Session 6: Cross-Sectional Analysis

Event Studies in Finance and Economics - Summer School¶

Learning Objectives¶

By the end of this session, you will be able to:

Understand why cross-sectional variation in event responses matters

Implement cross-sectional regression analysis of CARs

Handle heteroskedasticity in cross-sectional regressions

Use weighted least squares (WLS) for efficient estimation

Analyze determinants of abnormal returns

Address endogeneity concerns in event study settings

1. Introduction: Beyond Average Effects¶

From CAAR to Cross-Sectional Analysis¶

So far, we’ve focused on testing whether the average abnormal return differs from zero. But events often affect firms differently:

Earnings announcements: Surprise magnitude matters

M&A announcements: Deal characteristics affect returns

Regulatory changes: Firm exposure varies

Macroeconomic shocks: Industry and size matter

The Cross-Sectional Regression¶

Where are firm or event characteristics that may explain variation in abnormal returns.

Key Questions¶

What firm characteristics predict stronger/weaker event responses?

Do deal characteristics affect announcement returns?

How does prior information affect the market reaction?

Are there systematic patterns across industries or time?

2. Setup and Data¶

Source

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

from scipy import stats

import yfinance as yf

import statsmodels.api as sm

from statsmodels.stats.outliers_influence import variance_inflation_factor

from statsmodels.stats.diagnostic import het_breuschpagan, het_white

from datetime import timedelta

from dataclasses import dataclass

from typing import List, Dict, Optional, Tuple

import warnings

warnings.filterwarnings('ignore')

plt.style.use('seaborn-v0_8-whitegrid')

sns.set_palette("husl")

print("Libraries loaded!")Libraries loaded!

Source

# Extended sample with firm characteristics for cross-sectional analysis

# Using Q2-Q3 2023 earnings announcements with additional firm data

EVENTS = [

# Tech - Large Cap

{'ticker': 'AAPL', 'date': '2023-08-03', 'name': 'Apple', 'sector': 'Tech', 'eps_surprise': 0.05},

{'ticker': 'MSFT', 'date': '2023-07-25', 'name': 'Microsoft', 'sector': 'Tech', 'eps_surprise': 0.08},

{'ticker': 'GOOGL', 'date': '2023-07-25', 'name': 'Alphabet', 'sector': 'Tech', 'eps_surprise': 0.12},

{'ticker': 'AMZN', 'date': '2023-08-03', 'name': 'Amazon', 'sector': 'Tech', 'eps_surprise': 0.45},

{'ticker': 'META', 'date': '2023-07-26', 'name': 'Meta', 'sector': 'Tech', 'eps_surprise': 0.22},

{'ticker': 'NVDA', 'date': '2023-08-23', 'name': 'Nvidia', 'sector': 'Tech', 'eps_surprise': 0.35},

# Tech - Smaller

{'ticker': 'AMD', 'date': '2023-08-01', 'name': 'AMD', 'sector': 'Tech', 'eps_surprise': -0.02},

{'ticker': 'INTC', 'date': '2023-07-27', 'name': 'Intel', 'sector': 'Tech', 'eps_surprise': 0.18},

{'ticker': 'CRM', 'date': '2023-08-30', 'name': 'Salesforce', 'sector': 'Tech', 'eps_surprise': 0.15},

{'ticker': 'ADBE', 'date': '2023-09-14', 'name': 'Adobe', 'sector': 'Tech', 'eps_surprise': 0.06},

# Finance

{'ticker': 'JPM', 'date': '2023-07-14', 'name': 'JPMorgan', 'sector': 'Finance', 'eps_surprise': 0.10},

{'ticker': 'BAC', 'date': '2023-07-18', 'name': 'Bank of America', 'sector': 'Finance', 'eps_surprise': 0.03},

{'ticker': 'WFC', 'date': '2023-07-14', 'name': 'Wells Fargo', 'sector': 'Finance', 'eps_surprise': 0.08},

{'ticker': 'GS', 'date': '2023-07-19', 'name': 'Goldman Sachs', 'sector': 'Finance', 'eps_surprise': -0.15},

{'ticker': 'MS', 'date': '2023-07-18', 'name': 'Morgan Stanley', 'sector': 'Finance', 'eps_surprise': -0.05},

# Healthcare

{'ticker': 'JNJ', 'date': '2023-07-20', 'name': 'Johnson & Johnson', 'sector': 'Healthcare', 'eps_surprise': 0.04},

{'ticker': 'UNH', 'date': '2023-07-14', 'name': 'UnitedHealth', 'sector': 'Healthcare', 'eps_surprise': 0.02},

{'ticker': 'PFE', 'date': '2023-08-01', 'name': 'Pfizer', 'sector': 'Healthcare', 'eps_surprise': -0.08},

{'ticker': 'MRK', 'date': '2023-07-27', 'name': 'Merck', 'sector': 'Healthcare', 'eps_surprise': 0.12},

{'ticker': 'ABBV', 'date': '2023-07-27', 'name': 'AbbVie', 'sector': 'Healthcare', 'eps_surprise': 0.05},

# Consumer

{'ticker': 'PG', 'date': '2023-07-28', 'name': 'Procter & Gamble', 'sector': 'Consumer', 'eps_surprise': 0.03},

{'ticker': 'KO', 'date': '2023-07-26', 'name': 'Coca-Cola', 'sector': 'Consumer', 'eps_surprise': 0.05},

{'ticker': 'PEP', 'date': '2023-07-13', 'name': 'PepsiCo', 'sector': 'Consumer', 'eps_surprise': 0.07},

{'ticker': 'WMT', 'date': '2023-08-17', 'name': 'Walmart', 'sector': 'Consumer', 'eps_surprise': 0.09},

{'ticker': 'COST', 'date': '2023-09-26', 'name': 'Costco', 'sector': 'Consumer', 'eps_surprise': 0.04},

]

EST_WINDOW, GAP, PRE, POST = 120, 10, 5, 5

print(f"Sample: {len(EVENTS)} earnings announcements across {len(set(e['sector'] for e in EVENTS))} sectors")Sample: 25 earnings announcements across 4 sectors

Source

@dataclass

class EventResult:

"""Container for event study results with firm characteristics."""

ticker: str

name: str

sector: str

event_date: pd.Timestamp

eps_surprise: float

market_cap: float

beta: float

sigma: float

pre_event_return: float

event_data: pd.DataFrame

car_var: float # Variance of CAR for WLS

def get_firm_characteristics(ticker: str) -> Dict:

"""Fetch firm characteristics from Yahoo Finance."""

try:

stock = yf.Ticker(ticker)

info = stock.info

return {

'market_cap': info.get('marketCap', np.nan),

'beta': info.get('beta', np.nan),

}

except:

return {'market_cap': np.nan, 'beta': np.nan}

def process_event(event: Dict, est_window: int, gap: int, pre: int, post: int) -> Optional[EventResult]:

"""Process single event and extract characteristics."""

try:

ticker = event['ticker']

event_dt = pd.to_datetime(event['date'])

start = event_dt - timedelta(days=int((est_window + gap + pre) * 1.5))

end = event_dt + timedelta(days=int(post * 2.5))

stock = yf.download(ticker, start=start, end=end, progress=False)['Close']

market = yf.download('^GSPC', start=start, end=end, progress=False)['Close']

df = pd.DataFrame({'stock': stock.squeeze(), 'market': market.squeeze()})

df['stock_ret'] = df['stock'].pct_change()

df['market_ret'] = df['market'].pct_change()

df = df.dropna()

if event_dt not in df.index:

idx = df.index.get_indexer([event_dt], method='nearest')[0]

event_dt = df.index[idx]

event_idx = df.index.get_loc(event_dt)

df['event_time'] = range(-event_idx, len(df) - event_idx)

# Split windows

est_end = -(gap + pre)

est_data = df[(df['event_time'] >= est_end - est_window) & (df['event_time'] < est_end)]

evt_data = df[(df['event_time'] >= -pre) & (df['event_time'] <= post)].copy()

# Market model estimation

y, x = est_data['stock_ret'].values, est_data['market_ret'].values

X = sm.add_constant(x)

ols = sm.OLS(y, X).fit()

alpha, beta = ols.params[0], ols.params[1]

sigma = np.std(ols.resid, ddof=2)

# Abnormal returns

evt_data['expected'] = alpha + beta * evt_data['market_ret']

evt_data['AR'] = evt_data['stock_ret'] - evt_data['expected']

# Pre-event cumulative return (momentum proxy)

pre_event_data = df[(df['event_time'] >= -60) & (df['event_time'] < -pre)]

pre_event_return = (1 + pre_event_data['stock_ret']).prod() - 1 if len(pre_event_data) > 0 else 0

# CAR variance for WLS

L = len(evt_data[(evt_data['event_time'] >= -1) & (evt_data['event_time'] <= 1)])

car_var = L * sigma**2

# Get firm characteristics

chars = get_firm_characteristics(ticker)

return EventResult(

ticker=ticker,

name=event['name'],

sector=event['sector'],

event_date=event_dt,

eps_surprise=event['eps_surprise'],

market_cap=chars['market_cap'],

beta=beta,

sigma=sigma,

pre_event_return=pre_event_return,

event_data=evt_data,

car_var=car_var

)

except Exception as e:

print(f"{event['ticker']}: FAILED - {e}")

return None

print("Processing events...")

event_results = [r for e in EVENTS if (r := process_event(e, EST_WINDOW, GAP, PRE, POST))]

print(f"Successfully processed {len(event_results)} events")Processing events...

YF.download() has changed argument auto_adjust default to True

Successfully processed 25 events

Source

def calculate_car(event_data: pd.DataFrame, tau1: int, tau2: int) -> float:

mask = (event_data['event_time'] >= tau1) & (event_data['event_time'] <= tau2)

return event_data.loc[mask, 'AR'].sum()

# Create cross-sectional dataset

def create_cross_sectional_data(event_results: List[EventResult], tau1: int, tau2: int) -> pd.DataFrame:

"""Create dataset for cross-sectional regression."""

data = []

for r in event_results:

car = calculate_car(r.event_data, tau1, tau2)

data.append({

'ticker': r.ticker,

'name': r.name,

'sector': r.sector,

'CAR': car,

'eps_surprise': r.eps_surprise,

'log_mcap': np.log(r.market_cap) if r.market_cap and r.market_cap > 0 else np.nan,

'beta': r.beta,

'sigma': r.sigma,

'momentum': r.pre_event_return,

'car_var': r.car_var,

'car_se': np.sqrt(r.car_var)

})

df = pd.DataFrame(data)

df = df.dropna()

return df

# Create dataset for CAR(-1,+1)

cs_data = create_cross_sectional_data(event_results, -1, 1)

print(f"\nCross-sectional dataset: {len(cs_data)} observations")

print(cs_data[['ticker', 'sector', 'CAR', 'eps_surprise', 'log_mcap']].head(10).to_string())

Cross-sectional dataset: 24 observations

ticker sector CAR eps_surprise log_mcap

0 AAPL Tech -0.051469 0.05 28.931133

1 MSFT Tech -0.031932 0.08 28.840995

2 GOOGL Tech 0.062735 0.12 29.018200

3 AMZN Tech 0.090422 0.45 28.549368

4 META Tech 0.060857 0.22 28.121054

5 NVDA Tech -0.000214 0.35 29.135165

6 AMD Tech -0.011225 -0.02 26.746914

7 INTC Tech 0.075252 0.18 26.280505

8 CRM Tech 0.023052 0.15 26.103816

9 ADBE Tech -0.026877 0.06 25.555308

3. Exploratory Analysis¶

Source

# Summary statistics by sector

print("Summary Statistics by Sector:")

print("="*70)

sector_stats = cs_data.groupby('sector').agg({

'CAR': ['count', 'mean', 'median', 'std'],

'eps_surprise': 'mean',

'log_mcap': 'mean'

}).round(4)

sector_stats.columns = ['N', 'Mean CAR', 'Median CAR', 'Std CAR', 'Avg EPS Surp', 'Avg Log MCap']

sector_stats['Mean CAR'] = sector_stats['Mean CAR'].apply(lambda x: f"{x*100:.2f}%")

sector_stats['Median CAR'] = sector_stats['Median CAR'].apply(lambda x: f"{x*100:.2f}%")

sector_stats['Std CAR'] = sector_stats['Std CAR'].apply(lambda x: f"{x*100:.2f}%")

print(sector_stats.to_string())Summary Statistics by Sector:

======================================================================

N Mean CAR Median CAR Std CAR Avg EPS Surp Avg Log MCap

sector

Consumer 5 0.91% 1.42% 1.03% 0.056 26.6830

Finance 4 4.86% 4.89% 2.81% 0.015 26.7116

Healthcare 5 3.91% 6.73% 4.37% 0.030 26.4434

Tech 10 1.91% 1.14% 5.04% 0.164 27.7282

Source

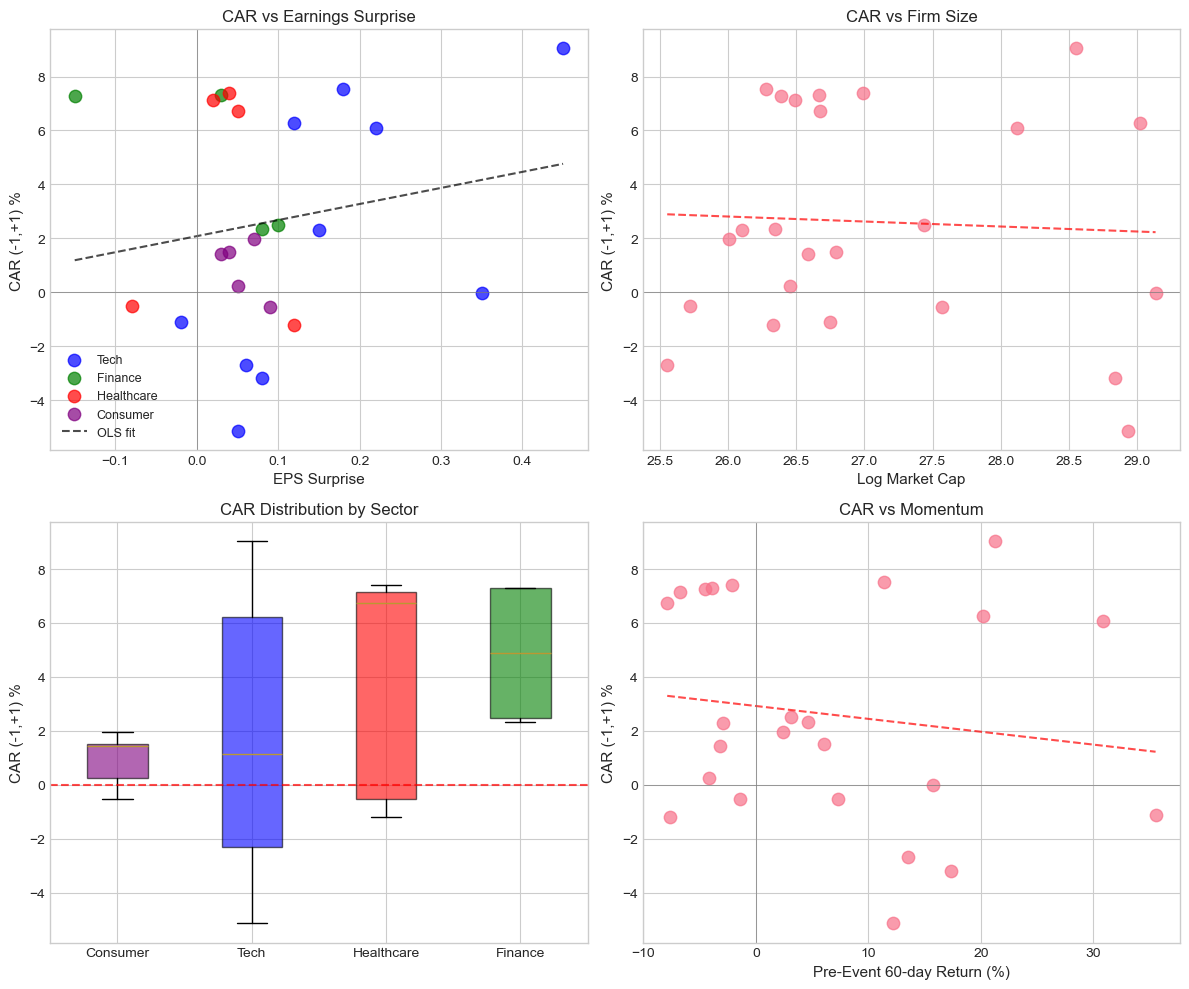

# Visualize relationships

fig, axes = plt.subplots(2, 2, figsize=(12, 10))

# CAR vs EPS Surprise

ax1 = axes[0, 0]

colors = {'Tech': 'blue', 'Finance': 'green', 'Healthcare': 'red', 'Consumer': 'purple'}

for sector in cs_data['sector'].unique():

mask = cs_data['sector'] == sector

ax1.scatter(cs_data.loc[mask, 'eps_surprise'], cs_data.loc[mask, 'CAR']*100,

label=sector, alpha=0.7, s=80, c=colors.get(sector, 'gray'))

# Add regression line

z = np.polyfit(cs_data['eps_surprise'], cs_data['CAR']*100, 1)

p = np.poly1d(z)

x_line = np.linspace(cs_data['eps_surprise'].min(), cs_data['eps_surprise'].max(), 100)

ax1.plot(x_line, p(x_line), 'k--', alpha=0.7, label='OLS fit')

ax1.set_xlabel('EPS Surprise', fontsize=11)

ax1.set_ylabel('CAR (-1,+1) %', fontsize=11)

ax1.set_title('CAR vs Earnings Surprise', fontsize=12)

ax1.axhline(0, color='gray', linestyle='-', linewidth=0.5)

ax1.axvline(0, color='gray', linestyle='-', linewidth=0.5)

ax1.legend(fontsize=9)

# CAR vs Market Cap

ax2 = axes[0, 1]

ax2.scatter(cs_data['log_mcap'], cs_data['CAR']*100, alpha=0.7, s=80)

z = np.polyfit(cs_data['log_mcap'], cs_data['CAR']*100, 1)

p = np.poly1d(z)

x_line = np.linspace(cs_data['log_mcap'].min(), cs_data['log_mcap'].max(), 100)

ax2.plot(x_line, p(x_line), 'r--', alpha=0.7)

ax2.set_xlabel('Log Market Cap', fontsize=11)

ax2.set_ylabel('CAR (-1,+1) %', fontsize=11)

ax2.set_title('CAR vs Firm Size', fontsize=12)

ax2.axhline(0, color='gray', linestyle='-', linewidth=0.5)

# CAR distribution by sector

ax3 = axes[1, 0]

sector_order = cs_data.groupby('sector')['CAR'].mean().sort_values().index

cs_data['sector_cat'] = pd.Categorical(cs_data['sector'], categories=sector_order, ordered=True)

bp = ax3.boxplot([cs_data[cs_data['sector'] == s]['CAR']*100 for s in sector_order],

labels=sector_order, patch_artist=True)

for patch, sector in zip(bp['boxes'], sector_order):

patch.set_facecolor(colors.get(sector, 'gray'))

patch.set_alpha(0.6)

ax3.axhline(0, color='red', linestyle='--', alpha=0.7)

ax3.set_ylabel('CAR (-1,+1) %', fontsize=11)

ax3.set_title('CAR Distribution by Sector', fontsize=12)

# CAR vs Pre-event Momentum

ax4 = axes[1, 1]

ax4.scatter(cs_data['momentum']*100, cs_data['CAR']*100, alpha=0.7, s=80)

z = np.polyfit(cs_data['momentum']*100, cs_data['CAR']*100, 1)

p = np.poly1d(z)

x_line = np.linspace(cs_data['momentum'].min()*100, cs_data['momentum'].max()*100, 100)

ax4.plot(x_line, p(x_line), 'r--', alpha=0.7)

ax4.set_xlabel('Pre-Event 60-day Return (%)', fontsize=11)

ax4.set_ylabel('CAR (-1,+1) %', fontsize=11)

ax4.set_title('CAR vs Momentum', fontsize=12)

ax4.axhline(0, color='gray', linestyle='-', linewidth=0.5)

ax4.axvline(0, color='gray', linestyle='-', linewidth=0.5)

plt.tight_layout()

plt.show()

Source

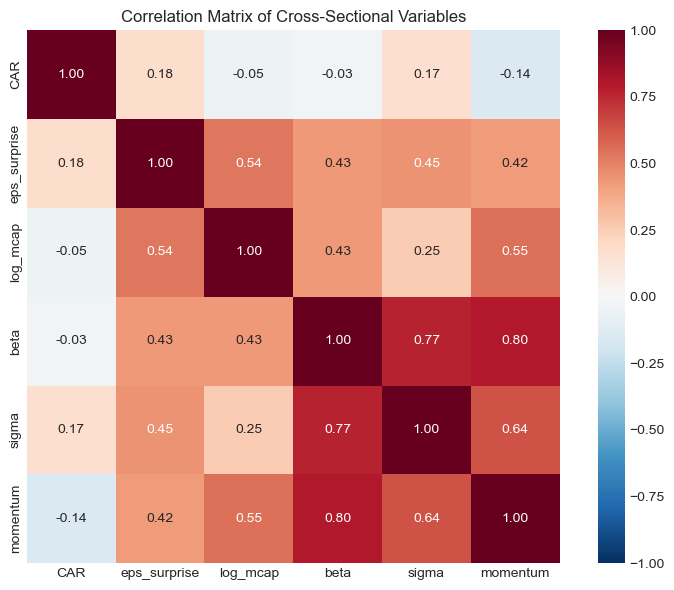

# Correlation matrix

corr_vars = ['CAR', 'eps_surprise', 'log_mcap', 'beta', 'sigma', 'momentum']

corr_matrix = cs_data[corr_vars].corr()

fig, ax = plt.subplots(figsize=(8, 6))

sns.heatmap(corr_matrix, annot=True, fmt='.2f', cmap='RdBu_r', center=0,

vmin=-1, vmax=1, ax=ax, square=True)

ax.set_title('Correlation Matrix of Cross-Sectional Variables', fontsize=12)

plt.tight_layout()

plt.show()

4. Basic OLS Cross-Sectional Regression¶

Model Specification¶

Interpretation¶

: Effect of 1 unit increase in EPS surprise on CAR

: Size effect (do larger firms react differently?)

: Momentum effect (does prior return predict event response?)

Source

def run_cross_sectional_regression(data: pd.DataFrame,

y_var: str,

x_vars: List[str],

add_constant: bool = True) -> sm.regression.linear_model.RegressionResultsWrapper:

"""Run OLS cross-sectional regression."""

y = data[y_var]

X = data[x_vars]

if add_constant:

X = sm.add_constant(X)

model = sm.OLS(y, X).fit()

return model

# Model 1: Simple - EPS Surprise only

print("="*80)

print("MODEL 1: CAR on EPS Surprise")

print("="*80)

model1 = run_cross_sectional_regression(cs_data, 'CAR', ['eps_surprise'])

print(model1.summary())================================================================================

MODEL 1: CAR on EPS Surprise

================================================================================

OLS Regression Results

==============================================================================

Dep. Variable: CAR R-squared: 0.033

Model: OLS Adj. R-squared: -0.011

Method: Least Squares F-statistic: 0.7415

Date: Fri, 23 Jan 2026 Prob (F-statistic): 0.398

Time: 14:23:42 Log-Likelihood: 43.686

No. Observations: 24 AIC: -83.37

Df Residuals: 22 BIC: -81.02

Df Model: 1

Covariance Type: nonrobust

================================================================================

coef std err t P>|t| [0.025 0.975]

--------------------------------------------------------------------------------

const 0.0208 0.010 2.005 0.057 -0.001 0.042

eps_surprise 0.0596 0.069 0.861 0.398 -0.084 0.203

==============================================================================

Omnibus: 3.483 Durbin-Watson: 1.432

Prob(Omnibus): 0.175 Jarque-Bera (JB): 1.391

Skew: -0.040 Prob(JB): 0.499

Kurtosis: 1.823 Cond. No. 8.35

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Source

# Model 2: Add firm characteristics

print("\n" + "="*80)

print("MODEL 2: CAR on EPS Surprise + Firm Characteristics")

print("="*80)

model2 = run_cross_sectional_regression(cs_data, 'CAR',

['eps_surprise', 'log_mcap', 'momentum'])

print(model2.summary())

================================================================================

MODEL 2: CAR on EPS Surprise + Firm Characteristics

================================================================================

OLS Regression Results

==============================================================================

Dep. Variable: CAR R-squared: 0.098

Model: OLS Adj. R-squared: -0.038

Method: Least Squares F-statistic: 0.7205

Date: Fri, 23 Jan 2026 Prob (F-statistic): 0.551

Time: 14:23:43 Log-Likelihood: 44.520

No. Observations: 24 AIC: -81.04

Df Residuals: 20 BIC: -76.33

Df Model: 3

Covariance Type: nonrobust

================================================================================

coef std err t P>|t| [0.025 0.975]

--------------------------------------------------------------------------------

const 0.1237 0.272 0.455 0.654 -0.443 0.691

eps_surprise 0.1095 0.084 1.297 0.210 -0.067 0.286

log_mcap -0.0038 0.010 -0.370 0.716 -0.025 0.018

momentum -0.0757 0.086 -0.876 0.391 -0.256 0.105

==============================================================================

Omnibus: 6.824 Durbin-Watson: 1.516

Prob(Omnibus): 0.033 Jarque-Bera (JB): 1.886

Skew: 0.089 Prob(JB): 0.389

Kurtosis: 1.638 Cond. No. 885.

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Source

# Model 3: Add sector fixed effects

print("\n" + "="*80)

print("MODEL 3: With Sector Fixed Effects")

print("="*80)

# Create sector dummies

cs_data_fe = cs_data.copy()

sector_dummies = pd.get_dummies(cs_data_fe['sector'], prefix='sector', drop_first=True)

cs_data_fe = pd.concat([cs_data_fe, sector_dummies], axis=1)

x_vars_fe = ['eps_surprise', 'log_mcap', 'momentum'] + list(sector_dummies.columns)

model3 = run_cross_sectional_regression(cs_data_fe, 'CAR', x_vars_fe)

print(model3.summary())

================================================================================

MODEL 3: With Sector Fixed Effects

================================================================================

---------------------------------------------------------------------------

ValueError Traceback (most recent call last)

Cell In[26], line 12

9 cs_data_fe = pd.concat([cs_data_fe, sector_dummies], axis=1)

11 x_vars_fe = ['eps_surprise', 'log_mcap', 'momentum'] + list(sector_dummies.columns)

---> 12 model3 = run_cross_sectional_regression(cs_data_fe, 'CAR', np.asarray(x_vars_fe))

13 print(model3.summary())

Cell In[20], line 12, in run_cross_sectional_regression(data, y_var, x_vars, add_constant)

9 if add_constant:

10 X = sm.add_constant(X)

---> 12 model = sm.OLS(y, X).fit()

13 return model

File ~\AppData\Local\anaconda3\Lib\site-packages\statsmodels\regression\linear_model.py:924, in OLS.__init__(self, endog, exog, missing, hasconst, **kwargs)

921 msg = ("Weights are not supported in OLS and will be ignored"

922 "An exception will be raised in the next version.")

923 warnings.warn(msg, ValueWarning)

--> 924 super().__init__(endog, exog, missing=missing,

925 hasconst=hasconst, **kwargs)

926 if "weights" in self._init_keys:

927 self._init_keys.remove("weights")

File ~\AppData\Local\anaconda3\Lib\site-packages\statsmodels\regression\linear_model.py:749, in WLS.__init__(self, endog, exog, weights, missing, hasconst, **kwargs)

747 else:

748 weights = weights.squeeze()

--> 749 super().__init__(endog, exog, missing=missing,

750 weights=weights, hasconst=hasconst, **kwargs)

751 nobs = self.exog.shape[0]

752 weights = self.weights

File ~\AppData\Local\anaconda3\Lib\site-packages\statsmodels\regression\linear_model.py:203, in RegressionModel.__init__(self, endog, exog, **kwargs)

202 def __init__(self, endog, exog, **kwargs):

--> 203 super().__init__(endog, exog, **kwargs)

204 self.pinv_wexog: Float64Array | None = None

205 self._data_attr.extend(['pinv_wexog', 'wendog', 'wexog', 'weights'])

File ~\AppData\Local\anaconda3\Lib\site-packages\statsmodels\base\model.py:270, in LikelihoodModel.__init__(self, endog, exog, **kwargs)

269 def __init__(self, endog, exog=None, **kwargs):

--> 270 super().__init__(endog, exog, **kwargs)

271 self.initialize()

File ~\AppData\Local\anaconda3\Lib\site-packages\statsmodels\base\model.py:95, in Model.__init__(self, endog, exog, **kwargs)

93 missing = kwargs.pop('missing', 'none')

94 hasconst = kwargs.pop('hasconst', None)

---> 95 self.data = self._handle_data(endog, exog, missing, hasconst,

96 **kwargs)

97 self.k_constant = self.data.k_constant

98 self.exog = self.data.exog

File ~\AppData\Local\anaconda3\Lib\site-packages\statsmodels\base\model.py:135, in Model._handle_data(self, endog, exog, missing, hasconst, **kwargs)

134 def _handle_data(self, endog, exog, missing, hasconst, **kwargs):

--> 135 data = handle_data(endog, exog, missing, hasconst, **kwargs)

136 # kwargs arrays could have changed, easier to just attach here

137 for key in kwargs:

File ~\AppData\Local\anaconda3\Lib\site-packages\statsmodels\base\data.py:675, in handle_data(endog, exog, missing, hasconst, **kwargs)

672 exog = np.asarray(exog)

674 klass = handle_data_class_factory(endog, exog)

--> 675 return klass(endog, exog=exog, missing=missing, hasconst=hasconst,

676 **kwargs)

File ~\AppData\Local\anaconda3\Lib\site-packages\statsmodels\base\data.py:84, in ModelData.__init__(self, endog, exog, missing, hasconst, **kwargs)

82 self.orig_endog = endog

83 self.orig_exog = exog

---> 84 self.endog, self.exog = self._convert_endog_exog(endog, exog)

86 self.const_idx = None

87 self.k_constant = 0

File ~\AppData\Local\anaconda3\Lib\site-packages\statsmodels\base\data.py:509, in PandasData._convert_endog_exog(self, endog, exog)

507 exog = exog if exog is None else np.asarray(exog)

508 if endog.dtype == object or exog is not None and exog.dtype == object:

--> 509 raise ValueError("Pandas data cast to numpy dtype of object. "

510 "Check input data with np.asarray(data).")

511 return super()._convert_endog_exog(endog, exog)

ValueError: Pandas data cast to numpy dtype of object. Check input data with np.asarray(data).Source

['eps_surprise', 'log_mcap', 'momentum'] + list(sector_dummies.columns)['eps_surprise',

'log_mcap',

'momentum',

'sector_Finance',

'sector_Healthcare',

'sector_Tech']5. Heteroskedasticity and Robust Standard Errors¶

The Problem¶

In event studies, varies across firms:

Firms with higher idiosyncratic volatility () have noisier CARs

This violates the OLS assumption of homoskedasticity

Testing for Heteroskedasticity¶

Breusch-Pagan test: Tests if variance depends on regressors

White test: More general test for heteroskedasticity

Solutions¶

Robust standard errors (White, 1980): Correct SEs without changing coefficients

Weighted Least Squares (WLS): Weight by inverse variance for efficiency

Source

# Test for heteroskedasticity

print("Heteroskedasticity Tests:")

print("="*60)

# Get residuals from Model 2

y = cs_data['CAR']

X = sm.add_constant(cs_data[['eps_surprise', 'log_mcap', 'momentum']])

# Breusch-Pagan test

bp_lm, bp_pval, bp_f, bp_fpval = het_breuschpagan(model2.resid, X)

print(f"\nBreusch-Pagan Test:")

print(f" LM statistic: {bp_lm:.4f}")

print(f" p-value: {bp_pval:.4f}")

print(f" Conclusion: {'Reject H0 - Heteroskedasticity present' if bp_pval < 0.05 else 'Fail to reject H0'}")

# White test

white_lm, white_pval, white_f, white_fpval = het_white(model2.resid, X)

print(f"\nWhite Test:")

print(f" LM statistic: {white_lm:.4f}")

print(f" p-value: {white_pval:.4f}")

print(f" Conclusion: {'Reject H0 - Heteroskedasticity present' if white_pval < 0.05 else 'Fail to reject H0'}")Heteroskedasticity Tests:

============================================================

Breusch-Pagan Test:

LM statistic: 3.9217

p-value: 0.2700

Conclusion: Fail to reject H0

White Test:

LM statistic: 16.9926

p-value: 0.0488

Conclusion: Reject H0 - Heteroskedasticity present

Source

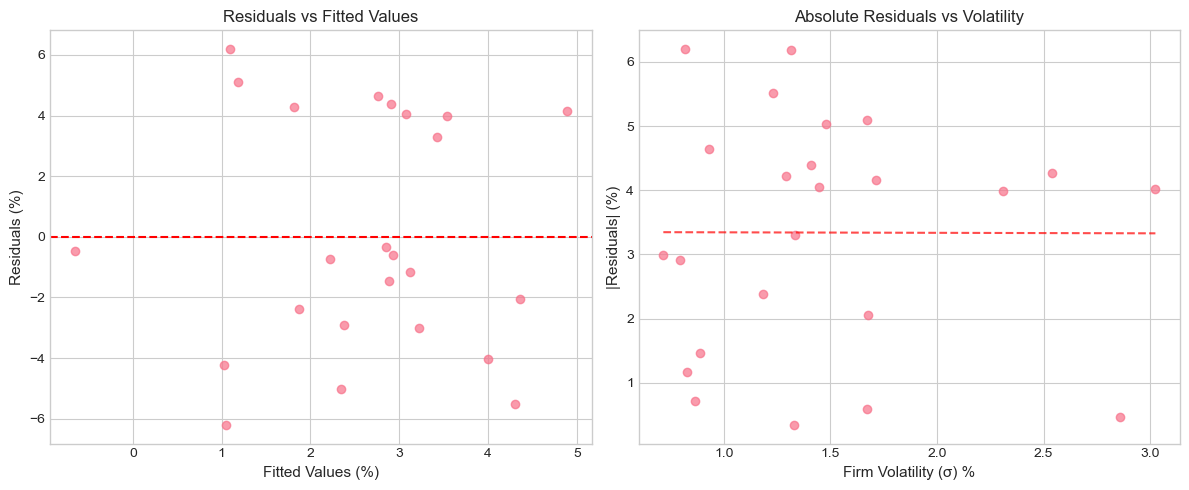

# Visualize heteroskedasticity

fig, axes = plt.subplots(1, 2, figsize=(12, 5))

# Residuals vs Fitted

ax1 = axes[0]

ax1.scatter(model2.fittedvalues*100, model2.resid*100, alpha=0.7)

ax1.axhline(0, color='red', linestyle='--')

ax1.set_xlabel('Fitted Values (%)', fontsize=11)

ax1.set_ylabel('Residuals (%)', fontsize=11)

ax1.set_title('Residuals vs Fitted Values', fontsize=12)

# Residuals vs Sigma (proxy for heteroskedasticity)

ax2 = axes[1]

ax2.scatter(cs_data['sigma']*100, np.abs(model2.resid)*100, alpha=0.7)

z = np.polyfit(cs_data['sigma']*100, np.abs(model2.resid)*100, 1)

p = np.poly1d(z)

x_line = np.linspace(cs_data['sigma'].min()*100, cs_data['sigma'].max()*100, 100)

ax2.plot(x_line, p(x_line), 'r--', alpha=0.7)

ax2.set_xlabel('Firm Volatility (σ) %', fontsize=11)

ax2.set_ylabel('|Residuals| (%)', fontsize=11)

ax2.set_title('Absolute Residuals vs Volatility', fontsize=12)

plt.tight_layout()

plt.show()

print("\nNote: If residuals spread out with volatility, we have heteroskedasticity.")

Note: If residuals spread out with volatility, we have heteroskedasticity.

Source

# Compare OLS with Robust Standard Errors

print("\n" + "="*80)

print("COMPARISON: OLS vs Robust Standard Errors")

print("="*80)

# OLS with robust SEs (HC1 = White's heteroskedasticity-consistent)

model2_robust = run_cross_sectional_regression(cs_data, 'CAR',

['eps_surprise', 'log_mcap', 'momentum'])

model2_robust_hc = model2_robust.get_robustcov_results(cov_type='HC1')

# Create comparison table

comparison = pd.DataFrame({

'Variable': model2.params.index,

'Coef': model2.params.values,

'OLS SE': model2.bse.values,

'OLS t-stat': model2.tvalues.values,

'Robust SE': model2_robust_hc.bse,

'Robust t-stat': model2_robust_hc.tvalues,

})

comparison['SE Change'] = (comparison['Robust SE'] / comparison['OLS SE'] - 1) * 100

print("\nCoefficient Comparison:")

for col in ['Coef', 'OLS SE', 'Robust SE']:

comparison[col] = comparison[col].apply(lambda x: f"{x:.6f}")

for col in ['OLS t-stat', 'Robust t-stat']:

comparison[col] = comparison[col].apply(lambda x: f"{x:.3f}")

comparison['SE Change'] = comparison['SE Change'].apply(lambda x: f"{x:+.1f}%")

print(comparison.to_string(index=False))

print("\nNote: Positive SE Change means robust SEs are larger (more conservative).")

================================================================================

COMPARISON: OLS vs Robust Standard Errors

================================================================================

Coefficient Comparison:

Variable Coef OLS SE OLS t-stat Robust SE Robust t-stat SE Change

const 0.123684 0.271768 0.455 0.324222 0.381 +19.3%

eps_surprise 0.109478 0.084438 1.297 0.098625 1.110 +16.8%

log_mcap -0.003781 0.010230 -0.370 0.012309 -0.307 +20.3%

momentum -0.075711 0.086403 -0.876 0.072240 -1.048 -16.4%

Note: Positive SE Change means robust SEs are larger (more conservative).

6. Weighted Least Squares (WLS)¶

Motivation¶

When we know the variance structure, WLS is more efficient than OLS with robust SEs.

Weights in Event Studies¶

Natural weight: inverse of CAR variance

Where is the event window length and is firm i’s residual volatility.

WLS Estimator¶

Where

Source

def run_wls_regression(data: pd.DataFrame,

y_var: str,

x_vars: List[str],

weight_var: str) -> sm.regression.linear_model.RegressionResultsWrapper:

"""Run Weighted Least Squares regression."""

y = data[y_var]

X = sm.add_constant(data[x_vars])

# Weights = 1/variance (inverse variance weighting)

weights = 1 / data[weight_var]

model = sm.WLS(y, X, weights=weights).fit()

return model

# Run WLS

print("="*80)

print("WEIGHTED LEAST SQUARES (Inverse Variance Weighting)")

print("="*80)

model_wls = run_wls_regression(cs_data, 'CAR',

['eps_surprise', 'log_mcap', 'momentum'],

'car_var')

print(model_wls.summary())================================================================================

WEIGHTED LEAST SQUARES (Inverse Variance Weighting)

================================================================================

WLS Regression Results

==============================================================================

Dep. Variable: CAR R-squared: 0.160

Model: WLS Adj. R-squared: 0.034

Method: Least Squares F-statistic: 1.272

Date: Fri, 23 Jan 2026 Prob (F-statistic): 0.311

Time: 14:25:56 Log-Likelihood: 43.066

No. Observations: 24 AIC: -78.13

Df Residuals: 20 BIC: -73.42

Df Model: 3

Covariance Type: nonrobust

================================================================================

coef std err t P>|t| [0.025 0.975]

--------------------------------------------------------------------------------

const 0.2094 0.281 0.745 0.465 -0.377 0.796

eps_surprise 0.1243 0.105 1.184 0.250 -0.095 0.343

log_mcap -0.0073 0.011 -0.692 0.497 -0.029 0.015

momentum -0.1302 0.124 -1.047 0.307 -0.390 0.129

==============================================================================

Omnibus: 1.108 Durbin-Watson: 1.225

Prob(Omnibus): 0.575 Jarque-Bera (JB): 0.821

Skew: 0.025 Prob(JB): 0.663

Kurtosis: 2.095 Cond. No. 1.01e+03

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 1.01e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

Source

# Compare OLS, Robust OLS, and WLS

print("\n" + "="*80)

print("COMPARISON: OLS vs Robust OLS vs WLS")

print("="*80)

# Create comprehensive comparison

vars_to_compare = ['const', 'eps_surprise', 'log_mcap', 'momentum']

comparison_full = pd.DataFrame({

'Variable': vars_to_compare,

'OLS Coef': [model2.params[v] for v in vars_to_compare],

'OLS t': [model2.tvalues[v] for v in vars_to_compare],

'Robust t': [model2_robust_hc.tvalues[v] for v in range(len(vars_to_compare))],

'WLS Coef': [model_wls.params[v] for v in vars_to_compare],

'WLS t': [model_wls.tvalues[v] for v in vars_to_compare],

})

def sig(t, df=20):

p = 2 * (1 - stats.t.cdf(abs(t), df))

if p < 0.01: return '***'

elif p < 0.05: return '**'

elif p < 0.10: return '*'

return ''

print("\n" + "-"*80)

print(f"{'Variable':<15} {'OLS Coef':>12} {'OLS t':>10} {'Robust t':>10} {'WLS Coef':>12} {'WLS t':>10}")

print("-"*80)

for _, row in comparison_full.iterrows():

print(f"{row['Variable']:<15} {row['OLS Coef']:>12.6f} {row['OLS t']:>8.2f}{sig(row['OLS t']):2s} "

f"{row['Robust t']:>8.2f}{sig(row['Robust t']):2s} {row['WLS Coef']:>12.6f} {row['WLS t']:>8.2f}{sig(row['WLS t']):2s}")

print("-"*80)

print(f"{'R-squared':<15} {model2.rsquared:>12.4f} {'':<22} {model_wls.rsquared:>12.4f}")

print(f"{'N':<15} {int(model2.nobs):>12} {'':<22} {int(model_wls.nobs):>12}")

print("\nSignificance: *** p<0.01, ** p<0.05, * p<0.10")

================================================================================

COMPARISON: OLS vs Robust OLS vs WLS

================================================================================

--------------------------------------------------------------------------------

Variable OLS Coef OLS t Robust t WLS Coef WLS t

--------------------------------------------------------------------------------

const 0.123684 0.46 0.38 0.209434 0.75

eps_surprise 0.109478 1.30 1.11 0.124321 1.18

log_mcap -0.003781 -0.37 -0.31 -0.007280 -0.69

momentum -0.075711 -0.88 -1.05 -0.130245 -1.05

--------------------------------------------------------------------------------

R-squared 0.0975 0.1602

N 24 24

Significance: *** p<0.01, ** p<0.05, * p<0.10

7. Multicollinearity Diagnostics¶

Why It Matters¶

If explanatory variables are highly correlated:

Coefficient estimates become unstable

Standard errors inflate

Hard to isolate individual effects

Variance Inflation Factor (VIF)¶

Where is from regressing on all other X variables.

Rule of thumb: VIF > 10 suggests serious multicollinearity

Source

def calculate_vif(data: pd.DataFrame, variables: List[str]) -> pd.DataFrame:

"""Calculate Variance Inflation Factors."""

X = data[variables]

X = sm.add_constant(X)

vif_data = []

for i, var in enumerate(X.columns):

if var == 'const':

continue

vif = variance_inflation_factor(X.values, i)

vif_data.append({'Variable': var, 'VIF': vif})

return pd.DataFrame(vif_data)

# Calculate VIFs

print("Multicollinearity Diagnostics:")

print("="*50)

vif_df = calculate_vif(cs_data, ['eps_surprise', 'log_mcap', 'momentum', 'beta', 'sigma'])

vif_df['VIF'] = vif_df['VIF'].apply(lambda x: f"{x:.2f}")

vif_df['Concern'] = vif_df['VIF'].apply(lambda x: 'High' if float(x) > 10 else 'Moderate' if float(x) > 5 else 'Low')

print("\nVariance Inflation Factors:")

print(vif_df.to_string(index=False))

print("\nRule of thumb: VIF > 10 indicates serious multicollinearity")Multicollinearity Diagnostics:

==================================================

Variance Inflation Factors:

Variable VIF Concern

eps_surprise 1.66 Low

log_mcap 1.88 Low

momentum 3.27 Low

beta 4.11 Low

sigma 2.82 Low

Rule of thumb: VIF > 10 indicates serious multicollinearity

8. Interaction Effects¶

Research Question¶

Does the earnings surprise effect vary by firm size? Perhaps smaller firms react more strongly to surprises.

Model with Interaction¶

: Larger firms react less to surprises

: Larger firms react more to surprises

Source

# Create interaction term

cs_data['surprise_x_size'] = cs_data['eps_surprise'] * cs_data['log_mcap']

# Model with interaction

print("="*80)

print("MODEL WITH INTERACTION: Does Surprise Effect Vary by Size?")

print("="*80)

model_interact = run_cross_sectional_regression(

cs_data, 'CAR',

['eps_surprise', 'log_mcap', 'surprise_x_size', 'momentum']

)

print(model_interact.summary())================================================================================

MODEL WITH INTERACTION: Does Surprise Effect Vary by Size?

================================================================================

OLS Regression Results

==============================================================================

Dep. Variable: CAR R-squared: 0.120

Model: OLS Adj. R-squared: -0.065

Method: Least Squares F-statistic: 0.6485

Date: Fri, 23 Jan 2026 Prob (F-statistic): 0.635

Time: 14:27:01 Log-Likelihood: 44.824

No. Observations: 24 AIC: -79.65

Df Residuals: 19 BIC: -73.76

Df Model: 4

Covariance Type: nonrobust

===================================================================================

coef std err t P>|t| [0.025 0.975]

-----------------------------------------------------------------------------------

const 0.2542 0.333 0.764 0.454 -0.442 0.951

eps_surprise -1.1918 1.865 -0.639 0.530 -5.096 2.712

log_mcap -0.0086 0.012 -0.691 0.498 -0.035 0.017

surprise_x_size 0.0469 0.067 0.698 0.493 -0.094 0.188

momentum -0.0772 0.088 -0.881 0.389 -0.260 0.106

==============================================================================

Omnibus: 8.908 Durbin-Watson: 1.659

Prob(Omnibus): 0.012 Jarque-Bera (JB): 2.088

Skew: 0.065 Prob(JB): 0.352

Kurtosis: 1.561 Cond. No. 5.96e+03

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 5.96e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

Source

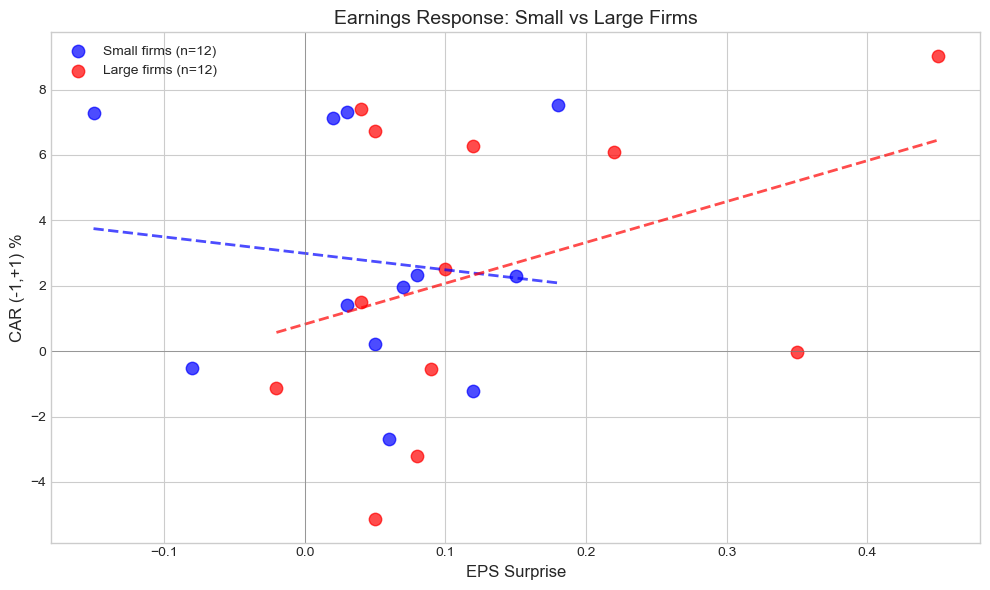

# Visualize interaction effect

fig, ax = plt.subplots(figsize=(10, 6))

# Split by size (median)

median_mcap = cs_data['log_mcap'].median()

small = cs_data[cs_data['log_mcap'] < median_mcap]

large = cs_data[cs_data['log_mcap'] >= median_mcap]

# Scatter plots

ax.scatter(small['eps_surprise'], small['CAR']*100, color='blue', alpha=0.7,

s=80, label=f'Small firms (n={len(small)})')

ax.scatter(large['eps_surprise'], large['CAR']*100, color='red', alpha=0.7,

s=80, label=f'Large firms (n={len(large)})')

# Separate regression lines

for data, color, label in [(small, 'blue', 'Small'), (large, 'red', 'Large')]:

if len(data) > 2:

z = np.polyfit(data['eps_surprise'], data['CAR']*100, 1)

p = np.poly1d(z)

x_line = np.linspace(data['eps_surprise'].min(), data['eps_surprise'].max(), 100)

ax.plot(x_line, p(x_line), f'{color[0]}--', linewidth=2, alpha=0.7)

ax.axhline(0, color='gray', linestyle='-', linewidth=0.5)

ax.axvline(0, color='gray', linestyle='-', linewidth=0.5)

ax.set_xlabel('EPS Surprise', fontsize=12)

ax.set_ylabel('CAR (-1,+1) %', fontsize=12)

ax.set_title('Earnings Response: Small vs Large Firms', fontsize=14)

ax.legend()

plt.tight_layout()

plt.show()

# Report slope differences

if len(small) > 2 and len(large) > 2:

slope_small = np.polyfit(small['eps_surprise'], small['CAR'], 1)[0]

slope_large = np.polyfit(large['eps_surprise'], large['CAR'], 1)[0]

print(f"\nEarnings Response Coefficient:")

print(f" Small firms: {slope_small:.4f} ({slope_small*100:.2f}% CAR per unit surprise)")

print(f" Large firms: {slope_large:.4f} ({slope_large*100:.2f}% CAR per unit surprise)")

Earnings Response Coefficient:

Small firms: -0.0503 (-5.03% CAR per unit surprise)

Large firms: 0.1251 (12.51% CAR per unit surprise)

9. Subsample Analysis¶

Splitting the Sample¶

Sometimes relationships differ across subgroups:

Positive vs negative surprises

Different sectors

Different time periods

Source

# Subsample: Positive vs Negative Surprises

print("="*80)

print("SUBSAMPLE ANALYSIS: Positive vs Negative Surprises")

print("="*80)

pos_surprise = cs_data[cs_data['eps_surprise'] > 0]

neg_surprise = cs_data[cs_data['eps_surprise'] <= 0]

print(f"\nPositive surprises: n={len(pos_surprise)}, Mean CAR={pos_surprise['CAR'].mean()*100:.2f}%")

print(f"Negative surprises: n={len(neg_surprise)}, Mean CAR={neg_surprise['CAR'].mean()*100:.2f}%")

# Run regressions on subsamples

if len(pos_surprise) > 5:

model_pos = run_cross_sectional_regression(pos_surprise, 'CAR', ['eps_surprise', 'log_mcap'])

print(f"\nPositive Surprise Subsample:")

print(f" EPS coefficient: {model_pos.params['eps_surprise']:.4f} (t={model_pos.tvalues['eps_surprise']:.2f})")

if len(neg_surprise) > 5:

model_neg = run_cross_sectional_regression(neg_surprise, 'CAR', ['eps_surprise', 'log_mcap'])

print(f"\nNegative Surprise Subsample:")

print(f" EPS coefficient: {model_neg.params['eps_surprise']:.4f} (t={model_neg.tvalues['eps_surprise']:.2f})")================================================================================

SUBSAMPLE ANALYSIS: Positive vs Negative Surprises

================================================================================

Positive surprises: n=21, Mean CAR=2.71%

Negative surprises: n=3, Mean CAR=1.88%

Positive Surprise Subsample:

EPS coefficient: 0.1402 (t=1.48)

Source

# Subsample: By Sector

print("\n" + "="*80)

print("SUBSAMPLE ANALYSIS: By Sector")

print("="*80)

sector_results = []

for sector in cs_data['sector'].unique():

sector_data = cs_data[cs_data['sector'] == sector]

if len(sector_data) >= 4:

try:

model = run_cross_sectional_regression(sector_data, 'CAR', ['eps_surprise'])

sector_results.append({

'Sector': sector,

'N': len(sector_data),

'Mean CAR': sector_data['CAR'].mean(),

'EPS Coef': model.params['eps_surprise'],

't-stat': model.tvalues['eps_surprise'],

'R-squared': model.rsquared

})

except:

pass

sector_df = pd.DataFrame(sector_results)

sector_df['Mean CAR'] = sector_df['Mean CAR'].apply(lambda x: f"{x*100:.2f}%")

sector_df['EPS Coef'] = sector_df['EPS Coef'].apply(lambda x: f"{x:.4f}")

sector_df['t-stat'] = sector_df['t-stat'].apply(lambda x: f"{x:.2f}")

sector_df['R-squared'] = sector_df['R-squared'].apply(lambda x: f"{x:.3f}")

print("\nEarnings Response by Sector:")

print(sector_df.to_string(index=False))

================================================================================

SUBSAMPLE ANALYSIS: By Sector

================================================================================

Earnings Response by Sector:

Sector N Mean CAR EPS Coef t-stat R-squared

Tech 10 1.91% 0.2184 2.26 0.389

Finance 4 4.86% -0.1867 -1.63 0.572

Healthcare 5 3.91% 0.0405 0.12 0.004

Consumer 5 0.91% -0.2298 -1.10 0.286

10. Standardized CAR Regressions¶

Alternative Approach¶

Instead of using CAR as dependent variable, use Standardized CAR (SCAR):

This makes the dependent variable unit-free and comparable across firms with different volatilities.

Source

# Create SCAR variable

cs_data['SCAR'] = cs_data['CAR'] / cs_data['car_se']

print("="*80)

print("SCAR REGRESSION (Standardized Dependent Variable)")

print("="*80)

model_scar = run_cross_sectional_regression(cs_data, 'SCAR',

['eps_surprise', 'log_mcap', 'momentum'])

print(model_scar.summary())================================================================================

SCAR REGRESSION (Standardized Dependent Variable)

================================================================================

OLS Regression Results

==============================================================================

Dep. Variable: SCAR R-squared: 0.115

Model: OLS Adj. R-squared: -0.017

Method: Least Squares F-statistic: 0.8685

Date: Fri, 23 Jan 2026 Prob (F-statistic): 0.474

Time: 14:27:18 Log-Likelihood: -46.455

No. Observations: 24 AIC: 100.9

Df Residuals: 20 BIC: 105.6

Df Model: 3

Covariance Type: nonrobust

================================================================================

coef std err t P>|t| [0.025 0.975]

--------------------------------------------------------------------------------

const 7.3942 12.035 0.614 0.546 -17.710 32.498

eps_surprise 3.5539 3.739 0.950 0.353 -4.246 11.354

log_mcap -0.2378 0.453 -0.525 0.605 -1.183 0.707

momentum -4.3966 3.826 -1.149 0.264 -12.378 3.585

==============================================================================

Omnibus: 0.047 Durbin-Watson: 1.264

Prob(Omnibus): 0.977 Jarque-Bera (JB): 0.213

Skew: -0.087 Prob(JB): 0.899

Kurtosis: 2.572 Cond. No. 885.

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Source

# Compare CAR vs SCAR regressions

print("\n" + "="*70)

print("COMPARISON: CAR vs SCAR as Dependent Variable")

print("="*70)

print("\nNote: SCAR regression gives t-statistics directly comparable to")

print("standardized test statistics from Sessions 4-5.")

print(f"\nMean SCAR in sample: {cs_data['SCAR'].mean():.3f}")

print(f"Std SCAR: {cs_data['SCAR'].std():.3f}")

print(f"\nIf SCAR ~ N(0,1) under null, mean significantly > 0 indicates positive abnormal returns.")

======================================================================

COMPARISON: CAR vs SCAR as Dependent Variable

======================================================================

Note: SCAR regression gives t-statistics directly comparable to

standardized test statistics from Sessions 4-5.

Mean SCAR in sample: 0.985

Std SCAR: 1.821

If SCAR ~ N(0,1) under null, mean significantly > 0 indicates positive abnormal returns.

11. Addressing Potential Endogeneity¶

The Problem¶

In some event studies, explanatory variables may be endogenous:

Reverse causality: Does the event response cause the characteristic?

Omitted variables: Unobserved factors affecting both X and CAR

Measurement error: Noisy proxies for true variables

Example: Earnings Surprise¶

Management may manage earnings based on expected market reaction

Analysts may adjust forecasts based on anticipated news

Solutions¶

Use lagged/predetermined variables: Characteristics measured before event

Instrumental Variables: Find exogenous instruments

Natural experiments: Events that are plausibly exogenous

Source

# Demonstrate using pre-determined variables

print("="*80)

print("ADDRESSING ENDOGENEITY: Using Pre-Determined Variables")

print("="*80)

print("\nVariables in our model and their timing:")

print("-" * 60)

print(" eps_surprise: Realized at event (potentially endogenous)")

print(" log_mcap: Measured before event (pre-determined)")

print(" momentum: 60-day pre-event return (pre-determined)")

print(" beta: Estimated from pre-event data (pre-determined)")

print(" sigma: Estimated from pre-event data (pre-determined)")

# Model using only pre-determined variables

print("\nModel with only pre-determined variables:")

model_predet = run_cross_sectional_regression(cs_data, 'CAR',

['log_mcap', 'momentum', 'beta', 'sigma'])

print(f"R-squared: {model_predet.rsquared:.4f}")

print(f"\nNote: Low R-squared without eps_surprise suggests surprise")

print(" is the main driver, as expected for earnings announcements.")================================================================================

ADDRESSING ENDOGENEITY: Using Pre-Determined Variables

================================================================================

Variables in our model and their timing:

------------------------------------------------------------

eps_surprise: Realized at event (potentially endogenous)

log_mcap: Measured before event (pre-determined)

momentum: 60-day pre-event return (pre-determined)

beta: Estimated from pre-event data (pre-determined)

sigma: Estimated from pre-event data (pre-determined)

Model with only pre-determined variables:

R-squared: 0.1461

Note: Low R-squared without eps_surprise suggests surprise

is the main driver, as expected for earnings announcements.

12. Publication-Ready Results¶

Source

def create_regression_table(models: List, model_names: List[str],

var_order: List[str]) -> pd.DataFrame:

"""Create publication-style regression table."""

rows = []

for var in var_order:

coef_row = {'Variable': var}

se_row = {'Variable': ''}

for model, name in zip(models, model_names):

if var in model.params.index:

coef = model.params[var]

se = model.bse[var]

t = model.tvalues[var]

p = model.pvalues[var]

sig = '***' if p < 0.01 else '**' if p < 0.05 else '*' if p < 0.10 else ''

coef_row[name] = f"{coef:.4f}{sig}"

se_row[name] = f"({se:.4f})"

else:

coef_row[name] = ''

se_row[name] = ''

rows.append(coef_row)

rows.append(se_row)

# Add statistics

rows.append({'Variable': ''})

r2_row = {'Variable': 'R-squared'}

n_row = {'Variable': 'N'}

for model, name in zip(models, model_names):

r2_row[name] = f"{model.rsquared:.3f}"

n_row[name] = f"{int(model.nobs)}"

rows.append(r2_row)

rows.append(n_row)

return pd.DataFrame(rows)

# Create table

print("\n" + "="*90)

print("TABLE: Cross-Sectional Determinants of Earnings Announcement Returns")

print("="*90)

print("Dependent Variable: CAR(-1,+1)")

print("-"*90)

models = [model1, model2, model_wls, model_interact]

names = ['(1)', '(2) OLS', '(3) WLS', '(4) Interact']

var_order = ['const', 'eps_surprise', 'log_mcap', 'momentum', 'surprise_x_size']

table = create_regression_table(models, names, var_order)

print(table.to_string(index=False))

print("-"*90)

print("Standard errors in parentheses. *** p<0.01, ** p<0.05, * p<0.10")

print("WLS uses inverse CAR variance as weights.")

==========================================================================================

TABLE: Cross-Sectional Determinants of Earnings Announcement Returns

==========================================================================================

Dependent Variable: CAR(-1,+1)

------------------------------------------------------------------------------------------

Variable (1) (2) OLS (3) WLS (4) Interact

const 0.0208* 0.1237 0.2094 0.2542

(0.0104) (0.2718) (0.2810) (0.3328)

eps_surprise 0.0596 0.1095 0.1243 -1.1918

(0.0692) (0.0844) (0.1050) (1.8653)

log_mcap -0.0038 -0.0073 -0.0086

(0.0102) (0.0105) (0.0125)

momentum -0.0757 -0.1302 -0.0772

(0.0864) (0.1244) (0.0876)

surprise_x_size 0.0469

(0.0672)

NaN NaN NaN NaN

R-squared 0.033 0.098 0.160 0.120

N 24 24 24 24

------------------------------------------------------------------------------------------

Standard errors in parentheses. *** p<0.01, ** p<0.05, * p<0.10

WLS uses inverse CAR variance as weights.

13. Exercises¶

Exercise 1: Additional Variables¶

Add analyst coverage (number of analysts) as an explanatory variable. Does it affect the earnings response?

Exercise 2: Non-Linear Effects¶

Test for non-linear effects by adding squared terms or using splines.

Exercise 3: Clustered Standard Errors¶

Implement standard errors clustered by sector or event date.

Source

# Exercise 3: Clustered Standard Errors

print("Exercise 3: Clustered Standard Errors")

print("="*60)

# Cluster by sector

y = cs_data['CAR']

X = sm.add_constant(cs_data[['eps_surprise', 'log_mcap', 'momentum']])

# OLS with clustered SEs by sector

model_cluster = sm.OLS(y, X).fit(cov_type='cluster',

cov_kwds={'groups': cs_data['sector']})

print("\nOLS with Standard Errors Clustered by Sector:")

print("-"*60)

print(f"{'Variable':<15} {'Coef':>12} {'Clustered SE':>14} {'t-stat':>10}")

print("-"*60)

for var in model_cluster.params.index:

coef = model_cluster.params[var]

se = model_cluster.bse[var]

t = model_cluster.tvalues[var]

print(f"{var:<15} {coef:>12.6f} {se:>14.6f} {t:>10.2f}")Exercise 3: Clustered Standard Errors

============================================================

OLS with Standard Errors Clustered by Sector:

------------------------------------------------------------

Variable Coef Clustered SE t-stat

------------------------------------------------------------

const 0.123684 0.239558 0.52

eps_surprise 0.109478 0.110609 0.99

log_mcap -0.003781 0.009481 -0.40

momentum -0.075711 0.059479 -1.27

14. Summary¶

Key Takeaways¶

Cross-sectional analysis reveals why events affect firms differently

Heteroskedasticity is common in event studies; use robust SEs or WLS

WLS with inverse variance weights is efficient when variance structure is known

Check for multicollinearity using VIF before interpreting coefficients

Interaction effects can reveal whether relationships vary across subgroups

Endogeneity may bias results; use pre-determined variables when possible

Best Practices¶

Report both OLS and robust SEs

Consider WLS when variance estimates are reliable

Test for heteroskedasticity explicitly

Run subsample analyses for robustness

Be cautious about endogeneity in event characteristics

Coming Up Next¶

Session 7: Long-Horizon Event Studies will cover:

Calendar-time portfolio approach

Buy-and-hold abnormal returns (BHAR)

Dealing with overlapping events

Power issues in long-horizon studies

References¶

White, H. (1980). A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity. Econometrica, 48(4), 817-838.

MacKinnon, J. G., & White, H. (1985). Some heteroskedasticity-consistent covariance matrix estimators with improved finite sample properties. Journal of Econometrics, 29(3), 305-325.

Kothari, S. P., & Warner, J. B. (2007). Econometrics of event studies. Handbook of Corporate Finance, 1, 3-36.

Prabhala, N. R. (1997). Conditional methods in event studies and an equilibrium justification for standard event-study procedures. Review of Financial Studies, 10(1), 1-38.