : int

Number of Monte Carlo paths

n_steps : int

Number of time steps

T : float

Time horizon

H : float

Hurst parameter

eta : float

Vol-of-vol

rho : float

Correlation between price and variance

xi0 : float

Initial forward variance (flat curve)

"""

if seed is not None:

np.random.seed(seed)

dt = T / n_steps

t = np.linspace(0, T, n_steps + 1)

S = np.zeros((n_paths, n_steps + 1))

V = np.zeros((n_paths, n_steps + 1))

S[:, 0] = S0

V[:, 0] = xi0

for path in range(n_paths):

# Generate fBM for this path (simplified using approximate method)

dW_H = np.zeros(n_steps)

for i in range(n_steps):

# Approximate fBM increment (simplified)

dW_H[i] = np.random.normal(0, dt**H)

W_H = np.cumsum(dW_H)

W_H = np.concatenate([[0], W_H])

# Variance process

for i in range(n_steps + 1):

V[path, i] = xi0 * np.exp(eta * W_H[i] - 0.5 * eta**2 * t[i]**(2*H))

# Price process

for i in range(n_steps):

Z = np.random.standard_normal()

dW_S = rho * dW_H[i] / (dt**H) * np.sqrt(dt) + np.sqrt(1 - rho**2) * Z * np.sqrt(dt)

S[path, i+1] = S[path, i] * np.exp(-0.5 * V[path, i] * dt + np.sqrt(V[path, i]) * dW_S)

return t, S, V

# Simulate rough Bergomi

T = 1

n_steps = 252

n_paths = 100

H = 0.1

eta = 1.5

rho = -0.7

xi0 = 0.04

t, S, V = simulate_rough_bergomi(n_paths, n_steps, T, H, eta, rho, xi0, seed=42)

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

for i in range(min(20, n_paths)):

axes[0].plot(t, S[i], linewidth=0.5, alpha=0.6)

axes[0].set_xlabel('Time')

axes[0].set_ylabel('Price')

axes[0].set_title('Rough Bergomi: Price Paths')

for i in range(min(20, n_paths)):

axes[1].plot(t, np.sqrt(V[i]) * 100, linewidth=0.5, alpha=0.6)

axes[1].set_xlabel('Time')

axes[1].set_ylabel('Volatility (%)')

axes[1].set_title(f'Rough Bergomi: Volatility (H={H})')

plt.tight_layout()

plt.show()

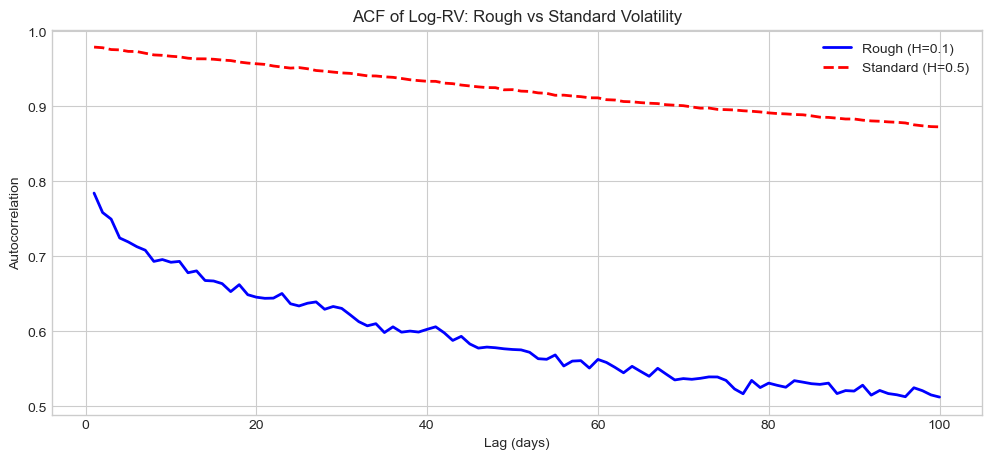

5. Empirical Evidence from Realized Volatility¶

Source

def simulate_rv_series(n_days, H=0.1, base_vol=0.02, seed=None):

"""Simulate daily RV series with rough volatility."""

if seed is not None:

np.random.seed(seed)

# Simulate log-volatility as fBM

_, log_vol_fBm = simulate_fbm_cholesky(n_days, H, T=n_days/252, seed=seed)

# Scale and exponentiate

log_vol = np.log(base_vol) + 0.3 * log_vol_fBm

rv = np.exp(2 * log_vol) # Variance

# Add measurement noise

rv = rv * np.random.lognormal(0, 0.1, len(rv))

return rv, log_vol

# Simulate and estimate H

n_days = 2500

true_H = 0.1

rv_rough, log_vol_rough = simulate_rv_series(n_days, H=true_H, seed=42)

H_est_rough, _, _ = estimate_hurst_variogram(np.log(rv_rough), q=2)

# Also simulate with standard H=0.5

rv_standard, log_vol_std = simulate_rv_series(n_days, H=0.5, seed=43)

H_est_std, _, _ = estimate_hurst_variogram(np.log(rv_standard), q=2)

print("Hurst Parameter Estimation from Log-RV")

print("="*50)

print(f"Rough volatility (true H={true_H}): Estimated H = {H_est_rough:.3f}")

print(f"Standard volatility (true H=0.5): Estimated H = {H_est_std:.3f}")Hurst Parameter Estimation from Log-RV

==================================================

Rough volatility (true H=0.1): Estimated H = 0.098

Standard volatility (true H=0.5): Estimated H = 0.287

6. Implications of Rough Volatility¶

6.1 For Option Pricing¶

Better fit to implied volatility surface

Explains short-term smile steepness

6.2 For Forecasting¶

Very short-term persistence but rapid mean reversion

Different from standard long-memory models

Source

# Autocorrelation comparison

def compute_acf(x, max_lag=100):

n = len(x)

x = x - x.mean()

acf = [np.corrcoef(x[:-lag], x[lag:])[0,1] for lag in range(1, max_lag+1)]

return np.array(acf)

acf_rough = compute_acf(np.log(rv_rough), 100)

acf_std = compute_acf(np.log(rv_standard), 100)

fig, ax = plt.subplots(figsize=(12, 5))

ax.plot(range(1, 101), acf_rough, 'b-', label=f'Rough (H={true_H})', linewidth=2)

ax.plot(range(1, 101), acf_std, 'r--', label='Standard (H=0.5)', linewidth=2)

ax.set_xlabel('Lag (days)')

ax.set_ylabel('Autocorrelation')

ax.set_title('ACF of Log-RV: Rough vs Standard Volatility')

ax.legend()

plt.show()

print("\nRough volatility shows faster initial decay but longer persistence.")

Rough volatility shows faster initial decay but longer persistence.

7. Summary¶

Key Takeaways¶

Empirical finding: H ≈ 0.1 across assets (much rougher than H=0.5)

Fractional BM: Driving process for rough volatility models

Rough Bergomi: Popular model for option pricing

Implications: Better option fit, different forecasting dynamics

Preview: Session 9¶

Multivariate volatility models (DCC, BEKK).

Exercises¶

Estimate H from real S&P 500 realized volatility data

Implement the rough Heston model

Compare option prices from Heston vs rough Bergomi

Investigate H across different asset classes (crypto, FX, commodities)

References¶

Gatheral, J., Jaisson, T., & Rosenbaum, M. (2018). Volatility is rough. Quantitative Finance, 18(6), 933-949.

Bayer, C., Friz, P., & Gatheral, J. (2016). Pricing under rough volatility. Quantitative Finance, 16(6), 887-904.

Bennedsen, M., Lunde, A., & Pakkanen, M. S. (2022). Decoupling the short-and long-term behavior of stochastic volatility. Journal of Financial Econometrics, 20(5), 961-1006.