Session 7: Stochastic Volatility Models

Course: Advanced Volatility Modeling¶

Learning Objectives¶

Understand stochastic volatility (SV) in continuous and discrete time

Compare SV to GARCH: key differences and implications

Estimate SV models using quasi-maximum likelihood

Explore the Heston model and affine structures

1. Stochastic Volatility: Core Idea¶

1.1 GARCH vs SV¶

GARCH: Volatility is deterministic given past returns:

Stochastic Volatility: Volatility has its own source of randomness:

where is a shock independent of the return innovation.

1.2 Why Stochastic Volatility?¶

More realistic: Volatility can change even without large returns

Option pricing: Better fits option smile/skew

Continuous-time foundation: Natural extension of diffusions

Separate risk factors: Volatility risk can be priced separately

Source

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from scipy.optimize import minimize

from scipy import stats

import warnings

warnings.filterwarnings('ignore')

plt.style.use('seaborn-v0_8-whitegrid')

plt.rcParams['figure.figsize'] = (12, 6)

np.random.seed(42)2. Discrete-Time SV Model¶

2.1 Basic Specification (Taylor, 1986)¶

where are returns and is log-volatility.

Parameters:

: long-run mean of log-volatility

: persistence (should be < 1 for stationarity)

: volatility of volatility

Source

def simulate_sv(n, mu, phi, sigma_eta, seed=None):

"""

Simulate discrete-time stochastic volatility model.

y_t = exp(h_t/2) * eps_t

h_t = mu + phi*(h_{t-1} - mu) + sigma_eta * eta_t

"""

if seed is not None:

np.random.seed(seed)

h = np.zeros(n)

y = np.zeros(n)

eps = np.random.standard_normal(n)

eta = np.random.standard_normal(n)

# Initialize at unconditional mean

h[0] = mu + sigma_eta * eta[0] / np.sqrt(1 - phi**2)

y[0] = np.exp(h[0] / 2) * eps[0]

for t in range(1, n):

h[t] = mu + phi * (h[t-1] - mu) + sigma_eta * eta[t]

y[t] = np.exp(h[t] / 2) * eps[t]

return y, h

# Simulate SV process

n = 2500

mu = -10 # exp(-10/2) ≈ 0.0067 daily vol

phi = 0.97

sigma_eta = 0.15

y_sv, h_sv = simulate_sv(n, mu, phi, sigma_eta, seed=42)

# Also simulate GARCH for comparison

def simulate_garch(n, omega, alpha, beta, seed=None):

if seed is not None:

np.random.seed(seed)

eps = np.random.standard_normal(n)

y = np.zeros(n)

sigma2 = np.zeros(n)

sigma2[0] = omega / (1 - alpha - beta)

y[0] = np.sqrt(sigma2[0]) * eps[0]

for t in range(1, n):

sigma2[t] = omega + alpha * y[t-1]**2 + beta * sigma2[t-1]

y[t] = np.sqrt(sigma2[t]) * eps[t]

return y, sigma2

y_garch, sigma2_garch = simulate_garch(n, 0.01, 0.05, 0.90, seed=42)

# Compare

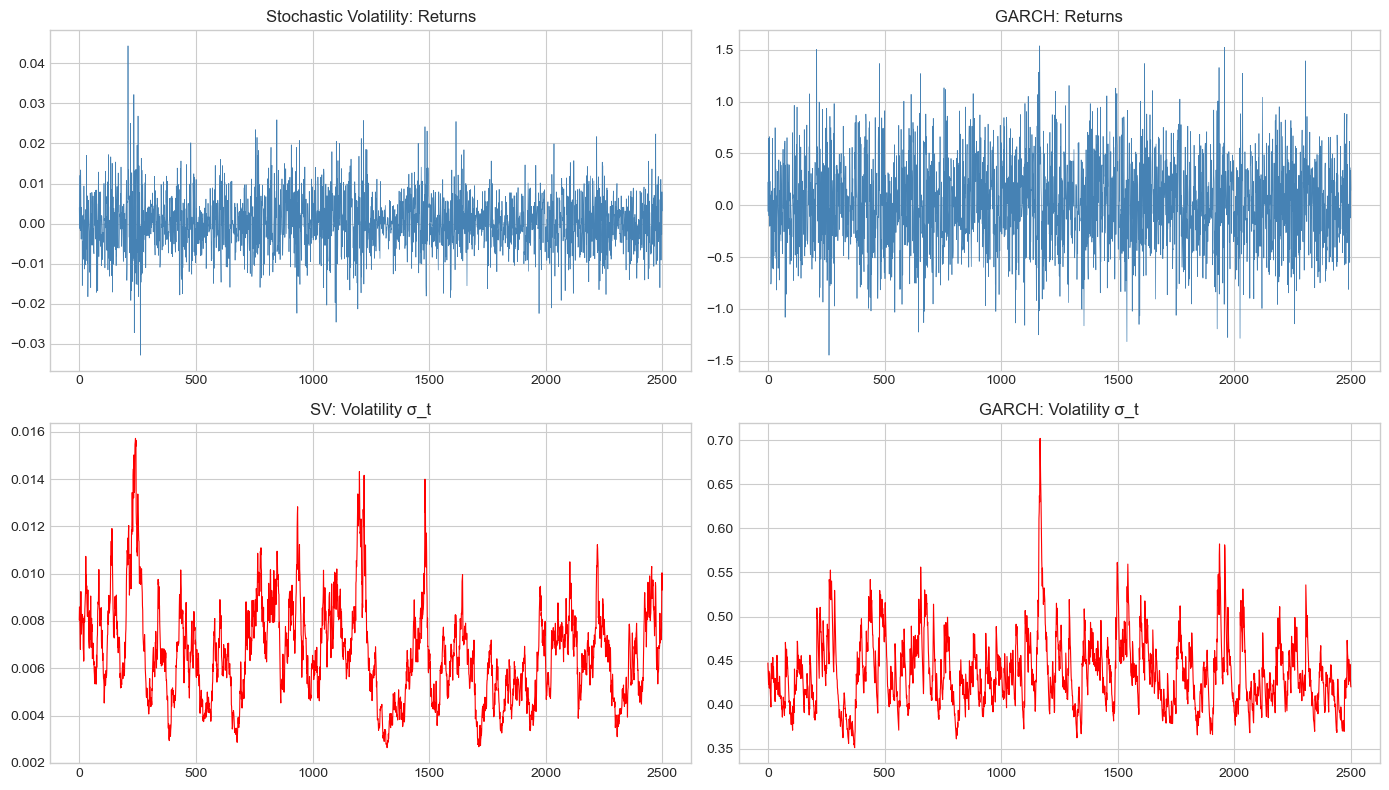

fig, axes = plt.subplots(2, 2, figsize=(14, 8))

axes[0,0].plot(y_sv, linewidth=0.5, color='steelblue')

axes[0,0].set_title('Stochastic Volatility: Returns')

axes[0,1].plot(y_garch, linewidth=0.5, color='steelblue')

axes[0,1].set_title('GARCH: Returns')

axes[1,0].plot(np.exp(h_sv/2), linewidth=0.8, color='red')

axes[1,0].set_title('SV: Volatility σ_t')

axes[1,1].plot(np.sqrt(sigma2_garch), linewidth=0.8, color='red')

axes[1,1].set_title('GARCH: Volatility σ_t')

plt.tight_layout()

plt.show()

3. Estimation: Quasi-Maximum Likelihood¶

3.1 The Estimation Challenge¶

SV models have a non-linear latent state , making exact MLE intractable.

3.2 Harvey et al. (1994) Approach¶

Transform to linear state-space form by squaring and taking logs:

where with mean -1.27 and variance .

This gives a linear Gaussian state-space model (approximately), enabling Kalman filter estimation.

Source

def sv_qml_loglik(params, y_squared_log):

"""

Quasi-MLE for SV model using Kalman filter.

Observation: y*_t = h_t + xi_t, where xi_t ~ log(chi^2_1)

State: h_t = mu + phi*(h_{t-1} - mu) + sigma_eta * eta_t

"""

mu, phi, sigma_eta = params

# Constraints

if sigma_eta <= 0 or abs(phi) >= 1:

return 1e10

T = len(y_squared_log)

# Constants for log(chi^2_1)

xi_mean = -1.2704 # E[log(chi^2_1)]

xi_var = 4.93 # Var[log(chi^2_1)] ≈ pi^2/2

# Adjust observations

y_adj = y_squared_log - xi_mean

# Initialize Kalman filter

h_pred = mu

P_pred = sigma_eta**2 / (1 - phi**2)

loglik = 0

for t in range(T):

# Prediction error

v = y_adj[t] - h_pred

F = P_pred + xi_var

# Log-likelihood contribution

loglik += -0.5 * (np.log(2*np.pi) + np.log(F) + v**2/F)

# Kalman gain

K = P_pred / F

# Update

h_filt = h_pred + K * v

P_filt = P_pred * (1 - K)

# Predict

h_pred = mu + phi * (h_filt - mu)

P_pred = phi**2 * P_filt + sigma_eta**2

return -loglik # Return negative for minimization

def fit_sv_qml(returns):

"""Fit SV model using QML."""

# Transform data

y_sq = returns**2

y_sq[y_sq == 0] = 1e-10 # Avoid log(0)

y_log = np.log(y_sq)

# Initial values

mu0 = np.mean(y_log)

phi0 = 0.95

sigma_eta0 = 0.2

result = minimize(

sv_qml_loglik,

[mu0, phi0, sigma_eta0],

args=(y_log,),

method='Nelder-Mead',

options={'maxiter': 5000}

)

return result

# Fit to simulated data

sv_fit = fit_sv_qml(y_sv)

print("Stochastic Volatility QML Estimation")

print("="*50)

print(f"\nTrue parameters:")

print(f" μ = {mu}")

print(f" φ = {phi}")

print(f" σ_η = {sigma_eta}")

print(f"\nEstimated parameters:")

print(f" μ = {sv_fit.x[0]:.4f}")

print(f" φ = {sv_fit.x[1]:.4f}")

print(f" σ_η = {sv_fit.x[2]:.4f}")Stochastic Volatility QML Estimation

==================================================

True parameters:

μ = -10

φ = 0.97

σ_η = 0.15

Estimated parameters:

μ = -10.1676

φ = 0.9508

σ_η = 0.2196

4. Continuous-Time SV: The Heston Model¶

4.1 Model Specification¶

with .

Parameters:

: mean reversion speed

: long-run variance

: volatility of volatility

: leverage correlation (typically negative)

4.2 Feller Condition¶

ensures variance stays positive.

Source

def simulate_heston(T, n_steps, S0, V0, mu, kappa, theta, sigma_v, rho, seed=None):

"""

Simulate Heston stochastic volatility model using Euler discretization.

"""

if seed is not None:

np.random.seed(seed)

dt = T / n_steps

S = np.zeros(n_steps + 1)

V = np.zeros(n_steps + 1)

S[0] = S0

V[0] = V0

for i in range(n_steps):

# Correlated Brownian motions

Z1 = np.random.standard_normal()

Z2 = np.random.standard_normal()

W_S = Z1

W_V = rho * Z1 + np.sqrt(1 - rho**2) * Z2

# Ensure variance stays positive (full truncation)

V_pos = max(V[i], 0)

# Euler step

S[i+1] = S[i] * np.exp((mu - 0.5*V_pos)*dt + np.sqrt(V_pos*dt)*W_S)

V[i+1] = V[i] + kappa*(theta - V_pos)*dt + sigma_v*np.sqrt(V_pos*dt)*W_V

V[i+1] = max(V[i+1], 0) # Reflection

return S, V

# Simulate Heston model

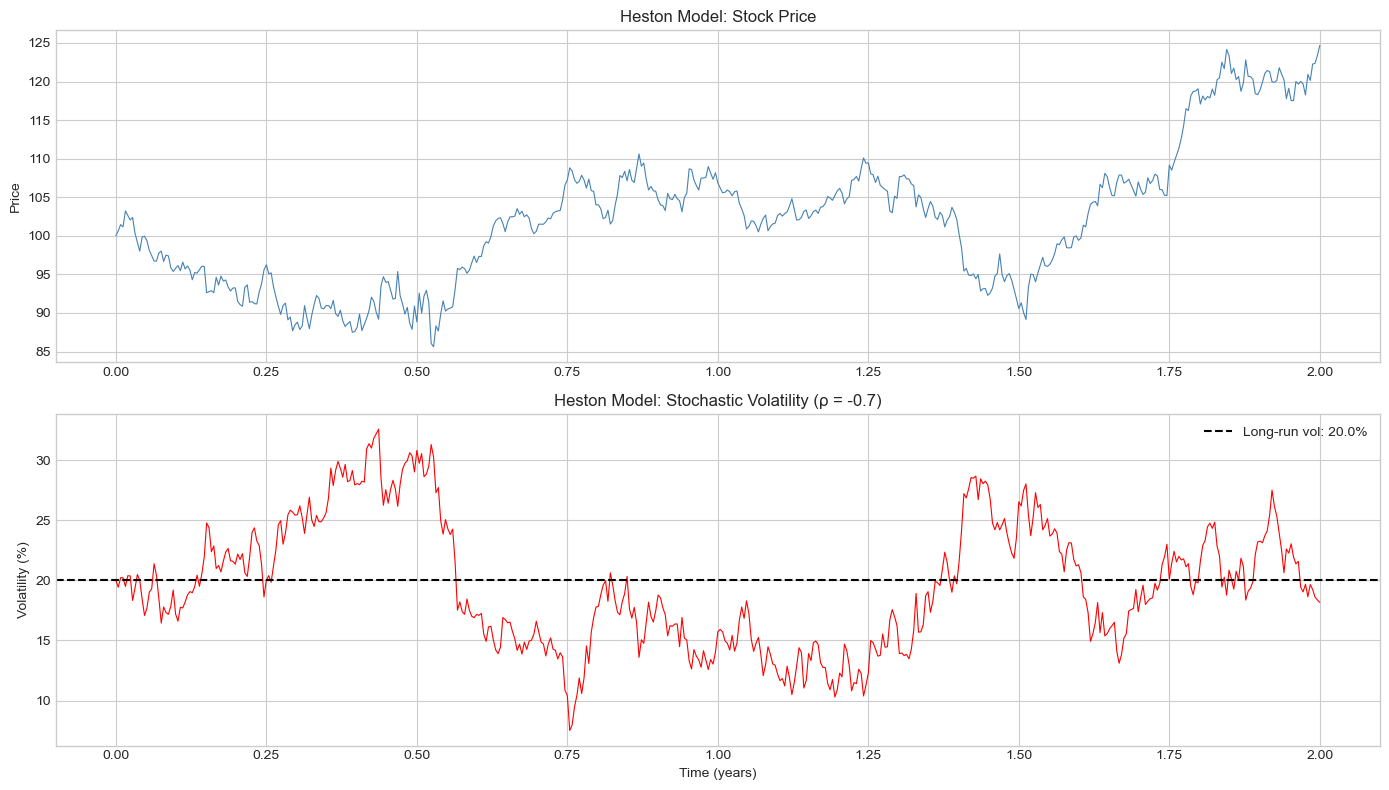

T = 2 # years

n_steps = 252 * 2 # daily

S0, V0 = 100, 0.04 # Initial price and variance

mu = 0.05

kappa = 3.0

theta = 0.04

sigma_v = 0.4

rho = -0.7

# Check Feller condition

feller = 2 * kappa * theta

print(f"Feller condition: 2κθ = {feller:.4f} vs σ²_v = {sigma_v**2:.4f}")

print(f"Condition {'satisfied' if feller > sigma_v**2 else 'VIOLATED'}")

S_heston, V_heston = simulate_heston(T, n_steps, S0, V0, mu, kappa, theta, sigma_v, rho, seed=42)

# Plot

fig, axes = plt.subplots(2, 1, figsize=(14, 8))

t = np.linspace(0, T, n_steps + 1)

axes[0].plot(t, S_heston, color='steelblue', linewidth=0.8)

axes[0].set_ylabel('Price')

axes[0].set_title('Heston Model: Stock Price', fontsize=12)

axes[1].plot(t, np.sqrt(V_heston) * 100, color='red', linewidth=0.8)

axes[1].axhline(np.sqrt(theta) * 100, color='black', linestyle='--',

label=f'Long-run vol: {np.sqrt(theta)*100:.1f}%')

axes[1].set_xlabel('Time (years)')

axes[1].set_ylabel('Volatility (%)')

axes[1].set_title(f'Heston Model: Stochastic Volatility (ρ = {rho})', fontsize=12)

axes[1].legend()

plt.tight_layout()

plt.show()Feller condition: 2κθ = 0.2400 vs σ²_v = 0.1600

Condition satisfied

5. SV with Leverage¶

5.1 Correlated Innovations¶

In discrete time, introduce correlation:

Negative captures the leverage effect: negative returns → higher volatility.

Source

def simulate_sv_leverage(n, mu, phi, sigma_eta, rho, seed=None):

"""SV model with leverage (correlated innovations)."""

if seed is not None:

np.random.seed(seed)

h = np.zeros(n)

y = np.zeros(n)

# Correlated innovations

for t in range(n):

z1 = np.random.standard_normal()

z2 = np.random.standard_normal()

eps = z1

eta = rho * z1 + np.sqrt(1 - rho**2) * z2

if t == 0:

h[t] = mu + sigma_eta * eta / np.sqrt(1 - phi**2)

else:

h[t] = mu + phi * (h[t-1] - mu) + sigma_eta * eta

y[t] = np.exp(h[t] / 2) * eps

return y, h

# Compare with and without leverage

n = 2000

mu, phi, sigma_eta = -10, 0.97, 0.15

y_no_lev, h_no_lev = simulate_sv(n, mu, phi, sigma_eta, seed=42)

y_lev, h_lev = simulate_sv_leverage(n, mu, phi, sigma_eta, rho=-0.5, seed=42)

# Compute correlation of returns with future volatility change

def leverage_correlation(y, h, lag=1):

dh = np.diff(h[lag:])

r = y[:-lag-1]

return np.corrcoef(r, dh)[0, 1]

print("Leverage Effect in SV Models")

print("="*50)

print(f"Corr(r_t, Δh_{{t+1}}) without leverage: {leverage_correlation(y_no_lev, h_no_lev):.4f}")

print(f"Corr(r_t, Δh_{{t+1}}) with leverage (ρ=-0.5): {leverage_correlation(y_lev, h_lev):.4f}")Leverage Effect in SV Models

==================================================

Corr(r_t, Δh_{t+1}) without leverage: 0.0172

Corr(r_t, Δh_{t+1}) with leverage (ρ=-0.5): 0.0326

6. Comparison: SV vs GARCH¶

| Feature | GARCH | Stochastic Volatility |

|---|---|---|

| Volatility dynamics | Deterministic given past | Random (own shock) |

| Estimation | MLE (straightforward) | Challenging (latent state) |

| Option pricing | Requires simulation | Closed-form (Heston) |

| Leverage | GJR-GARCH | Correlated innovations |

| Kurtosis | From GARCH dynamics | Can be more flexible |

7. Summary¶

Key Takeaways¶

Stochastic Volatility has separate randomness for volatility

Heston model is the workhorse continuous-time SV model

QML estimation via log-squared returns transformation

Leverage captured by correlation between return and volatility innovations

Preview: Session 8¶

Rough volatility - fractional Brownian motion in volatility.

Exercises¶

Implement the MCMC (Markov Chain Monte Carlo) estimator for SV

Simulate Heston paths and price a European call option

Compare volatility forecasts from GARCH vs SV

Estimate SV model with leverage on S&P 500 returns

References¶

Taylor, S. J. (1986). Modelling Financial Time Series. Wiley.

Harvey, A., Ruiz, E., & Shephard, N. (1994). Multivariate stochastic variance models. Review of Economic Studies, 61(2), 247-264.

Heston, S. L. (1993). A closed-form solution for options with stochastic volatility. Review of Financial Studies, 6(2), 327-343.