Session 7: Long-Horizon Event Studies

Event Studies in Finance and Economics - Summer School¶

Learning Objectives¶

By the end of this session, you will be able to:

Understand the challenges unique to long-horizon event studies

Implement Buy-and-Hold Abnormal Returns (BHAR)

Apply the Calendar-Time Portfolio approach

Handle overlapping events and cross-correlation

Choose appropriate benchmarks for long-horizon studies

Recognize power limitations and interpret results cautiously

1. Introduction: Why Long-Horizon Studies?¶

Short-Horizon vs Long-Horizon¶

| Aspect | Short-Horizon (3-5 days) | Long-Horizon (6-36 months) |

|---|---|---|

| Question | Immediate market reaction | Long-term value creation |

| Assumption | Market efficiency | Possible mispricing |

| Challenges | Relatively few | Many (compounding, benchmark, power) |

| Examples | Earnings, M&A announcement | Post-IPO, post-merger performance |

Research Questions¶

Do IPO firms underperform in the long run?

Is there post-merger drift?

Do stock splits predict future returns?

Is the initial market reaction correct?

Key Challenges¶

Compounding: Small daily biases compound to large errors

Benchmark selection: Expected returns hard to estimate

Cross-correlation: Events cluster in time

Survivorship bias: Firms may delist

Low power: Hard to detect true effects

2. Setup and Data¶

Source

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

from scipy import stats

import yfinance as yf

import statsmodels.api as sm

from datetime import datetime, timedelta

from dateutil.relativedelta import relativedelta

from dataclasses import dataclass

from typing import List, Dict, Optional, Tuple

import warnings

warnings.filterwarnings('ignore')

plt.style.use('seaborn-v0_8-whitegrid')

sns.set_palette("husl")

print("Libraries loaded!")Libraries loaded!

Source

# Sample: Tech IPOs from 2020-2021 for long-horizon analysis

# We'll examine 12-month post-IPO performance

IPOS = [

{'ticker': 'ABNB', 'date': '2020-12-10', 'name': 'Airbnb'},

{'ticker': 'DASH', 'date': '2020-12-09', 'name': 'DoorDash'},

{'ticker': 'SNOW', 'date': '2020-09-16', 'name': 'Snowflake'},

{'ticker': 'PLTR', 'date': '2020-09-30', 'name': 'Palantir'},

{'ticker': 'RBLX', 'date': '2021-03-10', 'name': 'Roblox'},

{'ticker': 'COIN', 'date': '2021-04-14', 'name': 'Coinbase'},

{'ticker': 'PATH', 'date': '2021-04-21', 'name': 'UiPath'},

{'ticker': 'DUOL', 'date': '2021-07-28', 'name': 'Duolingo'},

{'ticker': 'HOOD', 'date': '2021-07-29', 'name': 'Robinhood'},

{'ticker': 'RIVN', 'date': '2021-11-10', 'name': 'Rivian'},

]

# Long-horizon parameters

HORIZON_MONTHS = 12 # 1-year post-event

ESTIMATION_DAYS = 0 # No pre-event estimation for IPOs

print(f"Sample: {len(IPOS)} tech IPOs from 2020-2021")

print(f"Horizon: {HORIZON_MONTHS} months post-IPO")Sample: 10 tech IPOs from 2020-2021

Horizon: 12 months post-IPO

Source

@dataclass

class LongHorizonResult:

"""Container for long-horizon event study results."""

ticker: str

name: str

ipo_date: pd.Timestamp

end_date: pd.Timestamp

trading_days: int

data: pd.DataFrame

buy_hold_return: float

market_return: float

bhar: float

def download_long_horizon_data(ticker: str, event_date: str, name: str,

horizon_months: int) -> Optional[LongHorizonResult]:

"""Download data for long-horizon event study."""

try:

event_dt = pd.to_datetime(event_date)

# Add buffer for data availability

start_date = event_dt - timedelta(days=5)

end_date = event_dt + relativedelta(months=horizon_months) + timedelta(days=30)

# Download stock and market data

stock = yf.download(ticker, start=start_date, end=end_date, progress=False)['Close']

market = yf.download('^GSPC', start=start_date, end=end_date, progress=False)['Close']

# Create DataFrame

df = pd.DataFrame({

'stock_price': stock.squeeze(),

'market_price': market.squeeze()

}).dropna()

# Calculate returns

df['stock_ret'] = df['stock_price'].pct_change()

df['market_ret'] = df['market_price'].pct_change()

# Find actual IPO date in data (first trading day)

if event_dt not in df.index:

idx = df.index.get_indexer([event_dt], method='bfill')[0]

if idx < 0 or idx >= len(df):

return None

event_dt = df.index[idx]

# Get horizon end date

target_end = event_dt + relativedelta(months=horizon_months)

mask = (df.index >= event_dt) & (df.index <= target_end)

horizon_data = df[mask].copy()

if len(horizon_data) < 20:

return None

# Calculate event time (trading days)

horizon_data['event_day'] = range(len(horizon_data))

# Calculate cumulative returns

horizon_data['cum_stock_ret'] = (1 + horizon_data['stock_ret']).cumprod() - 1

horizon_data['cum_market_ret'] = (1 + horizon_data['market_ret']).cumprod() - 1

# Buy-and-hold returns

bhr_stock = horizon_data['cum_stock_ret'].iloc[-1]

bhr_market = horizon_data['cum_market_ret'].iloc[-1]

bhar = bhr_stock - bhr_market

return LongHorizonResult(

ticker=ticker,

name=name,

ipo_date=event_dt,

end_date=horizon_data.index[-1],

trading_days=len(horizon_data),

data=horizon_data,

buy_hold_return=bhr_stock,

market_return=bhr_market,

bhar=bhar

)

except Exception as e:

print(f"{ticker}: FAILED - {e}")

return None

print("Downloading long-horizon data...")

ipo_results = [r for ipo in IPOS if (r := download_long_horizon_data(

ipo['ticker'], ipo['date'], ipo['name'], HORIZON_MONTHS))]

print(f"Successfully processed {len(ipo_results)} IPOs")Downloading long-horizon data...

YF.download() has changed argument auto_adjust default to True

Successfully processed 10 IPOs

Source

# Display sample overview

print("\nIPO Sample Overview:")

print("="*80)

print(f"{'Ticker':<8} {'Name':<15} {'IPO Date':<12} {'Days':<6} {'BHR':>10} {'Market':>10} {'BHAR':>10}")

print("-"*80)

for r in ipo_results:

print(f"{r.ticker:<8} {r.name:<15} {r.ipo_date.strftime('%Y-%m-%d'):<12} {r.trading_days:<6} "

f"{r.buy_hold_return*100:>+9.1f}% {r.market_return*100:>+9.1f}% {r.bhar*100:>+9.1f}%")

print("-"*80)

avg_bhar = np.mean([r.bhar for r in ipo_results])

print(f"{'Average':<8} {'':<15} {'':<12} {'':<6} {'':<10} {'':<10} {avg_bhar*100:>+9.1f}%")

IPO Sample Overview:

================================================================================

Ticker Name IPO Date Days BHR Market BHAR

--------------------------------------------------------------------------------

ABNB Airbnb 2020-12-10 253 +24.7% +28.5% -3.8%

DASH DoorDash 2020-12-09 253 -13.0% +27.1% -40.1%

SNOW Snowflake 2020-09-16 253 +27.4% +32.1% -4.7%

PLTR Palantir 2020-09-30 253 +153.1% +28.1% +125.0%

RBLX Roblox 2021-03-10 254 -40.3% +9.3% -49.6%

COIN Coinbase 2021-04-14 255 -55.1% +6.5% -61.6%

PATH UiPath 2021-04-21 254 -73.9% +5.3% -79.1%

DUOL Duolingo 2021-07-28 253 -29.3% -7.5% -21.8%

HOOD Robinhood 2021-07-29 253 -74.0% -6.5% -67.5%

RIVN Rivian 2021-11-10 253 -67.3% -14.9% -52.4%

--------------------------------------------------------------------------------

Average -25.6%

3. Buy-and-Hold Abnormal Returns (BHAR)¶

Definition¶

Interpretation¶

BHAR represents the difference between:

What an investor would earn buying the event stock at and holding until

What they would earn from the benchmark over the same period

BHAR vs CAR¶

| Measure | Formula | Compounding | Bias |

|---|---|---|---|

| CAR | No | Overstates for gains | |

| BHAR | Yes | Can be skewed |

Source

def calculate_bhar(data: pd.DataFrame, start_day: int, end_day: int) -> Dict:

"""

Calculate BHAR for a specific window.

"""

mask = (data['event_day'] >= start_day) & (data['event_day'] <= end_day)

window_data = data[mask]

if len(window_data) < 2:

return {'bhr': np.nan, 'benchmark': np.nan, 'bhar': np.nan}

# Buy-and-hold return

bhr = (1 + window_data['stock_ret']).prod() - 1

benchmark = (1 + window_data['market_ret']).prod() - 1

bhar = bhr - benchmark

return {'bhr': bhr, 'benchmark': benchmark, 'bhar': bhar, 'days': len(window_data)}

# Calculate BHAR for different horizons

horizons = [

(0, 21, '1 month'),

(0, 63, '3 months'),

(0, 126, '6 months'),

(0, 252, '12 months'),

]

print("\nBHAR by Horizon:")

print("="*90)

bhar_results = {}

for start, end, label in horizons:

bhars = []

for r in ipo_results:

result = calculate_bhar(r.data, start, end)

if not np.isnan(result['bhar']):

bhars.append(result['bhar'])

if bhars:

bhars = np.array(bhars)

bhar_results[label] = bhars

# t-test

t_stat, p_value = stats.ttest_1samp(bhars, 0)

sig = '***' if p_value < 0.01 else '**' if p_value < 0.05 else '*' if p_value < 0.10 else ''

print(f"\n{label}:")

print(f" N = {len(bhars)}")

print(f" Mean BHAR = {np.mean(bhars)*100:+.2f}%")

print(f" Median BHAR = {np.median(bhars)*100:+.2f}%")

print(f" t-stat = {t_stat:.2f} {sig} (p = {p_value:.4f})")

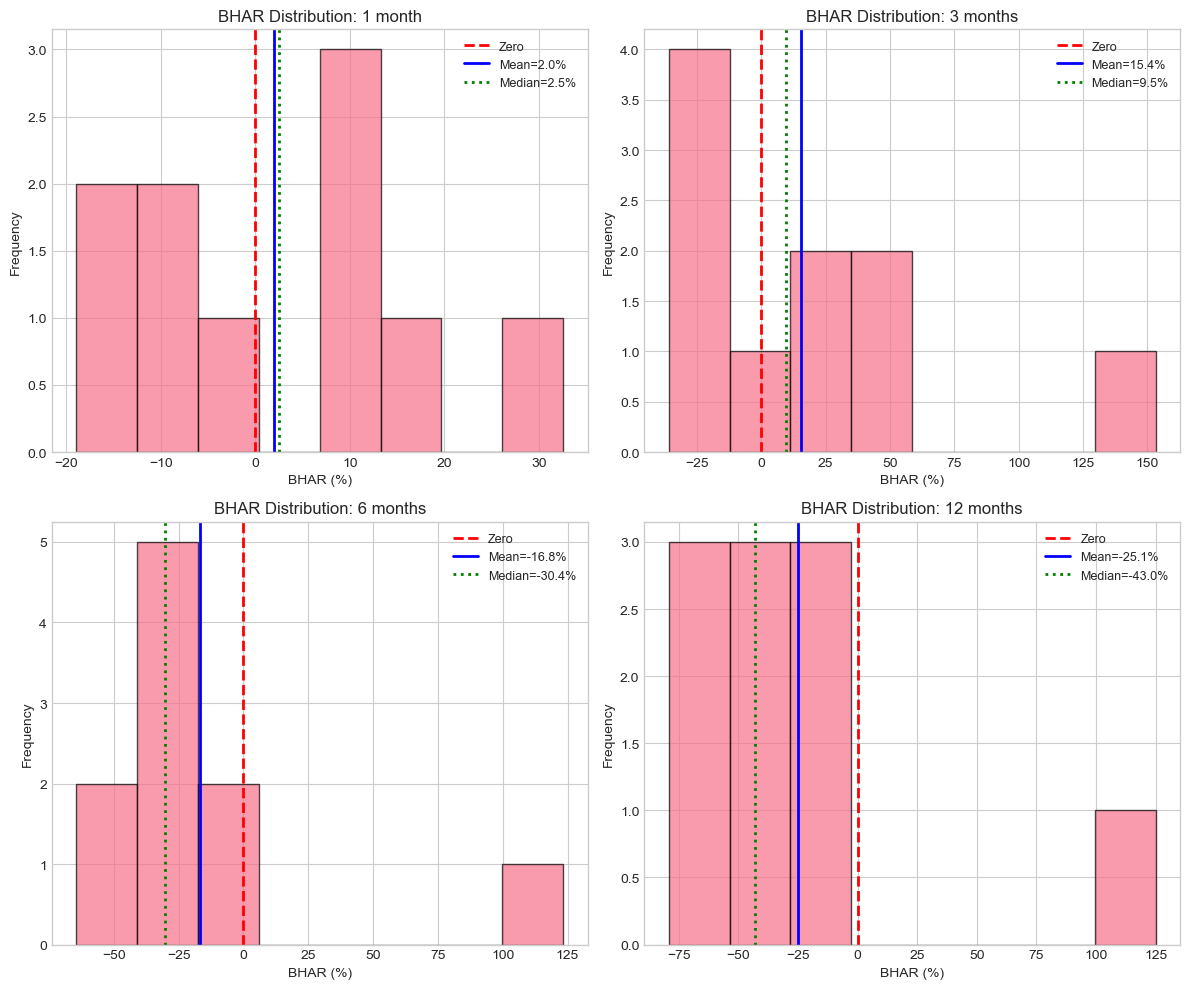

BHAR by Horizon:

==========================================================================================

1 month:

N = 10

Mean BHAR = +1.98%

Median BHAR = +2.47%

t-stat = 0.39 (p = 0.7073)

3 months:

N = 10

Mean BHAR = +15.36%

Median BHAR = +9.53%

t-stat = 0.87 (p = 0.4092)

6 months:

N = 10

Mean BHAR = -16.81%

Median BHAR = -30.37%

t-stat = -1.00 (p = 0.3430)

12 months:

N = 10

Mean BHAR = -25.14%

Median BHAR = -42.98%

t-stat = -1.36 (p = 0.2073)

Source

# Visualize BHAR distribution

fig, axes = plt.subplots(2, 2, figsize=(12, 10))

for i, (label, bhars) in enumerate(bhar_results.items()):

ax = axes.flatten()[i]

ax.hist(bhars * 100, bins=8, edgecolor='black', alpha=0.7)

ax.axvline(0, color='red', linestyle='--', linewidth=2, label='Zero')

ax.axvline(np.mean(bhars)*100, color='blue', linestyle='-', linewidth=2,

label=f'Mean={np.mean(bhars)*100:.1f}%')

ax.axvline(np.median(bhars)*100, color='green', linestyle=':', linewidth=2,

label=f'Median={np.median(bhars)*100:.1f}%')

ax.set_xlabel('BHAR (%)')

ax.set_ylabel('Frequency')

ax.set_title(f'BHAR Distribution: {label}')

ax.legend(fontsize=9)

plt.tight_layout()

plt.show()

Source

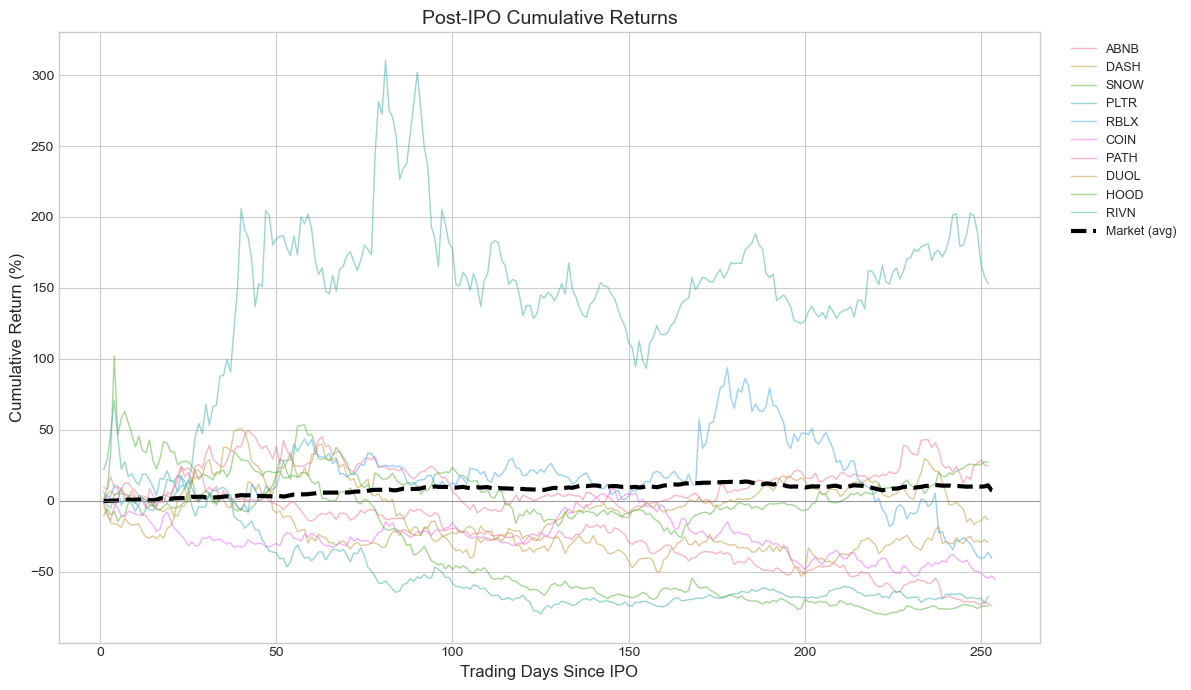

# Plot cumulative returns over time

fig, ax = plt.subplots(figsize=(12, 7))

# Plot each IPO's cumulative return

for r in ipo_results:

ax.plot(r.data['event_day'], r.data['cum_stock_ret']*100,

alpha=0.5, linewidth=1, label=r.ticker)

# Plot average market return

# Align all to same event time

max_days = max(r.trading_days for r in ipo_results)

avg_market = np.zeros(max_days)

count = np.zeros(max_days)

for r in ipo_results:

days = len(r.data)

avg_market[:days] += r.data['cum_market_ret'].values

count[:days] += 1

avg_market = avg_market / np.maximum(count, 1)

ax.plot(range(max_days), avg_market*100, 'k--', linewidth=3, label='Market (avg)')

ax.axhline(0, color='gray', linestyle='-', linewidth=0.5)

ax.set_xlabel('Trading Days Since IPO', fontsize=12)

ax.set_ylabel('Cumulative Return (%)', fontsize=12)

ax.set_title('Post-IPO Cumulative Returns', fontsize=14)

ax.legend(bbox_to_anchor=(1.02, 1), loc='upper left', fontsize=9)

plt.tight_layout()

plt.show()

4. CAR vs BHAR: The Compounding Problem¶

Why It Matters¶

Over long horizons, the difference between CAR and BHAR can be substantial:

Example¶

Consider a stock that goes up 10% then down 10%:

CAR = +10% - 10% = 0%

BHAR = (1.10)(0.90) - 1 = -1%

Source

def calculate_car_long_horizon(data: pd.DataFrame, start_day: int, end_day: int) -> float:

"""Calculate CAR (sum of abnormal returns) for long horizon."""

mask = (data['event_day'] >= start_day) & (data['event_day'] <= end_day)

window_data = data[mask]

ar = window_data['stock_ret'] - window_data['market_ret']

return ar.sum()

# Compare CAR vs BHAR

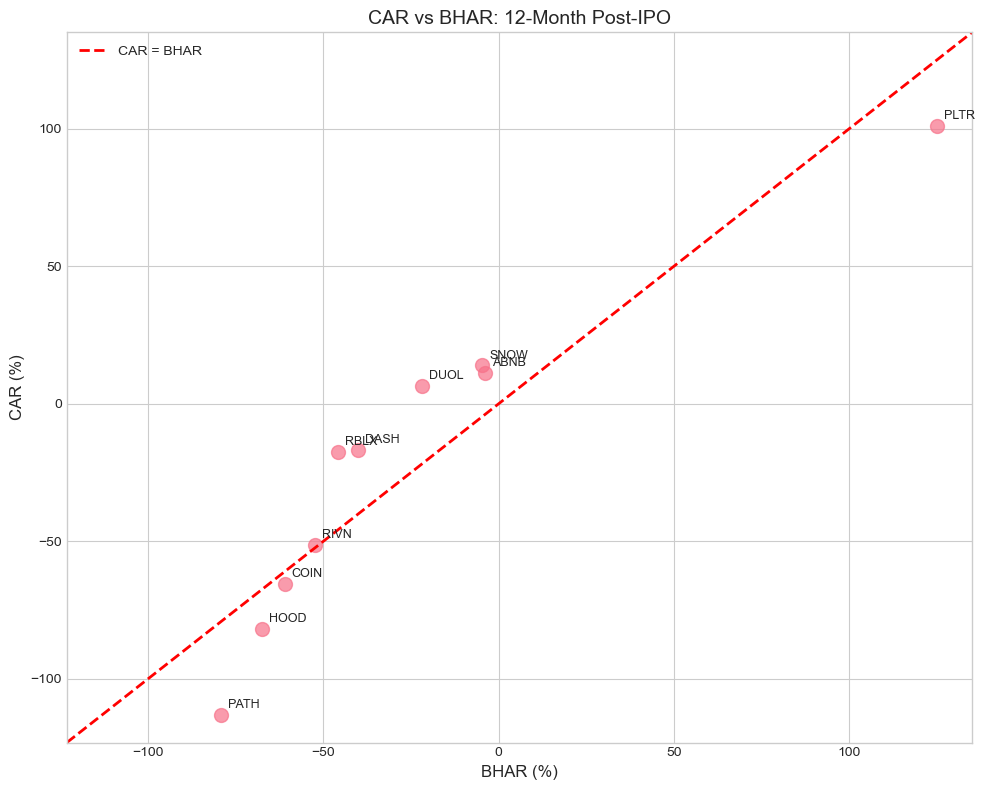

print("CAR vs BHAR Comparison:")

print("="*80)

print(f"{'Ticker':<8} {'CAR (12m)':>12} {'BHAR (12m)':>12} {'Difference':>12}")

print("-"*80)

car_bhar_diff = []

for r in ipo_results:

car = calculate_car_long_horizon(r.data, 0, 252)

bhar_result = calculate_bhar(r.data, 0, 252)

bhar = bhar_result['bhar'] if not np.isnan(bhar_result['bhar']) else np.nan

if not np.isnan(bhar):

diff = car - bhar

car_bhar_diff.append({'ticker': r.ticker, 'car': car, 'bhar': bhar, 'diff': diff})

print(f"{r.ticker:<8} {car*100:>+11.2f}% {bhar*100:>+11.2f}% {diff*100:>+11.2f}%")

print("-"*80)

avg_car = np.mean([d['car'] for d in car_bhar_diff])

avg_bhar = np.mean([d['bhar'] for d in car_bhar_diff])

avg_diff = np.mean([d['diff'] for d in car_bhar_diff])

print(f"{'Average':<8} {avg_car*100:>+11.2f}% {avg_bhar*100:>+11.2f}% {avg_diff*100:>+11.2f}%")

print("\nNote: Positive difference means CAR overstates performance.")CAR vs BHAR Comparison:

================================================================================

Ticker CAR (12m) BHAR (12m) Difference

--------------------------------------------------------------------------------

ABNB +11.07% -3.78% +14.85%

DASH -16.76% -40.09% +23.33%

SNOW +13.90% -4.74% +18.64%

PLTR +100.83% +124.97% -24.13%

RBLX -17.49% -45.87% +28.38%

COIN -65.47% -60.97% -4.51%

PATH -113.14% -79.19% -33.96%

DUOL +6.32% -21.82% +28.14%

HOOD -81.77% -67.47% -14.29%

RIVN -51.23% -52.42% +1.19%

--------------------------------------------------------------------------------

Average -21.37% -25.14% +3.76%

Note: Positive difference means CAR overstates performance.

Source

# Visualize CAR vs BHAR

fig, ax = plt.subplots(figsize=(10, 8))

cars = [d['car']*100 for d in car_bhar_diff]

bhars = [d['bhar']*100 for d in car_bhar_diff]

tickers = [d['ticker'] for d in car_bhar_diff]

ax.scatter(bhars, cars, s=100, alpha=0.7)

# Label points

for i, ticker in enumerate(tickers):

ax.annotate(ticker, (bhars[i], cars[i]), fontsize=9,

xytext=(5, 5), textcoords='offset points')

# 45-degree line

lims = [min(min(cars), min(bhars)) - 10, max(max(cars), max(bhars)) + 10]

ax.plot(lims, lims, 'r--', label='CAR = BHAR', linewidth=2)

ax.set_xlabel('BHAR (%)', fontsize=12)

ax.set_ylabel('CAR (%)', fontsize=12)

ax.set_title('CAR vs BHAR: 12-Month Post-IPO', fontsize=14)

ax.legend()

ax.set_xlim(lims)

ax.set_ylim(lims)

plt.tight_layout()

plt.show()

# Correlation

corr = np.corrcoef(cars, bhars)[0, 1]

print(f"\nCorrelation between CAR and BHAR: {corr:.3f}")

Correlation between CAR and BHAR: 0.929

5. Benchmark Selection¶

Why Benchmark Choice Matters¶

Over long horizons, small differences in expected returns compound:

0.5% monthly difference × 12 months ≈ 6% annual difference!

Common Benchmarks¶

Market return: Simple but ignores size/value effects

Size-matched portfolio: Match on market cap

Size and B/M matched: Two-way matching

Characteristic-matched firm: Single control firm

Factor models: Fama-French 3/5 factors

Source

def download_benchmark_data(start_date: str, end_date: str) -> pd.DataFrame:

"""Download various benchmark returns."""

tickers = {

'market': '^GSPC', # S&P 500

'nasdaq': '^IXIC', # NASDAQ (tech-heavy)

'russell': '^RUT', # Russell 2000 (small cap)

'growth': 'VUG', # Vanguard Growth ETF

}

data = {}

for name, ticker in tickers.items():

try:

prices = yf.download(ticker, start=start_date, end=end_date, progress=False)['Close']

data[name] = prices.squeeze().pct_change()

except:

pass

return pd.DataFrame(data).dropna()

# Download benchmark data

print("Downloading benchmark data...")

benchmark_data = download_benchmark_data('2020-09-01', '2023-01-01')

print(f"Downloaded {len(benchmark_data)} days of benchmark data")Downloading benchmark data...

Downloaded 587 days of benchmark data

Source

def calculate_bhar_with_benchmark(event_result: LongHorizonResult,

benchmark_returns: pd.Series,

end_day: int = 252) -> float:

"""Calculate BHAR using a specific benchmark."""

# Get event dates

event_dates = event_result.data.index[:end_day+1]

# Match benchmark dates

common_dates = event_dates.intersection(benchmark_returns.index)

if len(common_dates) < 20:

return np.nan

stock_rets = event_result.data.loc[common_dates, 'stock_ret']

bench_rets = benchmark_returns.loc[common_dates]

bhr_stock = (1 + stock_rets).prod() - 1

bhr_bench = (1 + bench_rets).prod() - 1

return bhr_stock - bhr_bench

# Calculate BHAR with different benchmarks

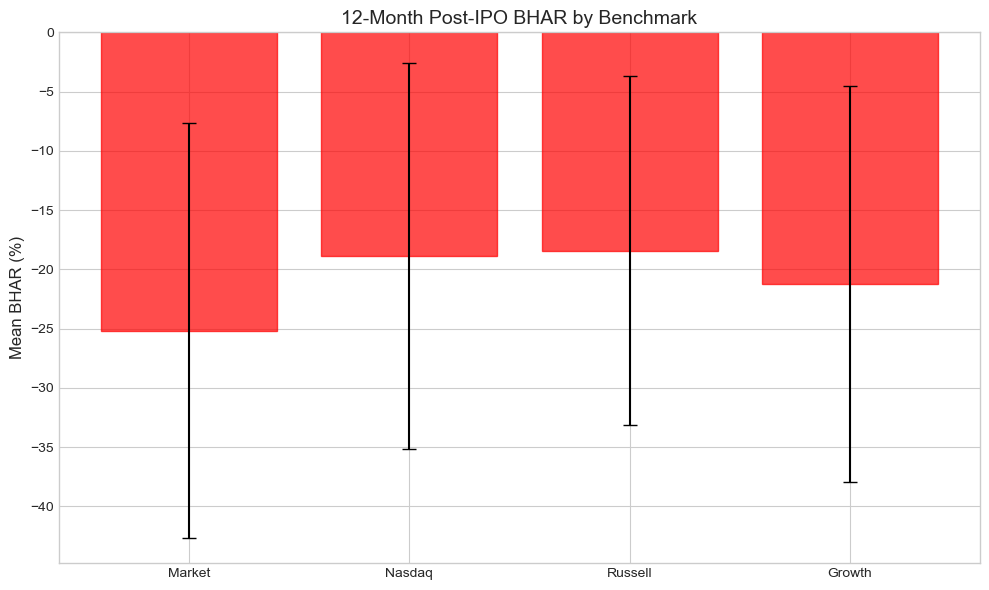

print("\nBHAR Sensitivity to Benchmark Choice (12-month horizon):")

print("="*90)

benchmark_names = ['market', 'nasdaq', 'russell', 'growth']

bhar_by_benchmark = {name: [] for name in benchmark_names}

for r in ipo_results:

for bench_name in benchmark_names:

if bench_name in benchmark_data.columns:

bhar = calculate_bhar_with_benchmark(r, benchmark_data[bench_name], 252)

if not np.isnan(bhar):

bhar_by_benchmark[bench_name].append(bhar)

print(f"\n{'Benchmark':<15} {'Mean BHAR':>12} {'Median BHAR':>12} {'t-stat':>10} {'p-value':>10}")

print("-"*65)

for bench_name in benchmark_names:

bhars = np.array(bhar_by_benchmark[bench_name])

if len(bhars) > 2:

t_stat, p_val = stats.ttest_1samp(bhars, 0)

print(f"{bench_name.capitalize():<15} {np.mean(bhars)*100:>+11.2f}% {np.median(bhars)*100:>+11.2f}% "

f"{t_stat:>10.2f} {p_val:>10.4f}")

print("\nNote: Results can vary substantially with benchmark choice!")

BHAR Sensitivity to Benchmark Choice (12-month horizon):

==========================================================================================

Benchmark Mean BHAR Median BHAR t-stat p-value

-----------------------------------------------------------------

Market -25.15% -42.80% -1.36 0.2056

Nasdaq -18.86% -36.78% -1.10 0.3008

Russell -18.42% -27.37% -1.19 0.2653

Growth -21.22% -39.98% -1.21 0.2585

Note: Results can vary substantially with benchmark choice!

Source

# Visualize benchmark sensitivity

fig, ax = plt.subplots(figsize=(10, 6))

bench_labels = [b.capitalize() for b in benchmark_names if bhar_by_benchmark[b]]

bench_means = [np.mean(bhar_by_benchmark[b])*100 for b in benchmark_names if bhar_by_benchmark[b]]

bench_stds = [np.std(bhar_by_benchmark[b])*100/np.sqrt(len(bhar_by_benchmark[b]))

for b in benchmark_names if bhar_by_benchmark[b]]

x = np.arange(len(bench_labels))

bars = ax.bar(x, bench_means, yerr=bench_stds, capsize=5, alpha=0.7, edgecolor='black')

# Color bars based on sign

for bar, val in zip(bars, bench_means):

bar.set_color('green' if val > 0 else 'red')

ax.axhline(0, color='black', linestyle='-', linewidth=0.5)

ax.set_xticks(x)

ax.set_xticklabels(bench_labels)

ax.set_ylabel('Mean BHAR (%)', fontsize=12)

ax.set_title('12-Month Post-IPO BHAR by Benchmark', fontsize=14)

plt.tight_layout()

plt.show()

6. Calendar-Time Portfolio Approach¶

The Problem with BHAR¶

BHAR treats each event as independent, but:

Events cluster in time (many IPOs in hot markets)

This creates cross-correlation in abnormal returns

Standard errors are understated → over-rejection

Calendar-Time Solution¶

Each calendar month, form a portfolio of all firms within the event window

Calculate portfolio excess return vs benchmark

Run time-series regression:

= average monthly abnormal return

Automatically accounts for cross-correlation

Source

def create_calendar_time_portfolio(event_results: List[LongHorizonResult],

horizon_months: int = 12,

weighting: str = 'equal') -> pd.DataFrame:

"""

Create calendar-time portfolio of event firms.

Args:

event_results: List of event study results

horizon_months: How long to hold each firm after event

weighting: 'equal' or 'value' weighted

Returns:

DataFrame with monthly portfolio returns

"""

# Collect all daily returns with event membership

all_returns = []

for r in event_results:

event_start = r.ipo_date

event_end = event_start + relativedelta(months=horizon_months)

for date, row in r.data.iterrows():

if event_start <= date <= event_end:

all_returns.append({

'date': date,

'ticker': r.ticker,

'stock_ret': row['stock_ret'],

'market_ret': row['market_ret']

})

df = pd.DataFrame(all_returns)

# Convert to monthly

df['year_month'] = df['date'].dt.to_period('M')

# Calculate monthly returns for each stock

monthly_stock = df.groupby(['year_month', 'ticker']).apply(

lambda x: (1 + x['stock_ret']).prod() - 1

).reset_index(name='monthly_ret')

# Calculate portfolio return (equal-weighted)

portfolio = monthly_stock.groupby('year_month').agg({

'monthly_ret': 'mean',

'ticker': 'count'

}).rename(columns={'monthly_ret': 'portfolio_ret', 'ticker': 'n_stocks'})

# Get market returns

market_monthly = df.groupby('year_month').apply(

lambda x: (1 + x['market_ret']).prod() - 1

)

portfolio['market_ret'] = market_monthly

# Excess return

portfolio['excess_ret'] = portfolio['portfolio_ret'] - portfolio['market_ret']

portfolio = portfolio.reset_index()

portfolio['date'] = portfolio['year_month'].dt.to_timestamp()

return portfolio

# Create calendar-time portfolio

ct_portfolio = create_calendar_time_portfolio(ipo_results, horizon_months=12)

print("Calendar-Time Portfolio:")

print("="*70)

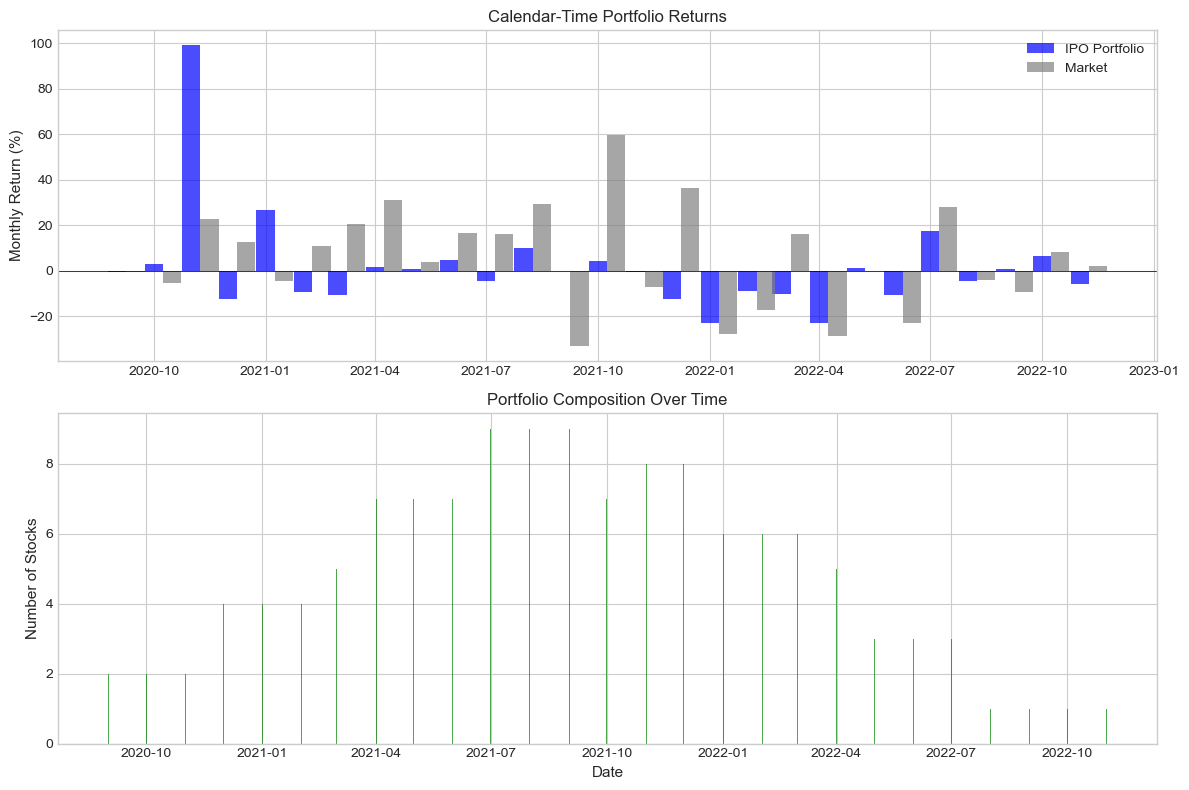

print(ct_portfolio[['year_month', 'n_stocks', 'portfolio_ret', 'market_ret', 'excess_ret']].to_string())Calendar-Time Portfolio:

======================================================================

year_month n_stocks portfolio_ret market_ret excess_ret

0 2020-09 2 -0.005769 -0.006643 0.000874

1 2020-10 2 0.031206 -0.054566 0.085772

2 2020-11 2 0.989733 0.226657 0.763075

3 2020-12 4 -0.125000 0.126382 -0.251383

4 2021-01 4 0.266707 -0.043808 0.310515

5 2021-02 4 -0.091834 0.108522 -0.200356

6 2021-03 5 -0.104970 0.203307 -0.308277

7 2021-04 7 0.015742 0.311209 -0.295466

8 2021-05 7 0.006804 0.039043 -0.032239

9 2021-06 7 0.046184 0.166253 -0.120069

10 2021-07 9 -0.043906 0.162774 -0.206680

11 2021-08 9 0.098731 0.293308 -0.194577

12 2021-09 9 -0.000091 -0.330203 0.330112

13 2021-10 7 0.044227 0.596809 -0.552582

14 2021-11 8 -0.007372 -0.073076 0.065704

15 2021-12 8 -0.125694 0.362265 -0.487959

16 2022-01 6 -0.231315 -0.276829 0.045514

17 2022-02 6 -0.087379 -0.174013 0.086634

18 2022-03 6 -0.101311 0.160944 -0.262255

19 2022-04 5 -0.230364 -0.286624 0.056260

20 2022-05 3 0.010431 0.000160 0.010271

21 2022-06 3 -0.105345 -0.231223 0.125879

22 2022-07 3 0.172684 0.280815 -0.108131

23 2022-08 1 -0.046356 -0.042440 -0.003916

24 2022-09 1 0.006114 -0.093396 0.099510

25 2022-10 1 0.062595 0.079863 -0.017268

26 2022-11 1 -0.057478 0.021795 -0.079273

Source

# Calendar-Time Portfolio Regression (Jensen's Alpha)

print("\n" + "="*70)

print("CALENDAR-TIME PORTFOLIO REGRESSION")

print("="*70)

# Filter months with sufficient observations

ct_valid = ct_portfolio[ct_portfolio['n_stocks'] >= 2].copy()

if len(ct_valid) > 5:

y = ct_valid['portfolio_ret']

X = sm.add_constant(ct_valid['market_ret'])

model = sm.OLS(y, X).fit()

print(f"\nMonths in regression: {len(ct_valid)}")

print(f"Average stocks per month: {ct_valid['n_stocks'].mean():.1f}")

print("\nRegression Results:")

print("-"*50)

print(f"Alpha (monthly): {model.params['const']*100:+.3f}% (t={model.tvalues['const']:.2f})")

print(f"Alpha (annual): {((1+model.params['const'])**12-1)*100:+.2f}%")

print(f"Beta: {model.params['market_ret']:.3f} (t={model.tvalues['market_ret']:.2f})")

print(f"R-squared: {model.rsquared:.3f}")

# Significance

alpha_p = model.pvalues['const']

sig = '***' if alpha_p < 0.01 else '**' if alpha_p < 0.05 else '*' if alpha_p < 0.10 else ''

print(f"\nAlpha p-value: {alpha_p:.4f} {sig}")

======================================================================

CALENDAR-TIME PORTFOLIO REGRESSION

======================================================================

Months in regression: 23

Average stocks per month: 5.5

Regression Results:

--------------------------------------------------

Alpha (monthly): -0.151% (t=-0.03)

Alpha (annual): -1.80%

Beta: 0.293 (t=1.36)

R-squared: 0.081

Alpha p-value: 0.9769

Source

# Visualize calendar-time returns

fig, axes = plt.subplots(2, 1, figsize=(12, 8))

# Portfolio vs Market Returns

ax1 = axes[0]

width = 15 # days for bar width

ax1.bar(ct_portfolio['date'], ct_portfolio['portfolio_ret']*100,

width=width, alpha=0.7, label='IPO Portfolio', color='blue')

ax1.bar(ct_portfolio['date'] + timedelta(days=width), ct_portfolio['market_ret']*100,

width=width, alpha=0.7, label='Market', color='gray')

ax1.axhline(0, color='black', linestyle='-', linewidth=0.5)

ax1.set_ylabel('Monthly Return (%)', fontsize=11)

ax1.set_title('Calendar-Time Portfolio Returns', fontsize=12)

ax1.legend()

# Number of stocks over time

ax2 = axes[1]

ax2.bar(ct_portfolio['date'], ct_portfolio['n_stocks'], alpha=0.7, color='green')

ax2.set_ylabel('Number of Stocks', fontsize=11)

ax2.set_xlabel('Date', fontsize=11)

ax2.set_title('Portfolio Composition Over Time', fontsize=12)

plt.tight_layout()

plt.show()

7. Handling Overlapping Events¶

The Problem¶

When event windows overlap in calendar time:

Cross-sectional dependence in abnormal returns

Standard errors are biased downward

t-statistics are inflated

Solutions¶

Calendar-time portfolio (Section 6): Automatically handles overlap

Crude dependence adjustment: Reduce effective N

Clustering adjustment: Cluster standard errors by time

Source

def analyze_event_clustering(event_results: List[LongHorizonResult],

horizon_months: int = 12) -> Dict:

"""

Analyze the degree of event clustering/overlap.

"""

# Create event timeline

events = []

for r in event_results:

start = r.ipo_date

end = start + relativedelta(months=horizon_months)

events.append({'ticker': r.ticker, 'start': start, 'end': end})

events_df = pd.DataFrame(events)

# Calculate overlap matrix

n = len(events)

overlap_matrix = np.zeros((n, n))

for i in range(n):

for j in range(n):

if i != j:

# Check if windows overlap

start_i, end_i = events[i]['start'], events[i]['end']

start_j, end_j = events[j]['start'], events[j]['end']

overlap_start = max(start_i, start_j)

overlap_end = min(end_i, end_j)

if overlap_start < overlap_end:

# Calculate overlap proportion

window_length_i = (end_i - start_i).days

overlap_days = (overlap_end - overlap_start).days

overlap_matrix[i, j] = overlap_days / window_length_i

# Summary statistics

avg_overlap = np.mean(overlap_matrix[overlap_matrix > 0]) if np.sum(overlap_matrix > 0) > 0 else 0

n_overlapping_pairs = np.sum(overlap_matrix > 0) / 2 # Divide by 2 for symmetric

return {

'n_events': n,

'n_overlapping_pairs': int(n_overlapping_pairs),

'avg_overlap': avg_overlap,

'overlap_matrix': overlap_matrix,

'events_df': events_df

}

# Analyze clustering

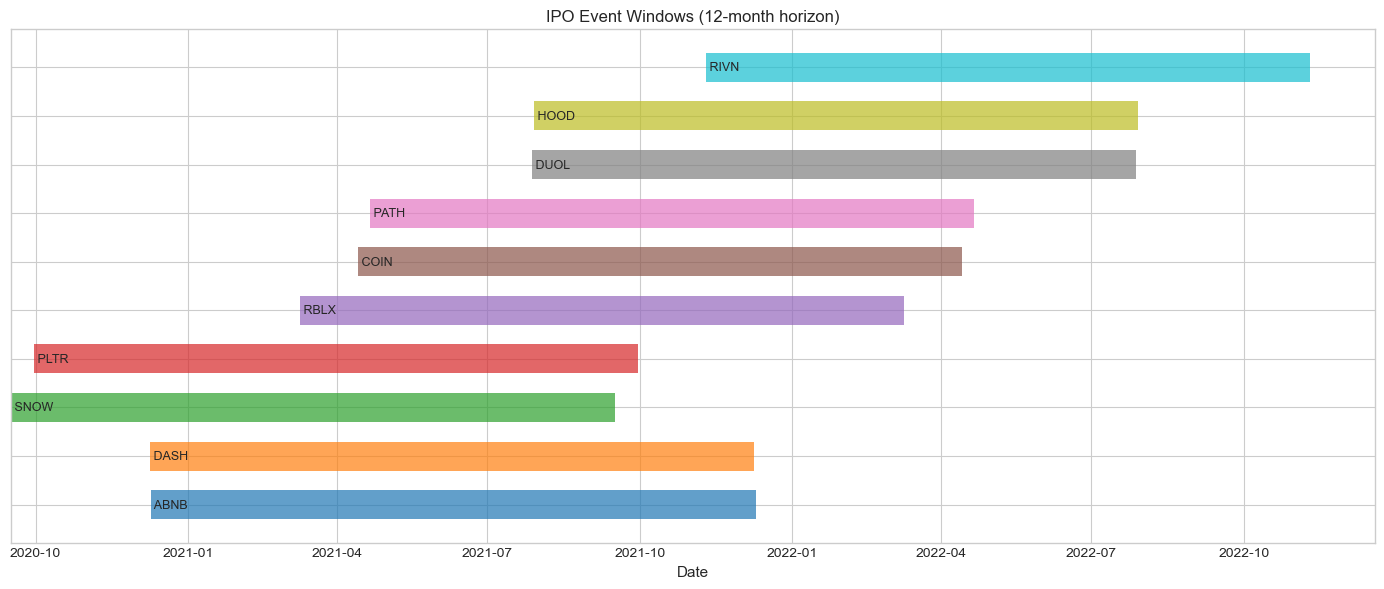

clustering = analyze_event_clustering(ipo_results, horizon_months=12)

print("Event Clustering Analysis:")

print("="*60)

print(f"Total events: {clustering['n_events']}")

print(f"Overlapping pairs: {clustering['n_overlapping_pairs']}")

print(f"Average overlap (when overlapping): {clustering['avg_overlap']*100:.1f}%")

print(f"\nThis clustering can inflate t-statistics in BHAR tests!")Event Clustering Analysis:

============================================================

Total events: 10

Overlapping pairs: 43

Average overlap (when overlapping): 57.6%

This clustering can inflate t-statistics in BHAR tests!

Source

# Visualize event timeline

fig, ax = plt.subplots(figsize=(14, 6))

events_df = clustering['events_df']

colors = plt.cm.tab10(np.linspace(0, 1, len(events_df)))

for i, (_, row) in enumerate(events_df.iterrows()):

ax.barh(i, (row['end'] - row['start']).days, left=row['start'],

height=0.6, alpha=0.7, color=colors[i], label=row['ticker'])

ax.text(row['start'], i, f" {row['ticker']}", va='center', fontsize=9)

ax.set_yticks(range(len(events_df)))

ax.set_yticklabels(['' for _ in range(len(events_df))])

ax.set_xlabel('Date', fontsize=11)

ax.set_title('IPO Event Windows (12-month horizon)', fontsize=12)

plt.tight_layout()

plt.show()

Source

# Crude dependence adjustment

def crude_dependence_adjustment(bhars: np.ndarray, avg_overlap: float) -> Dict:

"""

Adjust t-statistic for cross-sectional dependence.

Following Kolari-Pynnönen (2010) style adjustment.

"""

N = len(bhars)

mean_bhar = np.mean(bhars)

std_bhar = np.std(bhars, ddof=1)

# Unadjusted t-statistic

t_unadj = mean_bhar / (std_bhar / np.sqrt(N))

p_unadj = 2 * (1 - stats.t.cdf(abs(t_unadj), df=N-1))

# Adjusted: assume correlation proportional to overlap

# Effective N reduction

avg_corr = avg_overlap * 0.5 # Rough approximation

adjustment_factor = np.sqrt((1 - avg_corr) / (1 + (N-1) * avg_corr))

t_adj = t_unadj * adjustment_factor

p_adj = 2 * (1 - stats.t.cdf(abs(t_adj), df=N-1))

return {

'N': N,

'mean_bhar': mean_bhar,

't_unadjusted': t_unadj,

'p_unadjusted': p_unadj,

't_adjusted': t_adj,

'p_adjusted': p_adj,

'adjustment_factor': adjustment_factor

}

# Apply adjustment

bhars_12m = np.array([r.bhar for r in ipo_results])

adj_results = crude_dependence_adjustment(bhars_12m, clustering['avg_overlap'])

print("\nCrude Dependence Adjustment:")

print("="*60)

print(f"Mean BHAR: {adj_results['mean_bhar']*100:+.2f}%")

print(f"\nUnadjusted t-stat: {adj_results['t_unadjusted']:.3f} (p={adj_results['p_unadjusted']:.4f})")

print(f"Adjusted t-stat: {adj_results['t_adjusted']:.3f} (p={adj_results['p_adjusted']:.4f})")

print(f"\nAdjustment factor: {adj_results['adjustment_factor']:.3f}")

Crude Dependence Adjustment:

============================================================

Mean BHAR: -25.57%

Unadjusted t-stat: -1.377 (p=0.2017)

Adjusted t-stat: -0.613 (p=0.5549)

Adjustment factor: 0.445

8. Statistical Inference for Long-Horizon Studies¶

The Bad News: Low Power¶

Long-horizon tests have notoriously low power:

High variance in long-run returns

Model misspecification compounds

Need very large samples

Testing Approaches¶

Cross-sectional t-test on BHAR (problematic)

Bootstrapped confidence intervals

Calendar-time alpha (preferred)

Skewness-adjusted tests

Source

def bootstrap_bhar_test(bhars: np.ndarray, n_boot: int = 5000) -> Dict:

"""

Bootstrap test for BHAR.

"""

N = len(bhars)

observed_mean = np.mean(bhars)

np.random.seed(42)

boot_means = [np.mean(np.random.choice(bhars, N, replace=True)) for _ in range(n_boot)]

boot_means = np.array(boot_means)

# Confidence intervals

ci_90 = np.percentile(boot_means, [5, 95])

ci_95 = np.percentile(boot_means, [2.5, 97.5])

ci_99 = np.percentile(boot_means, [0.5, 99.5])

# p-value

p_value = np.mean(np.abs(boot_means - observed_mean) >= np.abs(observed_mean))

return {

'mean': observed_mean,

'boot_se': np.std(boot_means),

'ci_90': ci_90,

'ci_95': ci_95,

'ci_99': ci_99,

'p_value': p_value,

'boot_distribution': boot_means

}

# Bootstrap test

boot_results = bootstrap_bhar_test(bhars_12m, n_boot=5000)

print("Bootstrap Inference for 12-Month BHAR:")

print("="*60)

print(f"Mean BHAR: {boot_results['mean']*100:+.2f}%")

print(f"Bootstrap SE: {boot_results['boot_se']*100:.2f}%")

print(f"\n90% CI: [{boot_results['ci_90'][0]*100:+.2f}%, {boot_results['ci_90'][1]*100:+.2f}%]")

print(f"95% CI: [{boot_results['ci_95'][0]*100:+.2f}%, {boot_results['ci_95'][1]*100:+.2f}%]")

print(f"99% CI: [{boot_results['ci_99'][0]*100:+.2f}%, {boot_results['ci_99'][1]*100:+.2f}%]")

print(f"\np-value: {boot_results['p_value']:.4f}")Bootstrap Inference for 12-Month BHAR:

============================================================

Mean BHAR: -25.57%

Bootstrap SE: 17.40%

90% CI: [-50.78%, +6.11%]

95% CI: [-54.23%, +11.70%]

99% CI: [-58.91%, +27.29%]

p-value: 0.1320

Source

# Skewness-adjusted test (Lyon, Barber, Tsai 1999)

def skewness_adjusted_t_test(bhars: np.ndarray) -> Dict:

"""

Skewness-adjusted t-statistic following Lyon, Barber, Tsai (1999).

"""

N = len(bhars)

mean_bhar = np.mean(bhars)

std_bhar = np.std(bhars, ddof=1)

skew = stats.skew(bhars)

# Standard t-stat

t_standard = mean_bhar / (std_bhar / np.sqrt(N))

# Skewness adjustment

# t_sa = sqrt(N) * (S + (1/3)*gamma*S^2 + (1/6N)*gamma)

# where S = mean/std, gamma = skewness

S = mean_bhar / std_bhar

t_sa = np.sqrt(N) * (S + (1/3) * skew * S**2 + (1/(6*N)) * skew)

p_standard = 2 * (1 - stats.t.cdf(abs(t_standard), df=N-1))

p_adjusted = 2 * (1 - stats.norm.cdf(abs(t_sa)))

return {

'N': N,

'mean': mean_bhar,

'skewness': skew,

't_standard': t_standard,

'p_standard': p_standard,

't_skew_adj': t_sa,

'p_skew_adj': p_adjusted

}

skew_results = skewness_adjusted_t_test(bhars_12m)

print("\nSkewness-Adjusted t-Test (Lyon, Barber, Tsai 1999):")

print("="*60)

print(f"Sample skewness: {skew_results['skewness']:.3f}")

print(f"\nStandard t-stat: {skew_results['t_standard']:.3f} (p={skew_results['p_standard']:.4f})")

print(f"Skew-adjusted t-stat: {skew_results['t_skew_adj']:.3f} (p={skew_results['p_skew_adj']:.4f})")

Skewness-Adjusted t-Test (Lyon, Barber, Tsai 1999):

============================================================

Sample skewness: 1.806

Standard t-stat: -1.377 (p=0.2017)

Skew-adjusted t-stat: -0.921 (p=0.3571)

9. Comprehensive Results Comparison¶

Source

# Summary table of all approaches

print("\n" + "="*90)

print("COMPREHENSIVE RESULTS: 12-Month Post-IPO Performance")

print("="*90)

print(f"\nSample: {len(ipo_results)} tech IPOs (2020-2021)")

print(f"Mean BHAR: {np.mean(bhars_12m)*100:+.2f}%")

print(f"Median BHAR: {np.median(bhars_12m)*100:+.2f}%")

print("\n" + "-"*90)

print(f"{'Method':<35} {'Statistic':>15} {'p-value':>12} {'Conclusion':>20}")

print("-"*90)

# Standard t-test

t_stat, p_val = stats.ttest_1samp(bhars_12m, 0)

conclusion = 'Significant*' if p_val < 0.10 else 'Not significant'

print(f"{'Standard t-test (BHAR)':<35} {t_stat:>15.3f} {p_val:>12.4f} {conclusion:>20}")

# Dependence-adjusted

conclusion = 'Significant*' if adj_results['p_adjusted'] < 0.10 else 'Not significant'

print(f"{'Dependence-adjusted t-test':<35} {adj_results['t_adjusted']:>15.3f} "

f"{adj_results['p_adjusted']:>12.4f} {conclusion:>20}")

# Skewness-adjusted

conclusion = 'Significant*' if skew_results['p_skew_adj'] < 0.10 else 'Not significant'

print(f"{'Skewness-adjusted t-test':<35} {skew_results['t_skew_adj']:>15.3f} "

f"{skew_results['p_skew_adj']:>12.4f} {conclusion:>20}")

# Bootstrap

conclusion = 'Significant*' if boot_results['p_value'] < 0.10 else 'Not significant'

print(f"{'Bootstrap test':<35} {'N/A':>15} {boot_results['p_value']:>12.4f} {conclusion:>20}")

# Calendar-time alpha

if len(ct_valid) > 5:

alpha_annual = ((1 + model.params['const'])**12 - 1)

conclusion = 'Significant*' if model.pvalues['const'] < 0.10 else 'Not significant'

print(f"{'Calendar-time alpha (annual)':<35} {alpha_annual*100:>14.2f}% "

f"{model.pvalues['const']:>12.4f} {conclusion:>20}")

print("-"*90)

print("* Significant at 10% level")

==========================================================================================

COMPREHENSIVE RESULTS: 12-Month Post-IPO Performance

==========================================================================================

Sample: 10 tech IPOs (2020-2021)

Mean BHAR: -25.57%

Median BHAR: -44.84%

------------------------------------------------------------------------------------------

Method Statistic p-value Conclusion

------------------------------------------------------------------------------------------

Standard t-test (BHAR) -1.377 0.2017 Not significant

Dependence-adjusted t-test -0.613 0.5549 Not significant

Skewness-adjusted t-test -0.921 0.3571 Not significant

Bootstrap test N/A 0.1320 Not significant

Calendar-time alpha (annual) -1.80% 0.9769 Not significant

------------------------------------------------------------------------------------------

* Significant at 10% level

10. Best Practices and Recommendations¶

Reporting Guidelines¶

Report multiple measures: BHAR, CAR, and calendar-time alpha

Test multiple benchmarks: Show sensitivity

Acknowledge clustering: Report adjusted statistics

Graph cumulative returns: Visual inspection is informative

Report medians: BHAR is often skewed

Common Pitfalls¶

| Pitfall | Solution |

|---|---|

| Using only BHAR t-test | Report calendar-time alpha |

| Single benchmark | Test multiple benchmarks |

| Ignoring clustering | Use dependence adjustment |

| Small sample confidence | Bootstrap or be cautious |

| Survivorship bias | Address delistings |

Source

# Publication-ready table

print("\n" + "="*90)

print("TABLE: Long-Horizon Post-IPO Performance")

print("="*90)

print("\nPanel A: Buy-and-Hold Abnormal Returns (BHAR)")

print("-"*70)

print(f"{'Horizon':<15} {'N':>6} {'Mean':>10} {'Median':>10} {'t-stat':>10} {'% Neg':>10}")

print("-"*70)

for (start, end, label) in horizons:

if label in bhar_results:

bhars = bhar_results[label]

t, p = stats.ttest_1samp(bhars, 0)

sig = '***' if p < 0.01 else '**' if p < 0.05 else '*' if p < 0.10 else ''

pct_neg = np.mean(bhars < 0) * 100

print(f"{label:<15} {len(bhars):>6} {np.mean(bhars)*100:>+9.2f}% {np.median(bhars)*100:>+9.2f}% "

f"{t:>8.2f}{sig:<2} {pct_neg:>9.0f}%")

print("-"*70)

print("***, **, * indicate significance at 1%, 5%, 10% levels")

if len(ct_valid) > 5:

print("\nPanel B: Calendar-Time Portfolio Regression")

print("-"*70)

print(f"Monthly alpha: {model.params['const']*100:+.3f}% (t={model.tvalues['const']:.2f})")

print(f"Annual alpha: {((1+model.params['const'])**12-1)*100:+.2f}%")

print(f"Market beta: {model.params['market_ret']:.3f}")

print(f"Months: {len(ct_valid)}, Avg stocks/month: {ct_valid['n_stocks'].mean():.1f}")

==========================================================================================

TABLE: Long-Horizon Post-IPO Performance

==========================================================================================

Panel A: Buy-and-Hold Abnormal Returns (BHAR)

----------------------------------------------------------------------

Horizon N Mean Median t-stat % Neg

----------------------------------------------------------------------

1 month 10 +1.98% +2.47% 0.39 50%

3 months 10 +15.36% +9.53% 0.87 50%

6 months 10 -16.81% -30.37% -1.00 80%

12 months 10 -25.14% -42.98% -1.36 90%

----------------------------------------------------------------------

***, **, * indicate significance at 1%, 5%, 10% levels

Panel B: Calendar-Time Portfolio Regression

----------------------------------------------------------------------

Monthly alpha: -0.151% (t=-0.03)

Annual alpha: -1.80%

Market beta: 0.293

Months: 23, Avg stocks/month: 5.5

11. Exercises¶

Exercise 1: Fama-French Adjustment¶

Download Fama-French factors and estimate calendar-time alpha controlling for SMB and HML.

Exercise 2: Size Portfolios¶

Create size-matched benchmarks using market cap at IPO.

Exercise 3: Subsample Analysis¶

Split the sample by IPO year and test for differences.

Source

# Exercise 3: Subsample by IPO year

print("Exercise 3: BHAR by IPO Year")

print("="*60)

for year in [2020, 2021]:

year_results = [r for r in ipo_results if r.ipo_date.year == year]

if year_results:

bhars_year = np.array([r.bhar for r in year_results])

t, p = stats.ttest_1samp(bhars_year, 0) if len(bhars_year) > 1 else (np.nan, np.nan)

print(f"\n{year} IPOs (n={len(year_results)}):")

print(f" Mean BHAR: {np.mean(bhars_year)*100:+.2f}%")

print(f" Median BHAR: {np.median(bhars_year)*100:+.2f}%")

if not np.isnan(t):

print(f" t-stat: {t:.2f} (p={p:.4f})")Exercise 3: BHAR by IPO Year

============================================================

2020 IPOs (n=4):

Mean BHAR: +19.09%

Median BHAR: -4.26%

t-stat: 0.53 (p=0.6353)

2021 IPOs (n=6):

Mean BHAR: -55.34%

Median BHAR: -57.03%

t-stat: -6.92 (p=0.0010)

12. Summary¶

Key Takeaways¶

BHAR vs CAR: Use BHAR for long horizons (accounts for compounding)

Benchmark sensitivity: Results can change dramatically with benchmark choice

Calendar-time approach: Preferred for handling cross-correlation

Event clustering: Adjust standard errors or use calendar-time

Low power: Be cautious with small samples and non-significant results

Multiple tests: Report various methods for robustness

When to Use Long-Horizon Studies¶

Testing market efficiency (does initial reaction persist?)

Long-term value creation (M&A, restructuring)

Investment strategy evaluation (IPO underperformance)

Coming Up Next¶

Session 8: Extensions and Special Topics

References¶

Barber, B. M., & Lyon, J. D. (1997). Detecting long-run abnormal stock returns: The empirical power and specification of test statistics. Journal of Financial Economics, 43(3), 341-372.

Fama, E. F. (1998). Market efficiency, long-term returns, and behavioral finance. Journal of Financial Economics, 49(3), 283-306.

Lyon, J. D., Barber, B. M., & Tsai, C. L. (1999). Improved methods for tests of long-run abnormal stock returns. Journal of Finance, 54(1), 165-201.

Mitchell, M. L., & Stafford, E. (2000). Managerial decisions and long-term stock price performance. Journal of Business, 73(3), 287-329.