Session 9: Event Study Design and Implementation

Event Studies in Finance and Economics - Summer School¶

Learning Objectives¶

By the end of this session, you will be able to:

Design a complete event study from research question to publication

Handle common data issues and edge cases

Build a reusable event study framework in Python

Implement comprehensive robustness checks

Create publication-ready tables and figures

Avoid common pitfalls and errors

1. The Event Study Research Process¶

Overview¶

┌─────────────────────────────────────────────────────────────────┐

│ 1. Research Question → 2. Event Identification → │

│ 3. Data Collection → 4. Methodology Selection → │

│ 5. Implementation → 6. Robustness Checks → │

│ 7. Interpretation → 8. Reporting │

└─────────────────────────────────────────────────────────────────┘Key Design Decisions¶

| Decision | Options | Considerations |

|---|---|---|

| Event window | Short (3-5 days) vs Long (months) | Market efficiency, noise |

| Estimation window | 100-250 days | Stability, stationarity |

| Expected return model | Market, FF3, FF5 | Data availability, fit |

| Test statistics | Parametric vs Non-parametric | Distribution assumptions |

| Aggregation | Equally vs Value-weighted | Research question |

Source

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

from scipy import stats

import yfinance as yf

import statsmodels.api as sm

from datetime import datetime, timedelta

from dataclasses import dataclass, field

from typing import List, Dict, Optional, Tuple, Union

from enum import Enum

import warnings

warnings.filterwarnings('ignore')

plt.style.use('seaborn-v0_8-whitegrid')

sns.set_palette("husl")

print("Libraries loaded!")Libraries loaded!

2. Building a Comprehensive Event Study Framework¶

Design Principles¶

Modularity: Separate data, estimation, and testing

Flexibility: Support multiple models and tests

Robustness: Handle edge cases gracefully

Reproducibility: Clear parameters and logging

Source

class ExpectedReturnModel(Enum):

"""Supported expected return models."""

MARKET_MODEL = "market_model"

MARKET_ADJUSTED = "market_adjusted"

MEAN_ADJUSTED = "mean_adjusted"

FAMA_FRENCH_3 = "fama_french_3"

@dataclass

class EventStudyConfig:

"""Configuration for event study."""

# Window parameters

estimation_window: int = 120

gap: int = 10

event_window_pre: int = 5

event_window_post: int = 5

# Model selection

expected_return_model: ExpectedReturnModel = ExpectedReturnModel.MARKET_MODEL

# Data requirements

min_estimation_obs: int = 60

min_event_obs: int = 3

# Market index

market_index: str = "^GSPC"

# Test settings

confidence_level: float = 0.95

def __post_init__(self):

"""Validate configuration."""

assert self.estimation_window >= self.min_estimation_obs, \

f"Estimation window must be >= {self.min_estimation_obs}"

assert self.gap >= 0, "Gap must be non-negative"

assert 0 < self.confidence_level < 1, "Confidence level must be in (0, 1)"

@dataclass

class EventData:

"""Container for single event data."""

ticker: str

event_date: pd.Timestamp

event_description: str = ""

metadata: Dict = field(default_factory=dict)

@dataclass

class EstimationResult:

"""Results from estimation period."""

alpha: float

beta: float

sigma: float

r_squared: float

n_obs: int

residuals: np.ndarray

@dataclass

class EventResult:

"""Complete results for a single event."""

event: EventData

config: EventStudyConfig

estimation: EstimationResult

event_data: pd.DataFrame

valid: bool = True

error_message: str = ""

def get_car(self, tau1: int, tau2: int) -> float:

"""Calculate CAR for specified window."""

mask = (self.event_data['event_time'] >= tau1) & (self.event_data['event_time'] <= tau2)

return self.event_data.loc[mask, 'AR'].sum()

def get_car_variance(self, tau1: int, tau2: int) -> float:

"""Calculate CAR variance."""

L = len(self.event_data[(self.event_data['event_time'] >= tau1) &

(self.event_data['event_time'] <= tau2)])

return L * self.estimation.sigma ** 2

def get_scar(self, tau1: int, tau2: int) -> float:

"""Calculate Standardized CAR."""

car = self.get_car(tau1, tau2)

var = self.get_car_variance(tau1, tau2)

return car / np.sqrt(var) if var > 0 else np.nan

print("Event study classes defined!")Event study classes defined!

Source

class EventStudyEngine:

"""

Comprehensive event study implementation.

Supports multiple expected return models, test statistics,

and handles common data issues.

"""

def __init__(self, config: EventStudyConfig):

self.config = config

self._market_data_cache = {}

self._ff_data_cache = None

def _download_market_data(self, start_date: pd.Timestamp,

end_date: pd.Timestamp) -> pd.Series:

"""Download and cache market data."""

cache_key = (start_date.strftime('%Y-%m-%d'), end_date.strftime('%Y-%m-%d'))

if cache_key not in self._market_data_cache:

market = yf.download(self.config.market_index,

start=start_date, end=end_date,

progress=False)['Close']

self._market_data_cache[cache_key] = market.squeeze().pct_change().dropna()

return self._market_data_cache[cache_key]

def _download_stock_data(self, ticker: str, start_date: pd.Timestamp,

end_date: pd.Timestamp) -> pd.Series:

"""Download stock data."""

stock = yf.download(ticker, start=start_date, end=end_date,

progress=False)['Close']

return stock.squeeze().pct_change().dropna()

def _estimate_market_model(self, stock_returns: pd.Series,

market_returns: pd.Series) -> EstimationResult:

"""Estimate market model parameters."""

# Align data

common_idx = stock_returns.index.intersection(market_returns.index)

y = stock_returns.loc[common_idx]

x = market_returns.loc[common_idx]

if len(y) < self.config.min_estimation_obs:

raise ValueError(f"Insufficient observations: {len(y)} < {self.config.min_estimation_obs}")

X = sm.add_constant(x)

model = sm.OLS(y, X).fit()

return EstimationResult(

alpha=model.params.iloc[0],

beta=model.params.iloc[1],

sigma=np.std(model.resid, ddof=2),

r_squared=model.rsquared,

n_obs=len(y),

residuals=model.resid.values

)

def _estimate_mean_adjusted(self, stock_returns: pd.Series) -> EstimationResult:

"""Estimate mean-adjusted model."""

if len(stock_returns) < self.config.min_estimation_obs:

raise ValueError(f"Insufficient observations")

mean_return = stock_returns.mean()

residuals = stock_returns - mean_return

return EstimationResult(

alpha=mean_return,

beta=0.0,

sigma=stock_returns.std(),

r_squared=0.0,

n_obs=len(stock_returns),

residuals=residuals.values

)

def _calculate_expected_returns(self, estimation: EstimationResult,

market_returns: pd.Series) -> pd.Series:

"""Calculate expected returns based on model."""

if self.config.expected_return_model == ExpectedReturnModel.MARKET_MODEL:

return estimation.alpha + estimation.beta * market_returns

elif self.config.expected_return_model == ExpectedReturnModel.MARKET_ADJUSTED:

return market_returns

elif self.config.expected_return_model == ExpectedReturnModel.MEAN_ADJUSTED:

return pd.Series(estimation.alpha, index=market_returns.index)

else:

raise ValueError(f"Unsupported model: {self.config.expected_return_model}")

def process_event(self, event: EventData) -> EventResult:

"""

Process a single event.

Returns EventResult with valid=False if processing fails.

"""

try:

# Calculate date ranges

total_pre_days = self.config.estimation_window + self.config.gap + self.config.event_window_pre

start_date = event.event_date - timedelta(days=int(total_pre_days * 1.5))

end_date = event.event_date + timedelta(days=int(self.config.event_window_post * 2.5))

# Download data

stock_returns = self._download_stock_data(event.ticker, start_date, end_date)

market_returns = self._download_market_data(start_date, end_date)

# Align and create DataFrame

common_idx = stock_returns.index.intersection(market_returns.index)

df = pd.DataFrame({

'stock_ret': stock_returns.loc[common_idx],

'market_ret': market_returns.loc[common_idx]

})

# Find event date in data

if event.event_date not in df.index:

idx = df.index.get_indexer([event.event_date], method='nearest')[0]

if idx < 0 or idx >= len(df):

raise ValueError("Event date not found in data")

actual_event_date = df.index[idx]

else:

actual_event_date = event.event_date

event_idx = df.index.get_loc(actual_event_date)

# Create event time

df['event_time'] = range(-event_idx, len(df) - event_idx)

# Split into estimation and event periods

est_end = -(self.config.gap + self.config.event_window_pre)

est_start = est_end - self.config.estimation_window

est_mask = (df['event_time'] >= est_start) & (df['event_time'] < est_end)

evt_mask = (df['event_time'] >= -self.config.event_window_pre) & \

(df['event_time'] <= self.config.event_window_post)

est_data = df[est_mask]

evt_data = df[evt_mask].copy()

# Estimate model

if self.config.expected_return_model == ExpectedReturnModel.MEAN_ADJUSTED:

estimation = self._estimate_mean_adjusted(est_data['stock_ret'])

else:

estimation = self._estimate_market_model(

est_data['stock_ret'], est_data['market_ret']

)

# Calculate abnormal returns

evt_data['expected_ret'] = self._calculate_expected_returns(

estimation, evt_data['market_ret']

)

evt_data['AR'] = evt_data['stock_ret'] - evt_data['expected_ret']

evt_data['CAR'] = evt_data['AR'].cumsum()

# Check minimum event observations

if len(evt_data) < self.config.min_event_obs:

raise ValueError(f"Insufficient event observations: {len(evt_data)}")

return EventResult(

event=event,

config=self.config,

estimation=estimation,

event_data=evt_data,

valid=True

)

except Exception as e:

return EventResult(

event=event,

config=self.config,

estimation=None,

event_data=None,

valid=False,

error_message=str(e)

)

def process_events(self, events: List[EventData],

verbose: bool = True) -> List[EventResult]:

"""Process multiple events."""

results = []

for i, event in enumerate(events):

if verbose:

print(f"Processing {event.ticker} ({i+1}/{len(events)})...", end=" ")

result = self.process_event(event)

results.append(result)

if verbose:

status = "OK" if result.valid else f"FAILED: {result.error_message}"

print(status)

valid_count = sum(1 for r in results if r.valid)

if verbose:

print(f"\nProcessed {len(events)} events, {valid_count} valid")

return results

print("EventStudyEngine class defined!")EventStudyEngine class defined!

Source

class EventStudyAnalyzer:

"""

Statistical analysis for event study results.

"""

def __init__(self, results: List[EventResult]):

self.results = [r for r in results if r.valid]

self.n_events = len(self.results)

def calculate_caar(self, tau1: int, tau2: int) -> Dict:

"""Calculate Cumulative Average Abnormal Return."""

cars = np.array([r.get_car(tau1, tau2) for r in self.results])

caar = np.mean(cars)

caar_std = np.std(cars, ddof=1)

# Cross-sectional t-test

t_stat = caar / (caar_std / np.sqrt(self.n_events)) if caar_std > 0 else 0

p_value = 2 * (1 - stats.t.cdf(abs(t_stat), df=self.n_events - 1))

return {

'caar': caar,

'std': caar_std,

't_stat': t_stat,

'p_value': p_value,

'n': self.n_events,

'cars': cars

}

def patell_test(self, tau1: int, tau2: int) -> Dict:

"""Patell (1976) standardized residual test."""

scars = np.array([r.get_scar(tau1, tau2) for r in self.results])

scars = scars[~np.isnan(scars)]

n = len(scars)

if n < 2:

return {'z_stat': np.nan, 'p_value': np.nan, 'n': n}

z_stat = np.sum(scars) / np.sqrt(n)

p_value = 2 * (1 - stats.norm.cdf(abs(z_stat)))

return {

'z_stat': z_stat,

'p_value': p_value,

'n': n,

'mean_scar': np.mean(scars)

}

def bmp_test(self, tau1: int, tau2: int) -> Dict:

"""Boehmer, Musumeci, Poulsen (1991) test."""

scars = np.array([r.get_scar(tau1, tau2) for r in self.results])

scars = scars[~np.isnan(scars)]

n = len(scars)

if n < 2:

return {'t_stat': np.nan, 'p_value': np.nan, 'n': n}

mean_scar = np.mean(scars)

std_scar = np.std(scars, ddof=1)

t_stat = mean_scar / (std_scar / np.sqrt(n)) if std_scar > 0 else 0

p_value = 2 * (1 - stats.t.cdf(abs(t_stat), df=n - 1))

return {

't_stat': t_stat,

'p_value': p_value,

'n': n,

'mean_scar': mean_scar,

'std_scar': std_scar

}

def sign_test(self, tau1: int, tau2: int) -> Dict:

"""Non-parametric sign test."""

cars = np.array([r.get_car(tau1, tau2) for r in self.results])

n_pos = np.sum(cars > 0)

n = len(cars)

# Z-statistic

z_stat = (n_pos - 0.5 * n) / np.sqrt(0.25 * n)

p_value = 2 * (1 - stats.norm.cdf(abs(z_stat)))

return {

'n_positive': n_pos,

'n_negative': n - n_pos,

'pct_positive': n_pos / n * 100,

'z_stat': z_stat,

'p_value': p_value,

'n': n

}

def rank_test(self, tau1: int, tau2: int) -> Dict:

"""Corrado (1989) rank test."""

# Collect all ARs across estimation and event periods

rank_stats = []

for r in self.results:

# Get event window ARs

mask = (r.event_data['event_time'] >= tau1) & (r.event_data['event_time'] <= tau2)

event_ars = r.event_data.loc[mask, 'AR'].values

# Combine with estimation residuals for ranking

all_ars = np.concatenate([r.estimation.residuals, event_ars])

T = len(all_ars)

# Rank and transform

ranks = stats.rankdata(all_ars)

event_ranks = ranks[-len(event_ars):]

# Transformed rank

K = event_ranks / (T + 1) - 0.5

rank_stats.append(np.mean(K))

rank_stats = np.array(rank_stats)

n = len(rank_stats)

# Z-statistic

mean_K = np.mean(rank_stats)

std_K = np.std(rank_stats, ddof=1)

z_stat = mean_K / (std_K / np.sqrt(n)) if std_K > 0 else 0

p_value = 2 * (1 - stats.norm.cdf(abs(z_stat)))

return {

'z_stat': z_stat,

'p_value': p_value,

'n': n,

'mean_rank': mean_K

}

def bootstrap_test(self, tau1: int, tau2: int, n_boot: int = 5000) -> Dict:

"""Bootstrap test for CAAR."""

cars = np.array([r.get_car(tau1, tau2) for r in self.results])

n = len(cars)

observed_caar = np.mean(cars)

np.random.seed(42)

boot_caars = np.array([np.mean(np.random.choice(cars, n, replace=True))

for _ in range(n_boot)])

ci_lower = np.percentile(boot_caars, 2.5)

ci_upper = np.percentile(boot_caars, 97.5)

# Bootstrap p-value (two-sided)

p_value = np.mean(np.abs(boot_caars - observed_caar) >= np.abs(observed_caar))

return {

'caar': observed_caar,

'ci_lower': ci_lower,

'ci_upper': ci_upper,

'boot_se': np.std(boot_caars),

'p_value': p_value,

'n': n

}

def get_car_time_series(self) -> pd.DataFrame:

"""Get average CAR over event time."""

# Find common event times

all_times = set()

for r in self.results:

all_times.update(r.event_data['event_time'].values)

times = sorted(all_times)

# Calculate average AR and CAR for each time

data = []

for t in times:

ars = []

for r in self.results:

mask = r.event_data['event_time'] == t

if mask.any():

ars.append(r.event_data.loc[mask, 'AR'].values[0])

if ars:

data.append({

'event_time': t,

'AAR': np.mean(ars),

'AAR_std': np.std(ars, ddof=1) if len(ars) > 1 else 0,

'n': len(ars)

})

df = pd.DataFrame(data)

df['CAAR'] = df['AAR'].cumsum()

df['AAR_se'] = df['AAR_std'] / np.sqrt(df['n'])

return df

def comprehensive_analysis(self, windows: List[Tuple[int, int]] = None) -> pd.DataFrame:

"""Run all tests for multiple windows."""

if windows is None:

windows = [(-1, 1), (0, 0), (-5, 5), (-1, 5)]

results = []

for tau1, tau2 in windows:

caar = self.calculate_caar(tau1, tau2)

patell = self.patell_test(tau1, tau2)

bmp = self.bmp_test(tau1, tau2)

sign = self.sign_test(tau1, tau2)

rank = self.rank_test(tau1, tau2)

boot = self.bootstrap_test(tau1, tau2)

results.append({

'Window': f"({tau1},{tau2})",

'N': caar['n'],

'CAAR': caar['caar'],

'CAAR_t': caar['t_stat'],

'Patell_z': patell['z_stat'],

'BMP_t': bmp['t_stat'],

'Sign_z': sign['z_stat'],

'Rank_z': rank['z_stat'],

'Boot_p': boot['p_value'],

'%Pos': sign['pct_positive']

})

return pd.DataFrame(results)

print("EventStudyAnalyzer class defined!")EventStudyAnalyzer class defined!

3. Demonstration: Complete Event Study¶

Source

# Define events

events = [

EventData('AAPL', pd.Timestamp('2023-08-03'), 'Q3 Earnings'),

EventData('MSFT', pd.Timestamp('2023-07-25'), 'Q4 Earnings'),

EventData('GOOGL', pd.Timestamp('2023-07-25'), 'Q2 Earnings'),

EventData('AMZN', pd.Timestamp('2023-08-03'), 'Q2 Earnings'),

EventData('META', pd.Timestamp('2023-07-26'), 'Q2 Earnings'),

EventData('NVDA', pd.Timestamp('2023-08-23'), 'Q2 Earnings'),

EventData('TSLA', pd.Timestamp('2023-07-19'), 'Q2 Earnings'),

EventData('JPM', pd.Timestamp('2023-07-14'), 'Q2 Earnings'),

EventData('V', pd.Timestamp('2023-07-25'), 'Q3 Earnings'),

EventData('JNJ', pd.Timestamp('2023-07-20'), 'Q2 Earnings'),

EventData('WMT', pd.Timestamp('2023-08-17'), 'Q2 Earnings'),

EventData('PG', pd.Timestamp('2023-07-28'), 'Q4 Earnings'),

EventData('MA', pd.Timestamp('2023-07-27'), 'Q2 Earnings'),

EventData('HD', pd.Timestamp('2023-08-15'), 'Q2 Earnings'),

EventData('DIS', pd.Timestamp('2023-08-09'), 'Q3 Earnings'),

]

# Configure study

config = EventStudyConfig(

estimation_window=120,

gap=10,

event_window_pre=5,

event_window_post=5,

expected_return_model=ExpectedReturnModel.MARKET_MODEL,

min_estimation_obs=60

)

print(f"Event Study Configuration:")

print(f" Estimation window: {config.estimation_window} days")

print(f" Gap: {config.gap} days")

print(f" Event window: [{-config.event_window_pre}, +{config.event_window_post}]")

print(f" Model: {config.expected_return_model.value}")Event Study Configuration:

Estimation window: 120 days

Gap: 10 days

Event window: [-5, +5]

Model: market_model

Source

# Process events

engine = EventStudyEngine(config)

results = engine.process_events(events)Processing AAPL (1/15)... YF.download() has changed argument auto_adjust default to True

OK

Processing MSFT (2/15)... OK

Processing GOOGL (3/15)... OK

Processing AMZN (4/15)... OK

Processing META (5/15)... OK

Processing NVDA (6/15)... OK

Processing TSLA (7/15)... OK

Processing JPM (8/15)... OK

Processing V (9/15)... OK

Processing JNJ (10/15)... OK

Processing WMT (11/15)... OK

Processing PG (12/15)... OK

Processing MA (13/15)... OK

Processing HD (14/15)... OK

Processing DIS (15/15)... OK

Processed 15 events, 15 valid

Source

# Analyze results

analyzer = EventStudyAnalyzer(results)

print("\n" + "="*90)

print("COMPREHENSIVE EVENT STUDY RESULTS")

print("="*90)

# Get comprehensive analysis

analysis = analyzer.comprehensive_analysis()

# Format output

print(f"\nSample: {analyzer.n_events} events")

print("\n" + "-"*90)

print(f"{'Window':<10} {'N':>4} {'CAAR':>10} {'t-stat':>8} {'Patell':>8} {'BMP':>8} {'Sign':>8} {'Rank':>8} {'%Pos':>6}")

print("-"*90)

for _, row in analysis.iterrows():

# Significance markers

def sig(val):

if abs(val) > 2.58: return '***'

if abs(val) > 1.96: return '**'

if abs(val) > 1.65: return '*'

return ''

print(f"{row['Window']:<10} {int(row['N']):>4} {row['CAAR']*100:>+9.2f}% "

f"{row['CAAR_t']:>6.2f}{sig(row['CAAR_t']):<2} "

f"{row['Patell_z']:>6.2f}{sig(row['Patell_z']):<2} "

f"{row['BMP_t']:>6.2f}{sig(row['BMP_t']):<2} "

f"{row['Sign_z']:>6.2f}{sig(row['Sign_z']):<2} "

f"{row['Rank_z']:>6.2f}{sig(row['Rank_z']):<2} "

f"{row['%Pos']:>5.0f}%")

print("-"*90)

print("Significance: *** p<0.01, ** p<0.05, * p<0.10")

==========================================================================================

COMPREHENSIVE EVENT STUDY RESULTS

==========================================================================================

Sample: 15 events

------------------------------------------------------------------------------------------

Window N CAAR t-stat Patell BMP Sign Rank %Pos

------------------------------------------------------------------------------------------

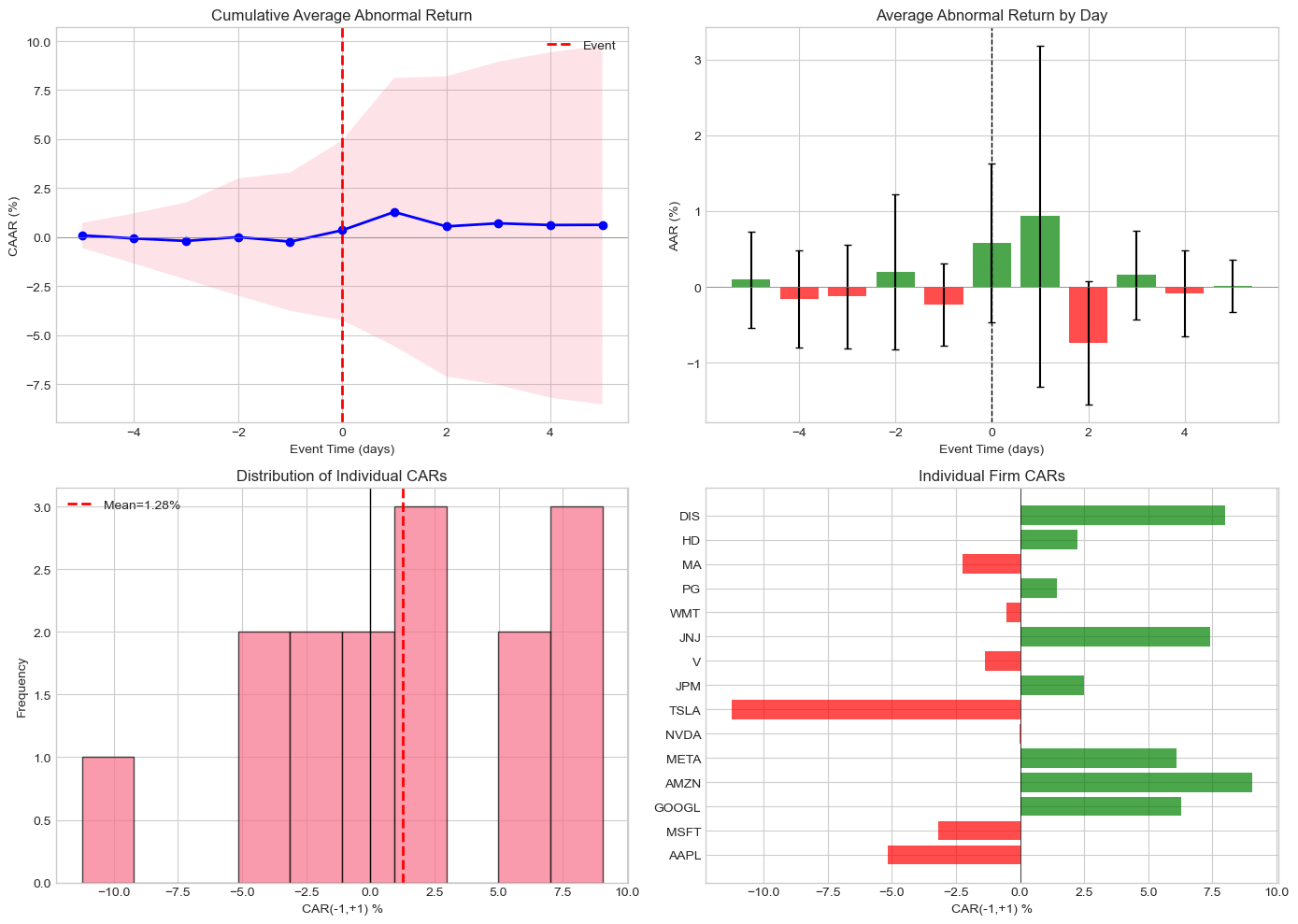

(-1,1) 15 +1.28% 0.89 2.01** 0.89 0.26 0.90 53%

(0,0) 15 +0.58% 1.08 1.86* 0.84 1.29 0.82 67%

(-5,5) 15 +0.63% 0.38 0.67 0.44 0.77 0.39 60%

(-1,5) 15 +0.62% 0.38 0.86 0.49 0.26 0.58 53%

------------------------------------------------------------------------------------------

Significance: *** p<0.01, ** p<0.05, * p<0.10

Source

# Visualization

fig, axes = plt.subplots(2, 2, figsize=(14, 10))

# Get time series data

ts_data = analyzer.get_car_time_series()

# CAAR over event time

ax1 = axes[0, 0]

ax1.plot(ts_data['event_time'], ts_data['CAAR']*100, 'b-', linewidth=2, marker='o')

ax1.fill_between(ts_data['event_time'],

(ts_data['CAAR'] - 1.96*ts_data['AAR_se'].cumsum())*100,

(ts_data['CAAR'] + 1.96*ts_data['AAR_se'].cumsum())*100,

alpha=0.2)

ax1.axhline(0, color='gray', linestyle='-', linewidth=0.5)

ax1.axvline(0, color='red', linestyle='--', linewidth=2, label='Event')

ax1.set_xlabel('Event Time (days)')

ax1.set_ylabel('CAAR (%)')

ax1.set_title('Cumulative Average Abnormal Return')

ax1.legend()

# AAR bar chart

ax2 = axes[0, 1]

colors = ['green' if x > 0 else 'red' for x in ts_data['AAR']]

ax2.bar(ts_data['event_time'], ts_data['AAR']*100, color=colors, alpha=0.7,

yerr=ts_data['AAR_se']*100*1.96, capsize=3)

ax2.axhline(0, color='gray', linestyle='-', linewidth=0.5)

ax2.axvline(0, color='black', linestyle='--', linewidth=1)

ax2.set_xlabel('Event Time (days)')

ax2.set_ylabel('AAR (%)')

ax2.set_title('Average Abnormal Return by Day')

# Individual CAR distribution for (-1,+1)

ax3 = axes[1, 0]

cars = [r.get_car(-1, 1)*100 for r in results if r.valid]

ax3.hist(cars, bins=10, edgecolor='black', alpha=0.7)

ax3.axvline(np.mean(cars), color='red', linestyle='--', linewidth=2,

label=f'Mean={np.mean(cars):.2f}%')

ax3.axvline(0, color='black', linestyle='-', linewidth=1)

ax3.set_xlabel('CAR(-1,+1) %')

ax3.set_ylabel('Frequency')

ax3.set_title('Distribution of Individual CARs')

ax3.legend()

# Individual firm CARs

ax4 = axes[1, 1]

valid_results = [r for r in results if r.valid]

tickers = [r.event.ticker for r in valid_results]

firm_cars = [r.get_car(-1, 1)*100 for r in valid_results]

colors = ['green' if c > 0 else 'red' for c in firm_cars]

y_pos = range(len(tickers))

ax4.barh(y_pos, firm_cars, color=colors, alpha=0.7)

ax4.axvline(0, color='black', linestyle='-', linewidth=0.5)

ax4.set_yticks(y_pos)

ax4.set_yticklabels(tickers)

ax4.set_xlabel('CAR(-1,+1) %')

ax4.set_title('Individual Firm CARs')

plt.tight_layout()

plt.show()

4. Robustness Checks¶

Why Robustness Matters¶

Results should be stable across:

Different window lengths

Different expected return models

Subsamples

Outlier treatment

Source

class RobustnessChecker:

"""

Comprehensive robustness checks for event studies.

"""

def __init__(self, events: List[EventData]):

self.events = events

def model_robustness(self, base_config: EventStudyConfig) -> pd.DataFrame:

"""Test robustness to expected return model choice."""

models = [

ExpectedReturnModel.MARKET_MODEL,

ExpectedReturnModel.MARKET_ADJUSTED,

ExpectedReturnModel.MEAN_ADJUSTED

]

results = []

for model in models:

config = EventStudyConfig(

estimation_window=base_config.estimation_window,

gap=base_config.gap,

event_window_pre=base_config.event_window_pre,

event_window_post=base_config.event_window_post,

expected_return_model=model

)

engine = EventStudyEngine(config)

event_results = engine.process_events(self.events, verbose=False)

analyzer = EventStudyAnalyzer(event_results)

caar = analyzer.calculate_caar(-1, 1)

results.append({

'Model': model.value,

'N': caar['n'],

'CAAR': caar['caar'],

't-stat': caar['t_stat'],

'p-value': caar['p_value']

})

return pd.DataFrame(results)

def window_robustness(self, base_config: EventStudyConfig) -> pd.DataFrame:

"""Test robustness to estimation window length."""

windows = [60, 90, 120, 150, 200]

results = []

for est_window in windows:

config = EventStudyConfig(

estimation_window=est_window,

gap=base_config.gap,

event_window_pre=base_config.event_window_pre,

event_window_post=base_config.event_window_post,

expected_return_model=base_config.expected_return_model,

min_estimation_obs=min(60, est_window)

)

engine = EventStudyEngine(config)

event_results = engine.process_events(self.events, verbose=False)

analyzer = EventStudyAnalyzer(event_results)

caar = analyzer.calculate_caar(-1, 1)

results.append({

'Est. Window': est_window,

'N': caar['n'],

'CAAR': caar['caar'],

't-stat': caar['t_stat'],

'p-value': caar['p_value']

})

return pd.DataFrame(results)

def outlier_robustness(self, event_results: List[EventResult],

tau1: int = -1, tau2: int = 1) -> Dict:

"""Test robustness to outlier treatment."""

valid_results = [r for r in event_results if r.valid]

cars = np.array([r.get_car(tau1, tau2) for r in valid_results])

# Full sample

full_mean = np.mean(cars)

full_t = full_mean / (np.std(cars, ddof=1) / np.sqrt(len(cars)))

# Winsorized (1% and 99%)

p1, p99 = np.percentile(cars, [1, 99])

winsorized = np.clip(cars, p1, p99)

wins_mean = np.mean(winsorized)

wins_t = wins_mean / (np.std(winsorized, ddof=1) / np.sqrt(len(winsorized)))

# Trimmed (exclude top/bottom 5%)

p5, p95 = np.percentile(cars, [5, 95])

trimmed = cars[(cars >= p5) & (cars <= p95)]

trim_mean = np.mean(trimmed)

trim_t = trim_mean / (np.std(trimmed, ddof=1) / np.sqrt(len(trimmed)))

return {

'Full Sample': {'N': len(cars), 'CAAR': full_mean, 't-stat': full_t},

'Winsorized (1-99%)': {'N': len(winsorized), 'CAAR': wins_mean, 't-stat': wins_t},

'Trimmed (5-95%)': {'N': len(trimmed), 'CAAR': trim_mean, 't-stat': trim_t}

}

# Run robustness checks

checker = RobustnessChecker(events)

print("\n" + "="*70)

print("ROBUSTNESS CHECKS")

print("="*70)

# Model robustness

print("\n1. Expected Return Model Robustness:")

print("-"*70)

model_robust = checker.model_robustness(config)

model_robust['CAAR'] = model_robust['CAAR'].apply(lambda x: f"{x*100:+.2f}%")

model_robust['t-stat'] = model_robust['t-stat'].apply(lambda x: f"{x:.2f}")

model_robust['p-value'] = model_robust['p-value'].apply(lambda x: f"{x:.4f}")

print(model_robust.to_string(index=False))

======================================================================

ROBUSTNESS CHECKS

======================================================================

1. Expected Return Model Robustness:

----------------------------------------------------------------------

Model N CAAR t-stat p-value

market_model 15 +1.28% 0.89 0.3898

market_adjusted 15 +1.52% 1.13 0.2766

mean_adjusted 15 +0.48% 0.34 0.7364

Source

# Window robustness

print("\n2. Estimation Window Robustness:")

print("-"*70)

window_robust = checker.window_robustness(config)

window_robust['CAAR'] = window_robust['CAAR'].apply(lambda x: f"{x*100:+.2f}%")

window_robust['t-stat'] = window_robust['t-stat'].apply(lambda x: f"{x:.2f}")

window_robust['p-value'] = window_robust['p-value'].apply(lambda x: f"{x:.4f}")

print(window_robust.to_string(index=False))

2. Estimation Window Robustness:

----------------------------------------------------------------------

1 Failed download:

['MSFT']: Timeout('Failed to perform, curl: (28) Operation timed out after 10002 milliseconds with 0 bytes received. See https://curl.se/libcurl/c/libcurl-errors.html first for more details.')

Est. Window N CAAR t-stat p-value

60 15 +1.32% 0.96 0.3536

90 14 +1.57% 1.09 0.2948

120 15 +1.28% 0.89 0.3898

150 15 +1.34% 0.97 0.3485

200 15 +1.49% 1.08 0.2966

Source

# Outlier robustness

print("\n3. Outlier Treatment Robustness:")

print("-"*70)

outlier_robust = checker.outlier_robustness(results)

for treatment, stats in outlier_robust.items():

print(f" {treatment}: N={stats['N']}, CAAR={stats['CAAR']*100:+.2f}%, t={stats['t-stat']:.2f}")

3. Outlier Treatment Robustness:

----------------------------------------------------------------------

Full Sample: N=15, CAAR=+1.28%, t=0.89

Winsorized (1-99%): N=15, CAAR=+1.33%, t=0.95

Trimmed (5-95%): N=13, CAAR=+1.64%, t=1.39

5. Common Pitfalls and How to Avoid Them¶

Source

def demonstrate_pitfalls():

"""

Demonstrate common event study pitfalls.

"""

print("\n" + "="*80)

print("COMMON EVENT STUDY PITFALLS")

print("="*80)

# Pitfall 1: Look-ahead bias in event date

print("\n1. LOOK-AHEAD BIAS")

print("-"*60)

print("Problem: Using information not available at event time")

print("Example: Using close price on announcement day when news")

print(" came after market close")

print("Solution: Verify event timing; use t+1 if after-hours")

# Pitfall 2: Survivorship bias

print("\n2. SURVIVORSHIP BIAS")

print("-"*60)

print("Problem: Only including firms that survived")

print("Example: Studying M&A for current S&P 500 members")

print("Solution: Use point-in-time data; include delisted firms")

# Pitfall 3: Event date errors

print("\n3. EVENT DATE ERRORS")

print("-"*60)

print("Problem: Using wrong event date (filing vs announcement)")

print("Example: Using SEC filing date instead of press release")

print("Solution: Verify dates from multiple sources; check for")

print(" price reaction to confirm timing")

# Pitfall 4: Thin trading

print("\n4. THIN TRADING / ILLIQUIDITY")

print("-"*60)

print("Problem: Missing or stale prices for illiquid stocks")

print("Example: Using daily returns with many zero-return days")

print("Solution: Use trade-to-trade returns; Scholes-Williams beta;")

print(" exclude extremely illiquid stocks")

# Pitfall 5: Clustering

print("\n5. EVENT CLUSTERING")

print("-"*60)

print("Problem: Many events on same day (e.g., earnings season)")

print("Example: Testing 50 earnings announcements, 20 on same day")

print("Solution: Use portfolio approach; crude dependence adjustment;")

print(" cluster standard errors by date")

# Pitfall 6: Confounding events

print("\n6. CONFOUNDING EVENTS")

print("-"*60)

print("Problem: Multiple events in same window")

print("Example: Earnings announcement during Fed meeting week")

print("Solution: Screen for confounding events; use shorter windows;")

print(" control for confounds in cross-sectional regression")

demonstrate_pitfalls()

================================================================================

COMMON EVENT STUDY PITFALLS

================================================================================

1. LOOK-AHEAD BIAS

------------------------------------------------------------

Problem: Using information not available at event time

Example: Using close price on announcement day when news

came after market close

Solution: Verify event timing; use t+1 if after-hours

2. SURVIVORSHIP BIAS

------------------------------------------------------------

Problem: Only including firms that survived

Example: Studying M&A for current S&P 500 members

Solution: Use point-in-time data; include delisted firms

3. EVENT DATE ERRORS

------------------------------------------------------------

Problem: Using wrong event date (filing vs announcement)

Example: Using SEC filing date instead of press release

Solution: Verify dates from multiple sources; check for

price reaction to confirm timing

4. THIN TRADING / ILLIQUIDITY

------------------------------------------------------------

Problem: Missing or stale prices for illiquid stocks

Example: Using daily returns with many zero-return days

Solution: Use trade-to-trade returns; Scholes-Williams beta;

exclude extremely illiquid stocks

5. EVENT CLUSTERING

------------------------------------------------------------

Problem: Many events on same day (e.g., earnings season)

Example: Testing 50 earnings announcements, 20 on same day

Solution: Use portfolio approach; crude dependence adjustment;

cluster standard errors by date

6. CONFOUNDING EVENTS

------------------------------------------------------------

Problem: Multiple events in same window

Example: Earnings announcement during Fed meeting week

Solution: Screen for confounding events; use shorter windows;

control for confounds in cross-sectional regression

Source

def data_quality_checks(results: List[EventResult]) -> pd.DataFrame:

"""

Perform data quality checks.

"""

checks = []

for r in results:

if not r.valid:

checks.append({

'Ticker': r.event.ticker,

'Status': 'FAILED',

'Issue': r.error_message,

'Est. N': 'N/A',

'R²': 'N/A',

'Beta': 'N/A'

})

continue

issues = []

# Check estimation observations

if r.estimation.n_obs < 100:

issues.append(f"Low est. obs ({r.estimation.n_obs})")

# Check R-squared

if r.estimation.r_squared < 0.1:

issues.append(f"Low R² ({r.estimation.r_squared:.2f})")

# Check beta range

if r.estimation.beta < 0 or r.estimation.beta > 3:

issues.append(f"Unusual beta ({r.estimation.beta:.2f})")

# Check for extreme CARs

car = r.get_car(-1, 1)

if abs(car) > 0.20: # 20%

issues.append(f"Extreme CAR ({car*100:.1f}%)")

checks.append({

'Ticker': r.event.ticker,

'Status': 'WARNING' if issues else 'OK',

'Issue': '; '.join(issues) if issues else 'None',

'Est. N': r.estimation.n_obs,

'R²': f"{r.estimation.r_squared:.3f}",

'Beta': f"{r.estimation.beta:.2f}"

})

return pd.DataFrame(checks)

# Run quality checks

print("\n" + "="*80)

print("DATA QUALITY CHECKS")

print("="*80)

quality_df = data_quality_checks(results)

print(quality_df.to_string(index=False))

================================================================================

DATA QUALITY CHECKS

================================================================================

Ticker Status Issue Est. N R² Beta

AAPL OK None 120 0.598 1.12

MSFT OK None 120 0.455 1.31

GOOGL OK None 120 0.374 1.44

AMZN OK None 120 0.371 1.49

META OK None 120 0.327 1.97

NVDA OK None 120 0.219 1.95

TSLA OK None 120 0.278 2.18

JPM OK None 120 0.295 0.92

V OK None 120 0.411 0.76

JNJ OK None 120 0.120 0.37

WMT WARNING Low R² (0.08) 120 0.076 0.27

PG OK None 120 0.118 0.36

MA OK None 120 0.465 0.83

HD OK None 120 0.370 1.09

DIS OK None 120 0.435 1.30

6. Publication-Ready Output¶

Source

class PublicationFormatter:

"""

Create publication-ready tables and figures.

"""

@staticmethod

def main_results_table(analyzer: EventStudyAnalyzer,

windows: List[Tuple[int, int]] = None) -> str:

"""Create main results table."""

if windows is None:

windows = [(-1, 1), (0, 0), (-5, 5)]

lines = []

lines.append("\n" + "="*90)

lines.append("TABLE: Event Study Results")

lines.append("="*90)

lines.append(f"\nSample: {analyzer.n_events} events")

lines.append("\n" + "-"*90)

lines.append(f"{'Window':<12} {'CAAR':>10} {'Median':>10} {'t-stat':>10} "

f"{'Patell-z':>10} {'%Positive':>10}")

lines.append("-"*90)

for tau1, tau2 in windows:

caar = analyzer.calculate_caar(tau1, tau2)

patell = analyzer.patell_test(tau1, tau2)

sign = analyzer.sign_test(tau1, tau2)

# Significance markers

def sig_marker(p):

if p < 0.01: return '***'

if p < 0.05: return '**'

if p < 0.10: return '*'

return ''

median_car = np.median(caar['cars'])

lines.append(f"({tau1:+d},{tau2:+d}){'':<6} "

f"{caar['caar']*100:>+9.2f}%{sig_marker(caar['p_value'])} "

f"{median_car*100:>+9.2f}% "

f"{caar['t_stat']:>9.2f} "

f"{patell['z_stat']:>9.2f} "

f"{sign['pct_positive']:>9.1f}%")

lines.append("-"*90)

lines.append("***, **, * indicate significance at 1%, 5%, 10% levels (two-tailed)")

return '\n'.join(lines)

@staticmethod

def latex_table(analyzer: EventStudyAnalyzer,

windows: List[Tuple[int, int]] = None,

caption: str = "Event Study Results") -> str:

"""Generate LaTeX table."""

if windows is None:

windows = [(-1, 1), (0, 0), (-5, 5)]

latex = f"""\\begin{{table}}[htbp]

\\centering

\\caption{{{caption}}}

\\begin{{tabular}}{{lccccc}}

\\hline\\hline

Window & N & CAAR & t-stat & Patell z & \\% Positive \\\\

\\hline

"""

for tau1, tau2 in windows:

caar = analyzer.calculate_caar(tau1, tau2)

patell = analyzer.patell_test(tau1, tau2)

sign = analyzer.sign_test(tau1, tau2)

def sig_marker(p):

if p < 0.01: return '$^{***}$'

if p < 0.05: return '$^{**}$'

if p < 0.10: return '$^{*}$'

return ''

latex += f"({tau1:+d},{tau2:+d}) & {caar['n']} & "

latex += f"{caar['caar']*100:.2f}\\%{sig_marker(caar['p_value'])} & "

latex += f"{caar['t_stat']:.2f} & {patell['z_stat']:.2f} & "

latex += f"{sign['pct_positive']:.1f}\\% \\\\\n"

latex += """\\hline\\hline

\\end{tabular}

\\begin{tablenotes}

\\small

\\item Notes: $^{***}$, $^{**}$, $^{*}$ indicate significance at 1\\%, 5\\%, 10\\% levels.

\\end{tablenotes}

\\end{table}"""

return latex

# Generate publication output

formatter = PublicationFormatter()

print(formatter.main_results_table(analyzer))

print("\n\nLaTeX Code:")

print(formatter.latex_table(analyzer, caption="Earnings Announcement Returns"))---------------------------------------------------------------------------

AttributeError Traceback (most recent call last)

Cell In[30], line 96

93 # Generate publication output

94 formatter = PublicationFormatter()

---> 96 print(formatter.main_results_table(analyzer))

97 print("\n\nLaTeX Code:")

98 print(formatter.latex_table(analyzer, caption="Earnings Announcement Returns"))

Cell In[30], line 24, in PublicationFormatter.main_results_table(analyzer, windows)

21 lines.append("-"*90)

23 for tau1, tau2 in windows:

---> 24 caar = analyzer.calculate_caar(tau1, tau2)

25 patell = analyzer.patell_test(tau1, tau2)

26 sign = analyzer.sign_test(tau1, tau2)

Cell In[9], line 19, in EventStudyAnalyzer.calculate_caar(self, tau1, tau2)

17 # Cross-sectional t-test

18 t_stat = caar / (caar_std / np.sqrt(self.n_events)) if caar_std > 0 else 0

---> 19 p_value = 2 * (1 - stats.t.cdf(abs(t_stat), df=self.n_events - 1))

21 return {

22 'caar': caar,

23 'std': caar_std,

(...)

27 'cars': cars

28 }

AttributeError: 'dict' object has no attribute 't'Source

# Publication-ready figure

def create_publication_figure(analyzer: EventStudyAnalyzer,

save_path: str = None):

"""Create publication-quality figure."""

fig, ax = plt.subplots(figsize=(10, 6))

ts_data = analyzer.get_car_time_series()

# Plot CAAR with confidence bands

ax.plot(ts_data['event_time'], ts_data['CAAR']*100, 'k-',

linewidth=2, label='CAAR')

# 95% CI

cumulative_se = ts_data['AAR_se'].cumsum()

lower = (ts_data['CAAR'] - 1.96 * cumulative_se) * 100

upper = (ts_data['CAAR'] + 1.96 * cumulative_se) * 100

ax.fill_between(ts_data['event_time'], lower, upper,

alpha=0.2, color='gray', label='95% CI')

# Reference lines

ax.axhline(0, color='black', linestyle='-', linewidth=0.5)

ax.axvline(0, color='black', linestyle='--', linewidth=1)

# Labels

ax.set_xlabel('Event Time (Trading Days)', fontsize=12)

ax.set_ylabel('Cumulative Average Abnormal Return (%)', fontsize=12)

ax.set_title('Event Study: Cumulative Abnormal Returns', fontsize=14)

# Add annotation for key window

caar_11 = analyzer.calculate_caar(-1, 1)

ax.annotate(f'CAAR(-1,+1) = {caar_11["caar"]*100:.2f}%\n(t = {caar_11["t_stat"]:.2f})',

xy=(1, ts_data[ts_data['event_time'] == 1]['CAAR'].values[0]*100),

xytext=(3, ts_data[ts_data['event_time'] == 1]['CAAR'].values[0]*100 + 0.5),

fontsize=10,

arrowprops=dict(arrowstyle='->', color='black'))

ax.legend(loc='upper left', fontsize=10)

ax.grid(True, alpha=0.3)

plt.tight_layout()

if save_path:

plt.savefig(save_path, dpi=300, bbox_inches='tight')

print(f"Figure saved to {save_path}")

plt.show()

create_publication_figure(analyzer)7. Checklist for Event Study Research¶

Source

def print_research_checklist():

"""Print comprehensive research checklist."""

checklist = """

╔══════════════════════════════════════════════════════════════════════════════╗

║ EVENT STUDY RESEARCH CHECKLIST ║

╠══════════════════════════════════════════════════════════════════════════════╣

║ ║

║ □ RESEARCH DESIGN ║

║ □ Clear research question and hypothesis ║

║ □ Appropriate event type for question ║

║ □ Justified window lengths ║

║ □ Expected return model appropriate for setting ║

║ ║

║ □ DATA COLLECTION ║

║ □ Event dates verified from multiple sources ║

║ □ Point-in-time data (no survivorship bias) ║

║ □ Sufficient estimation period observations ║

║ □ Adjusted for splits, dividends ║

║ ║

║ □ IMPLEMENTATION ║

║ □ Data quality checks performed ║

║ □ Outliers identified and handled ║

║ □ Confounding events screened ║

║ □ Event clustering addressed ║

║ ║

║ □ STATISTICAL TESTING ║

║ □ Multiple test statistics reported ║

║ □ Both parametric and non-parametric tests ║

║ □ Cross-sectional standard errors appropriate ║

║ □ Bootstrap inference for small samples ║

║ ║

║ □ ROBUSTNESS ║

║ □ Different window lengths ║

║ □ Different expected return models ║

║ □ Outlier treatment sensitivity ║

║ □ Subsample analysis ║

║ ║

║ □ REPORTING ║

║ □ Sample construction transparent ║

║ □ Methodology clearly described ║

║ □ Multiple windows reported ║

║ □ Economic significance discussed ║

║ □ Limitations acknowledged ║

║ ║

╚══════════════════════════════════════════════════════════════════════════════╝

"""

print(checklist)

print_research_checklist()

╔══════════════════════════════════════════════════════════════════════════════╗

║ EVENT STUDY RESEARCH CHECKLIST ║

╠══════════════════════════════════════════════════════════════════════════════╣

║ ║

║ □ RESEARCH DESIGN ║

║ □ Clear research question and hypothesis ║

║ □ Appropriate event type for question ║

║ □ Justified window lengths ║

║ □ Expected return model appropriate for setting ║

║ ║

║ □ DATA COLLECTION ║

║ □ Event dates verified from multiple sources ║

║ □ Point-in-time data (no survivorship bias) ║

║ □ Sufficient estimation period observations ║

║ □ Adjusted for splits, dividends ║

║ ║

║ □ IMPLEMENTATION ║

║ □ Data quality checks performed ║

║ □ Outliers identified and handled ║

║ □ Confounding events screened ║

║ □ Event clustering addressed ║

║ ║

║ □ STATISTICAL TESTING ║

║ □ Multiple test statistics reported ║

║ □ Both parametric and non-parametric tests ║

║ □ Cross-sectional standard errors appropriate ║

║ □ Bootstrap inference for small samples ║

║ ║

║ □ ROBUSTNESS ║

║ □ Different window lengths ║

║ □ Different expected return models ║

║ □ Outlier treatment sensitivity ║

║ □ Subsample analysis ║

║ ║

║ □ REPORTING ║

║ □ Sample construction transparent ║

║ □ Methodology clearly described ║

║ □ Multiple windows reported ║

║ □ Economic significance discussed ║

║ □ Limitations acknowledged ║

║ ║

╚══════════════════════════════════════════════════════════════════════════════╝

8. Summary¶

Key Takeaways¶

Design carefully: Window lengths, models, and tests should match your question

Build robust code: Modular, flexible, handles edge cases

Check data quality: Verify dates, screen for issues

Test robustness: Results should be stable across specifications

Avoid pitfalls: Look-ahead bias, survivorship, clustering

Report comprehensively: Multiple windows, tests, robustness checks

The Framework Provided¶

EventStudyConfig: Configurable parametersEventStudyEngine: Data processing and estimationEventStudyAnalyzer: Statistical analysisRobustnessChecker: Sensitivity analysisPublicationFormatter: Output generation

References¶

MacKinlay, A. C. (1997). Event studies in economics and finance. Journal of Economic Literature, 35(1), 13-39.

Kothari, S. P., & Warner, J. B. (2007). Econometrics of event studies. Handbook of Corporate Finance, 1, 3-36.

Kolari, J. W., & Pynnönen, S. (2010). Event study testing with cross-sectional correlation of abnormal returns. Review of Financial Studies, 23(11), 3996-4025.