Session 4: Statistical Inference I - Parametric Tests

Event Studies in Finance and Economics - Summer School¶

Learning Objectives¶

By the end of this session, you will be able to:

Understand the assumptions underlying parametric event study tests

Implement and interpret the standard t-test for event studies

Apply the Patell (1976) standardized residual test

Use the Boehmer, Musumeci, and Poulsen (1991) test for event-induced variance

Distinguish between cross-sectional and time-series variance approaches

Evaluate the power and specification of different test statistics

1. Introduction: The Inference Problem¶

From Measurement to Inference¶

In Session 3, we learned how to measure abnormal returns. But measurement alone doesn’t tell us whether the event had a statistically significant effect. We need formal hypothesis tests.

The Null Hypothesis¶

Key Challenges¶

Estimation error: Parameters (, ) are estimated, not known

Cross-sectional correlation: Events may cluster in calendar time

Event-induced variance: The event itself may change volatility

Non-normality: Returns are often fat-tailed

Small samples: Limited number of events in many studies

This session focuses on parametric tests that assume (approximately) normal distributions. Session 5 will cover non-parametric alternatives.

2. Setup and Data¶

Source

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

from scipy import stats

from scipy.special import comb

import yfinance as yf

import statsmodels.api as sm

from datetime import datetime, timedelta

from typing import List, Dict, Tuple, Optional

from dataclasses import dataclass

import warnings

warnings.filterwarnings('ignore')

plt.style.use('seaborn-v0_8-whitegrid')

sns.set_palette("husl")

print("Libraries loaded successfully!")Libraries loaded successfully!

Source

# We'll use a larger sample for better demonstration of test properties

EVENTS = [

# Tech earnings Q2-Q3 2023

{'ticker': 'AAPL', 'date': '2023-08-03', 'name': 'Apple Q3'},

{'ticker': 'MSFT', 'date': '2023-07-25', 'name': 'Microsoft Q4'},

{'ticker': 'GOOGL', 'date': '2023-07-25', 'name': 'Alphabet Q2'},

{'ticker': 'AMZN', 'date': '2023-08-03', 'name': 'Amazon Q2'},

{'ticker': 'META', 'date': '2023-07-26', 'name': 'Meta Q2'},

{'ticker': 'NVDA', 'date': '2023-08-23', 'name': 'Nvidia Q2'},

{'ticker': 'TSLA', 'date': '2023-07-19', 'name': 'Tesla Q2'},

{'ticker': 'AMD', 'date': '2023-08-01', 'name': 'AMD Q2'},

{'ticker': 'INTC', 'date': '2023-07-27', 'name': 'Intel Q2'},

{'ticker': 'CRM', 'date': '2023-08-30', 'name': 'Salesforce Q2'},

]

ESTIMATION_WINDOW = 120

GAP = 10

EVENT_WINDOW_PRE = 10

EVENT_WINDOW_POST = 10

print(f"Sample: {len(EVENTS)} tech earnings announcements")Sample: 10 tech earnings announcements

Source

@dataclass

class MarketModelResults:

"""Container for market model estimation results."""

alpha: float

beta: float

sigma: float

r_squared: float

n_obs: int

market_mean: float

market_var: float

residuals: np.ndarray

@dataclass

class EventStudyResult:

"""Container for single event study results."""

ticker: str

name: str

event_date: pd.Timestamp

model: MarketModelResults

event_data: pd.DataFrame

estimation_data: pd.DataFrame

def download_and_process_event(ticker: str, event_date: str, name: str,

est_window: int, gap: int,

pre: int, post: int) -> Optional[EventStudyResult]:

"""

Download data and estimate market model for a single event.

"""

try:

event_dt = pd.to_datetime(event_date)

start_date = event_dt - timedelta(days=int((est_window + gap + pre) * 1.5))

end_date = event_dt + timedelta(days=int(post * 2.5))

stock = yf.download(ticker, start=start_date, end=end_date, progress=False)['Close']

market = yf.download('^GSPC', start=start_date, end=end_date, progress=False)['Close']

df = pd.DataFrame({

'stock_price': stock.squeeze(),

'market_price': market.squeeze()

})

df['stock_ret'] = df['stock_price'].pct_change()

df['market_ret'] = df['market_price'].pct_change()

df = df.dropna()

if event_dt not in df.index:

idx = df.index.get_indexer([event_dt], method='nearest')[0]

event_dt = df.index[idx]

event_idx = df.index.get_loc(event_dt)

df['event_time'] = range(-event_idx, len(df) - event_idx)

# Split windows

est_end = -(gap + pre)

est_start = est_end - est_window

est_data = df[(df['event_time'] >= est_start) & (df['event_time'] < est_end)].copy()

evt_data = df[(df['event_time'] >= -pre) & (df['event_time'] <= post)].copy()

# Estimate market model

y = est_data['stock_ret'].values

x = est_data['market_ret'].values

X = sm.add_constant(x)

ols = sm.OLS(y, X).fit()

model = MarketModelResults(

alpha=ols.params[0],

beta=ols.params[1],

sigma=np.std(ols.resid, ddof=2),

r_squared=ols.rsquared,

n_obs=len(y),

market_mean=np.mean(x),

market_var=np.sum((x - np.mean(x))**2),

residuals=ols.resid

)

# Calculate abnormal returns

evt_data['expected_ret'] = model.alpha + model.beta * evt_data['market_ret']

evt_data['AR'] = evt_data['stock_ret'] - evt_data['expected_ret']

return EventStudyResult(

ticker=ticker,

name=name,

event_date=event_dt,

model=model,

event_data=evt_data,

estimation_data=est_data

)

except Exception as e:

print(f" {ticker}: FAILED - {e}")

return None

# Process all events

print("Processing events...")

event_results = []

for event in EVENTS:

result = download_and_process_event(

event['ticker'], event['date'], event['name'],

ESTIMATION_WINDOW, GAP, EVENT_WINDOW_PRE, EVENT_WINDOW_POST

)

if result:

event_results.append(result)

print(f" {result.ticker}: OK (beta={result.model.beta:.3f}, sigma={result.model.sigma:.4f})")

print(f"\nSuccessfully processed {len(event_results)} events")Processing events...

YF.download() has changed argument auto_adjust default to True

AAPL: OK (beta=1.127, sigma=0.0080)

MSFT: OK (beta=1.249, sigma=0.0140)

GOOGL: OK (beta=1.404, sigma=0.0166)

AMZN: OK (beta=1.521, sigma=0.0175)

META: OK (beta=1.891, sigma=0.0256)

NVDA: OK (beta=2.068, sigma=0.0305)

TSLA: OK (beta=2.163, sigma=0.0334)

AMD: OK (beta=1.770, sigma=0.0290)

INTC: OK (beta=1.304, sigma=0.0230)

CRM: OK (beta=1.078, sigma=0.0173)

Successfully processed 10 events

3. Test 1: Simple Cross-Sectional t-Test¶

The Simplest Approach¶

The most basic test treats individual CARs as independent draws and uses their cross-sectional distribution:

Where:

Assumptions¶

CARs are independent across firms

CARs are identically distributed

CARs are (approximately) normally distributed

Distribution¶

Under the null:

Source

def calculate_car(event_data: pd.DataFrame, tau1: int, tau2: int) -> float:

"""Calculate Cumulative Abnormal Return for a window."""

mask = (event_data['event_time'] >= tau1) & (event_data['event_time'] <= tau2)

return event_data.loc[mask, 'AR'].sum()

def cross_sectional_t_test(event_results: List[EventStudyResult],

tau1: int, tau2: int) -> Dict:

"""

Simple cross-sectional t-test for CAAR.

H0: E[CAR] = 0

Returns:

--------

Dictionary with test statistics

"""

# Calculate individual CARs

cars = np.array([calculate_car(r.event_data, tau1, tau2) for r in event_results])

N = len(cars)

# Sample statistics

caar = np.mean(cars)

s_car = np.std(cars, ddof=1)

se = s_car / np.sqrt(N)

# t-statistic

t_stat = caar / se if se > 0 else 0

# p-value (two-tailed)

p_value = 2 * (1 - stats.t.cdf(abs(t_stat), df=N-1))

return {

'test_name': 'Cross-Sectional t-Test',

'N': N,

'CAAR': caar,

'std_dev': s_car,

'std_error': se,

't_stat': t_stat,

'df': N - 1,

'p_value': p_value,

'individual_cars': cars

}

# Run test for standard windows

print("Cross-Sectional t-Test Results:")

print("="*70)

windows = [(-1, +1), (0, 0), (-5, +5), (-10, +10)]

cs_results = []

for tau1, tau2 in windows:

result = cross_sectional_t_test(event_results, tau1, tau2)

cs_results.append(result)

sig = '***' if result['p_value'] < 0.01 else '**' if result['p_value'] < 0.05 else '*' if result['p_value'] < 0.10 else ''

print(f"\nWindow [{tau1:+d}, {tau2:+d}]:")

print(f" CAAR = {result['CAAR']*100:+.3f}%")

print(f" Std. Dev. = {result['std_dev']*100:.3f}%")

print(f" t-stat = {result['t_stat']:.3f} {sig}")

print(f" p-value = {result['p_value']:.4f}")

print("\n" + "="*70)

print("Significance: * p<0.10, ** p<0.05, *** p<0.01")Cross-Sectional t-Test Results:

======================================================================

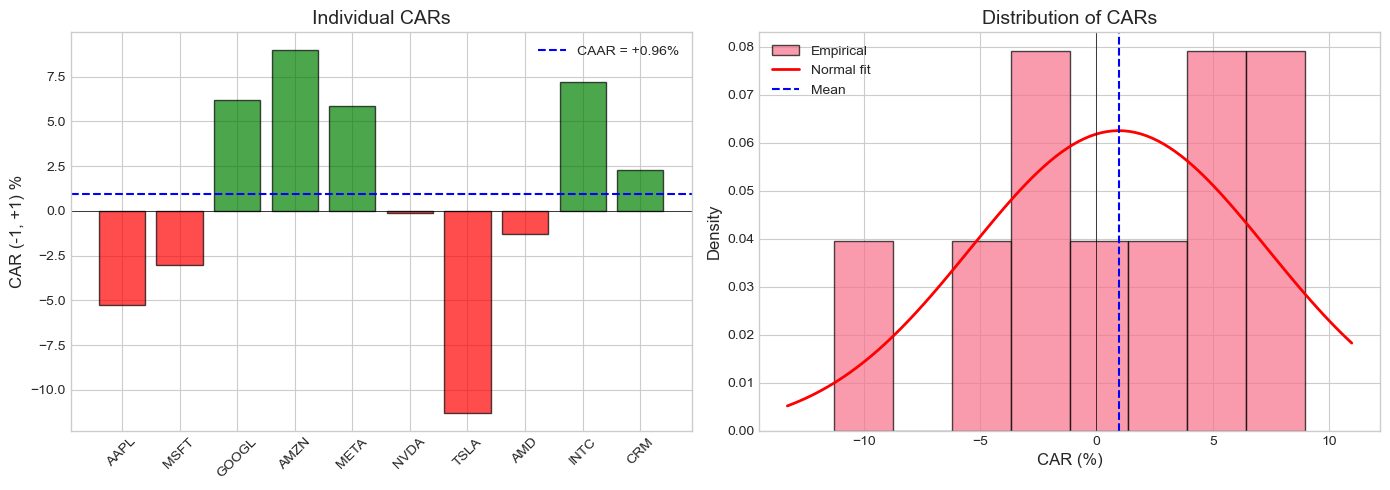

Window [-1, +1]:

CAAR = +0.959%

Std. Dev. = 6.380%

t-stat = 0.475

p-value = 0.6459

Window [+0, +0]:

CAAR = +0.600%

Std. Dev. = 1.223%

t-stat = 1.550

p-value = 0.1556

Window [-5, +5]:

CAAR = -0.761%

Std. Dev. = 6.559%

t-stat = -0.367

p-value = 0.7223

Window [-10, +10]:

CAAR = -5.226%

Std. Dev. = 7.930%

t-stat = -2.084 *

p-value = 0.0669

======================================================================

Significance: * p<0.10, ** p<0.05, *** p<0.01

Source

# Visualize individual CARs and distribution

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

# Get CAR(-1,+1) results

result = cs_results[0] # (-1, +1) window

cars = result['individual_cars']

tickers = [r.ticker for r in event_results]

# Bar chart of individual CARs

ax1 = axes[0]

colors = ['green' if c >= 0 else 'red' for c in cars]

bars = ax1.bar(tickers, cars * 100, color=colors, alpha=0.7, edgecolor='black')

ax1.axhline(0, color='black', linewidth=0.5)

ax1.axhline(result['CAAR'] * 100, color='blue', linestyle='--',

label=f'CAAR = {result["CAAR"]*100:+.2f}%')

ax1.set_ylabel('CAR (-1, +1) %', fontsize=12)

ax1.set_title('Individual CARs', fontsize=14)

ax1.legend()

ax1.tick_params(axis='x', rotation=45)

# Distribution of CARs

ax2 = axes[1]

ax2.hist(cars * 100, bins=8, density=True, alpha=0.7, edgecolor='black', label='Empirical')

# Overlay normal distribution

x = np.linspace(cars.min()*100 - 2, cars.max()*100 + 2, 100)

y = stats.norm.pdf(x, result['CAAR']*100, result['std_dev']*100)

ax2.plot(x, y, 'r-', linewidth=2, label='Normal fit')

ax2.axvline(0, color='black', linestyle='-', linewidth=0.5)

ax2.axvline(result['CAAR']*100, color='blue', linestyle='--', label='Mean')

ax2.set_xlabel('CAR (%)', fontsize=12)

ax2.set_ylabel('Density', fontsize=12)

ax2.set_title('Distribution of CARs', fontsize=14)

ax2.legend()

plt.tight_layout()

plt.show()

4. Test 2: Time-Series Standard Error Approach¶

Alternative Variance Estimation¶

Instead of using cross-sectional variation, we can use the time-series variance from the estimation period:

Where is the length of the event window.

Aggregated Test Statistic¶

Comparison¶

| Approach | Variance Source | Pros | Cons |

|---|---|---|---|

| Cross-sectional | Event window | Captures heterogeneity | Needs many events |

| Time-series | Estimation window | Works with few events | Assumes stable variance |

Source

def calculate_car_variance_ts(model: MarketModelResults,

event_data: pd.DataFrame,

tau1: int, tau2: int) -> float:

"""

Calculate time-series variance of CAR.

Includes adjustment for estimation error in alpha and beta.

"""

mask = (event_data['event_time'] >= tau1) & (event_data['event_time'] <= tau2)

window_data = event_data[mask]

L = len(window_data)

T = model.n_obs

sigma_sq = model.sigma ** 2

Rm_bar = model.market_mean

sum_sq = model.market_var

# Sum of market return deviations in event window

Rm_event = window_data['market_ret'].values

sum_dev_sq = np.sum((Rm_event - Rm_bar) ** 2)

# Variance formula (Campbell, Lo, MacKinlay 1997, eq. 4.8)

var = sigma_sq * (L + L**2/T + sum_dev_sq/sum_sq)

return var

def time_series_t_test(event_results: List[EventStudyResult],

tau1: int, tau2: int) -> Dict:

"""

Time-series variance t-test for CAAR.

Uses estimation period variance instead of cross-sectional variance.

"""

cars = []

car_vars = []

for r in event_results:

car = calculate_car(r.event_data, tau1, tau2)

var = calculate_car_variance_ts(r.model, r.event_data, tau1, tau2)

cars.append(car)

car_vars.append(var)

cars = np.array(cars)

car_vars = np.array(car_vars)

N = len(cars)

caar = np.mean(cars)

# Time-series aggregated variance

# Assuming independence: Var(CAAR) = (1/N^2) * sum(Var(CAR_i))

var_caar = np.sum(car_vars) / (N ** 2)

se_caar = np.sqrt(var_caar)

t_stat = caar / se_caar if se_caar > 0 else 0

# Approximate df (conservative)

df = N * (ESTIMATION_WINDOW - 2)

p_value = 2 * (1 - stats.t.cdf(abs(t_stat), df=df))

return {

'test_name': 'Time-Series t-Test',

'N': N,

'CAAR': caar,

'var_caar': var_caar,

'std_error': se_caar,

't_stat': t_stat,

'df': df,

'p_value': p_value,

'individual_cars': cars,

'individual_vars': car_vars

}

# Compare cross-sectional and time-series tests

print("Cross-Sectional vs Time-Series t-Tests:")

print("="*80)

comparison_data = []

for tau1, tau2 in windows:

cs = cross_sectional_t_test(event_results, tau1, tau2)

ts = time_series_t_test(event_results, tau1, tau2)

comparison_data.append({

'Window': f'[{tau1:+d},{tau2:+d}]',

'CAAR': cs['CAAR'],

'CS_SE': cs['std_error'],

'CS_t': cs['t_stat'],

'CS_p': cs['p_value'],

'TS_SE': ts['std_error'],

'TS_t': ts['t_stat'],

'TS_p': ts['p_value']

})

comp_df = pd.DataFrame(comparison_data)

display_comp = comp_df.copy()

display_comp['CAAR'] = display_comp['CAAR'].apply(lambda x: f"{x*100:+.3f}%")

display_comp['CS_SE'] = display_comp['CS_SE'].apply(lambda x: f"{x*100:.3f}%")

display_comp['TS_SE'] = display_comp['TS_SE'].apply(lambda x: f"{x*100:.3f}%")

for col in ['CS_t', 'TS_t']:

display_comp[col] = display_comp[col].apply(lambda x: f"{x:+.3f}")

for col in ['CS_p', 'TS_p']:

display_comp[col] = display_comp[col].apply(lambda x: f"{x:.4f}")

print(display_comp.to_string(index=False))

print("\nCS = Cross-Sectional, TS = Time-Series")Cross-Sectional vs Time-Series t-Tests:

================================================================================

Window CAAR CS_SE CS_t CS_p TS_SE TS_t TS_p

[-1,+1] +0.959% 2.018% +0.475 0.6459 1.271% +0.755 0.4506

[+0,+0] +0.600% 0.387% +1.550 0.1556 0.727% +0.825 0.4095

[-5,+5] -0.761% 2.074% -0.367 0.7223 2.509% -0.303 0.7618

[-10,+10] -5.226% 2.508% -2.084 0.0669 3.595% -1.454 0.1463

CS = Cross-Sectional, TS = Time-Series

5. Test 3: Patell (1976) Standardized Residual Test¶

Motivation¶

The simple tests treat all firms equally, but firms have different estimation period variances. Patell’s test standardizes each firm’s abnormal return by its own standard error.

Standardized Abnormal Return¶

Where:

Standardized CAR¶

Where:

Patell Test Statistic¶

Under the null:

Source

def calculate_sar(event_data: pd.DataFrame, model: MarketModelResults) -> np.ndarray:

"""

Calculate Standardized Abnormal Returns.

"""

T = model.n_obs

sigma = model.sigma

Rm_bar = model.market_mean

sum_sq = model.market_var

Rm = event_data['market_ret'].values

AR = event_data['AR'].values

# Standard error for each AR

S_AR = sigma * np.sqrt(1 + 1/T + (Rm - Rm_bar)**2 / sum_sq)

# Standardized AR

SAR = AR / S_AR

return SAR, S_AR

def calculate_scar(event_data: pd.DataFrame, model: MarketModelResults,

tau1: int, tau2: int) -> Tuple[float, float]:

"""

Calculate Standardized Cumulative Abnormal Return.

Returns: (SCAR, CAR)

"""

mask = (event_data['event_time'] >= tau1) & (event_data['event_time'] <= tau2)

window_data = event_data[mask].copy()

_, S_AR = calculate_sar(window_data, model)

CAR = window_data['AR'].sum()

S_CAR = np.sqrt(np.sum(S_AR**2))

SCAR = CAR / S_CAR if S_CAR > 0 else 0

return SCAR, CAR

def patell_test(event_results: List[EventStudyResult],

tau1: int, tau2: int) -> Dict:

"""

Patell (1976) Standardized Residual Test.

Aggregates standardized CARs across firms.

"""

scars = []

cars = []

adjustment_factors = []

for r in event_results:

scar, car = calculate_scar(r.event_data, r.model, tau1, tau2)

T = r.model.n_obs

# Patell adjustment factor

adj = np.sqrt((T - 4) / (T - 2))

scars.append(scar)

cars.append(car)

adjustment_factors.append(adj)

scars = np.array(scars)

cars = np.array(cars)

adj_factors = np.array(adjustment_factors)

N = len(scars)

# Patell Z-statistic

# Z = (1/sqrt(N)) * sum(SCAR_i * adjustment_i)

Z_patell = np.sum(scars * adj_factors) / np.sqrt(N)

# p-value (standard normal)

p_value = 2 * (1 - stats.norm.cdf(abs(Z_patell)))

return {

'test_name': 'Patell (1976)',

'N': N,

'CAAR': np.mean(cars),

'mean_SCAR': np.mean(scars),

'Z_stat': Z_patell,

'p_value': p_value,

'individual_scars': scars,

'individual_cars': cars

}

# Run Patell test

print("Patell (1976) Standardized Residual Test:")

print("="*70)

patell_results = []

for tau1, tau2 in windows:

result = patell_test(event_results, tau1, tau2)

patell_results.append(result)

sig = '***' if result['p_value'] < 0.01 else '**' if result['p_value'] < 0.05 else '*' if result['p_value'] < 0.10 else ''

print(f"\nWindow [{tau1:+d}, {tau2:+d}]:")

print(f" CAAR = {result['CAAR']*100:+.3f}%")

print(f" Mean SCAR = {result['mean_SCAR']:+.3f}")

print(f" Z-stat = {result['Z_stat']:+.3f} {sig}")

print(f" p-value = {result['p_value']:.4f}")Patell (1976) Standardized Residual Test:

======================================================================

Window [-1, +1]:

CAAR = +0.959%

Mean SCAR = +0.175

Z-stat = +0.550

p-value = 0.5825

Window [+0, +0]:

CAAR = +0.600%

Mean SCAR = +0.252

Z-stat = +0.790

p-value = 0.4298

Window [-5, +5]:

CAAR = -0.761%

Mean SCAR = -0.244

Z-stat = -0.764

p-value = 0.4449

Window [-10, +10]:

CAAR = -5.226%

Mean SCAR = -0.592

Z-stat = -1.858 *

p-value = 0.0632

6. Test 4: Boehmer, Musumeci, and Poulsen (1991) Test¶

The Event-Induced Variance Problem¶

The Patell test can be severely misspecified when events induce changes in variance. If the event increases volatility, Patell’s test will over-reject the null.

BMP Solution¶

Use the cross-sectional variance of standardized abnormal returns instead of assuming unit variance:

Where:

Why It Works¶

If event-induced variance affects all firms similarly, the cross-sectional variance of SCARs will capture it, providing a more robust test.

Source

def bmp_test(event_results: List[EventStudyResult],

tau1: int, tau2: int) -> Dict:

"""

Boehmer, Musumeci, and Poulsen (1991) Test.

Uses cross-sectional standard error of SCARs to account for

event-induced variance changes.

"""

scars = []

cars = []

for r in event_results:

scar, car = calculate_scar(r.event_data, r.model, tau1, tau2)

scars.append(scar)

cars.append(car)

scars = np.array(scars)

cars = np.array(cars)

N = len(scars)

# BMP statistic uses cross-sectional variance of SCARs

mean_scar = np.mean(scars)

std_scar = np.std(scars, ddof=1)

se_scar = std_scar / np.sqrt(N)

# Z-statistic

Z_bmp = mean_scar / se_scar if se_scar > 0 else 0

# Under null with event-induced variance, this should be t-distributed

p_value = 2 * (1 - stats.t.cdf(abs(Z_bmp), df=N-1))

return {

'test_name': 'BMP (1991)',

'N': N,

'CAAR': np.mean(cars),

'mean_SCAR': mean_scar,

'std_SCAR': std_scar,

'se_SCAR': se_scar,

't_stat': Z_bmp,

'df': N - 1,

'p_value': p_value,

'individual_scars': scars,

'individual_cars': cars

}

# Run BMP test

print("Boehmer-Musumeci-Poulsen (1991) Test:")

print("="*70)

bmp_results = []

for tau1, tau2 in windows:

result = bmp_test(event_results, tau1, tau2)

bmp_results.append(result)

sig = '***' if result['p_value'] < 0.01 else '**' if result['p_value'] < 0.05 else '*' if result['p_value'] < 0.10 else ''

print(f"\nWindow [{tau1:+d}, {tau2:+d}]:")

print(f" CAAR = {result['CAAR']*100:+.3f}%")

print(f" Mean SCAR = {result['mean_SCAR']:+.3f}")

print(f" Std. SCAR = {result['std_SCAR']:.3f}")

print(f" t-stat = {result['t_stat']:+.3f} {sig}")

print(f" p-value = {result['p_value']:.4f}")Boehmer-Musumeci-Poulsen (1991) Test:

======================================================================

Window [-1, +1]:

CAAR = +0.959%

Mean SCAR = +0.175

Std. SCAR = 2.048

t-stat = +0.271

p-value = 0.7927

Window [+0, +0]:

CAAR = +0.600%

Mean SCAR = +0.252

Std. SCAR = 0.565

t-stat = +1.410

p-value = 0.1923

Window [-5, +5]:

CAAR = -0.761%

Mean SCAR = -0.244

Std. SCAR = 1.335

t-stat = -0.577

p-value = 0.5781

Window [-10, +10]:

CAAR = -5.226%

Mean SCAR = -0.592

Std. SCAR = 1.044

t-stat = -1.794

p-value = 0.1064

Source

# Compare Patell vs BMP

print("\nPatell vs BMP Comparison:")

print("="*80)

print("\nIf Std. SCAR > 1, events are increasing variance (BMP is more conservative)")

print("If Std. SCAR < 1, events are decreasing variance (BMP is more powerful)\n")

pvb_data = []

for i, (tau1, tau2) in enumerate(windows):

patell = patell_results[i]

bmp = bmp_results[i]

pvb_data.append({

'Window': f'[{tau1:+d},{tau2:+d}]',

'Patell_Z': patell['Z_stat'],

'Patell_p': patell['p_value'],

'BMP_t': bmp['t_stat'],

'BMP_p': bmp['p_value'],

'Std_SCAR': bmp['std_SCAR'],

'Variance_Effect': 'Increase' if bmp['std_SCAR'] > 1.1 else 'Decrease' if bmp['std_SCAR'] < 0.9 else 'Neutral'

})

pvb_df = pd.DataFrame(pvb_data)

display_pvb = pvb_df.copy()

for col in ['Patell_Z', 'BMP_t']:

display_pvb[col] = display_pvb[col].apply(lambda x: f"{x:+.3f}")

for col in ['Patell_p', 'BMP_p']:

display_pvb[col] = display_pvb[col].apply(lambda x: f"{x:.4f}")

display_pvb['Std_SCAR'] = display_pvb['Std_SCAR'].apply(lambda x: f"{x:.3f}")

print(display_pvb.to_string(index=False))

Patell vs BMP Comparison:

================================================================================

If Std. SCAR > 1, events are increasing variance (BMP is more conservative)

If Std. SCAR < 1, events are decreasing variance (BMP is more powerful)

Window Patell_Z Patell_p BMP_t BMP_p Std_SCAR Variance_Effect

[-1,+1] +0.550 0.5825 +0.271 0.7927 2.048 Increase

[+0,+0] +0.790 0.4298 +1.410 0.1923 0.565 Decrease

[-5,+5] -0.764 0.4449 -0.577 0.5781 1.335 Increase

[-10,+10] -1.858 0.0632 -1.794 0.1064 1.044 Neutral

7. Test 5: Kolari and Pynnönen (2010) Adjusted BMP¶

Cross-Correlation Problem¶

When events cluster in calendar time, abnormal returns may be cross-sectionally correlated. This violates the independence assumption and inflates test statistics.

Adjustment¶

Kolari and Pynnönen (2010) propose adjusting the BMP test for cross-correlation:

Where is the average cross-correlation of abnormal returns in the estimation period.

Source

def estimate_cross_correlation(event_results: List[EventStudyResult]) -> float:

"""

Estimate average cross-correlation of residuals.

Uses estimation period residuals to estimate cross-sectional correlation.

"""

# Collect residuals (may have different lengths/dates, so we use pairwise correlation)

residuals_list = [r.model.residuals for r in event_results]

N = len(residuals_list)

if N < 2:

return 0.0

# Calculate pairwise correlations

correlations = []

for i in range(N):

for j in range(i+1, N):

# Use minimum common length

min_len = min(len(residuals_list[i]), len(residuals_list[j]))

if min_len > 10:

corr = np.corrcoef(residuals_list[i][:min_len],

residuals_list[j][:min_len])[0, 1]

if not np.isnan(corr):

correlations.append(corr)

return np.mean(correlations) if correlations else 0.0

def kolari_pynnonen_test(event_results: List[EventStudyResult],

tau1: int, tau2: int) -> Dict:

"""

Kolari and Pynnönen (2010) adjusted BMP test.

Adjusts for cross-sectional correlation of abnormal returns.

"""

# First get BMP results

bmp = bmp_test(event_results, tau1, tau2)

N = bmp['N']

t_bmp = bmp['t_stat']

# Estimate cross-correlation

r_bar = estimate_cross_correlation(event_results)

# Adjustment factor

if r_bar >= 1/(1-N): # Avoid negative under radical

adj_factor = 0.01 # Very small adjustment

else:

adj_factor = np.sqrt((1 - r_bar) / (1 + (N-1) * r_bar))

# Adjusted t-statistic

t_adj = t_bmp * adj_factor

# p-value

p_value = 2 * (1 - stats.t.cdf(abs(t_adj), df=N-1))

return {

'test_name': 'Kolari-Pynnönen (2010)',

'N': N,

'CAAR': bmp['CAAR'],

'mean_SCAR': bmp['mean_SCAR'],

't_BMP': t_bmp,

'r_bar': r_bar,

'adj_factor': adj_factor,

't_adjusted': t_adj,

'p_value': p_value

}

# Run Kolari-Pynnönen test

print("Kolari-Pynnönen (2010) Adjusted Test:")

print("="*70)

# First show cross-correlation estimate

r_bar = estimate_cross_correlation(event_results)

print(f"\nEstimated average cross-correlation: {r_bar:.4f}")

print("(High correlation requires larger adjustment)\n")

kp_results = []

for tau1, tau2 in windows:

result = kolari_pynnonen_test(event_results, tau1, tau2)

kp_results.append(result)

sig = '***' if result['p_value'] < 0.01 else '**' if result['p_value'] < 0.05 else '*' if result['p_value'] < 0.10 else ''

print(f"Window [{tau1:+d}, {tau2:+d}]:")

print(f" BMP t-stat = {result['t_BMP']:+.3f}")

print(f" Adjustment factor = {result['adj_factor']:.3f}")

print(f" Adjusted t-stat = {result['t_adjusted']:+.3f} {sig}")

print(f" p-value = {result['p_value']:.4f}\n")Kolari-Pynnönen (2010) Adjusted Test:

======================================================================

Estimated average cross-correlation: 0.0203

(High correlation requires larger adjustment)

Window [-1, +1]:

BMP t-stat = +0.271

Adjustment factor = 0.010

Adjusted t-stat = +0.003

p-value = 0.9979

Window [+0, +0]:

BMP t-stat = +1.410

Adjustment factor = 0.010

Adjusted t-stat = +0.014

p-value = 0.9891

Window [-5, +5]:

BMP t-stat = -0.577

Adjustment factor = 0.010

Adjusted t-stat = -0.006

p-value = 0.9955

Window [-10, +10]:

BMP t-stat = -1.794

Adjustment factor = 0.010

Adjusted t-stat = -0.018

p-value = 0.9861

8. Comprehensive Test Comparison¶

Let’s compare all parametric tests side by side.

Source

def run_all_parametric_tests(event_results: List[EventStudyResult],

tau1: int, tau2: int) -> pd.DataFrame:

"""

Run all parametric tests and return comparison table.

"""

cs = cross_sectional_t_test(event_results, tau1, tau2)

ts = time_series_t_test(event_results, tau1, tau2)

patell = patell_test(event_results, tau1, tau2)

bmp = bmp_test(event_results, tau1, tau2)

kp = kolari_pynnonen_test(event_results, tau1, tau2)

results = [

{'Test': 'Cross-Sectional t', 'Statistic': cs['t_stat'], 'p-value': cs['p_value']},

{'Test': 'Time-Series t', 'Statistic': ts['t_stat'], 'p-value': ts['p_value']},

{'Test': 'Patell Z', 'Statistic': patell['Z_stat'], 'p-value': patell['p_value']},

{'Test': 'BMP t', 'Statistic': bmp['t_stat'], 'p-value': bmp['p_value']},

{'Test': 'Kolari-Pynnönen t', 'Statistic': kp['t_adjusted'], 'p-value': kp['p_value']},

]

return pd.DataFrame(results)

# Create comprehensive comparison

print("\n" + "="*90)

print("COMPREHENSIVE PARAMETRIC TEST COMPARISON")

print("="*90)

for tau1, tau2 in windows:

print(f"\n\nWindow [{tau1:+d}, {tau2:+d}]")

print("-" * 60)

# Get CAAR for reference

cars = [calculate_car(r.event_data, tau1, tau2) for r in event_results]

caar = np.mean(cars)

print(f"CAAR = {caar*100:+.3f}% (N = {len(event_results)})\n")

results = run_all_parametric_tests(event_results, tau1, tau2)

# Add significance markers

def sig_marker(p):

if p < 0.01: return '***'

elif p < 0.05: return '**'

elif p < 0.10: return '*'

else: return ''

results['Sig'] = results['p-value'].apply(sig_marker)

results['Statistic'] = results['Statistic'].apply(lambda x: f"{x:+.3f}")

results['p-value'] = results['p-value'].apply(lambda x: f"{x:.4f}")

print(results.to_string(index=False))

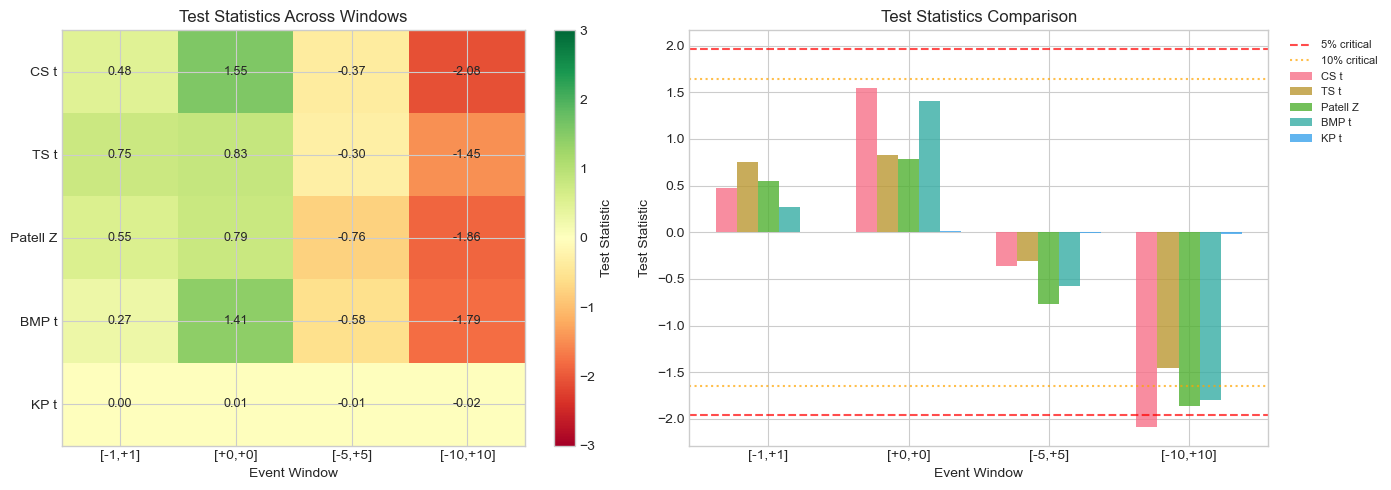

==========================================================================================

COMPREHENSIVE PARAMETRIC TEST COMPARISON

==========================================================================================

Window [-1, +1]

------------------------------------------------------------

CAAR = +0.959% (N = 10)

Test Statistic p-value Sig

Cross-Sectional t +0.475 0.6459

Time-Series t +0.755 0.4506

Patell Z +0.550 0.5825

BMP t +0.271 0.7927

Kolari-Pynnönen t +0.003 0.9979

Window [+0, +0]

------------------------------------------------------------

CAAR = +0.600% (N = 10)

Test Statistic p-value Sig

Cross-Sectional t +1.550 0.1556

Time-Series t +0.825 0.4095

Patell Z +0.790 0.4298

BMP t +1.410 0.1923

Kolari-Pynnönen t +0.014 0.9891

Window [-5, +5]

------------------------------------------------------------

CAAR = -0.761% (N = 10)

Test Statistic p-value Sig

Cross-Sectional t -0.367 0.7223

Time-Series t -0.303 0.7618

Patell Z -0.764 0.4449

BMP t -0.577 0.5781

Kolari-Pynnönen t -0.006 0.9955

Window [-10, +10]

------------------------------------------------------------

CAAR = -5.226% (N = 10)

Test Statistic p-value Sig

Cross-Sectional t -2.084 0.0669 *

Time-Series t -1.454 0.1463

Patell Z -1.858 0.0632 *

BMP t -1.794 0.1064

Kolari-Pynnönen t -0.018 0.9861

Source

# Visualize test statistics comparison

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

# Collect test statistics for all windows

test_names = ['CS t', 'TS t', 'Patell Z', 'BMP t', 'KP t']

window_labels = [f'[{t1:+d},{t2:+d}]' for t1, t2 in windows]

stats_matrix = np.zeros((len(windows), len(test_names)))

for i, (tau1, tau2) in enumerate(windows):

cs = cross_sectional_t_test(event_results, tau1, tau2)

ts = time_series_t_test(event_results, tau1, tau2)

patell = patell_test(event_results, tau1, tau2)

bmp = bmp_test(event_results, tau1, tau2)

kp = kolari_pynnonen_test(event_results, tau1, tau2)

stats_matrix[i, :] = [cs['t_stat'], ts['t_stat'], patell['Z_stat'],

bmp['t_stat'], kp['t_adjusted']]

# Heatmap of test statistics

ax1 = axes[0]

im = ax1.imshow(stats_matrix.T, cmap='RdYlGn', aspect='auto', vmin=-3, vmax=3)

ax1.set_xticks(range(len(windows)))

ax1.set_xticklabels(window_labels)

ax1.set_yticks(range(len(test_names)))

ax1.set_yticklabels(test_names)

ax1.set_xlabel('Event Window')

ax1.set_title('Test Statistics Across Windows')

# Add value annotations

for i in range(len(test_names)):

for j in range(len(windows)):

ax1.text(j, i, f'{stats_matrix[j, i]:.2f}', ha='center', va='center', fontsize=9)

plt.colorbar(im, ax=ax1, label='Test Statistic')

# Critical value lines for reference

ax2 = axes[1]

x = np.arange(len(windows))

width = 0.15

for i, test in enumerate(test_names):

ax2.bar(x + i*width, stats_matrix[:, i], width, label=test, alpha=0.8)

ax2.axhline(1.96, color='red', linestyle='--', alpha=0.7, label='5% critical')

ax2.axhline(-1.96, color='red', linestyle='--', alpha=0.7)

ax2.axhline(1.645, color='orange', linestyle=':', alpha=0.7, label='10% critical')

ax2.axhline(-1.645, color='orange', linestyle=':', alpha=0.7)

ax2.set_xticks(x + 2*width)

ax2.set_xticklabels(window_labels)

ax2.set_xlabel('Event Window')

ax2.set_ylabel('Test Statistic')

ax2.set_title('Test Statistics Comparison')

ax2.legend(bbox_to_anchor=(1.02, 1), loc='upper left', fontsize=8)

plt.tight_layout()

plt.show()

9. Power Analysis: Monte Carlo Simulation¶

Understanding Test Power¶

Power = Probability of rejecting when it is false

We want tests with:

Correct size (reject at stated significance level under )

High power (detect true effects)

Simulation Setup¶

Generate synthetic abnormal returns with known properties

Apply different tests

Measure rejection rates under (size) and (power)

Source

def simulate_event_study(N: int, T_est: int, L_event: int,

true_car: float = 0.0,

sigma: float = 0.02,

event_variance_multiplier: float = 1.0) -> List[Dict]:

"""

Simulate event study data for power analysis.

Parameters:

-----------

N : int

Number of events

T_est : int

Estimation window length

L_event : int

Event window length

true_car : float

True cumulative abnormal return (0 under null)

sigma : float

Residual standard deviation

event_variance_multiplier : float

Multiplier for event window variance (>1 means event-induced variance)

Returns:

--------

List of simulated event results

"""

results = []

# True abnormal return per day (spread evenly)

true_ar_daily = true_car / L_event

for i in range(N):

# Generate estimation period residuals

est_residuals = np.random.normal(0, sigma, T_est)

# Generate event window abnormal returns

event_sigma = sigma * np.sqrt(event_variance_multiplier)

event_ar = np.random.normal(true_ar_daily, event_sigma, L_event)

# Create mock model

model = MarketModelResults(

alpha=0.0,

beta=1.0,

sigma=np.std(est_residuals, ddof=2),

r_squared=0.3,

n_obs=T_est,

market_mean=0.0005,

market_var=T_est * 0.0001,

residuals=est_residuals

)

# Create event data

event_data = pd.DataFrame({

'event_time': range(-L_event//2, L_event//2 + L_event%2),

'stock_ret': event_ar + 0.0005, # Add expected return

'market_ret': np.random.normal(0.0005, 0.01, L_event),

'expected_ret': np.full(L_event, 0.0005),

'AR': event_ar

})

results.append({

'model': model,

'event_data': event_data

})

return results

def run_simulation_tests(sim_results: List[Dict], tau1: int, tau2: int) -> Dict:

"""

Run all tests on simulated data.

"""

# Convert to format expected by test functions

class MockResult:

def __init__(self, d):

self.model = d['model']

self.event_data = d['event_data']

mock_results = [MockResult(d) for d in sim_results]

cs = cross_sectional_t_test(mock_results, tau1, tau2)

patell = patell_test(mock_results, tau1, tau2)

bmp = bmp_test(mock_results, tau1, tau2)

return {

'CS_p': cs['p_value'],

'Patell_p': patell['p_value'],

'BMP_p': bmp['p_value']

}

def monte_carlo_power(N_events: int, N_sims: int, true_car: float,

event_var_mult: float = 1.0,

alpha: float = 0.05) -> Dict:

"""

Monte Carlo simulation for test power/size.

"""

rejections = {'CS': 0, 'Patell': 0, 'BMP': 0}

for _ in range(N_sims):

sim_data = simulate_event_study(

N=N_events, T_est=120, L_event=3,

true_car=true_car, sigma=0.02,

event_variance_multiplier=event_var_mult

)

results = run_simulation_tests(sim_data, -1, 1)

if results['CS_p'] < alpha:

rejections['CS'] += 1

if results['Patell_p'] < alpha:

rejections['Patell'] += 1

if results['BMP_p'] < alpha:

rejections['BMP'] += 1

return {

'CS_rejection_rate': rejections['CS'] / N_sims,

'Patell_rejection_rate': rejections['Patell'] / N_sims,

'BMP_rejection_rate': rejections['BMP'] / N_sims

}

print("Monte Carlo Simulation: Test Size and Power")

print("="*70)

print("(This may take a moment...)\n")

N_SIMS = 500 # Reduced for speed; use 1000+ for research

N_EVENTS = 30

# Test size under H0 (true_car = 0)

print("1. SIZE (H0: CAR = 0, No event-induced variance)")

size_results = monte_carlo_power(N_EVENTS, N_SIMS, true_car=0.0, event_var_mult=1.0)

print(f" CS t-test: {size_results['CS_rejection_rate']*100:.1f}% (nominal: 5%)")

print(f" Patell test: {size_results['Patell_rejection_rate']*100:.1f}%")

print(f" BMP test: {size_results['BMP_rejection_rate']*100:.1f}%")

# Test size with event-induced variance

print("\n2. SIZE WITH EVENT-INDUCED VARIANCE (H0: CAR = 0, Variance x2)")

size_eiv = monte_carlo_power(N_EVENTS, N_SIMS, true_car=0.0, event_var_mult=2.0)

print(f" CS t-test: {size_eiv['CS_rejection_rate']*100:.1f}%")

print(f" Patell test: {size_eiv['Patell_rejection_rate']*100:.1f}% <- Over-rejects!")

print(f" BMP test: {size_eiv['BMP_rejection_rate']*100:.1f}% <- Robust")

# Test power

print("\n3. POWER (H1: CAR = 1%)")

power_results = monte_carlo_power(N_EVENTS, N_SIMS, true_car=0.01, event_var_mult=1.0)

print(f" CS t-test: {power_results['CS_rejection_rate']*100:.1f}%")

print(f" Patell test: {power_results['Patell_rejection_rate']*100:.1f}%")

print(f" BMP test: {power_results['BMP_rejection_rate']*100:.1f}%")Monte Carlo Simulation: Test Size and Power

======================================================================

(This may take a moment...)

1. SIZE (H0: CAR = 0, No event-induced variance)

---------------------------------------------------------------------------

ValueError Traceback (most recent call last)

Cell In[31], line 132

130 # Test size under H0 (true_car = 0)

131 print("1. SIZE (H0: CAR = 0, No event-induced variance)")

--> 132 size_results = monte_carlo_power(N_EVENTS, N_SIMS, true_car=0.0, event_var_mult=1.0)

133 print(f" CS t-test: {size_results['CS_rejection_rate']*100:.1f}% (nominal: 5%)")

134 print(f" Patell test: {size_results['Patell_rejection_rate']*100:.1f}%")

Cell In[31], line 101, in monte_carlo_power(N_events, N_sims, true_car, event_var_mult, alpha)

98 rejections = {'CS': 0, 'Patell': 0, 'BMP': 0}

100 for _ in range(N_sims):

--> 101 sim_data = simulate_event_study(

102 N=N_events, T_est=120, L_event=3,

103 true_car=true_car, sigma=0.02,

104 event_variance_multiplier=event_var_mult

105 )

107 results = run_simulation_tests(sim_data, -1, 1)

109 if results['CS_p'] < alpha:

Cell In[31], line 53, in simulate_event_study(N, T_est, L_event, true_car, sigma, event_variance_multiplier)

41 model = MarketModelResults(

42 alpha=0.0,

43 beta=1.0,

(...)

49 residuals=est_residuals

50 )

52 # Create event data

---> 53 event_data = pd.DataFrame({

54 'event_time': range(-L_event//2, L_event//2 + L_event%2),

55 'stock_ret': event_ar + 0.0005, # Add expected return

56 'market_ret': np.random.normal(0.0005, 0.01, L_event),

57 'expected_ret': np.full(L_event, 0.0005),

58 'AR': event_ar

59 })

61 results.append({

62 'model': model,

63 'event_data': event_data

64 })

66 return results

File ~\AppData\Local\anaconda3\Lib\site-packages\pandas\core\frame.py:778, in DataFrame.__init__(self, data, index, columns, dtype, copy)

772 mgr = self._init_mgr(

773 data, axes={"index": index, "columns": columns}, dtype=dtype, copy=copy

774 )

776 elif isinstance(data, dict):

777 # GH#38939 de facto copy defaults to False only in non-dict cases

--> 778 mgr = dict_to_mgr(data, index, columns, dtype=dtype, copy=copy, typ=manager)

779 elif isinstance(data, ma.MaskedArray):

780 from numpy.ma import mrecords

File ~\AppData\Local\anaconda3\Lib\site-packages\pandas\core\internals\construction.py:503, in dict_to_mgr(data, index, columns, dtype, typ, copy)

499 else:

500 # dtype check to exclude e.g. range objects, scalars

501 arrays = [x.copy() if hasattr(x, "dtype") else x for x in arrays]

--> 503 return arrays_to_mgr(arrays, columns, index, dtype=dtype, typ=typ, consolidate=copy)

File ~\AppData\Local\anaconda3\Lib\site-packages\pandas\core\internals\construction.py:114, in arrays_to_mgr(arrays, columns, index, dtype, verify_integrity, typ, consolidate)

111 if verify_integrity:

112 # figure out the index, if necessary

113 if index is None:

--> 114 index = _extract_index(arrays)

115 else:

116 index = ensure_index(index)

File ~\AppData\Local\anaconda3\Lib\site-packages\pandas\core\internals\construction.py:677, in _extract_index(data)

675 lengths = list(set(raw_lengths))

676 if len(lengths) > 1:

--> 677 raise ValueError("All arrays must be of the same length")

679 if have_dicts:

680 raise ValueError(

681 "Mixing dicts with non-Series may lead to ambiguous ordering."

682 )

ValueError: All arrays must be of the same lengthSource

# Power curve as function of true CAR

print("\nGenerating power curves (this may take a minute)...")

true_cars = [0, 0.005, 0.01, 0.015, 0.02, 0.025, 0.03]

power_data = {'CAR': [], 'CS': [], 'Patell': [], 'BMP': []}

for car in true_cars:

result = monte_carlo_power(N_EVENTS, 300, true_car=car)

power_data['CAR'].append(car * 100)

power_data['CS'].append(result['CS_rejection_rate'] * 100)

power_data['Patell'].append(result['Patell_rejection_rate'] * 100)

power_data['BMP'].append(result['BMP_rejection_rate'] * 100)

print(f" CAR = {car*100:.1f}%: CS={result['CS_rejection_rate']*100:.0f}%, "

f"Patell={result['Patell_rejection_rate']*100:.0f}%, "

f"BMP={result['BMP_rejection_rate']*100:.0f}%")

# Plot power curves

fig, ax = plt.subplots(figsize=(10, 6))

ax.plot(power_data['CAR'], power_data['CS'], 'b-o', label='CS t-test', markersize=8)

ax.plot(power_data['CAR'], power_data['Patell'], 'g-s', label='Patell', markersize=8)

ax.plot(power_data['CAR'], power_data['BMP'], 'r-^', label='BMP', markersize=8)

ax.axhline(5, color='gray', linestyle='--', alpha=0.7, label='5% significance')

ax.axhline(80, color='gray', linestyle=':', alpha=0.7, label='80% power target')

ax.set_xlabel('True CAR (%)', fontsize=12)

ax.set_ylabel('Rejection Rate (%)', fontsize=12)

ax.set_title(f'Power Curves (N={N_EVENTS} events, 5% significance)', fontsize=14)

ax.legend()

ax.grid(True, alpha=0.3)

ax.set_ylim(0, 100)

plt.tight_layout()

plt.show()

Generating power curves (this may take a minute)...

---------------------------------------------------------------------------

ValueError Traceback (most recent call last)

Cell In[33], line 8

5 power_data = {'CAR': [], 'CS': [], 'Patell': [], 'BMP': []}

7 for car in true_cars:

----> 8 result = monte_carlo_power(N_EVENTS, 300, true_car=car)

9 power_data['CAR'].append(car * 100)

10 power_data['CS'].append(result['CS_rejection_rate'] * 100)

Cell In[31], line 101, in monte_carlo_power(N_events, N_sims, true_car, event_var_mult, alpha)

98 rejections = {'CS': 0, 'Patell': 0, 'BMP': 0}

100 for _ in range(N_sims):

--> 101 sim_data = simulate_event_study(

102 N=N_events, T_est=120, L_event=3,

103 true_car=true_car, sigma=0.02,

104 event_variance_multiplier=event_var_mult

105 )

107 results = run_simulation_tests(sim_data, -1, 1)

109 if results['CS_p'] < alpha:

Cell In[31], line 53, in simulate_event_study(N, T_est, L_event, true_car, sigma, event_variance_multiplier)

41 model = MarketModelResults(

42 alpha=0.0,

43 beta=1.0,

(...)

49 residuals=est_residuals

50 )

52 # Create event data

---> 53 event_data = pd.DataFrame({

54 'event_time': range(-L_event//2, L_event//2 + L_event%2),

55 'stock_ret': event_ar + 0.0005, # Add expected return

56 'market_ret': np.random.normal(0.0005, 0.01, L_event),

57 'expected_ret': np.full(L_event, 0.0005),

58 'AR': event_ar

59 })

61 results.append({

62 'model': model,

63 'event_data': event_data

64 })

66 return results

File ~\AppData\Local\anaconda3\Lib\site-packages\pandas\core\frame.py:778, in DataFrame.__init__(self, data, index, columns, dtype, copy)

772 mgr = self._init_mgr(

773 data, axes={"index": index, "columns": columns}, dtype=dtype, copy=copy

774 )

776 elif isinstance(data, dict):

777 # GH#38939 de facto copy defaults to False only in non-dict cases

--> 778 mgr = dict_to_mgr(data, index, columns, dtype=dtype, copy=copy, typ=manager)

779 elif isinstance(data, ma.MaskedArray):

780 from numpy.ma import mrecords

File ~\AppData\Local\anaconda3\Lib\site-packages\pandas\core\internals\construction.py:503, in dict_to_mgr(data, index, columns, dtype, typ, copy)

499 else:

500 # dtype check to exclude e.g. range objects, scalars

501 arrays = [x.copy() if hasattr(x, "dtype") else x for x in arrays]

--> 503 return arrays_to_mgr(arrays, columns, index, dtype=dtype, typ=typ, consolidate=copy)

File ~\AppData\Local\anaconda3\Lib\site-packages\pandas\core\internals\construction.py:114, in arrays_to_mgr(arrays, columns, index, dtype, verify_integrity, typ, consolidate)

111 if verify_integrity:

112 # figure out the index, if necessary

113 if index is None:

--> 114 index = _extract_index(arrays)

115 else:

116 index = ensure_index(index)

File ~\AppData\Local\anaconda3\Lib\site-packages\pandas\core\internals\construction.py:677, in _extract_index(data)

675 lengths = list(set(raw_lengths))

676 if len(lengths) > 1:

--> 677 raise ValueError("All arrays must be of the same length")

679 if have_dicts:

680 raise ValueError(

681 "Mixing dicts with non-Series may lead to ambiguous ordering."

682 )

ValueError: All arrays must be of the same length10. Practical Guidelines¶

Which Test to Use?¶

| Situation | Recommended Test | Reason |

|---|---|---|

| General use | BMP | Robust to event-induced variance |

| No event clustering | Patell | More powerful when assumptions hold |

| Event clustering | Kolari-Pynnönen | Adjusts for cross-correlation |

| Very small sample (N<10) | Cross-sectional t | Simple, interpretable |

| Heterogeneous firms | BMP or KP | Account for variance differences |

Reporting Best Practices¶

Report multiple tests for robustness

Include both CAAR and test statistics

Note sample size and any clustering

Report results for multiple windows

Discuss economic vs. statistical significance

Source

def create_publication_table(event_results: List[EventStudyResult],

windows: List[Tuple[int, int]]) -> pd.DataFrame:

"""

Create a publication-ready results table.

"""

rows = []

for tau1, tau2 in windows:

cars = [calculate_car(r.event_data, tau1, tau2) for r in event_results]

caar = np.mean(cars)

cs = cross_sectional_t_test(event_results, tau1, tau2)

patell = patell_test(event_results, tau1, tau2)

bmp = bmp_test(event_results, tau1, tau2)

def sig(p):

if p < 0.01: return '***'

elif p < 0.05: return '**'

elif p < 0.10: return '*'

return ''

rows.append({

'Window': f'[{tau1:+d}, {tau2:+d}]',

'N': len(event_results),

'CAAR (%)': f"{caar*100:+.2f}",

'CS t-stat': f"{cs['t_stat']:.2f}{sig(cs['p_value'])}",

'Patell Z': f"{patell['Z_stat']:.2f}{sig(patell['p_value'])}",

'BMP t-stat': f"{bmp['t_stat']:.2f}{sig(bmp['p_value'])}"

})

return pd.DataFrame(rows)

# Generate publication table

print("\n" + "="*90)

print("PUBLICATION-READY RESULTS TABLE")

print("="*90)

print("\nTable: Cumulative Average Abnormal Returns Around Earnings Announcements")

print("Sample: Tech companies, Q2-Q3 2023 earnings")

print("-"*90)

pub_table = create_publication_table(event_results, windows)

print(pub_table.to_string(index=False))

print("-"*90)

print("Notes: ***, **, * indicate significance at 1%, 5%, 10% levels.")

print("CS = cross-sectional t-test; Patell = Patell (1976) standardized test;")

print("BMP = Boehmer et al. (1991) standardized cross-sectional test.")

==========================================================================================

PUBLICATION-READY RESULTS TABLE

==========================================================================================

Table: Cumulative Average Abnormal Returns Around Earnings Announcements

Sample: Tech companies, Q2-Q3 2023 earnings

------------------------------------------------------------------------------------------

Window N CAAR (%) CS t-stat Patell Z BMP t-stat

[-1, +1] 10 +0.96 0.48 0.55 0.27

[+0, +0] 10 +0.60 1.55 0.79 1.41

[-5, +5] 10 -0.76 -0.37 -0.76 -0.58

[-10, +10] 10 -5.23 -2.08* -1.86* -1.79

------------------------------------------------------------------------------------------

Notes: ***, **, * indicate significance at 1%, 5%, 10% levels.

CS = cross-sectional t-test; Patell = Patell (1976) standardized test;

BMP = Boehmer et al. (1991) standardized cross-sectional test.

11. Exercises¶

Exercise 1: Sample Size Sensitivity¶

Using Monte Carlo simulation, examine how test power changes with sample size (N = 10, 30, 50, 100).

Exercise 2: Window Length Effects¶

How does test power change as you lengthen the event window? Why?

Exercise 3: Skewness Adjustment¶

Implement a skewness-adjusted t-test that accounts for non-normality in CARs.

Exercise 4: Calendar-Time Portfolio¶

Implement a calendar-time portfolio approach that forms portfolios of event firms and regresses on market factors.

Source

# Exercise 3 Template: Skewness-Adjusted t-Test

def skewness_adjusted_t_test(event_results: List[EventStudyResult],

tau1: int, tau2: int) -> Dict:

"""

Hall (1992) skewness-adjusted t-test.

Adjusts for skewness in the CAR distribution.

"""

cars = np.array([calculate_car(r.event_data, tau1, tau2) for r in event_results])

N = len(cars)

# Standard t-test components

mean_car = np.mean(cars)

std_car = np.std(cars, ddof=1)

se = std_car / np.sqrt(N)

t_standard = mean_car / se if se > 0 else 0

# Skewness

skew = stats.skew(cars)

# Hall (1992) adjustment

# t_adj = t + (1/6) * skew * (t^2 + 2) / sqrt(N)

t_adjusted = t_standard + (1/6) * skew * (t_standard**2 + 2) / np.sqrt(N)

p_value = 2 * (1 - stats.t.cdf(abs(t_adjusted), df=N-1))

return {

'test_name': 'Skewness-Adjusted t',

'N': N,

'CAAR': mean_car,

'skewness': skew,

't_standard': t_standard,

't_adjusted': t_adjusted,

'p_value': p_value

}

# Test the skewness-adjusted t-test

print("Skewness-Adjusted t-Test:")

print("="*50)

for tau1, tau2 in [(-1, +1), (0, 0)]:

result = skewness_adjusted_t_test(event_results, tau1, tau2)

print(f"\nWindow [{tau1:+d}, {tau2:+d}]:")

print(f" Skewness = {result['skewness']:.3f}")

print(f" Standard t = {result['t_standard']:.3f}")

print(f" Adjusted t = {result['t_adjusted']:.3f}")

print(f" p-value = {result['p_value']:.4f}")Skewness-Adjusted t-Test:

==================================================

Window [-1, +1]:

Skewness = -0.507

Standard t = 0.475

Adjusted t = 0.416

p-value = 0.6873

Window [+0, +0]:

Skewness = -0.001

Standard t = 1.550

Adjusted t = 1.550

p-value = 0.1556

12. Summary¶

In this session, we covered:

Cross-Sectional t-Test: Simple but assumes homogeneous variance

Time-Series t-Test: Uses estimation period variance

Patell (1976) Test: Standardizes ARs, more powerful but assumes no event-induced variance

BMP (1991) Test: Robust to event-induced variance changes

Kolari-Pynnönen (2010): Adjusts for cross-correlation

Monte Carlo Analysis: Understanding test size and power

Key Takeaways¶

BMP is the recommended default for most applications

Event-induced variance is common and Patell over-rejects

Cross-correlation from event clustering requires adjustment

Report multiple tests for robustness

Consider economic significance alongside statistical significance

Coming Up Next¶

Session 5: Statistical Inference II - Non-Parametric and Robust Tests will cover:

Sign test and generalized sign test

Rank tests (Corrado, Corrado-Zivney)

Bootstrap methods

Dealing with non-normality

13. References¶

Core Methodology¶

Patell, J. M. (1976). Corporate forecasts of earnings per share and stock price behavior. Journal of Accounting Research, 14(2), 246-276.

Boehmer, E., Musumeci, J., & Poulsen, A. B. (1991). Event-study methodology under conditions of event-induced variance. Journal of Financial Economics, 30(2), 253-272.

Kolari, J. W., & Pynnönen, S. (2010). Event study testing with cross-sectional correlation of abnormal returns. Review of Financial Studies, 23(11), 3996-4025.

Power and Specification¶

Brown, S. J., & Warner, J. B. (1985). Using daily stock returns: The case of event studies. Journal of Financial Economics, 14(1), 3-31.

Campbell, J. Y., Lo, A. W., & MacKinlay, A. C. (1997). The Econometrics of Financial Markets. Princeton University Press.