Session 3: Measuring Abnormal Returns

Event Studies in Finance and Economics - Summer School¶

Learning Objectives¶

By the end of this session, you will be able to:

Calculate and interpret different measures of abnormal returns (AR, CAR, BHAR)

Understand the trade-offs between CAR and BHAR approaches

Compute standardized abnormal returns for improved inference

Translate abnormal returns into economic magnitudes (wealth effects)

Handle multiple events and aggregate abnormal returns across firms

1. Introduction: From Normal to Abnormal¶

In Sessions 1 and 2, we established how to estimate “normal” returns. Now we focus on measuring and interpreting the abnormal component — the return attributable to the event.

The Fundamental Equation¶

Where:

= Abnormal return for firm on day

= Actual (realized) return

= Expected (normal) return from our benchmark model

Why Measurement Matters¶

The choice of how we aggregate abnormal returns over time affects:

Statistical properties of our test statistics

Economic interpretation of the results

Comparability across studies

Bias in long-horizon studies

2. Setup and Data¶

Source

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

from scipy import stats

import yfinance as yf

import statsmodels.api as sm

from datetime import datetime, timedelta

from typing import List, Dict, Tuple, Optional

import warnings

warnings.filterwarnings('ignore')

plt.style.use('seaborn-v0_8-whitegrid')

sns.set_palette("husl")

print("Libraries loaded successfully!")Libraries loaded successfully!

Source

# We'll use multiple events to demonstrate aggregation

EVENTS = [

{'ticker': 'AAPL', 'date': '2023-08-03', 'name': 'Apple Q3 Earnings'},

{'ticker': 'MSFT', 'date': '2023-07-25', 'name': 'Microsoft Q4 Earnings'},

{'ticker': 'GOOGL', 'date': '2023-07-25', 'name': 'Alphabet Q2 Earnings'},

{'ticker': 'AMZN', 'date': '2023-08-03', 'name': 'Amazon Q2 Earnings'},

{'ticker': 'META', 'date': '2023-07-26', 'name': 'Meta Q2 Earnings'},

]

ESTIMATION_WINDOW = 120

GAP = 10

EVENT_WINDOW_PRE = 10

EVENT_WINDOW_POST = 10

print(f"Analyzing {len(EVENTS)} earnings announcements")

for e in EVENTS:

print(f" {e['ticker']}: {e['name']} ({e['date']})")Analyzing 5 earnings announcements

AAPL: Apple Q3 Earnings (2023-08-03)

MSFT: Microsoft Q4 Earnings (2023-07-25)

GOOGL: Alphabet Q2 Earnings (2023-07-25)

AMZN: Amazon Q2 Earnings (2023-08-03)

META: Meta Q2 Earnings (2023-07-26)

Source

def download_event_data(ticker: str, event_date: str, est_window: int,

gap: int, pre: int, post: int) -> Tuple[pd.DataFrame, pd.Timestamp]:

"""

Download and prepare data for a single event.

Returns:

--------

DataFrame with returns and event time, actual event date

"""

event_dt = pd.to_datetime(event_date)

start_date = event_dt - timedelta(days=int((est_window + gap + pre) * 1.5))

end_date = event_dt + timedelta(days=int(post * 2.5))

stock = yf.download(ticker, start=start_date, end=end_date, progress=False)['Close']

market = yf.download('^GSPC', start=start_date, end=end_date, progress=False)['Close']

df = pd.DataFrame({

'stock_price': stock.squeeze(),

'market_price': market.squeeze()

})

df['stock_ret'] = df['stock_price'].pct_change()

df['market_ret'] = df['market_price'].pct_change()

df = df.dropna()

# Adjust event date if not a trading day

if event_dt not in df.index:

idx = df.index.get_indexer([event_dt], method='nearest')[0]

event_dt = df.index[idx]

event_idx = df.index.get_loc(event_dt)

df['event_time'] = range(-event_idx, len(df) - event_idx)

return df, event_dt

def estimate_market_model(est_data: pd.DataFrame) -> Dict:

"""

Estimate market model parameters.

"""

y = est_data['stock_ret'].values

x = est_data['market_ret'].values

X = sm.add_constant(x)

results = sm.OLS(y, X).fit()

return {

'alpha': results.params[0],

'beta': results.params[1],

'sigma': np.std(results.resid, ddof=2),

'r_squared': results.rsquared,

'n_obs': len(y),

'market_mean': np.mean(x),

'market_var': np.sum((x - np.mean(x))**2)

}

def process_single_event(event: Dict, est_window: int, gap: int,

pre: int, post: int) -> Dict:

"""

Process a single event: download data, estimate model, calculate ARs.

"""

data, actual_date = download_event_data(

event['ticker'], event['date'], est_window, gap, pre, post

)

# Split windows

est_end = -(gap + pre)

est_start = est_end - est_window

est_data = data[(data['event_time'] >= est_start) & (data['event_time'] < est_end)]

evt_data = data[(data['event_time'] >= -pre) & (data['event_time'] <= post)].copy()

# Estimate model

model = estimate_market_model(est_data)

# Calculate expected and abnormal returns

evt_data['expected_ret'] = model['alpha'] + model['beta'] * evt_data['market_ret']

evt_data['AR'] = evt_data['stock_ret'] - evt_data['expected_ret']

return {

'ticker': event['ticker'],

'name': event['name'],

'event_date': actual_date,

'model': model,

'event_data': evt_data,

'estimation_data': est_data

}

# Process all events

print("Processing events...")

event_results = []

for event in EVENTS:

try:

result = process_single_event(event, ESTIMATION_WINDOW, GAP,

EVENT_WINDOW_PRE, EVENT_WINDOW_POST)

event_results.append(result)

print(f" {event['ticker']}: OK (beta={result['model']['beta']:.3f})")

except Exception as e:

print(f" {event['ticker']}: FAILED - {e}")

print(f"\nSuccessfully processed {len(event_results)} events")Processing events...

YF.download() has changed argument auto_adjust default to True

AAPL: OK (beta=1.127)

MSFT: OK (beta=1.249)

GOOGL: OK (beta=1.404)

AMZN: OK (beta=1.521)

META: OK (beta=1.891)

Successfully processed 5 events

3. Daily Abnormal Returns (AR)¶

Definition¶

The daily abnormal return is simply the difference between actual and expected return:

Properties¶

Under the null hypothesis of no event effect:

The variance includes:

Residual variance from the market model

Estimation error in alpha

Estimation error in beta (larger when market return is extreme)

Source

def calculate_ar_variance(model: Dict, market_returns: np.ndarray) -> np.ndarray:

"""

Calculate the variance of abnormal returns accounting for estimation error.

Var(AR) = sigma^2 * [1 + 1/T + (Rm - Rm_bar)^2 / sum((Rm - Rm_bar)^2)]

"""

sigma_sq = model['sigma'] ** 2

T = model['n_obs']

Rm_bar = model['market_mean']

sum_sq = model['market_var']

variance = sigma_sq * (

1 +

1/T +

(market_returns - Rm_bar)**2 / sum_sq

)

return variance

# Display AR for first event

example = event_results[0]

evt_data = example['event_data'].copy()

# Add variance and standard error

evt_data['AR_var'] = calculate_ar_variance(example['model'], evt_data['market_ret'].values)

evt_data['AR_se'] = np.sqrt(evt_data['AR_var'])

print(f"Daily Abnormal Returns: {example['ticker']} ({example['name']})")

print("="*80)

display_df = evt_data[['event_time', 'stock_ret', 'market_ret', 'expected_ret', 'AR', 'AR_se']].copy()

display_df.index = evt_data.index.strftime('%Y-%m-%d')

for col in ['stock_ret', 'market_ret', 'expected_ret', 'AR', 'AR_se']:

display_df[col] = display_df[col].apply(lambda x: f"{x*100:.2f}%")

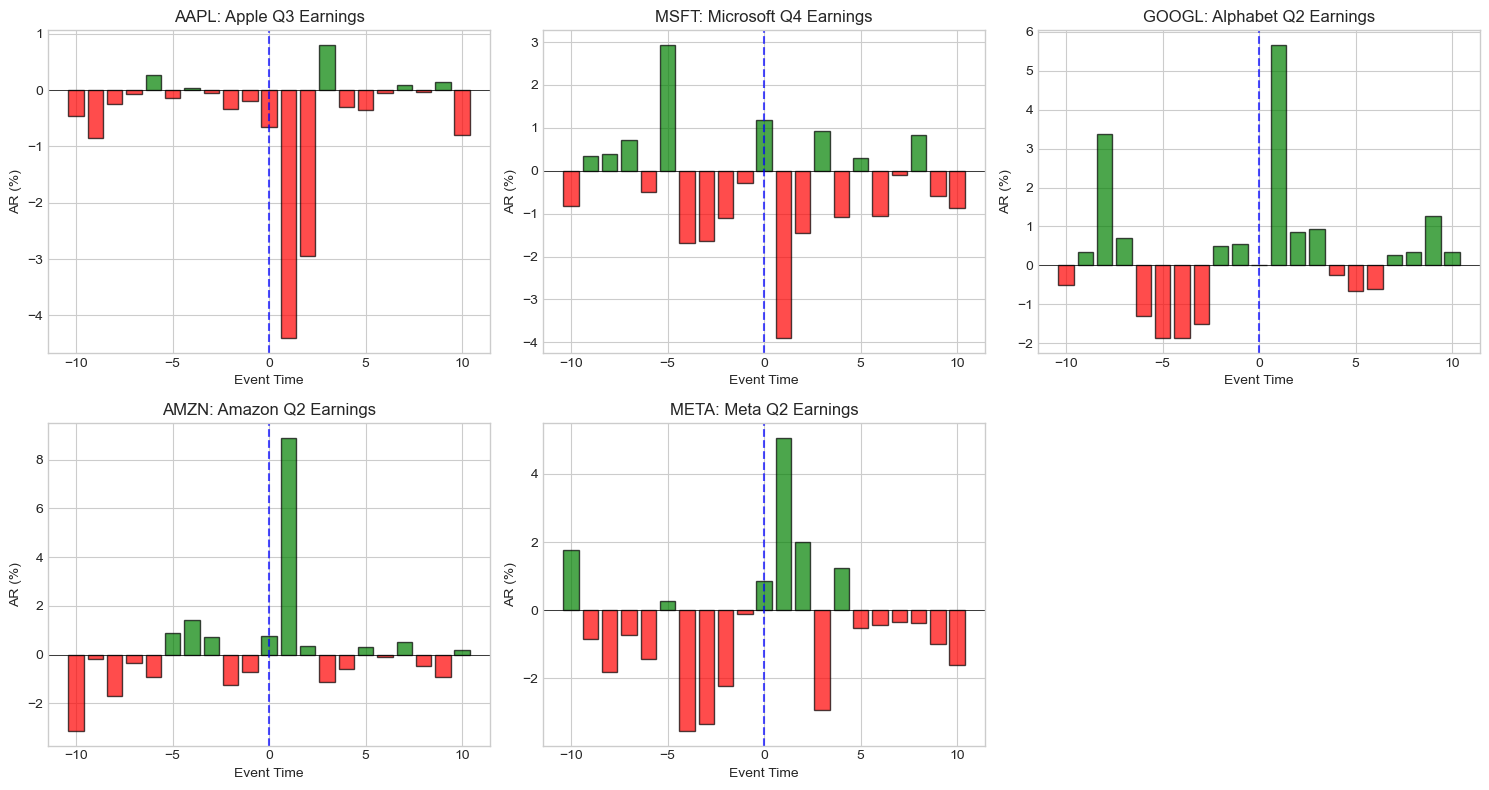

print(display_df.to_string())Daily Abnormal Returns: AAPL (Apple Q3 Earnings)

================================================================================

event_time stock_ret market_ret expected_ret AR AR_se

Date

2023-07-20 -10 -1.01% -0.68% -0.56% -0.45% 0.81%

2023-07-21 -9 -0.62% 0.03% 0.24% -0.86% 0.81%

2023-07-24 -8 0.42% 0.40% 0.66% -0.24% 0.81%

2023-07-25 -7 0.45% 0.28% 0.52% -0.07% 0.81%

2023-07-26 -6 0.45% -0.02% 0.19% 0.27% 0.81%

2023-07-27 -5 -0.66% -0.64% -0.52% -0.14% 0.81%

2023-07-28 -4 1.35% 0.99% 1.32% 0.03% 0.81%

2023-07-31 -3 0.32% 0.15% 0.37% -0.05% 0.81%

2023-08-01 -2 -0.43% -0.27% -0.09% -0.33% 0.81%

2023-08-02 -1 -1.55% -1.38% -1.35% -0.20% 0.82%

2023-08-03 0 -0.73% -0.25% -0.08% -0.65% 0.81%

2023-08-04 1 -4.80% -0.53% -0.39% -4.41% 0.81%

2023-08-07 2 -1.73% 0.90% 1.22% -2.95% 0.81%

2023-08-08 3 0.53% -0.42% -0.27% 0.80% 0.81%

2023-08-09 4 -0.90% -0.70% -0.59% -0.31% 0.81%

2023-08-10 5 -0.12% 0.03% 0.23% -0.36% 0.81%

2023-08-11 6 0.03% -0.11% 0.08% -0.05% 0.81%

2023-08-14 7 0.94% 0.58% 0.85% 0.09% 0.81%

2023-08-15 8 -1.12% -1.16% -1.10% -0.02% 0.81%

2023-08-16 9 -0.50% -0.76% -0.65% 0.15% 0.81%

2023-08-17 10 -1.46% -0.77% -0.66% -0.79% 0.81%

Source

# Visualize daily ARs for all events

fig, axes = plt.subplots(2, 3, figsize=(15, 8))

axes = axes.flatten()

for i, result in enumerate(event_results):

if i >= 5:

break

ax = axes[i]

evt = result['event_data']

colors = ['green' if ar >= 0 else 'red' for ar in evt['AR']]

ax.bar(evt['event_time'], evt['AR']*100, color=colors, alpha=0.7, edgecolor='black')

ax.axhline(0, color='black', linewidth=0.5)

ax.axvline(0, color='blue', linestyle='--', alpha=0.7, label='Event Day')

ax.set_xlabel('Event Time')

ax.set_ylabel('AR (%)')

ax.set_title(f"{result['ticker']}: {result['name']}")

ax.set_xticks(range(-EVENT_WINDOW_PRE, EVENT_WINDOW_POST+1, 5))

# Hide empty subplot

axes[5].axis('off')

plt.tight_layout()

plt.show()

4. Cumulative Abnormal Returns (CAR)¶

Definition¶

The CAR sums daily abnormal returns over an event window:

Common Windows¶

| Window | Interpretation |

|---|---|

| CAR(0, 0) | Event day only |

| CAR(-1, +1) | Three-day window (captures leakage and delayed reaction) |

| CAR(-5, +5) | Eleven-day window |

| CAR(0, +T) | Post-event drift |

| CAR(-T, -1) | Pre-event anticipation |

Variance of CAR¶

Assuming independence across days:

For the simplified case (ignoring estimation error):

Source

def calculate_car(event_data: pd.DataFrame, tau1: int, tau2: int) -> float:

"""

Calculate Cumulative Abnormal Return for a window.

Parameters:

-----------

event_data : DataFrame with 'event_time' and 'AR' columns

tau1, tau2 : Start and end of window (inclusive)

Returns:

--------

CAR value

"""

mask = (event_data['event_time'] >= tau1) & (event_data['event_time'] <= tau2)

return event_data.loc[mask, 'AR'].sum()

def calculate_car_variance(model: Dict, event_data: pd.DataFrame,

tau1: int, tau2: int) -> float:

"""

Calculate variance of CAR accounting for estimation error.

"""

mask = (event_data['event_time'] >= tau1) & (event_data['event_time'] <= tau2)

window_data = event_data[mask]

ar_variances = calculate_ar_variance(model, window_data['market_ret'].values)

return np.sum(ar_variances)

def calculate_all_cars(result: Dict, windows: List[Tuple[int, int]]) -> pd.DataFrame:

"""

Calculate CARs for multiple windows.

"""

cars = []

for tau1, tau2 in windows:

car = calculate_car(result['event_data'], tau1, tau2)

car_var = calculate_car_variance(result['model'], result['event_data'], tau1, tau2)

car_se = np.sqrt(car_var)

t_stat = car / car_se if car_se > 0 else 0

cars.append({

'Window': f'[{tau1:+d}, {tau2:+d}]',

'CAR': car,

'SE': car_se,

't-stat': t_stat,

'p-value': 2 * (1 - stats.t.cdf(abs(t_stat), df=result['model']['n_obs']-2))

})

return pd.DataFrame(cars)

# Calculate CARs for standard windows

standard_windows = [

(-10, -2), # Pre-event

(-1, +1), # Standard 3-day

(0, 0), # Event day

(-5, +5), # 11-day window

(+2, +10), # Post-event drift

(-10, +10), # Full window

]

print("CARs by Event and Window:")

print("="*90)

for result in event_results:

print(f"\n{result['ticker']}: {result['name']}")

cars_df = calculate_all_cars(result, standard_windows)

# Format for display

display_df = cars_df.copy()

display_df['CAR'] = display_df['CAR'].apply(lambda x: f"{x*100:+.2f}%")

display_df['SE'] = display_df['SE'].apply(lambda x: f"{x*100:.2f}%")

display_df['t-stat'] = display_df['t-stat'].apply(lambda x: f"{x:.3f}")

display_df['p-value'] = display_df['p-value'].apply(lambda x: f"{x:.4f}")

print(display_df.to_string(index=False))CARs by Event and Window:

==========================================================================================

AAPL: Apple Q3 Earnings

Window CAR SE t-stat p-value

[-10, -2] -1.85% 2.42% -0.763 0.4470

[-1, +1] -5.26% 1.40% -3.744 0.0003

[+0, +0] -0.65% 0.81% -0.806 0.4219

[-5, +5] -8.56% 2.68% -3.192 0.0018

[+2, +10] -3.44% 2.43% -1.419 0.1586

[-10, +10] -10.55% 3.71% -2.847 0.0052

MSFT: Microsoft Q4 Earnings

Window CAR SE t-stat p-value

[-10, -2] -1.35% 4.22% -0.319 0.7503

[-1, +1] -3.00% 2.43% -1.232 0.2205

[+0, +0] +1.19% 1.40% 0.845 0.3999

[-5, +5] -5.78% 4.66% -1.241 0.2172

[+2, +10] -3.07% 4.23% -0.727 0.4688

[-10, +10] -7.41% 6.45% -1.150 0.2526

GOOGL: Alphabet Q2 Earnings

Window CAR SE t-stat p-value

[-10, -2] -2.11% 5.01% -0.421 0.6743

[-1, +1] +6.22% 2.89% 2.155 0.0332

[+0, +0] +0.02% 1.67% 0.012 0.9902

[-5, +5] +2.37% 5.53% 0.428 0.6696

[+2, +10] +2.49% 5.01% 0.497 0.6200

[-10, +10] +6.61% 7.65% 0.863 0.3896

AMZN: Amazon Q2 Earnings

Window CAR SE t-stat p-value

[-10, -2] -4.50% 5.29% -0.850 0.3972

[-1, +1] +8.96% 3.07% 2.924 0.0041

[+0, +0] +0.76% 1.76% 0.434 0.6652

[-5, +5] +9.68% 5.86% 1.652 0.1012

[+2, +10] -1.84% 5.30% -0.347 0.7292

[-10, +10] +2.63% 8.09% 0.325 0.7458

META: Meta Q2 Earnings

Window CAR SE t-stat p-value

[-10, -2] -11.84% 7.72% -1.533 0.1278

[-1, +1] +5.84% 4.46% 1.310 0.1926

[+0, +0] +0.87% 2.57% 0.340 0.7347

[-5, +5] -3.20% 8.55% -0.375 0.7087

[+2, +10] -3.94% 7.74% -0.509 0.6114

[-10, +10] -9.94% 11.81% -0.842 0.4014

Source

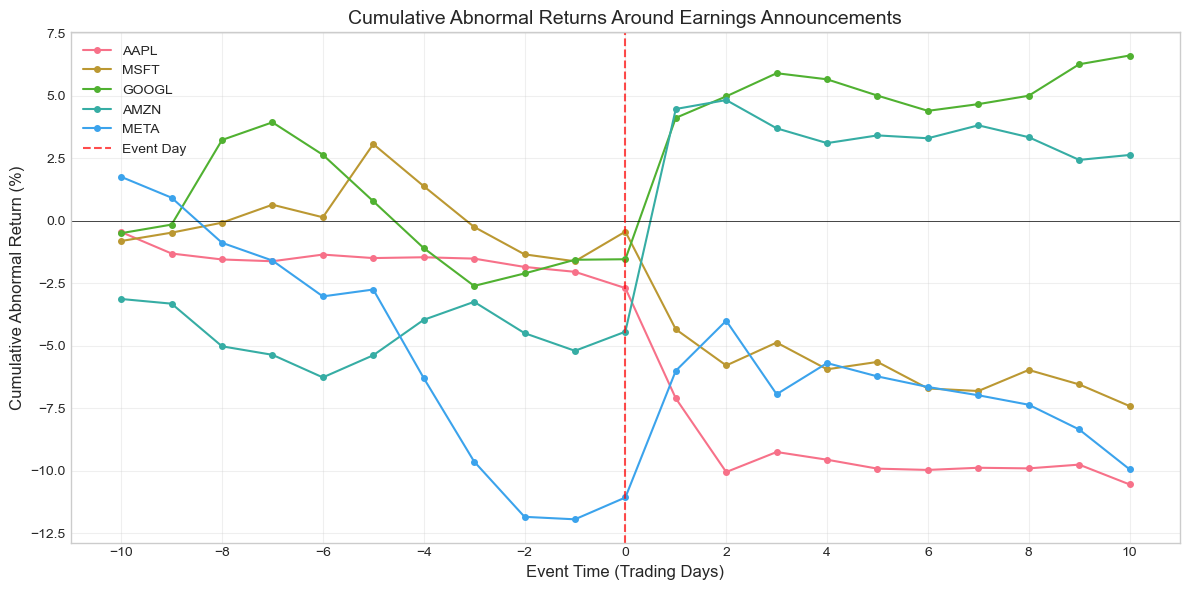

# Plot cumulative ARs over the event window

fig, ax = plt.subplots(figsize=(12, 6))

for result in event_results:

evt = result['event_data'].sort_values('event_time')

car = evt['AR'].cumsum()

ax.plot(evt['event_time'], car * 100, 'o-', label=result['ticker'],

markersize=4, linewidth=1.5)

ax.axhline(0, color='black', linewidth=0.5)

ax.axvline(0, color='red', linestyle='--', alpha=0.7, label='Event Day')

ax.set_xlabel('Event Time (Trading Days)', fontsize=12)

ax.set_ylabel('Cumulative Abnormal Return (%)', fontsize=12)

ax.set_title('Cumulative Abnormal Returns Around Earnings Announcements', fontsize=14)

ax.legend(loc='best')

ax.grid(True, alpha=0.3)

ax.set_xticks(range(-EVENT_WINDOW_PRE, EVENT_WINDOW_POST+1, 2))

plt.tight_layout()

plt.show()

5. Buy-and-Hold Abnormal Returns (BHAR)¶

Definition¶

BHAR compounds returns rather than summing them:

Or equivalently:

CAR vs. BHAR¶

| Aspect | CAR | BHAR |

|---|---|---|

| Calculation | Sum of ARs | Compound returns |

| Interpretation | Average daily abnormal return × days | Actual wealth change |

| Statistical properties | Better understood | Right-skewed distribution |

| Short horizons | Very similar | Very similar |

| Long horizons | May understate compounding | Captures true investor experience |

| Bias | Less sensitive to outliers | Sensitive to extreme returns |

Source

def calculate_bhar(event_data: pd.DataFrame, tau1: int, tau2: int) -> float:

"""

Calculate Buy-and-Hold Abnormal Return.

BHAR = Product(1 + R_actual) - Product(1 + R_expected)

"""

mask = (event_data['event_time'] >= tau1) & (event_data['event_time'] <= tau2)

window_data = event_data[mask]

# Compound actual returns

actual_wealth = np.prod(1 + window_data['stock_ret'].values)

# Compound expected returns

expected_wealth = np.prod(1 + window_data['expected_ret'].values)

return actual_wealth - expected_wealth

def calculate_bhar_market_adjusted(event_data: pd.DataFrame, tau1: int, tau2: int) -> float:

"""

Calculate market-adjusted BHAR (simple benchmark).

BHAR = Product(1 + R_stock) - Product(1 + R_market)

"""

mask = (event_data['event_time'] >= tau1) & (event_data['event_time'] <= tau2)

window_data = event_data[mask]

stock_wealth = np.prod(1 + window_data['stock_ret'].values)

market_wealth = np.prod(1 + window_data['market_ret'].values)

return stock_wealth - market_wealth

# Compare CAR and BHAR

print("CAR vs BHAR Comparison:")

print("="*90)

comparison_windows = [(-1, +1), (-5, +5), (-10, +10)]

comparison_data = []

for result in event_results:

for tau1, tau2 in comparison_windows:

car = calculate_car(result['event_data'], tau1, tau2)

bhar = calculate_bhar(result['event_data'], tau1, tau2)

bhar_ma = calculate_bhar_market_adjusted(result['event_data'], tau1, tau2)

comparison_data.append({

'Ticker': result['ticker'],

'Window': f'[{tau1:+d},{tau2:+d}]',

'CAR': car,

'BHAR': bhar,

'BHAR_MA': bhar_ma,

'Diff (BHAR-CAR)': bhar - car

})

comp_df = pd.DataFrame(comparison_data)

# Format for display

display_comp = comp_df.copy()

for col in ['CAR', 'BHAR', 'BHAR_MA', 'Diff (BHAR-CAR)']:

display_comp[col] = display_comp[col].apply(lambda x: f"{x*100:+.3f}%")

print(display_comp.to_string(index=False))CAR vs BHAR Comparison:

==========================================================================================

Ticker Window CAR BHAR BHAR_MA Diff (BHAR-CAR)

AAPL [-1,+1] -5.256% -5.143% -4.806% +0.114%

AAPL [-5,+5] -8.562% -8.315% -6.355% +0.246%

AAPL [-10,+10] -10.547% -10.083% -6.416% +0.465%

MSFT [-1,+1] -2.997% -3.074% -2.416% -0.077%

MSFT [-5,+5] -5.785% -6.031% -3.909% -0.246%

MSFT [-10,+10] -7.413% -7.835% -3.779% -0.422%

GOOGL [-1,+1] +6.223% +6.330% +7.037% +0.107%

GOOGL [-5,+5] +2.368% +2.247% +4.343% -0.121%

GOOGL [-10,+10] +6.607% +6.841% +10.801% +0.234%

AMZN [-1,+1] +8.965% +8.758% +8.140% -0.207%

AMZN [-5,+5] +9.680% +9.570% +10.267% -0.110%

AMZN [-10,+10] +2.629% +2.067% +3.259% -0.563%

META [-1,+1] +5.842% +5.965% +7.271% +0.124%

META [-5,+5] -3.200% -3.621% +1.637% -0.420%

META [-10,+10] -9.942% -11.126% +1.679% -1.184%

Source

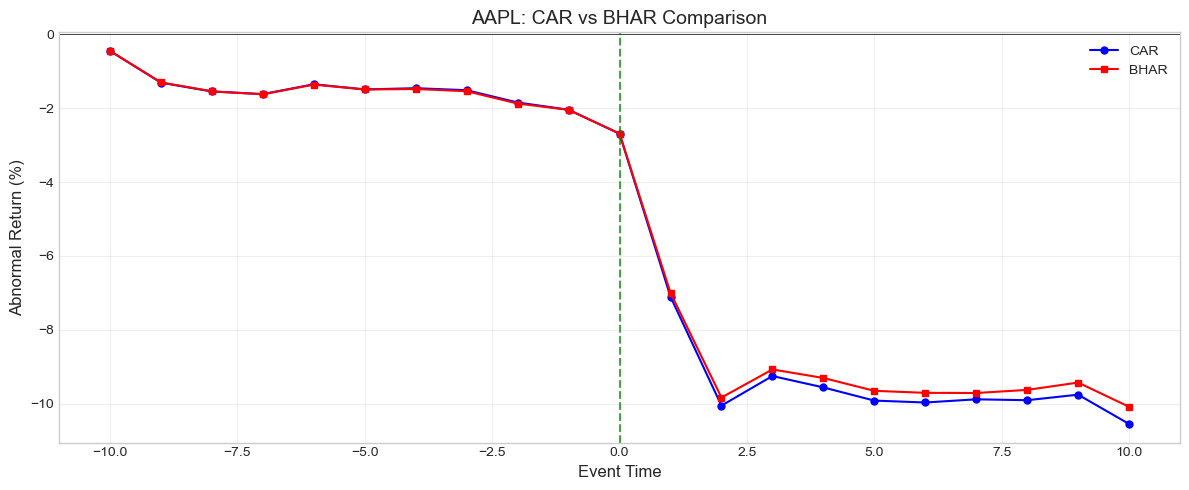

# Visualize CAR vs BHAR over time for one event

example = event_results[0]

evt = example['event_data'].sort_values('event_time')

# Calculate running CAR and BHAR

car_series = evt['AR'].cumsum()

bhar_series = []

start_time = evt['event_time'].min()

for t in evt['event_time']:

bhar = calculate_bhar(evt, start_time, t)

bhar_series.append(bhar)

fig, ax = plt.subplots(figsize=(12, 5))

ax.plot(evt['event_time'], car_series * 100, 'b-o', label='CAR', markersize=5)

ax.plot(evt['event_time'], np.array(bhar_series) * 100, 'r-s', label='BHAR', markersize=5)

ax.axhline(0, color='black', linewidth=0.5)

ax.axvline(0, color='green', linestyle='--', alpha=0.7)

ax.set_xlabel('Event Time', fontsize=12)

ax.set_ylabel('Abnormal Return (%)', fontsize=12)

ax.set_title(f'{example["ticker"]}: CAR vs BHAR Comparison', fontsize=14)

ax.legend()

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print(f"\nFor short windows, CAR and BHAR are nearly identical.")

print(f"Difference at day +{EVENT_WINDOW_POST}: {(bhar_series[-1] - car_series.iloc[-1])*100:.4f}%")

For short windows, CAR and BHAR are nearly identical.

Difference at day +10: 0.4646%

6. Standardized Abnormal Returns (SAR)¶

Motivation¶

Raw abnormal returns have different variances across firms. Standardization improves cross-sectional comparability and statistical power.

Definition¶

Where:

Standardized CAR (SCAR)¶

Where:

Under the null: approximately for large T.

Source

def calculate_standardized_ar(event_data: pd.DataFrame, model: Dict) -> pd.Series:

"""

Calculate Standardized Abnormal Returns (SAR).

SAR = AR / sigma_AR

"""

ar_var = calculate_ar_variance(model, event_data['market_ret'].values)

ar_se = np.sqrt(ar_var)

sar = event_data['AR'].values / ar_se

return pd.Series(sar, index=event_data.index)

def calculate_standardized_car(event_data: pd.DataFrame, model: Dict,

tau1: int, tau2: int) -> Tuple[float, float]:

"""

Calculate Standardized CAR (SCAR).

Returns: (SCAR, CAR)

"""

car = calculate_car(event_data, tau1, tau2)

car_var = calculate_car_variance(model, event_data, tau1, tau2)

car_se = np.sqrt(car_var)

scar = car / car_se if car_se > 0 else 0

return scar, car

# Calculate SARs for all events

print("Standardized Abnormal Returns (SAR):")

print("="*90)

for result in event_results:

evt = result['event_data'].copy()

evt['SAR'] = calculate_standardized_ar(evt, result['model'])

# Display around event day

display_data = evt[(evt['event_time'] >= -3) & (evt['event_time'] <= 3)]

print(f"\n{result['ticker']}:")

disp = display_data[['event_time', 'AR', 'SAR']].copy()

disp['AR'] = disp['AR'].apply(lambda x: f"{x*100:+.2f}%")

disp['SAR'] = disp['SAR'].apply(lambda x: f"{x:+.3f}")

print(disp.to_string(index=False))Standardized Abnormal Returns (SAR):

==========================================================================================

AAPL:

event_time AR SAR

-3 -0.05% -0.067

-2 -0.33% -0.412

-1 -0.20% -0.239

0 -0.65% -0.806

1 -4.41% -5.456

2 -2.95% -3.642

3 +0.80% +0.992

MSFT:

event_time AR SAR

-3 -1.63% -1.158

-2 -1.10% -0.781

-1 -0.28% -0.197

0 +1.19% +0.845

1 -3.91% -2.782

2 -1.45% -1.028

3 +0.92% +0.650

GOOGL:

event_time AR SAR

-3 -1.51% -0.906

-2 +0.50% +0.299

-1 +0.55% +0.328

0 +0.02% +0.012

1 +5.65% +3.393

2 +0.86% +0.514

3 +0.93% +0.554

AMZN:

event_time AR SAR

-3 +0.72% +0.409

-2 -1.25% -0.710

-1 -0.71% -0.397

0 +0.76% +0.434

1 +8.91% +5.045

2 +0.36% +0.202

3 -1.13% -0.641

META:

event_time AR SAR

-3 -3.34% -1.299

-2 -2.21% -0.860

-1 -0.10% -0.039

0 +0.87% +0.340

1 +5.07% +1.966

2 +2.00% +0.775

3 -2.94% -1.143

Source

# Compare SCARs across events

print("\nStandardized CAR (SCAR) Comparison:")

print("="*80)

scar_data = []

for result in event_results:

for tau1, tau2 in [(-1, +1), (0, 0), (-5, +5)]:

scar, car = calculate_standardized_car(result['event_data'], result['model'], tau1, tau2)

scar_data.append({

'Ticker': result['ticker'],

'Window': f'[{tau1:+d},{tau2:+d}]',

'CAR': car,

'SCAR': scar,

'Significant': '***' if abs(scar) > 2.576 else '**' if abs(scar) > 1.96 else '*' if abs(scar) > 1.645 else ''

})

scar_df = pd.DataFrame(scar_data)

display_scar = scar_df.copy()

display_scar['CAR'] = display_scar['CAR'].apply(lambda x: f"{x*100:+.2f}%")

display_scar['SCAR'] = display_scar['SCAR'].apply(lambda x: f"{x:+.3f}")

print(display_scar.to_string(index=False))

print("\nSignificance: * p<0.10, ** p<0.05, *** p<0.01")

Standardized CAR (SCAR) Comparison:

================================================================================

Ticker Window CAR SCAR Significant

AAPL [-1,+1] -5.26% -3.744 ***

AAPL [+0,+0] -0.65% -0.806

AAPL [-5,+5] -8.56% -3.192 ***

MSFT [-1,+1] -3.00% -1.232

MSFT [+0,+0] +1.19% +0.845

MSFT [-5,+5] -5.78% -1.241

GOOGL [-1,+1] +6.22% +2.155 **

GOOGL [+0,+0] +0.02% +0.012

GOOGL [-5,+5] +2.37% +0.428

AMZN [-1,+1] +8.96% +2.924 ***

AMZN [+0,+0] +0.76% +0.434

AMZN [-5,+5] +9.68% +1.652 *

META [-1,+1] +5.84% +1.310

META [+0,+0] +0.87% +0.340

META [-5,+5] -3.20% -0.375

Significance: * p<0.10, ** p<0.05, *** p<0.01

7. Aggregating Across Events¶

Average Abnormal Return (AAR)¶

For a sample of events:

Cumulative Average Abnormal Return (CAAR)¶

Variance of CAAR¶

Assuming independence across firms (no event clustering):

Source

def calculate_aar_series(event_results: List[Dict]) -> pd.DataFrame:

"""

Calculate Average Abnormal Return for each event time.

"""

# Collect all ARs by event time

ar_by_time = {}

for result in event_results:

evt = result['event_data']

for _, row in evt.iterrows():

t = int(row['event_time'])

if t not in ar_by_time:

ar_by_time[t] = []

ar_by_time[t].append(row['AR'])

# Calculate statistics

aar_data = []

for t in sorted(ar_by_time.keys()):

ars = np.array(ar_by_time[t])

n = len(ars)

aar = np.mean(ars)

std = np.std(ars, ddof=1) if n > 1 else 0

se = std / np.sqrt(n) if n > 0 else 0

t_stat = aar / se if se > 0 else 0

aar_data.append({

'event_time': t,

'N': n,

'AAR': aar,

'Std': std,

'SE': se,

't-stat': t_stat

})

return pd.DataFrame(aar_data)

def calculate_caar(event_results: List[Dict], tau1: int, tau2: int) -> Dict:

"""

Calculate Cumulative Average Abnormal Return and test statistics.

"""

cars = []

car_vars = []

for result in event_results:

car = calculate_car(result['event_data'], tau1, tau2)

car_var = calculate_car_variance(result['model'], result['event_data'], tau1, tau2)

cars.append(car)

car_vars.append(car_var)

cars = np.array(cars)

car_vars = np.array(car_vars)

N = len(cars)

caar = np.mean(cars)

# Cross-sectional standard error

cs_se = np.std(cars, ddof=1) / np.sqrt(N)

# Time-series standard error (assuming independence)

ts_var = np.sum(car_vars) / (N**2)

ts_se = np.sqrt(ts_var)

return {

'CAAR': caar,

'N': N,

'CS_SE': cs_se,

'TS_SE': ts_se,

't_stat_CS': caar / cs_se if cs_se > 0 else 0,

't_stat_TS': caar / ts_se if ts_se > 0 else 0,

'individual_CARs': cars

}

# Calculate AAR series

aar_df = calculate_aar_series(event_results)

print("Average Abnormal Returns (AAR) by Event Time:")

print("="*70)

display_aar = aar_df.copy()

display_aar['AAR'] = display_aar['AAR'].apply(lambda x: f"{x*100:+.3f}%")

display_aar['SE'] = display_aar['SE'].apply(lambda x: f"{x*100:.3f}%")

display_aar['t-stat'] = display_aar['t-stat'].apply(lambda x: f"{x:+.3f}")

print(display_aar.to_string(index=False))Average Abnormal Returns (AAR) by Event Time:

======================================================================

event_time N AAR Std SE t-stat

-10 5 -0.628% 0.017335 0.775% -0.810

-9 5 -0.240% 0.005934 0.265% -0.906

-8 5 +0.007% 0.021109 0.944% +0.008

-7 5 +0.061% 0.006370 0.285% +0.213

-6 5 -0.774% 0.006864 0.307% -2.523

-5 5 +0.419% 0.017342 0.776% +0.540

-4 5 -1.129% 0.019040 0.852% -1.326

-3 5 -1.164% 0.015696 0.702% -1.658

-2 5 -0.879% 0.010196 0.456% -1.927

-1 5 -0.146% 0.004520 0.202% -0.723

0 5 +0.439% 0.007444 0.333% +1.319

1 5 +2.262% 0.060438 2.703% +0.837

2 5 -0.235% 0.019606 0.877% -0.268

3 5 -0.285% 0.017214 0.770% -0.370

4 5 -0.194% 0.008681 0.388% -0.499

5 5 -0.188% 0.004589 0.205% -0.914

6 5 -0.452% 0.004102 0.183% -2.464

7 5 +0.088% 0.003273 0.146% +0.601

8 5 +0.060% 0.005417 0.242% +0.248

9 5 -0.214% 0.009375 0.419% -0.509

10 5 -0.541% 0.008085 0.362% -1.496

Source

# Calculate CAAR for standard windows

print("\nCumulative Average Abnormal Returns (CAAR):")

print("="*80)

caar_results = []

for tau1, tau2 in standard_windows:

result = calculate_caar(event_results, tau1, tau2)

caar_results.append({

'Window': f'[{tau1:+d}, {tau2:+d}]',

'N': result['N'],

'CAAR': result['CAAR'],

'CS_SE': result['CS_SE'],

't-stat (CS)': result['t_stat_CS'],

't-stat (TS)': result['t_stat_TS']

})

caar_df = pd.DataFrame(caar_results)

display_caar = caar_df.copy()

display_caar['CAAR'] = display_caar['CAAR'].apply(lambda x: f"{x*100:+.3f}%")

display_caar['CS_SE'] = display_caar['CS_SE'].apply(lambda x: f"{x*100:.3f}%")

display_caar['t-stat (CS)'] = display_caar['t-stat (CS)'].apply(lambda x: f"{x:+.3f}")

display_caar['t-stat (TS)'] = display_caar['t-stat (TS)'].apply(lambda x: f"{x:+.3f}")

print(display_caar.to_string(index=False))

print("\nCS = Cross-sectional, TS = Time-series standard errors")

Cumulative Average Abnormal Returns (CAAR):

================================================================================

Window N CAAR CS_SE t-stat (CS) t-stat (TS)

[-10, -2] 5 -4.328% 1.955% -2.214 -1.853

[-1, +1] 5 +2.555% 2.803% +0.912 +1.894

[+0, +0] 5 +0.439% 0.333% +1.319 +0.564

[-5, +5] 5 -1.100% 3.242% -0.339 -0.426

[+2, +10] 5 -1.960% 1.166% -1.681 -0.838

[-10, +10] 5 -3.733% 3.507% -1.065 -1.046

CS = Cross-sectional, TS = Time-series standard errors

Source

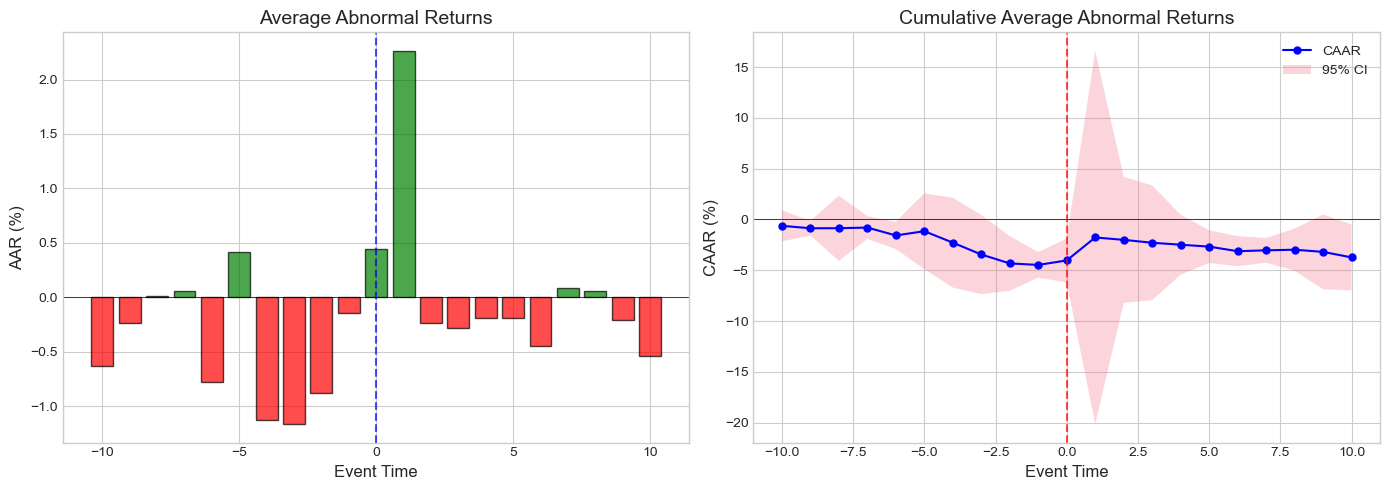

# Plot CAAR with confidence bands

aar_df['CAAR'] = aar_df['AAR'].cumsum()

# Calculate running standard error for CAAR

# Simplified: assume constant variance

aar_df['CAAR_SE'] = aar_df['SE'] * np.sqrt(np.arange(1, len(aar_df) + 1))

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

# AAR plot

ax1 = axes[0]

colors = ['green' if aar >= 0 else 'red' for aar in aar_df['AAR']]

ax1.bar(aar_df['event_time'], aar_df['AAR']*100, color=colors, alpha=0.7, edgecolor='black')

ax1.axhline(0, color='black', linewidth=0.5)

ax1.axvline(0, color='blue', linestyle='--', alpha=0.7)

ax1.set_xlabel('Event Time', fontsize=12)

ax1.set_ylabel('AAR (%)', fontsize=12)

ax1.set_title('Average Abnormal Returns', fontsize=14)

# CAAR plot with confidence bands

ax2 = axes[1]

ax2.plot(aar_df['event_time'], aar_df['CAAR']*100, 'b-o', markersize=5, label='CAAR')

ax2.fill_between(aar_df['event_time'],

(aar_df['CAAR'] - 1.96*aar_df['CAAR_SE'])*100,

(aar_df['CAAR'] + 1.96*aar_df['CAAR_SE'])*100,

alpha=0.3, label='95% CI')

ax2.axhline(0, color='black', linewidth=0.5)

ax2.axvline(0, color='red', linestyle='--', alpha=0.7)

ax2.set_xlabel('Event Time', fontsize=12)

ax2.set_ylabel('CAAR (%)', fontsize=12)

ax2.set_title('Cumulative Average Abnormal Returns', fontsize=14)

ax2.legend()

plt.tight_layout()

plt.show()

8. Wealth Effects and Economic Significance¶

Dollar Wealth Change¶

The CAR can be translated into dollar terms:

Where is the market value of equity before the event.

Aggregate Wealth Effect¶

Value-Weighted CAAR¶

Source

def get_market_cap(ticker: str, date: str) -> float:

"""

Get approximate market cap for a stock.

Uses price × shares outstanding.

"""

try:

stock = yf.Ticker(ticker)

info = stock.info

market_cap = info.get('marketCap', None)

if market_cap:

return market_cap

except:

pass

# Fallback: use approximate values (in billions)

approx_caps = {

'AAPL': 2800e9,

'MSFT': 2500e9,

'GOOGL': 1700e9,

'AMZN': 1400e9,

'META': 800e9

}

return approx_caps.get(ticker, 100e9)

def calculate_wealth_effects(event_results: List[Dict], tau1: int, tau2: int) -> pd.DataFrame:

"""

Calculate dollar wealth changes from event.

"""

wealth_data = []

for result in event_results:

car = calculate_car(result['event_data'], tau1, tau2)

mkt_cap = get_market_cap(result['ticker'], str(result['event_date']))

wealth_change = car * mkt_cap

wealth_data.append({

'Ticker': result['ticker'],

'Market Cap ($B)': mkt_cap / 1e9,

f'CAR[{tau1:+d},{tau2:+d}]': car,

'Wealth Change ($B)': wealth_change / 1e9

})

df = pd.DataFrame(wealth_data)

# Add totals

total_mkt_cap = df['Market Cap ($B)'].sum()

total_wealth_change = df['Wealth Change ($B)'].sum()

vw_car = total_wealth_change / total_mkt_cap

return df, total_wealth_change, vw_car

# Calculate wealth effects for 3-day window

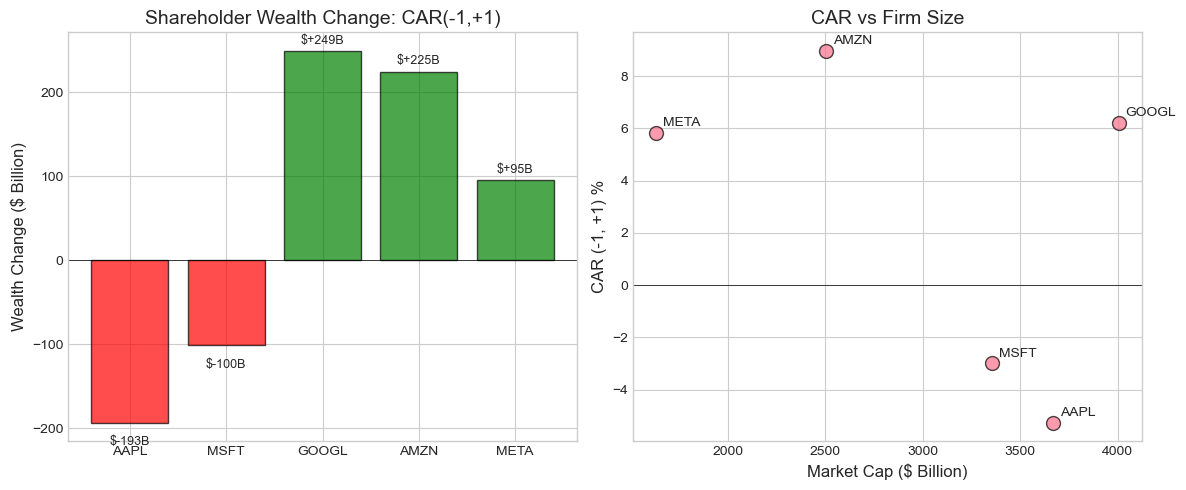

wealth_df, total_change, vw_car = calculate_wealth_effects(event_results, -1, +1)

print("Wealth Effects Analysis: CAR(-1, +1)")

print("="*70)

display_wealth = wealth_df.copy()

display_wealth['Market Cap ($B)'] = display_wealth['Market Cap ($B)'].apply(lambda x: f"${x:,.0f}")

display_wealth['CAR[-1,+1]'] = display_wealth['CAR[-1,+1]'].apply(lambda x: f"{x*100:+.2f}%")

display_wealth['Wealth Change ($B)'] = display_wealth['Wealth Change ($B)'].apply(lambda x: f"${x:+,.1f}")

print(display_wealth.to_string(index=False))

print(f"\nAggregate Statistics:")

print(f" Total Wealth Change: ${total_change:+,.1f} billion")

print(f" Value-Weighted CAAR: {vw_car*100:+.3f}%")

print(f" Equal-Weighted CAAR: {np.mean(wealth_df['CAR[-1,+1]'])*100:+.3f}%")Wealth Effects Analysis: CAR(-1, +1)

======================================================================

Ticker Market Cap ($B) CAR[-1,+1] Wealth Change ($B)

AAPL $3,670 -5.26% $-192.9

MSFT $3,353 -3.00% $-100.5

GOOGL $4,004 +6.22% $+249.1

AMZN $2,505 +8.96% $+224.6

META $1,632 +5.84% $+95.4

Aggregate Statistics:

Total Wealth Change: $+275.7 billion

Value-Weighted CAAR: +1.818%

Equal-Weighted CAAR: +2.555%

Source

# Visualize wealth effects

fig, axes = plt.subplots(1, 2, figsize=(12, 5))

# Bar chart of wealth changes

ax1 = axes[0]

colors = ['green' if x >= 0 else 'red' for x in wealth_df['Wealth Change ($B)']]

bars = ax1.bar(wealth_df['Ticker'], wealth_df['Wealth Change ($B)'], color=colors, alpha=0.7, edgecolor='black')

ax1.axhline(0, color='black', linewidth=0.5)

ax1.set_ylabel('Wealth Change ($ Billion)', fontsize=12)

ax1.set_title('Shareholder Wealth Change: CAR(-1,+1)', fontsize=14)

# Add value labels

for bar, val in zip(bars, wealth_df['Wealth Change ($B)']):

height = bar.get_height()

ax1.annotate(f'${val:+.0f}B',

xy=(bar.get_x() + bar.get_width()/2, height),

xytext=(0, 3 if height >= 0 else -10),

textcoords="offset points",

ha='center', va='bottom' if height >= 0 else 'top',

fontsize=9)

# Scatter: Market cap vs CAR

ax2 = axes[1]

ax2.scatter(wealth_df['Market Cap ($B)'], wealth_df['CAR[-1,+1]']*100,

s=100, alpha=0.7, edgecolors='black')

for i, row in wealth_df.iterrows():

ax2.annotate(row['Ticker'],

(row['Market Cap ($B)'], row['CAR[-1,+1]']*100),

xytext=(5, 5), textcoords='offset points', fontsize=10)

ax2.axhline(0, color='black', linewidth=0.5)

ax2.set_xlabel('Market Cap ($ Billion)', fontsize=12)

ax2.set_ylabel('CAR (-1, +1) %', fontsize=12)

ax2.set_title('CAR vs Firm Size', fontsize=14)

plt.tight_layout()

plt.show()

9. Precision-Weighted Measures¶

Motivation¶

Not all abnormal return estimates are equally precise. Firms with:

Higher residual variance → less precise AR estimates

Shorter estimation windows → more estimation error

Precision-Weighted CAR¶

Weight each firm’s CAR by the inverse of its variance:

Where

Source

def calculate_precision_weighted_caar(event_results: List[Dict],

tau1: int, tau2: int) -> Dict:

"""

Calculate precision-weighted CAAR.

"""

cars = []

weights = [] # Precision = 1/variance

for result in event_results:

car = calculate_car(result['event_data'], tau1, tau2)

car_var = calculate_car_variance(result['model'], result['event_data'], tau1, tau2)

precision = 1 / car_var if car_var > 0 else 0

cars.append(car)

weights.append(precision)

cars = np.array(cars)

weights = np.array(weights)

# Normalize weights

weights_norm = weights / np.sum(weights)

# Precision-weighted CAAR

pw_caar = np.sum(weights_norm * cars)

# Standard error

pw_var = 1 / np.sum(weights)

pw_se = np.sqrt(pw_var)

return {

'PW_CAAR': pw_caar,

'PW_SE': pw_se,

'PW_t_stat': pw_caar / pw_se if pw_se > 0 else 0,

'EW_CAAR': np.mean(cars), # Equal-weighted for comparison

'weights': weights_norm

}

# Compare equal-weighted and precision-weighted CAAR

print("Equal-Weighted vs Precision-Weighted CAAR:")

print("="*70)

for tau1, tau2 in [(-1, +1), (0, 0), (-5, +5)]:

pw_result = calculate_precision_weighted_caar(event_results, tau1, tau2)

print(f"\nWindow [{tau1:+d}, {tau2:+d}]:")

print(f" Equal-Weighted CAAR: {pw_result['EW_CAAR']*100:+.3f}%")

print(f" Precision-Weighted CAAR: {pw_result['PW_CAAR']*100:+.3f}%")

print(f" PW t-statistic: {pw_result['PW_t_stat']:+.3f}")Equal-Weighted vs Precision-Weighted CAAR:

======================================================================

Window [-1, +1]:

Equal-Weighted CAAR: +2.555%

Precision-Weighted CAAR: -1.238%

PW t-statistic: -1.208

Window [+0, +0]:

Equal-Weighted CAAR: +0.439%

Precision-Weighted CAAR: -0.004%

PW t-statistic: -0.007

Window [-5, +5]:

Equal-Weighted CAAR: -1.100%

Precision-Weighted CAAR: -4.379%

PW t-statistic: -2.235

10. Handling Event Clustering¶

The Problem¶

When events cluster in calendar time (e.g., earnings season), the independence assumption is violated. Cross-sectional correlation inflates test statistics.

Solutions¶

Portfolio approach: Form portfolios of stocks with events on the same day

Crude dependence adjustment: Reduce degrees of freedom

Calendar-time portfolio: Regress portfolio returns on factors

Clustered standard errors: Allow for within-period correlation

Source

def check_event_clustering(event_results: List[Dict]) -> pd.DataFrame:

"""

Check for event clustering in calendar time.

"""

dates = [result['event_date'] for result in event_results]

tickers = [result['ticker'] for result in event_results]

df = pd.DataFrame({'Ticker': tickers, 'Event_Date': dates})

# Count events per date

cluster_count = df.groupby('Event_Date').size().reset_index(name='N_Events')

return df.merge(cluster_count, on='Event_Date')

def crude_dependence_adjustment(event_results: List[Dict], tau1: int, tau2: int) -> Dict:

"""

Crude dependence adjustment for clustered events.

Reduces effective N based on clustering.

"""

cluster_df = check_event_clustering(event_results)

# Effective N = number of unique event dates

n_effective = cluster_df['Event_Date'].nunique()

n_actual = len(event_results)

# Calculate CAAR

caar_result = calculate_caar(event_results, tau1, tau2)

# Adjust standard error

adjustment_factor = np.sqrt(n_actual / n_effective)

adjusted_se = caar_result['CS_SE'] * adjustment_factor

adjusted_t = caar_result['CAAR'] / adjusted_se if adjusted_se > 0 else 0

return {

'N_actual': n_actual,

'N_effective': n_effective,

'CAAR': caar_result['CAAR'],

'SE_unadjusted': caar_result['CS_SE'],

'SE_adjusted': adjusted_se,

't_unadjusted': caar_result['t_stat_CS'],

't_adjusted': adjusted_t

}

# Check clustering

cluster_df = check_event_clustering(event_results)

print("Event Clustering Analysis:")

print("="*50)

print(cluster_df.to_string(index=False))

print(f"\nUnique event dates: {cluster_df['Event_Date'].nunique()}")

print(f"Total events: {len(event_results)}")

# Apply crude dependence adjustment

print("\nCrude Dependence Adjustment (CAR[-1,+1]):")

adj = crude_dependence_adjustment(event_results, -1, +1)

print(f" Unadjusted t-stat: {adj['t_unadjusted']:+.3f}")

print(f" Adjusted t-stat: {adj['t_adjusted']:+.3f}")Event Clustering Analysis:

==================================================

Ticker Event_Date N_Events

AAPL 2023-08-03 2

MSFT 2023-07-25 2

GOOGL 2023-07-25 2

AMZN 2023-08-03 2

META 2023-07-26 1

Unique event dates: 3

Total events: 5

Crude Dependence Adjustment (CAR[-1,+1]):

Unadjusted t-stat: +0.912

Adjusted t-stat: +0.706

11. Summary Statistics Table¶

A complete event study report should include summary statistics.

Source

def create_summary_table(event_results: List[Dict], windows: List[Tuple[int, int]]) -> pd.DataFrame:

"""

Create a comprehensive summary table for event study results.

"""

summary = []

for tau1, tau2 in windows:

cars = []

for result in event_results:

car = calculate_car(result['event_data'], tau1, tau2)

cars.append(car)

cars = np.array(cars)

n = len(cars)

# Calculate statistics

mean_car = np.mean(cars)

median_car = np.median(cars)

std_car = np.std(cars, ddof=1)

se = std_car / np.sqrt(n)

t_stat = mean_car / se if se > 0 else 0

# Count positive

n_positive = np.sum(cars > 0)

pct_positive = n_positive / n * 100

# Sign test

sign_stat = (n_positive - n/2) / np.sqrt(n/4)

summary.append({

'Window': f'[{tau1:+d},{tau2:+d}]',

'N': n,

'Mean CAR': mean_car,

'Median CAR': median_car,

'Std Dev': std_car,

't-stat': t_stat,

'% Positive': pct_positive,

'Sign Stat': sign_stat

})

return pd.DataFrame(summary)

# Create summary table

summary_table = create_summary_table(event_results, standard_windows)

print("\n" + "="*90)

print("EVENT STUDY SUMMARY STATISTICS")

print("="*90)

print(f"Sample: {len(event_results)} Big Tech Earnings Announcements (Q2-Q3 2023)")

print(f"Estimation Window: {ESTIMATION_WINDOW} days")

print(f"Model: Market Model (S&P 500 benchmark)")

print("="*90)

display_summary = summary_table.copy()

display_summary['Mean CAR'] = display_summary['Mean CAR'].apply(lambda x: f"{x*100:+.3f}%")

display_summary['Median CAR'] = display_summary['Median CAR'].apply(lambda x: f"{x*100:+.3f}%")

display_summary['Std Dev'] = display_summary['Std Dev'].apply(lambda x: f"{x*100:.3f}%")

display_summary['t-stat'] = display_summary['t-stat'].apply(lambda x: f"{x:+.3f}")

display_summary['% Positive'] = display_summary['% Positive'].apply(lambda x: f"{x:.0f}%")

display_summary['Sign Stat'] = display_summary['Sign Stat'].apply(lambda x: f"{x:+.3f}")

print(display_summary.to_string(index=False))

print("\nSignificance: |t| > 1.645 (10%), |t| > 1.96 (5%), |t| > 2.576 (1%)")

==========================================================================================

EVENT STUDY SUMMARY STATISTICS

==========================================================================================

Sample: 5 Big Tech Earnings Announcements (Q2-Q3 2023)

Estimation Window: 120 days

Model: Market Model (S&P 500 benchmark)

==========================================================================================

Window N Mean CAR Median CAR Std Dev t-stat % Positive Sign Stat

[-10,-2] 5 -4.328% -2.109% 4.372% -2.214 0% -2.236

[-1,+1] 5 +2.555% +5.842% 6.269% +0.912 60% +0.447

[+0,+0] 5 +0.439% +0.765% 0.744% +1.319 80% +1.342

[-5,+5] 5 -1.100% -3.200% 7.250% -0.339 40% -0.447

[+2,+10] 5 -1.960% -3.070% 2.608% -1.681 20% -1.342

[-10,+10] 5 -3.733% -7.413% 7.841% -1.065 40% -0.447

Significance: |t| > 1.645 (10%), |t| > 1.96 (5%), |t| > 2.576 (1%)

12. Exercises¶

Exercise 1: Alternative Benchmarks¶

Recalculate abnormal returns using:

Market-adjusted returns (beta = 1)

Industry-adjusted returns (use sector ETF)

Exercise 2: Long-Horizon BHAR¶

Extend the event window to [-20, +20] days. Calculate both CAR and BHAR. How much do they diverge?

Exercise 3: Subsample Analysis¶

Split the sample by some characteristic (e.g., positive vs negative earnings surprise if you can identify it). Do the subsamples show different patterns?

Exercise 4: Bootstrap Confidence Intervals¶

Implement bootstrap confidence intervals for CAAR instead of assuming normality.

Source

# Exercise 4 Template: Bootstrap CAAR

def bootstrap_caar(event_results: List[Dict], tau1: int, tau2: int,

n_bootstrap: int = 1000) -> Dict:

"""

Bootstrap confidence intervals for CAAR.

"""

# Calculate individual CARs

cars = np.array([calculate_car(r['event_data'], tau1, tau2) for r in event_results])

n = len(cars)

# Original CAAR

original_caar = np.mean(cars)

# Bootstrap

bootstrap_caars = []

for _ in range(n_bootstrap):

# Resample with replacement

sample_idx = np.random.choice(n, size=n, replace=True)

sample_cars = cars[sample_idx]

bootstrap_caars.append(np.mean(sample_cars))

bootstrap_caars = np.array(bootstrap_caars)

# Confidence intervals

ci_90 = np.percentile(bootstrap_caars, [5, 95])

ci_95 = np.percentile(bootstrap_caars, [2.5, 97.5])

ci_99 = np.percentile(bootstrap_caars, [0.5, 99.5])

return {

'CAAR': original_caar,

'Bootstrap_SE': np.std(bootstrap_caars),

'CI_90': ci_90,

'CI_95': ci_95,

'CI_99': ci_99

}

# Run bootstrap

print("Bootstrap Confidence Intervals for CAAR(-1, +1):")

print("="*50)

boot_result = bootstrap_caar(event_results, -1, +1, n_bootstrap=5000)

print(f"CAAR: {boot_result['CAAR']*100:+.3f}%")

print(f"Bootstrap SE: {boot_result['Bootstrap_SE']*100:.3f}%")

print(f"90% CI: [{boot_result['CI_90'][0]*100:+.3f}%, {boot_result['CI_90'][1]*100:+.3f}%]")

print(f"95% CI: [{boot_result['CI_95'][0]*100:+.3f}%, {boot_result['CI_95'][1]*100:+.3f}%]")

print(f"99% CI: [{boot_result['CI_99'][0]*100:+.3f}%, {boot_result['CI_99'][1]*100:+.3f}%]")Bootstrap Confidence Intervals for CAAR(-1, +1):

==================================================

CAAR: +2.555%

Bootstrap SE: 2.522%

90% CI: [-1.960%, +6.695%]

95% CI: [-2.508%, +7.244%]

99% CI: [-3.901%, +7.868%]

13. Summary¶

In this session, we covered:

Daily Abnormal Returns (AR): The building block of event studies

Cumulative Abnormal Returns (CAR): Summing ARs over event windows

Buy-and-Hold Abnormal Returns (BHAR): Compounding for true wealth effects

Standardized Abnormal Returns (SAR/SCAR): Improving cross-sectional comparability

Aggregation Methods:

Average Abnormal Return (AAR)

Cumulative Average Abnormal Return (CAAR)

Precision-weighted aggregation

Economic Interpretation:

Dollar wealth changes

Value-weighted vs. equal-weighted measures

Event Clustering: The problem and solutions

Key Takeaways¶

CAR and BHAR are nearly identical for short windows

Standardization improves statistical power

Always report multiple windows for robustness

Consider economic significance, not just statistical significance

Watch out for event clustering

Coming Up Next¶

Session 4: Statistical Inference I - Parametric Tests will cover:

The Patell test

Boehmer-Musumeci-Poulsen (BMP) test

Cross-sectional vs. time-series variance

Event-induced variance

14. References¶

Methodology¶

Fama, E. F. (1998). Market efficiency, long-term returns, and behavioral finance. Journal of Financial Economics, 49(3), 283-306.

Barber, B. M., & Lyon, J. D. (1997). Detecting long-run abnormal stock returns: The empirical power and specification of test statistics. Journal of Financial Economics, 43(3), 341-372.

Lyon, J. D., Barber, B. M., & Tsai, C. L. (1999). Improved methods for tests of long-run abnormal stock returns. Journal of Finance, 54(1), 165-201.

Applications¶

MacKinlay, A. C. (1997). Event studies in economics and finance. Journal of Economic Literature, 35(1), 13-39.

Kothari, S. P., & Warner, J. B. (2007). Econometrics of event studies. Handbook of Corporate Finance, 1, 3-36.