Session 8: Extensions and Special Topics

Event Studies in Finance and Economics - Summer School¶

Learning Objectives¶

By the end of this session, you will be able to:

Handle intraday event studies with high-frequency data

Implement event studies for bonds and other asset classes

Apply event study methods to international/multi-market settings

Use difference-in-differences with event studies

Account for confounding events and event contamination

Implement rolling window and time-varying approaches

1. Introduction: Beyond Standard Event Studies¶

Extensions Covered¶

| Extension | Application | Key Challenge |

|---|---|---|

| Intraday | HFT, news announcements | Microstructure noise |

| Multi-asset | Bonds, options, FX | Different return dynamics |

| International | Cross-border events | Time zones, market linkages |

| Diff-in-Diff | Policy evaluation | Control group selection |

| Confounding events | Earnings + M&A | Isolation of effects |

| Time-varying | Changing market conditions | Parameter instability |

Source

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

from scipy import stats

import yfinance as yf

import statsmodels.api as sm

from datetime import datetime, timedelta

from dataclasses import dataclass

from typing import List, Dict, Optional, Tuple

import warnings

warnings.filterwarnings('ignore')

plt.style.use('seaborn-v0_8-whitegrid')

sns.set_palette("husl")

print("Libraries loaded!")Libraries loaded!

2. Intraday Event Studies¶

When to Use Intraday Data¶

Precise event timing: Fed announcements, earnings releases

High-frequency trading: Algorithmic response to news

Price discovery: How quickly is information incorporated?

Challenges¶

Microstructure noise: Bid-ask bounce, discrete prices

Intraday patterns: U-shaped volatility, lunch effect

Data requirements: Tick or minute-level data

Benchmark selection: Intraday expected returns

Source

def simulate_intraday_data(event_time_minutes: int = 180, # 3 hours into trading

trading_minutes: int = 390, # 6.5 hours

event_impact: float = 0.0005, # 0.05% immediate impact

n_days: int = 5) -> pd.DataFrame:

"""

Simulate intraday price data around an event.

Includes realistic features:

- U-shaped intraday volatility

- Event impact at specific time

- Mean reversion after impact

"""

np.random.seed(42)

all_data = []

base_price = 100

for day in range(-n_days//2, n_days//2 + 1):

# Generate minute-by-minute data

minutes = np.arange(trading_minutes)

# U-shaped volatility pattern

vol_pattern = 0.0002 * (1 + 2*np.exp(-minutes/60) + 2*np.exp(-(trading_minutes-minutes)/60))

# Generate returns

returns = np.random.normal(0, vol_pattern)

# Add event impact on event day

if day == 0:

returns[event_time_minutes] += event_impact

# Slight mean reversion

returns[event_time_minutes+1:event_time_minutes+30] -= event_impact * 0.1 / 30

# Calculate prices

prices = base_price * np.cumprod(1 + returns)

base_price = prices[-1] # Carry to next day

# Create timestamps (9:30 AM start)

date = pd.Timestamp('2023-07-26') + timedelta(days=day)

timestamps = [date + timedelta(hours=9, minutes=30) + timedelta(minutes=int(m))

for m in minutes]

day_df = pd.DataFrame({

'timestamp': timestamps,

'price': prices,

'return': returns,

'day': day,

'minute': minutes

})

all_data.append(day_df)

return pd.concat(all_data, ignore_index=True)

# Simulate intraday data

intraday_data = simulate_intraday_data(event_time_minutes=180, event_impact=0.005)

print(f"Simulated {len(intraday_data)} minute observations")

print(f"Event day data points: {len(intraday_data[intraday_data['day'] == 0])}")Simulated 2340 minute observations

Event day data points: 390

Source

def intraday_event_study(data: pd.DataFrame,

event_minute: int,

pre_minutes: int = 30,

post_minutes: int = 60) -> Dict:

"""

Conduct intraday event study.

Uses pre-event period on same day as benchmark.

"""

event_day = data[data['day'] == 0].copy()

# Pre-event benchmark (e.g., morning before announcement)

pre_event = event_day[(event_day['minute'] >= event_minute - pre_minutes - 60) &

(event_day['minute'] < event_minute - pre_minutes)]

# Expected return per minute (from pre-event period)

expected_return = pre_event['return'].mean()

expected_vol = pre_event['return'].std()

# Event window

event_window = event_day[(event_day['minute'] >= event_minute - pre_minutes) &

(event_day['minute'] <= event_minute + post_minutes)].copy()

# Abnormal returns

event_window['AR'] = event_window['return'] - expected_return

event_window['event_time'] = event_window['minute'] - event_minute

# Cumulative abnormal returns

event_window['CAR'] = event_window['AR'].cumsum()

# Key statistics

car_total = event_window['CAR'].iloc[-1]

car_immediate = event_window[event_window['event_time'] <= 5]['AR'].sum()

# t-statistic (using pre-event volatility)

n_minutes = len(event_window)

car_se = expected_vol * np.sqrt(n_minutes)

t_stat = car_total / car_se if car_se > 0 else 0

return {

'event_window': event_window,

'car_total': car_total,

'car_immediate': car_immediate,

't_stat': t_stat,

'expected_vol': expected_vol

}

# Run intraday event study

intraday_results = intraday_event_study(intraday_data, event_minute=180,

pre_minutes=30, post_minutes=60)

print("Intraday Event Study Results:")

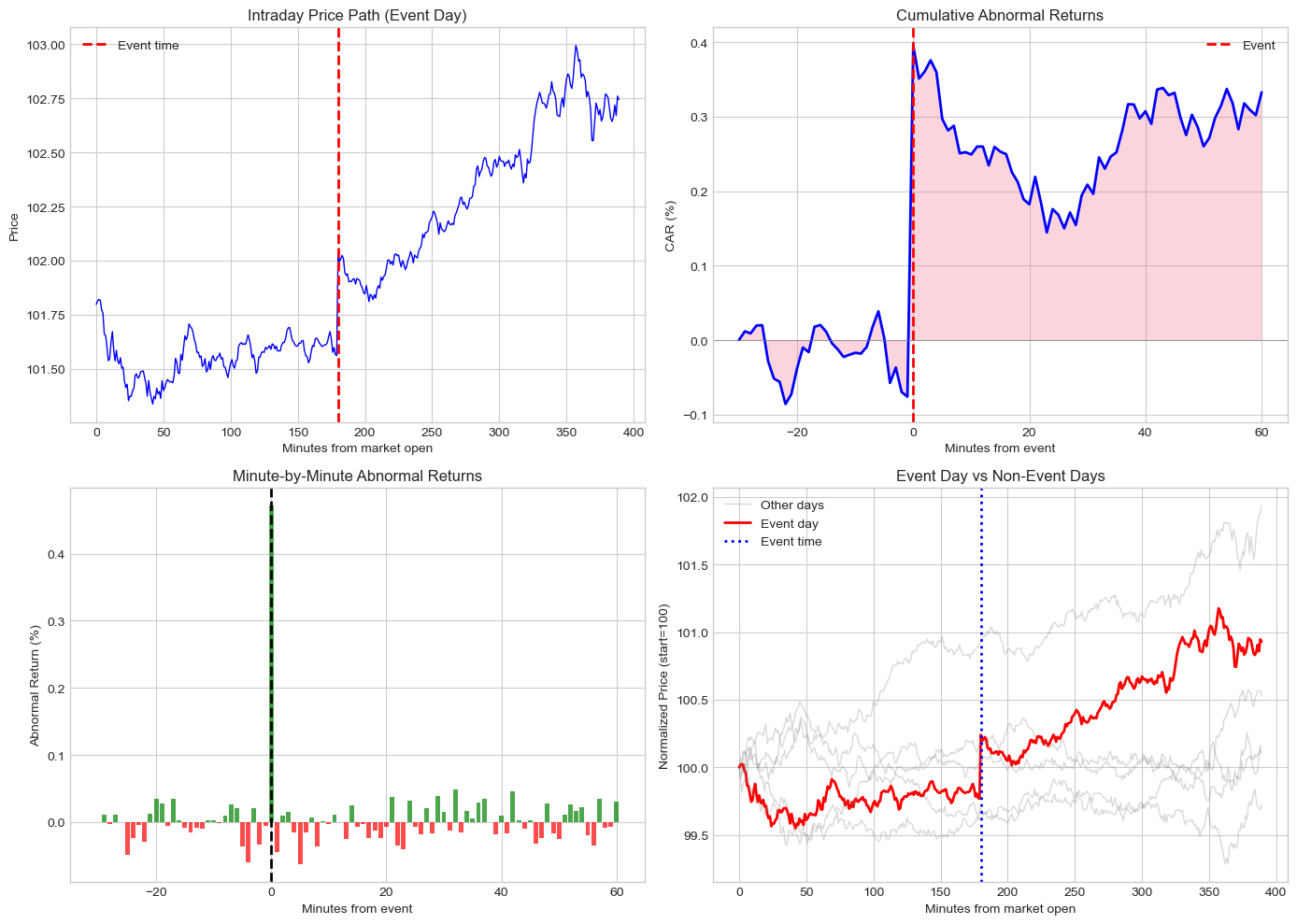

print("="*50)

print(f"Total CAR (30 min pre to 60 min post): {intraday_results['car_total']*100:.3f}%")

print(f"Immediate CAR (0 to +5 min): {intraday_results['car_immediate']*100:.3f}%")

print(f"t-statistic: {intraday_results['t_stat']:.2f}")Intraday Event Study Results:

==================================================

Total CAR (30 min pre to 60 min post): 0.333%

Immediate CAR (0 to +5 min): 0.297%

t-statistic: 1.46

Source

# Visualize intraday event study

fig, axes = plt.subplots(2, 2, figsize=(14, 10))

event_window = intraday_results['event_window']

# Price path on event day

ax1 = axes[0, 0]

event_day = intraday_data[intraday_data['day'] == 0]

ax1.plot(event_day['minute'], event_day['price'], 'b-', linewidth=1)

ax1.axvline(180, color='red', linestyle='--', linewidth=2, label='Event time')

ax1.set_xlabel('Minutes from market open')

ax1.set_ylabel('Price')

ax1.set_title('Intraday Price Path (Event Day)')

ax1.legend()

# Cumulative abnormal returns

ax2 = axes[0, 1]

ax2.plot(event_window['event_time'], event_window['CAR']*100, 'b-', linewidth=2)

ax2.axhline(0, color='gray', linestyle='-', linewidth=0.5)

ax2.axvline(0, color='red', linestyle='--', linewidth=2, label='Event')

ax2.fill_between(event_window['event_time'], 0, event_window['CAR']*100, alpha=0.3)

ax2.set_xlabel('Minutes from event')

ax2.set_ylabel('CAR (%)')

ax2.set_title('Cumulative Abnormal Returns')

ax2.legend()

# Minute-by-minute abnormal returns

ax3 = axes[1, 0]

colors = ['green' if x > 0 else 'red' for x in event_window['AR']]

ax3.bar(event_window['event_time'], event_window['AR']*100, color=colors, alpha=0.7)

ax3.axvline(0, color='black', linestyle='--', linewidth=2)

ax3.set_xlabel('Minutes from event')

ax3.set_ylabel('Abnormal Return (%)')

ax3.set_title('Minute-by-Minute Abnormal Returns')

# Compare event day to non-event days

ax4 = axes[1, 1]

for day in intraday_data['day'].unique():

day_data = intraday_data[intraday_data['day'] == day]

normalized = day_data['price'] / day_data['price'].iloc[0] * 100

color = 'red' if day == 0 else 'gray'

alpha = 1.0 if day == 0 else 0.3

lw = 2 if day == 0 else 1

label = 'Event day' if day == 0 else ('Other days' if day == -2 else None)

ax4.plot(day_data['minute'], normalized, color=color, alpha=alpha, linewidth=lw, label=label)

ax4.axvline(180, color='blue', linestyle=':', linewidth=2, label='Event time')

ax4.set_xlabel('Minutes from market open')

ax4.set_ylabel('Normalized Price (start=100)')

ax4.set_title('Event Day vs Non-Event Days')

ax4.legend()

plt.tight_layout()

plt.show()

3. Multi-Asset Event Studies¶

Beyond Equities¶

Event studies can be applied to:

Corporate bonds: Credit events, rating changes

Options: Implied volatility changes

Foreign exchange: Central bank announcements

Commodities: Supply/demand shocks

Bond Event Study Considerations¶

Illiquidity: Bonds trade less frequently

Duration/convexity: Interest rate sensitivity

Credit spread: Isolate credit-specific effects

Multiple bonds per issuer: Aggregate or analyze separately

Source

def simulate_bond_event_data(n_firms: int = 15,

event_type: str = 'downgrade') -> pd.DataFrame:

"""

Simulate corporate bond event study data.

Models credit spread changes around rating events.

"""

np.random.seed(42)

data = []

for i in range(n_firms):

# Firm characteristics

initial_spread = np.random.uniform(100, 400) # bps

duration = np.random.uniform(3, 10) # years

# Event impact (downgrades increase spreads)

if event_type == 'downgrade':

spread_change = np.random.uniform(20, 80) # bps widening

else: # upgrade

spread_change = np.random.uniform(-60, -10) # bps tightening

# Daily spread changes (21 days: -10 to +10)

for t in range(-10, 11):

noise = np.random.normal(0, 5) # Daily noise

if t == 0: # Event day

spread_delta = spread_change * 0.6 + noise # 60% on event day

elif t == 1: # Day after

spread_delta = spread_change * 0.2 + noise # 20% drift

elif t == 2:

spread_delta = spread_change * 0.1 + noise # 10% more drift

else:

spread_delta = noise

# Bond return approximation: -duration * spread_change / 10000

bond_return = -duration * spread_delta / 10000

data.append({

'firm_id': i,

'event_time': t,

'spread_change': spread_delta,

'bond_return': bond_return,

'duration': duration,

'initial_spread': initial_spread

})

return pd.DataFrame(data)

# Simulate bond data

bond_data = simulate_bond_event_data(n_firms=15, event_type='downgrade')

print(f"Simulated {len(bond_data)} bond-day observations for {bond_data['firm_id'].nunique()} firms")Simulated 315 bond-day observations for 15 firms

Source

def bond_event_study(data: pd.DataFrame) -> Dict:

"""

Analyze bond market response to credit events.

"""

# Average spread change by event time

avg_by_time = data.groupby('event_time').agg({

'spread_change': ['mean', 'std', 'count'],

'bond_return': ['mean', 'std']

})

avg_by_time.columns = ['spread_mean', 'spread_std', 'n', 'return_mean', 'return_std']

avg_by_time = avg_by_time.reset_index()

# Cumulative spread change

avg_by_time['cum_spread'] = avg_by_time['spread_mean'].cumsum()

avg_by_time['cum_return'] = avg_by_time['return_mean'].cumsum()

# Standard errors

avg_by_time['spread_se'] = avg_by_time['spread_std'] / np.sqrt(avg_by_time['n'])

# t-statistics

avg_by_time['t_stat'] = avg_by_time['spread_mean'] / avg_by_time['spread_se']

# Windows

windows = {

'(0,0)': data[data['event_time'] == 0]['spread_change'].values,

'(-1,+1)': data[data['event_time'].between(-1, 1)].groupby('firm_id')['spread_change'].sum().values,

'(0,+5)': data[data['event_time'].between(0, 5)].groupby('firm_id')['spread_change'].sum().values,

}

window_stats = {}

for name, values in windows.items():

t, p = stats.ttest_1samp(values, 0)

window_stats[name] = {

'mean': np.mean(values),

'std': np.std(values),

't_stat': t,

'p_value': p

}

return {

'time_series': avg_by_time,

'window_stats': window_stats

}

bond_results = bond_event_study(bond_data)

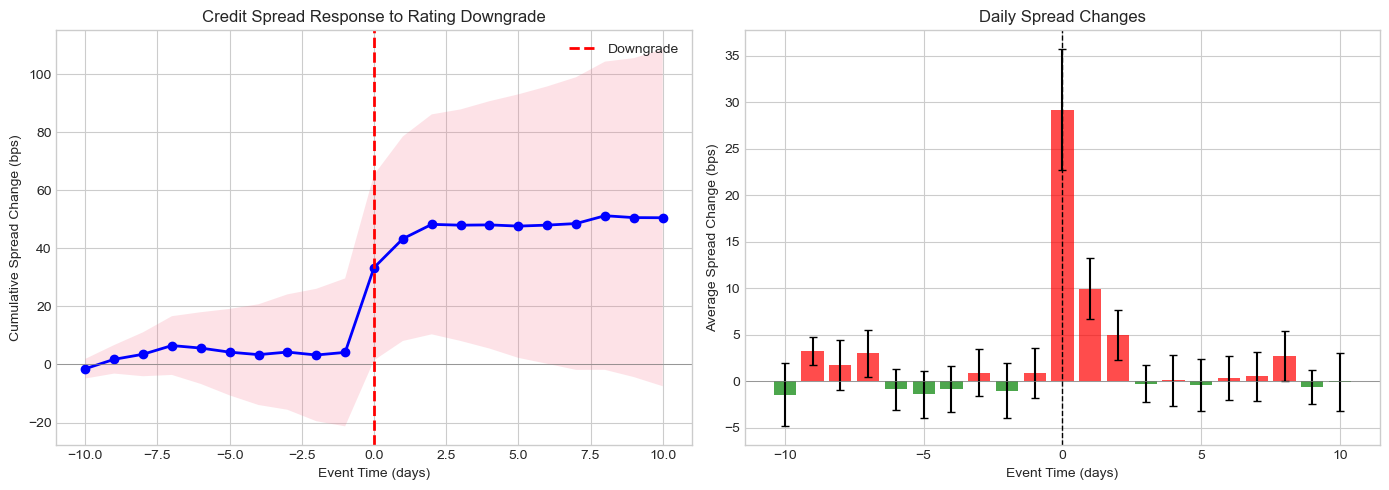

print("Bond Event Study: Credit Rating Downgrade")

print("="*60)

print("\nCumulative Spread Change by Window (bps):")

print("-"*60)

for window, stats_dict in bond_results['window_stats'].items():

sig = '***' if stats_dict['p_value'] < 0.01 else '**' if stats_dict['p_value'] < 0.05 else '*' if stats_dict['p_value'] < 0.10 else ''

print(f" {window}: {stats_dict['mean']:+.1f} bps (t={stats_dict['t_stat']:.2f}{sig})")Bond Event Study: Credit Rating Downgrade

============================================================

Cumulative Spread Change by Window (bps):

------------------------------------------------------------

(0,0): +29.2 bps (t=8.84***)

(-1,+1): +40.1 bps (t=8.66***)

(0,+5): +43.5 bps (t=6.56***)

Source

# Visualize bond event study

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

ts = bond_results['time_series']

# Cumulative spread change

ax1 = axes[0]

ax1.plot(ts['event_time'], ts['cum_spread'], 'b-', linewidth=2, marker='o')

ax1.fill_between(ts['event_time'],

ts['cum_spread'] - 1.96*ts['spread_se'].cumsum(),

ts['cum_spread'] + 1.96*ts['spread_se'].cumsum(),

alpha=0.2)

ax1.axhline(0, color='gray', linestyle='-', linewidth=0.5)

ax1.axvline(0, color='red', linestyle='--', linewidth=2, label='Downgrade')

ax1.set_xlabel('Event Time (days)')

ax1.set_ylabel('Cumulative Spread Change (bps)')

ax1.set_title('Credit Spread Response to Rating Downgrade')

ax1.legend()

# Daily spread changes

ax2 = axes[1]

colors = ['red' if x > 0 else 'green' for x in ts['spread_mean']]

ax2.bar(ts['event_time'], ts['spread_mean'], color=colors, alpha=0.7,

yerr=ts['spread_se']*1.96, capsize=3)

ax2.axhline(0, color='gray', linestyle='-', linewidth=0.5)

ax2.axvline(0, color='black', linestyle='--', linewidth=1)

ax2.set_xlabel('Event Time (days)')

ax2.set_ylabel('Average Spread Change (bps)')

ax2.set_title('Daily Spread Changes')

plt.tight_layout()

plt.show()

4. International Event Studies¶

Challenges¶

Time zones: Events occur at different local times

Non-synchronous trading: Markets open/close at different times

Currency effects: Local vs USD returns

Market linkages: Spillovers across markets

Handling Time Zones¶

Define event day based on market where event occurs

Account for information transmission delays

Consider overnight returns for earlier markets

Source

def download_international_data(tickers: Dict[str, str],

start_date: str,

end_date: str) -> pd.DataFrame:

"""

Download international stock data.

Args:

tickers: Dict mapping market name to ticker symbol

"""

data = {}

for market, ticker in tickers.items():

try:

prices = yf.download(ticker, start=start_date, end=end_date, progress=False)['Close']

data[market] = prices.squeeze().pct_change()

except Exception as e:

print(f"Failed to download {market}: {e}")

df = pd.DataFrame(data).dropna()

return df

# International indices

international_tickers = {

'US': '^GSPC', # S&P 500

'Europe': '^STOXX50E', # Euro Stoxx 50

'UK': '^FTSE', # FTSE 100

'Japan': '^N225', # Nikkei 225

'China': '000001.SS', # Shanghai Composite

}

print("Downloading international market data...")

intl_data = download_international_data(international_tickers, '2022-01-01', '2023-12-31')

print(f"Downloaded {len(intl_data)} trading days for {len(intl_data.columns)} markets")Downloading international market data...

Downloaded 428 trading days for 5 markets

Source

def international_event_study(data: pd.DataFrame,

event_date: str,

event_market: str,

estimation_window: int = 120,

event_window: Tuple[int, int] = (-5, 5)) -> Dict:

"""

Study international market response to event.

Estimates market model for each market using event market as benchmark.

"""

event_dt = pd.to_datetime(event_date)

# Find event date in data

if event_dt not in data.index:

idx = data.index.get_indexer([event_dt], method='nearest')[0]

event_dt = data.index[idx]

event_idx = data.index.get_loc(event_dt)

results = {}

for market in data.columns:

if market == event_market:

continue

# Estimation period

est_start = max(0, event_idx - estimation_window - 10)

est_end = event_idx - 10

est_data = data.iloc[est_start:est_end]

# Market model: R_market = alpha + beta * R_event_market

y = est_data[market].dropna()

x = est_data[event_market].loc[y.index]

if len(y) < 30:

continue

X = sm.add_constant(x)

model = sm.OLS(y, X).fit()

# Event window

evt_start = event_idx + event_window[0]

evt_end = event_idx + event_window[1] + 1

evt_data = data.iloc[evt_start:evt_end].copy()

# Abnormal returns

expected = model.params['const'] + model.params[event_market] * evt_data[event_market]

ar = evt_data[market] - expected

car = ar.cumsum()

# Statistics

sigma = np.std(model.resid)

car_total = car.iloc[-1] if len(car) > 0 else np.nan

t_stat = car_total / (sigma * np.sqrt(len(ar))) if sigma > 0 and len(ar) > 0 else np.nan

results[market] = {

'beta': model.params[event_market],

'ar_series': ar,

'car_series': car,

'car_total': car_total,

't_stat': t_stat,

'sigma': sigma

}

return results

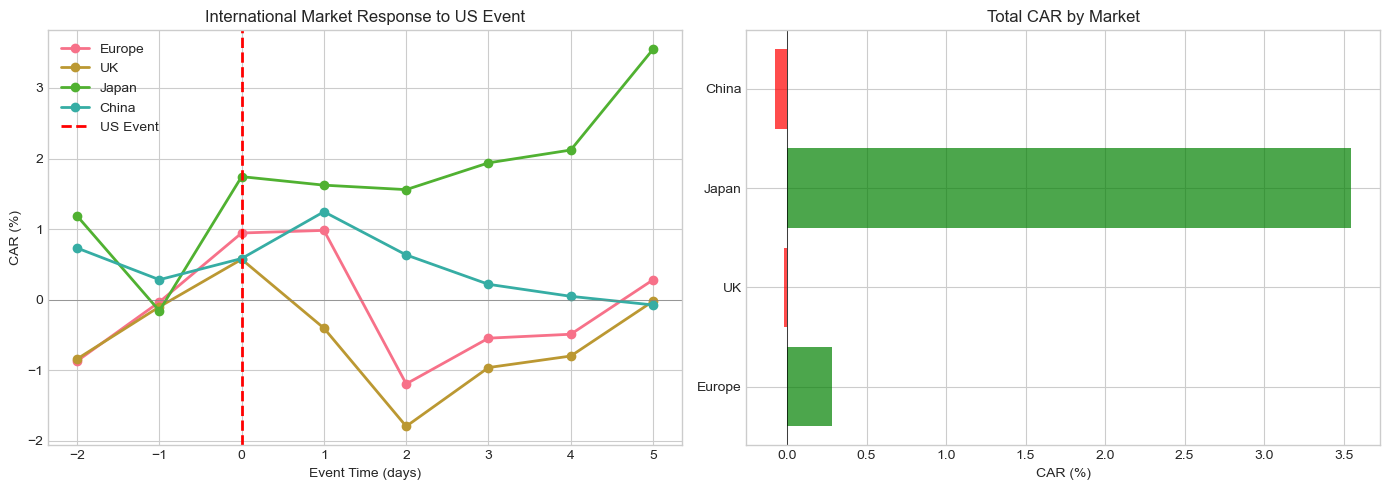

# Study US Fed announcement spillovers (example date)

fed_event = '2023-03-22' # FOMC meeting

intl_results = international_event_study(intl_data, fed_event, 'US',

estimation_window=120, event_window=(-2, 5))

print(f"\nInternational Spillovers from US Event ({fed_event}):")

print("="*70)

print(f"{'Market':<15} {'Beta':>10} {'CAR':>12} {'t-stat':>10}")

print("-"*70)

for market, stats in intl_results.items():

if not np.isnan(stats['car_total']):

sig = '***' if abs(stats['t_stat']) > 2.58 else '**' if abs(stats['t_stat']) > 1.96 else '*' if abs(stats['t_stat']) > 1.65 else ''

print(f"{market:<15} {stats['beta']:>10.3f} {stats['car_total']*100:>+11.2f}% {stats['t_stat']:>8.2f}{sig}")

International Spillovers from US Event (2023-03-22):

======================================================================

Market Beta CAR t-stat

----------------------------------------------------------------------

Europe 0.450 +0.28% 0.12

UK 0.182 -0.02% -0.01

Japan -0.043 +3.55% 1.16

China -0.017 -0.07% -0.03

Source

# Visualize international spillovers

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

# CAR paths

ax1 = axes[0]

for market, stats in intl_results.items():

if not stats['car_series'].empty:

event_time = range(-2, -2 + len(stats['car_series']))

ax1.plot(event_time, stats['car_series']*100, marker='o', label=market, linewidth=2)

ax1.axhline(0, color='gray', linestyle='-', linewidth=0.5)

ax1.axvline(0, color='red', linestyle='--', linewidth=2, label='US Event')

ax1.set_xlabel('Event Time (days)')

ax1.set_ylabel('CAR (%)')

ax1.set_title('International Market Response to US Event')

ax1.legend()

# Bar chart of total CARs

ax2 = axes[1]

markets = [m for m in intl_results.keys() if not np.isnan(intl_results[m]['car_total'])]

cars = [intl_results[m]['car_total']*100 for m in markets]

colors = ['green' if c > 0 else 'red' for c in cars]

ax2.barh(markets, cars, color=colors, alpha=0.7)

ax2.axvline(0, color='black', linestyle='-', linewidth=0.5)

ax2.set_xlabel('CAR (%)')

ax2.set_title('Total CAR by Market')

plt.tight_layout()

plt.show()

5. Difference-in-Differences Event Study¶

Concept¶

Combine event study with diff-in-diff to:

Compare treated vs control firms

Account for common time trends

Identify causal effects of policies/regulations

Model¶

: Difference-in-differences estimate (causal effect)

Source

def simulate_did_data(n_treated: int = 20,

n_control: int = 30,

treatment_effect: float = 0.02,

pre_periods: int = 60,

post_periods: int = 60) -> pd.DataFrame:

"""

Simulate data for difference-in-differences event study.

"""

np.random.seed(42)

data = []

# Common time trend

time_trend = np.concatenate([

np.linspace(0, 0.001, pre_periods),

np.linspace(0.001, 0.002, post_periods)

])

for i in range(n_treated + n_control):

treated = i < n_treated

firm_fe = np.random.normal(0, 0.001) # Firm fixed effect

for t in range(-pre_periods, post_periods):

post = t >= 0

# Base return

ret = firm_fe + time_trend[t + pre_periods]

# Add noise

ret += np.random.normal(0, 0.02)

# Treatment effect (only for treated firms after event)

if treated and post:

# Gradual effect

effect_strength = min(t / 20, 1) # Ramp up over 20 days

ret += treatment_effect * effect_strength / post_periods

data.append({

'firm_id': i,

'treated': treated,

'event_time': t,

'post': post,

'return': ret

})

return pd.DataFrame(data)

# Simulate DiD data

did_data = simulate_did_data(n_treated=20, n_control=30, treatment_effect=0.03)

print(f"Simulated {len(did_data)} firm-day observations")

print(f"Treated firms: {did_data[did_data['treated']]['firm_id'].nunique()}")

print(f"Control firms: {did_data[~did_data['treated']]['firm_id'].nunique()}")Simulated 6000 firm-day observations

Treated firms: 20

Control firms: 30

Source

def diff_in_diff_event_study(data: pd.DataFrame) -> Dict:

"""

Run difference-in-differences event study.

"""

# Create interaction term

data = data.copy()

data['treated_post'] = data['treated'].astype(int) * data['post'].astype(int)

# DiD regression

y = data['return']

X = sm.add_constant(data[['post', 'treated', 'treated_post']].astype(float))

model = sm.OLS(y, X).fit(cov_type='cluster', cov_kwds={'groups': data['firm_id']})

# Calculate cumulative returns by group

cum_returns = data.groupby(['event_time', 'treated']).agg({

'return': 'mean'

}).reset_index()

cum_returns['cum_return'] = cum_returns.groupby('treated')['return'].cumsum()

return {

'model': model,

'did_estimate': model.params['treated_post'],

'did_se': model.bse['treated_post'],

'did_tstat': model.tvalues['treated_post'],

'did_pvalue': model.pvalues['treated_post'],

'cum_returns': cum_returns

}

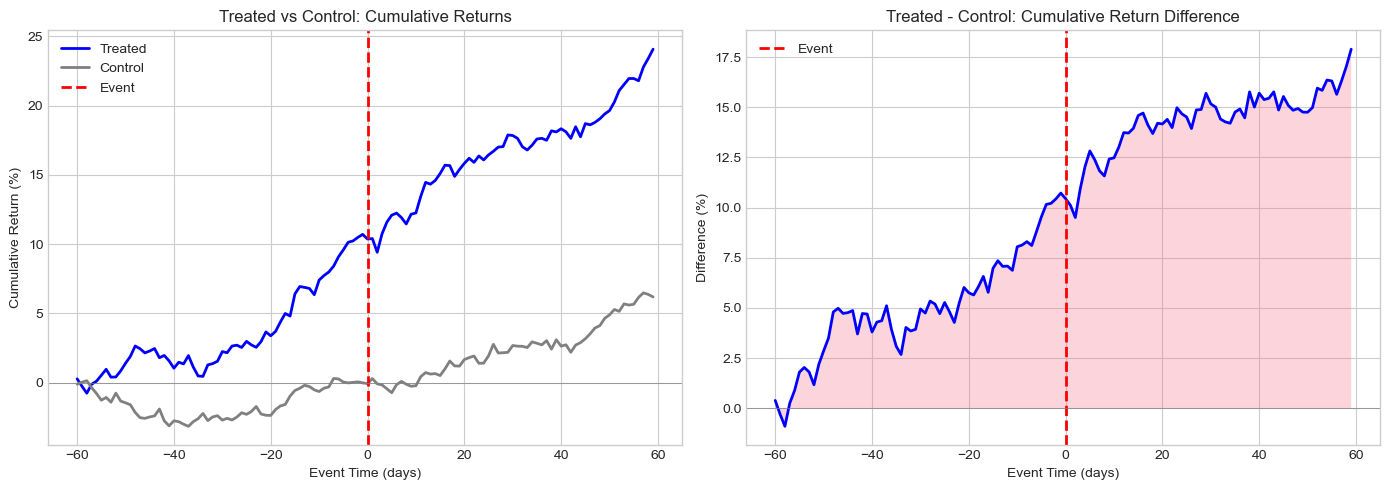

did_results = diff_in_diff_event_study(did_data)

print("Difference-in-Differences Event Study Results:")

print("="*60)

print(f"\nDiD Estimate (β₃): {did_results['did_estimate']*100:.4f}%")

print(f"Clustered SE: {did_results['did_se']*100:.4f}%")

print(f"t-statistic: {did_results['did_tstat']:.2f}")

print(f"p-value: {did_results['did_pvalue']:.4f}")

print("\n" + "="*60)

print("Full Regression Results:")

print(did_results['model'].summary().tables[1])Difference-in-Differences Event Study Results:

============================================================

DiD Estimate (β₃): -0.0592%

Clustered SE: 0.1043%

t-statistic: -0.57

p-value: 0.5705

============================================================

Full Regression Results:

================================================================================

coef std err z P>|z| [0.025 0.975]

--------------------------------------------------------------------------------

const -2.613e-06 0.000 -0.006 0.995 -0.001 0.001

post 0.0010 0.001 1.867 0.062 -5.16e-05 0.002

treated 0.0018 0.001 2.305 0.021 0.000 0.003

treated_post -0.0006 0.001 -0.567 0.570 -0.003 0.001

================================================================================

Source

# Visualize DiD

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

cum_ret = did_results['cum_returns']

# Cumulative returns by group

ax1 = axes[0]

for treated in [True, False]:

group_data = cum_ret[cum_ret['treated'] == treated]

label = 'Treated' if treated else 'Control'

color = 'blue' if treated else 'gray'

ax1.plot(group_data['event_time'], group_data['cum_return']*100,

label=label, color=color, linewidth=2)

ax1.axvline(0, color='red', linestyle='--', linewidth=2, label='Event')

ax1.axhline(0, color='gray', linestyle='-', linewidth=0.5)

ax1.set_xlabel('Event Time (days)')

ax1.set_ylabel('Cumulative Return (%)')

ax1.set_title('Treated vs Control: Cumulative Returns')

ax1.legend()

# Difference (treated - control)

ax2 = axes[1]

treated_cum = cum_ret[cum_ret['treated'] == True].set_index('event_time')['cum_return']

control_cum = cum_ret[cum_ret['treated'] == False].set_index('event_time')['cum_return']

diff = (treated_cum - control_cum) * 100

ax2.plot(diff.index, diff.values, 'b-', linewidth=2)

ax2.fill_between(diff.index, 0, diff.values, alpha=0.3)

ax2.axvline(0, color='red', linestyle='--', linewidth=2, label='Event')

ax2.axhline(0, color='gray', linestyle='-', linewidth=0.5)

ax2.set_xlabel('Event Time (days)')

ax2.set_ylabel('Difference (%)')

ax2.set_title('Treated - Control: Cumulative Return Difference')

ax2.legend()

plt.tight_layout()

plt.show()

6. Confounding Events¶

The Problem¶

Multiple events may occur around the same time:

Earnings + M&A announcement

Dividend + stock split

Multiple news items on same day

Solutions¶

Exclusion: Remove contaminated observations

Indicator variables: Control for confounding events

Shorter windows: Reduce chance of contamination

Event-specific analysis: Separate the effects

Source

def simulate_confounded_events(n_events: int = 50,

pct_confounded: float = 0.3) -> pd.DataFrame:

"""

Simulate event study with confounding events.

"""

np.random.seed(42)

data = []

for i in range(n_events):

# Primary event effect

primary_effect = np.random.normal(0.02, 0.01)

# Is there a confounding event?

confounded = np.random.random() < pct_confounded

confound_effect = np.random.normal(0.01, 0.02) if confounded else 0

# Generate CAR

noise = np.random.normal(0, 0.03)

car = primary_effect + confound_effect + noise

data.append({

'event_id': i,

'CAR': car,

'confounded': confounded,

'primary_effect': primary_effect,

'confound_effect': confound_effect

})

return pd.DataFrame(data)

# Simulate data

confound_data = simulate_confounded_events(n_events=50, pct_confounded=0.3)

print("Confounding Events Analysis:")

print("="*60)

print(f"Total events: {len(confound_data)}")

print(f"Confounded events: {confound_data['confounded'].sum()} ({confound_data['confounded'].mean()*100:.0f}%)")Confounding Events Analysis:

============================================================

Total events: 50

Confounded events: 17 (34%)

Source

# Compare analysis with and without confounding adjustment

print("\nAnalysis Comparison:")

print("-"*60)

# Full sample

full_mean = confound_data['CAR'].mean()

full_t, full_p = stats.ttest_1samp(confound_data['CAR'], 0)

print(f"\n1. Full Sample (N={len(confound_data)}):")

print(f" Mean CAR: {full_mean*100:.2f}%")

print(f" t-stat: {full_t:.2f} (p={full_p:.4f})")

# Exclude confounded

clean = confound_data[~confound_data['confounded']]

clean_mean = clean['CAR'].mean()

clean_t, clean_p = stats.ttest_1samp(clean['CAR'], 0)

print(f"\n2. Excluding Confounded (N={len(clean)}):")

print(f" Mean CAR: {clean_mean*100:.2f}%")

print(f" t-stat: {clean_t:.2f} (p={clean_p:.4f})")

# Regression with indicator

y = confound_data['CAR']

X = sm.add_constant(confound_data['confounded'].astype(float))

model = sm.OLS(y, X).fit()

print(f"\n3. Regression with Confound Indicator:")

print(f" Intercept (clean events): {model.params['const']*100:.2f}%")

print(f" Confound effect: {model.params['confounded']*100:+.2f}%")

print(f" t-stat (intercept): {model.tvalues['const']:.2f}")

Analysis Comparison:

------------------------------------------------------------

---------------------------------------------------------------------------

AttributeError Traceback (most recent call last)

Cell In[63], line 7

5 # Full sample

6 full_mean = confound_data['CAR'].mean()

----> 7 full_t, full_p = stats.ttest_1samp(confound_data['CAR'], 0)

8 print(f"\n1. Full Sample (N={len(confound_data)}):")

9 print(f" Mean CAR: {full_mean*100:.2f}%")

AttributeError: 'dict' object has no attribute 'ttest_1samp'Source

# Visualize confounding

fig, axes = plt.subplots(1, 2, figsize=(12, 5))

# Distribution by confound status

ax1 = axes[0]

ax1.hist(confound_data[~confound_data['confounded']]['CAR']*100, bins=15, alpha=0.7,

label='Clean', color='blue', edgecolor='black')

ax1.hist(confound_data[confound_data['confounded']]['CAR']*100, bins=15, alpha=0.7,

label='Confounded', color='red', edgecolor='black')

ax1.axvline(0, color='black', linestyle='--', linewidth=1)

ax1.set_xlabel('CAR (%)')

ax1.set_ylabel('Frequency')

ax1.set_title('CAR Distribution by Confound Status')

ax1.legend()

# Box plot comparison

ax2 = axes[1]

bp = ax2.boxplot([confound_data[~confound_data['confounded']]['CAR']*100,

confound_data[confound_data['confounded']]['CAR']*100],

labels=['Clean', 'Confounded'],

patch_artist=True)

bp['boxes'][0].set_facecolor('blue')

bp['boxes'][1].set_facecolor('red')

for box in bp['boxes']:

box.set_alpha(0.6)

ax2.axhline(0, color='gray', linestyle='--', linewidth=1)

ax2.set_ylabel('CAR (%)')

ax2.set_title('CAR by Confound Status')

plt.tight_layout()

plt.show()7. Rolling Window Event Studies¶

Motivation¶

Market conditions change over time:

Beta may be time-varying

Volatility regimes shift

Market efficiency may evolve

Rolling Estimation¶

Instead of fixed estimation window, use rolling parameters:

Source

def rolling_event_study(ticker: str,

event_dates: List[str],

rolling_window: int = 60,

event_window: Tuple[int, int] = (-1, 1)) -> pd.DataFrame:

"""

Event study with rolling parameter estimation.

"""

# Download data

start = pd.to_datetime(min(event_dates)) - timedelta(days=rolling_window*2)

end = pd.to_datetime(max(event_dates)) + timedelta(days=30)

stock = yf.download(ticker, start=start, end=end, progress=False)['Close']

market = yf.download('^GSPC', start=start, end=end, progress=False)['Close']

df = pd.DataFrame({'stock': stock.squeeze(), 'market': market.squeeze()})

df['stock_ret'] = df['stock'].pct_change()

df['market_ret'] = df['market'].pct_change()

df = df.dropna()

# Rolling beta estimation

def rolling_beta(window):

if len(window) < 20:

return np.nan

cov = np.cov(window['stock_ret'], window['market_ret'])[0, 1]

var = np.var(window['market_ret'])

return cov / var if var > 0 else np.nan

df['rolling_beta'] = df['stock_ret'].rolling(rolling_window).apply(

lambda x: np.cov(x, df.loc[x.index, 'market_ret'])[0, 1] / np.var(df.loc[x.index, 'market_ret'])

if len(x) >= 20 else np.nan

)

# Simple rolling beta calculation

betas = []

for i in range(len(df)):

if i < rolling_window:

betas.append(np.nan)

else:

window = df.iloc[i-rolling_window:i]

cov = np.cov(window['stock_ret'], window['market_ret'])[0, 1]

var = np.var(window['market_ret'])

betas.append(cov / var if var > 0 else np.nan)

df['rolling_beta'] = betas

# Process events

results = []

for event_date in event_dates:

event_dt = pd.to_datetime(event_date)

if event_dt not in df.index:

idx = df.index.get_indexer([event_dt], method='nearest')[0]

if idx < 0:

continue

event_dt = df.index[idx]

event_idx = df.index.get_loc(event_dt)

# Get rolling beta at event time

beta = df.iloc[event_idx]['rolling_beta']

if np.isnan(beta):

continue

# Calculate CAR using rolling beta

car = 0

for t in range(event_window[0], event_window[1] + 1):

idx = event_idx + t

if 0 <= idx < len(df):

expected = beta * df.iloc[idx]['market_ret']

ar = df.iloc[idx]['stock_ret'] - expected

car += ar

results.append({

'event_date': event_dt,

'rolling_beta': beta,

'CAR': car

})

return pd.DataFrame(results), df

# Example: Multiple earnings announcements for one stock

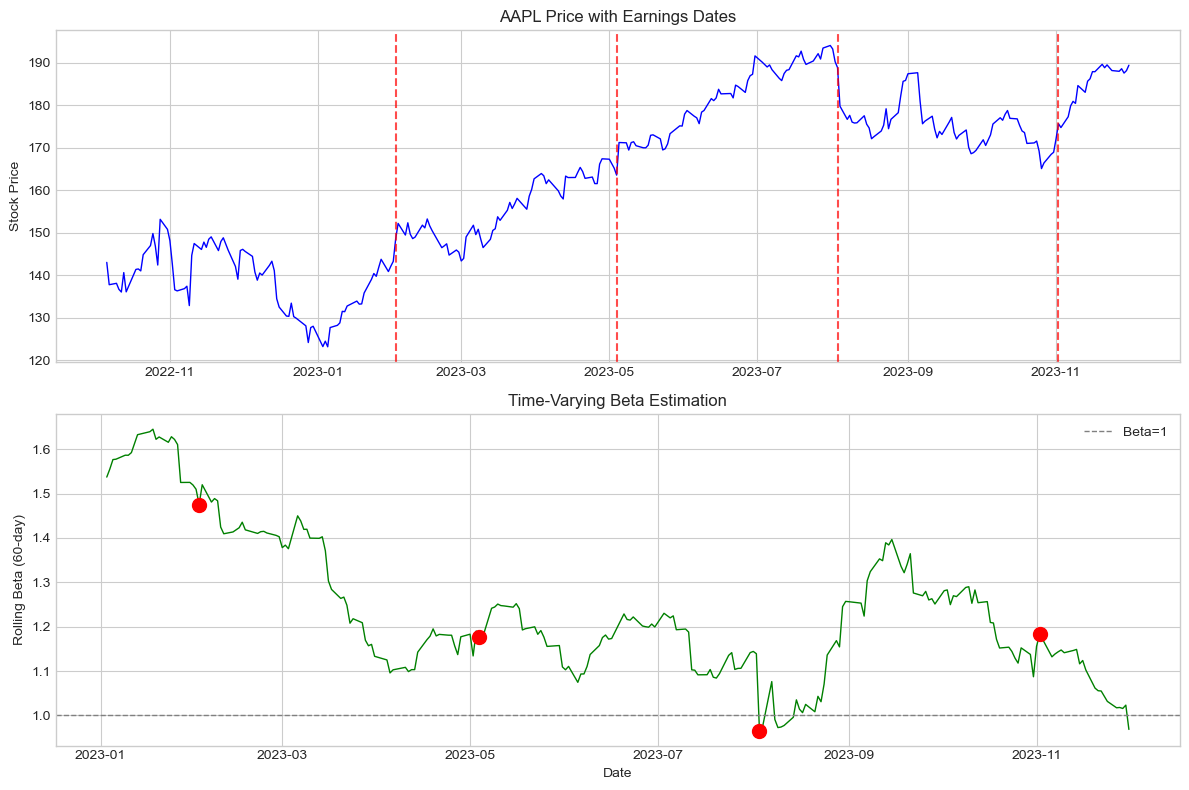

aapl_events = ['2023-02-02', '2023-05-04', '2023-08-03', '2023-11-02']

rolling_results, price_data = rolling_event_study('AAPL', aapl_events,

rolling_window=60,

event_window=(-1, 1))

print("Rolling Window Event Study Results:")

print("="*60)

print(rolling_results.to_string())Rolling Window Event Study Results:

============================================================

event_date rolling_beta CAR

0 2023-02-02 1.475314 0.047533

1 2023-05-04 1.175724 0.025540

2 2023-08-03 0.965858 -0.049885

3 2023-11-02 1.182602 -0.011585

Source

# Visualize rolling beta

fig, axes = plt.subplots(2, 1, figsize=(12, 8))

# Price and events

ax1 = axes[0]

ax1.plot(price_data.index, price_data['stock'], 'b-', linewidth=1)

for date in rolling_results['event_date']:

ax1.axvline(date, color='red', linestyle='--', alpha=0.7)

ax1.set_ylabel('Stock Price')

ax1.set_title('AAPL Price with Earnings Dates')

# Rolling beta

ax2 = axes[1]

ax2.plot(price_data.index, price_data['rolling_beta'], 'g-', linewidth=1)

for _, row in rolling_results.iterrows():

ax2.scatter(row['event_date'], row['rolling_beta'], color='red', s=100, zorder=5)

ax2.axhline(1, color='gray', linestyle='--', linewidth=1, label='Beta=1')

ax2.set_ylabel('Rolling Beta (60-day)')

ax2.set_xlabel('Date')

ax2.set_title('Time-Varying Beta Estimation')

ax2.legend()

plt.tight_layout()

plt.show()

8. Event Study with Machine Learning Benchmarks¶

Alternative Expected Return Models¶

Beyond CAPM and Fama-French:

LASSO/Ridge regression: Many potential factors

Random forests: Non-linear relationships

Neural networks: Complex patterns

Caution¶

Overfitting risk

Interpretability concerns

May not improve inference

Source

from sklearn.linear_model import LassoCV, RidgeCV

from sklearn.ensemble import RandomForestRegressor

from sklearn.preprocessing import StandardScaler

def ml_expected_returns(estimation_data: pd.DataFrame,

event_data: pd.DataFrame,

method: str = 'lasso') -> np.ndarray:

"""

Estimate expected returns using ML methods.

Uses lagged returns as features (simple demonstration).

"""

# Create features (lagged returns)

def create_features(data, lags=5):

features = pd.DataFrame(index=data.index)

for lag in range(1, lags + 1):

features[f'lag_{lag}'] = data['stock_ret'].shift(lag)

features[f'market_lag_{lag}'] = data['market_ret'].shift(lag)

features['market_current'] = data['market_ret']

return features.dropna()

est_features = create_features(estimation_data)

est_y = estimation_data.loc[est_features.index, 'stock_ret']

# Scale features

scaler = StandardScaler()

X_train = scaler.fit_transform(est_features)

# Fit model

if method == 'lasso':

model = LassoCV(cv=5, random_state=42)

elif method == 'ridge':

model = RidgeCV(cv=5)

elif method == 'rf':

model = RandomForestRegressor(n_estimators=100, max_depth=5, random_state=42)

model.fit(X_train, est_y)

# Predict for event window

evt_features = create_features(event_data)

if len(evt_features) == 0:

return np.array([])

X_test = scaler.transform(evt_features)

predictions = model.predict(X_test)

return predictions, evt_features.index

# Demonstrate with synthetic data

print("ML-Based Expected Returns (Demonstration):")

print("="*60)

print("\nNote: This is a simplified demonstration. In practice:")

print("- Use more sophisticated features (factors, technical indicators)")

print("- Careful cross-validation to avoid look-ahead bias")

print("- Consider economic interpretability")ML-Based Expected Returns (Demonstration):

============================================================

Note: This is a simplified demonstration. In practice:

- Use more sophisticated features (factors, technical indicators)

- Careful cross-validation to avoid look-ahead bias

- Consider economic interpretability

9. Publication-Quality Reporting¶

Best Practices¶

Clearly state methodology: Window length, benchmark, test statistics

Report multiple windows: Robustness across specifications

Show distributions: Not just means and t-stats

Address clustering: If events overlap in time

Discuss economic significance: Not just statistical

Source

def create_publication_table(results_dict: Dict, title: str) -> str:

"""

Create publication-quality LaTeX table.

"""

latex = f"""\n

\\begin{{table}}[htbp]

\\centering

\\caption{{{title}}}

\\begin{{tabular}}{{lccccc}}

\\hline\\hline

Window & N & Mean CAR & Median CAR & t-stat & \\% Positive \\\\

\\hline

"""

for window, stats in results_dict.items():

sig = '$^{***}$' if stats['p'] < 0.01 else '$^{**}$' if stats['p'] < 0.05 else '$^{*}$' if stats['p'] < 0.10 else ''

latex += f"{window} & {stats['n']} & {stats['mean']*100:.2f}\\%{sig} & {stats['median']*100:.2f}\\% & {stats['t']:.2f} & {stats['pct_pos']:.0f}\\% \\\\\n"

latex += """\\hline\\hline

\\end{tabular}

\\begin{tablenotes}

\\small

\\item Notes: $^{***}$, $^{**}$, $^{*}$ indicate significance at 1\\%, 5\\%, 10\\% levels.

\\end{tablenotes}

\\end{table}

"""

return latex

# Example results

example_results = {

'(-1, +1)': {'n': 50, 'mean': 0.025, 'median': 0.020, 't': 3.45, 'p': 0.001, 'pct_pos': 72},

'(0, 0)': {'n': 50, 'mean': 0.018, 'median': 0.015, 't': 2.89, 'p': 0.006, 'pct_pos': 68},

'(-5, +5)': {'n': 50, 'mean': 0.032, 'median': 0.028, 't': 2.15, 'p': 0.036, 'pct_pos': 64},

}

latex_table = create_publication_table(example_results, "Abnormal Returns Around Event")

print("LaTeX Table Code:")

print(latex_table)LaTeX Table Code:

\begin{table}[htbp]

\centering

\caption{Abnormal Returns Around Event}

\begin{tabular}{lccccc}

\hline\hline

Window & N & Mean CAR & Median CAR & t-stat & \% Positive \\

\hline

(-1, +1) & 50 & 2.50\%$^{***}$ & 2.00\% & 3.45 & 72\% \\

(0, 0) & 50 & 1.80\%$^{***}$ & 1.50\% & 2.89 & 68\% \\

(-5, +5) & 50 & 3.20\%$^{**}$ & 2.80\% & 2.15 & 64\% \\

\hline\hline

\end{tabular}

\begin{tablenotes}

\small

\item Notes: $^{***}$, $^{**}$, $^{*}$ indicate significance at 1\%, 5\%, 10\% levels.

\end{tablenotes}

\end{table}

10. Summary and Best Practices¶

Key Extensions Covered¶

| Extension | Key Insight |

|---|---|

| Intraday | Account for microstructure noise, intraday patterns |

| Bonds | Use credit spreads, account for duration |

| International | Handle time zones, market linkages |

| Diff-in-Diff | Need valid control group, parallel trends |

| Confounding | Exclude or control for other events |

| Rolling | Parameters may be time-varying |

General Best Practices¶

Match method to question: Not all extensions are needed

Report robustness: Multiple specifications

Economic significance: Beyond statistical significance

Transparent methodology: Replicability

Address limitations: No method is perfect

11. Exercises¶

Exercise 1: Intraday Fed Announcement¶

Implement an intraday event study for a Fed interest rate announcement.

Exercise 2: Credit Event Analysis¶

Analyze stock and bond responses to the same credit event.

Exercise 3: Parallel Trends Test¶

Implement a formal test for parallel trends in a DiD setting.

Source

# Exercise 3: Parallel Trends Test

def test_parallel_trends(data: pd.DataFrame, pre_periods: int = 5) -> Dict:

"""

Test for parallel trends in pre-event period.

Tests whether treated and control have similar trends before event.

"""

# Get pre-event data

pre_data = data[data['event_time'] < 0].copy()

# Interaction of time with treatment

pre_data['time_treated'] = pre_data['event_time'] * pre_data['treated'].astype(int)

# Regression: R = a + b*time + c*treated + d*(time*treated)

y = pre_data['return']

X = sm.add_constant(pre_data[['event_time', 'treated', 'time_treated']].astype(float))

model = sm.OLS(y, X).fit(cov_type='cluster', cov_kwds={'groups': pre_data['firm_id']})

# Test: is d (time_treated) significantly different from zero?

diff_trend = model.params['time_treated']

diff_trend_t = model.tvalues['time_treated']

diff_trend_p = model.pvalues['time_treated']

return {

'diff_trend_coef': diff_trend,

't_stat': diff_trend_t,

'p_value': diff_trend_p,

'parallel_trends': diff_trend_p > 0.10 # Fail to reject = good!

}

# Test on our DiD data

pt_results = test_parallel_trends(did_data)

print("Parallel Trends Test:")

print("="*60)

print(f"Differential trend coefficient: {pt_results['diff_trend_coef']:.6f}")

print(f"t-statistic: {pt_results['t_stat']:.3f}")

print(f"p-value: {pt_results['p_value']:.4f}")

print(f"\nConclusion: {'Parallel trends assumption supported' if pt_results['parallel_trends'] else 'Parallel trends assumption violated'}")Parallel Trends Test:

============================================================

Differential trend coefficient: 0.000015

t-statistic: 0.324

p-value: 0.7461

Conclusion: Parallel trends assumption supported

References¶

Barclay, M. J., & Litzenberger, R. H. (1988). Announcement effects of new equity issues and the use of intraday price data. Journal of Financial Economics, 21(1), 71-99.

Bessembinder, H., Kahle, K. M., Maxwell, W. F., & Xu, D. (2009). Measuring abnormal bond performance. Review of Financial Studies, 22(10), 4219-4258.

Angrist, J. D., & Pischke, J. S. (2009). Mostly harmless econometrics: An empiricist’s companion. Princeton University Press.

Goodman-Bacon, A. (2021). Difference-in-differences with variation in treatment timing. Journal of Econometrics, 225(2), 254-277.