Session 4: Advanced Univariate Volatility Models

Course: Advanced Volatility Modeling¶

Learning Objectives¶

By the end of this session, students will be able to:

Understand long memory in volatility and the FIGARCH model

Work with power transformations using APARCH

Decompose volatility into permanent and transitory components

Apply model selection criteria across complex specifications

1. Long Memory in Volatility¶

1.1 Motivation¶

Recall from Session 1: the autocorrelation of squared/absolute returns decays slowly - much slower than exponential decay would predict. Standard GARCH models imply exponential ACF decay:

But empirically, we observe hyperbolic decay:

This is long memory (or long-range dependence) with parameter .

1.2 Fractional Integration¶

A time series is integrated of order , denoted , if:

where is stationary and is the lag operator.

The fractional difference operator is defined via binomial expansion:

For : stationary with long memory For : standard stationary process For : unit root (random walk)

Source

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from scipy.special import gamma as gamma_func

from scipy.optimize import minimize

import yfinance as yf

from arch import arch_model

import warnings

warnings.filterwarnings('ignore')

plt.style.use('seaborn-v0_8-whitegrid')

plt.rcParams['figure.figsize'] = (12, 6)

plt.rcParams['font.size'] = 11

np.random.seed(42)Source

# Download data

spy = yf.download('SPY', start='2000-01-01', end='2024-12-31', progress=False)

if isinstance(spy.columns, pd.MultiIndex):

spy.columns = spy.columns.get_level_values(0)

returns = (np.log(spy['Close'] / spy['Close'].shift(1)) * 100).dropna()

abs_returns = np.abs(returns)

print(f"Sample: {returns.index[0].date()} to {returns.index[-1].date()}")

print(f"Observations: {len(returns)}")YF.download() has changed argument auto_adjust default to True

Sample: 2000-01-04 to 2024-12-30

Observations: 6287

Source

def estimate_d_gph(series, m=None):

"""

Estimate fractional differencing parameter d using GPH estimator.

The GPH (Geweke-Porter-Hudak) estimator uses the periodogram.

Parameters

----------

series : array-like

Time series

m : int

Number of low-frequency ordinates to use (default: T^0.5)

Returns

-------

d_hat : float

Estimated d

se : float

Standard error

"""

T = len(series)

if m is None:

m = int(T ** 0.5)

# Compute periodogram

fft_vals = np.fft.fft(series - series.mean())

periodogram = np.abs(fft_vals) ** 2 / T

# Frequencies

freqs = 2 * np.pi * np.arange(1, m + 1) / T

# Log-periodogram regression

y = np.log(periodogram[1:m+1])

x = np.log(4 * np.sin(freqs / 2) ** 2)

# OLS

x_dm = x - x.mean()

d_hat = -np.sum(x_dm * y) / np.sum(x_dm ** 2) / 2

# Standard error

se = np.pi / (np.sqrt(24) * np.sqrt(np.sum(x_dm ** 2)))

return d_hat, se

# Estimate d for absolute returns

d_hat, se = estimate_d_gph(abs_returns.values)

print("GPH Estimation of Long Memory Parameter")

print("="*50)

print(f"d̂ = {d_hat:.4f}")

print(f"Standard Error = {se:.4f}")

print(f"95% CI: [{d_hat - 1.96*se:.4f}, {d_hat + 1.96*se:.4f}]")

print(f"\nInterpretation:")

if 0 < d_hat < 0.5:

print(f"d ∈ (0, 0.5): Stationary long memory")

print(f"ACF decays like k^{2*d_hat - 1:.2f} (hyperbolic)")GPH Estimation of Long Memory Parameter

==================================================

d̂ = 0.2140

Standard Error = 0.0396

95% CI: [0.1364, 0.2917]

Interpretation:

d ∈ (0, 0.5): Stationary long memory

ACF decays like k^-0.57 (hyperbolic)

Source

# Compare empirical ACF decay to theoretical

def compute_acf(series, max_lag):

"""Compute sample ACF."""

n = len(series)

mean = series.mean()

var = series.var()

acf = np.zeros(max_lag + 1)

acf[0] = 1.0

for k in range(1, max_lag + 1):

acf[k] = np.mean((series.iloc[k:] - mean).values * (series.iloc[:-k] - mean).values) / var

return acf

max_lag = 500

acf_empirical = compute_acf(abs_returns, max_lag)

# Theoretical ACF under GARCH (exponential decay)

garch_fit = arch_model(returns, vol='Garch', p=1, q=1).fit(disp='off')

persistence = garch_fit.params['alpha[1]'] + garch_fit.params['beta[1]']

acf_garch = persistence ** np.arange(max_lag + 1) * acf_empirical[1]

# Theoretical ACF under long memory (hyperbolic decay)

lags = np.arange(1, max_lag + 1)

acf_long_memory = acf_empirical[1] * lags ** (2 * d_hat - 1)

acf_long_memory = np.concatenate([[1], acf_long_memory])

# Plot

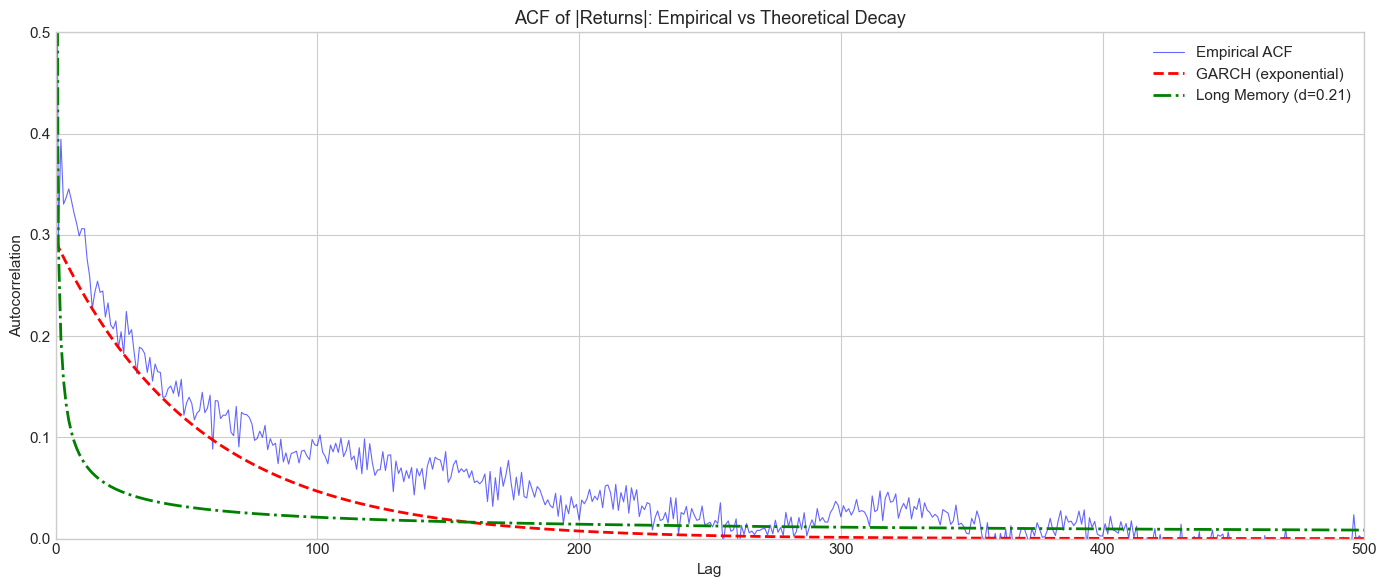

fig, ax = plt.subplots(figsize=(14, 6))

ax.plot(acf_empirical, 'b-', alpha=0.6, linewidth=0.8, label='Empirical ACF')

ax.plot(acf_garch, 'r--', linewidth=2, label='GARCH (exponential)')

ax.plot(acf_long_memory, 'g-.', linewidth=2, label=f'Long Memory (d={d_hat:.2f})')

ax.set_xlabel('Lag')

ax.set_ylabel('Autocorrelation')

ax.set_title('ACF of |Returns|: Empirical vs Theoretical Decay', fontsize=13)

ax.legend(loc='upper right')

ax.set_xlim(0, max_lag)

ax.set_ylim(0, 0.5)

plt.tight_layout()

plt.show()

print("\nThe empirical ACF decays much slower than GARCH predicts,")

print("consistent with long memory in volatility.")

The empirical ACF decays much slower than GARCH predicts,

consistent with long memory in volatility.

2. FIGARCH Model¶

2.1 Model Specification¶

Baillie, Bollerslev & Mikkelsen (1996) introduced Fractionally Integrated GARCH:

where .

For FIGARCH(1,d,1):

2.2 Special Cases¶

: Standard GARCH (short memory)

: IGARCH (unit root)

: Long memory

2.3 Properties¶

ACF of decays hyperbolically:

Impulse response also decays hyperbolically

Forecasts revert to long-run mean but slowly

Source

# Fit FIGARCH using arch library

model_figarch = arch_model(returns, vol='FIGARCH', p=1, q=1, power=2.0)

fit_figarch = model_figarch.fit(disp='off')

print("FIGARCH(1,d,1) Estimation Results")

print("="*60)

print(fit_figarch.summary())

d_figarch = fit_figarch.params['d']

print(f"\nEstimated d = {d_figarch:.4f}")

print(f"This is {'similar to' if abs(d_figarch - d_hat) < 0.1 else 'different from'} the GPH estimate ({d_hat:.4f})")FIGARCH(1,d,1) Estimation Results

============================================================

Constant Mean - FIGARCH Model Results

==============================================================================

Dep. Variable: Close R-squared: 0.000

Mean Model: Constant Mean Adj. R-squared: 0.000

Vol Model: FIGARCH Log-Likelihood: -8627.81

Distribution: Normal AIC: 17265.6

Method: Maximum Likelihood BIC: 17299.3

No. Observations: 6287

Date: Thu, Feb 05 2026 Df Residuals: 6286

Time: 09:36:22 Df Model: 1

Mean Model

============================================================================

coef std err t P>|t| 95.0% Conf. Int.

----------------------------------------------------------------------------

mu 0.0731 1.005e-02 7.278 3.396e-13 [5.344e-02,9.282e-02]

Volatility Model

============================================================================

coef std err t P>|t| 95.0% Conf. Int.

----------------------------------------------------------------------------

omega 0.0430 1.358e-02 3.169 1.531e-03 [1.642e-02,6.966e-02]

phi 0.0360 6.216e-02 0.579 0.563 [-8.583e-02, 0.158]

d 0.5374 8.142e-02 6.601 4.077e-11 [ 0.378, 0.697]

beta 0.4770 0.110 4.332 1.479e-05 [ 0.261, 0.693]

============================================================================

Covariance estimator: robust

Estimated d = 0.5374

This is different from the GPH estimate (0.2140)

Source

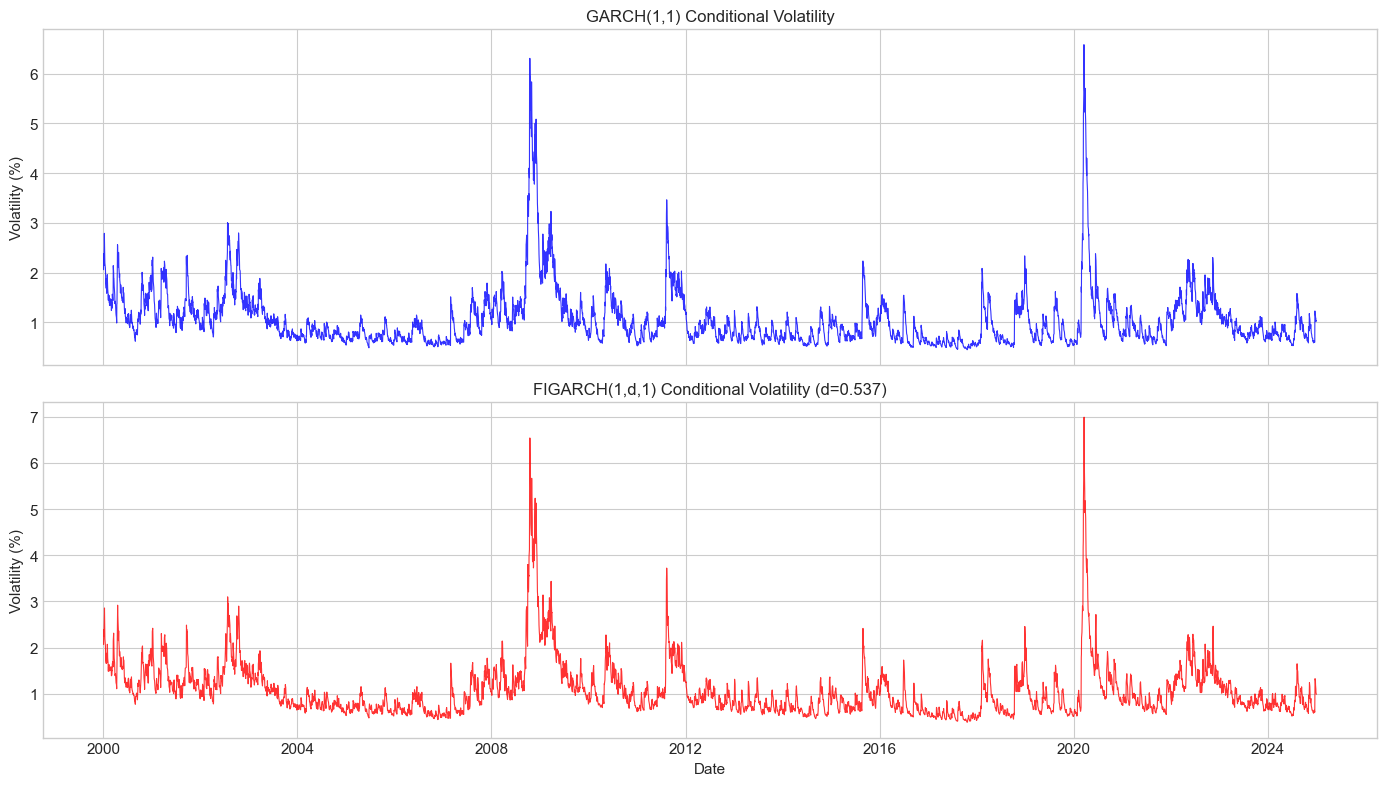

# Compare GARCH vs FIGARCH volatility

fig, axes = plt.subplots(2, 1, figsize=(14, 8), sharex=True)

vol_garch = garch_fit.conditional_volatility

vol_figarch = fit_figarch.conditional_volatility

axes[0].plot(vol_garch.index, vol_garch.values, 'b-', linewidth=0.8, alpha=0.8)

axes[0].set_title('GARCH(1,1) Conditional Volatility', fontsize=12)

axes[0].set_ylabel('Volatility (%)')

axes[1].plot(vol_figarch.index, vol_figarch.values, 'r-', linewidth=0.8, alpha=0.8)

axes[1].set_title(f'FIGARCH(1,d,1) Conditional Volatility (d={d_figarch:.3f})', fontsize=12)

axes[1].set_ylabel('Volatility (%)')

axes[1].set_xlabel('Date')

plt.tight_layout()

plt.show()

# Model comparison

print(f"\nModel Comparison:")

print(f"{'Model':<20} {'Log-Lik':>12} {'AIC':>12} {'BIC':>12}")

print("-"*60)

print(f"{'GARCH(1,1)':<20} {garch_fit.loglikelihood:>12.2f} {garch_fit.aic:>12.2f} {garch_fit.bic:>12.2f}")

print(f"{'FIGARCH(1,d,1)':<20} {fit_figarch.loglikelihood:>12.2f} {fit_figarch.aic:>12.2f} {fit_figarch.bic:>12.2f}")

Model Comparison:

Model Log-Lik AIC BIC

------------------------------------------------------------

GARCH(1,1) -8644.06 17296.12 17323.10

FIGARCH(1,d,1) -8627.81 17265.61 17299.34

3. APARCH Model¶

3.1 Model Specification¶

Ding, Granger & Engle (1993) proposed the Asymmetric Power ARCH model:

Key features:

Power parameter : transforms volatility (data-driven, not fixed at 2)

Asymmetry : leverage effect (similar to GJR-GARCH)

3.2 Special Cases¶

| Model | ||

|---|---|---|

| 2 | 0 | GARCH |

| 2 | GJR-GARCH | |

| 1 | 0 | AVGARCH (Taylor) |

| 1 | TGARCH (Zakoian) |

3.3 Optimal Power¶

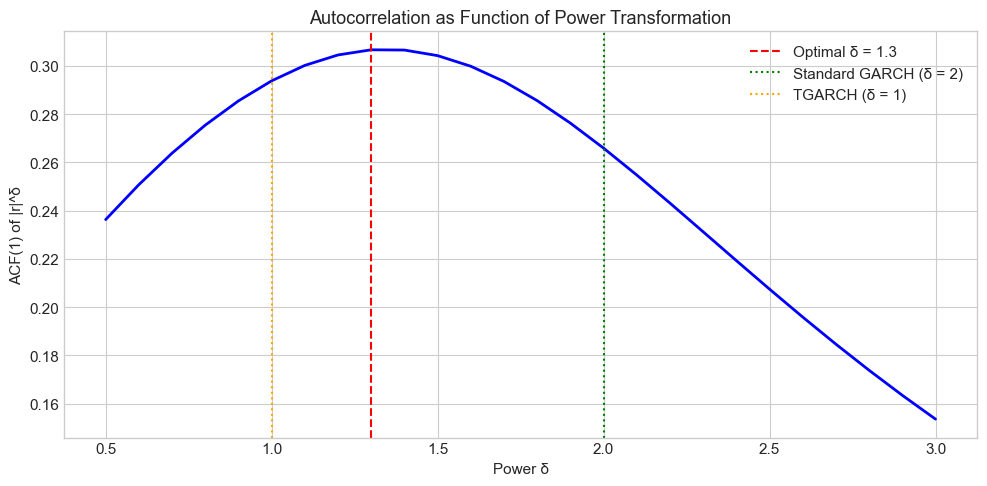

Ding et al. (1993) showed that has maximum autocorrelation around for equity returns, not !

Source

# Find optimal power transformation

def find_optimal_power(returns, powers=np.arange(0.5, 3.1, 0.1)):

"""

Find power δ that maximizes ACF(1) of |r|^δ.

"""

acf1_values = []

for delta in powers:

transformed = np.abs(returns) ** delta

acf1 = transformed.autocorr(lag=1)

acf1_values.append(acf1)

return powers, np.array(acf1_values)

powers, acf1s = find_optimal_power(returns)

optimal_power = powers[np.argmax(acf1s)]

fig, ax = plt.subplots(figsize=(10, 5))

ax.plot(powers, acf1s, 'b-', linewidth=2)

ax.axvline(optimal_power, color='red', linestyle='--', label=f'Optimal δ = {optimal_power:.1f}')

ax.axvline(2.0, color='green', linestyle=':', label='Standard GARCH (δ = 2)')

ax.axvline(1.0, color='orange', linestyle=':', label='TGARCH (δ = 1)')

ax.set_xlabel('Power δ')

ax.set_ylabel('ACF(1) of |r|^δ')

ax.set_title('Autocorrelation as Function of Power Transformation', fontsize=13)

ax.legend()

plt.tight_layout()

plt.show()

print(f"Optimal power: δ = {optimal_power:.2f}")

print(f"ACF(1) at optimal power: {acf1s[np.argmax(acf1s)]:.4f}")

powers = [round(x,2) for x in powers]

print(f"ACF(1) at δ=2 (GARCH): {acf1s[[x==2. for x in powers]][0]:.4f}")

Optimal power: δ = 1.30

ACF(1) at optimal power: 0.3066

ACF(1) at δ=2 (GARCH): 0.2659

Source

# Fit APARCH with estimated power

model_aparch = arch_model(returns, vol='APARCH', p=1, o=1, q=1, dist='t')

fit_aparch = model_aparch.fit(disp='off')

print("APARCH(1,1) Estimation Results")

print("="*60)

print(fit_aparch.summary().tables[1])

delta_hat = fit_aparch.params['delta']

gamma_hat = fit_aparch.params['gamma[1]']

print(f"\nEstimated δ = {delta_hat:.4f}")

print(f"Estimated γ = {gamma_hat:.4f}")

print(f"\nThe estimated power is {'close to' if abs(delta_hat - optimal_power) < 0.3 else 'different from'} the grid search optimal ({optimal_power:.1f})")APARCH(1,1) Estimation Results

============================================================

Mean Model

============================================================================

coef std err t P>|t| 95.0% Conf. Int.

----------------------------------------------------------------------------

mu 0.0514 8.671e-03 5.929 3.042e-09 [3.442e-02,6.841e-02]

============================================================================

Estimated δ = 0.9397

Estimated γ = 0.9997

The estimated power is different from the grid search optimal (1.3)

4. Component GARCH¶

4.1 Motivation¶

Volatility appears to have multiple components operating at different time scales:

Long-run (permanent) component: slow-moving trend

Short-run (transitory) component: mean-reverting around trend

4.2 Model Specification (Engle & Lee, 1999)¶

where:

Long-run component (slow mean reversion):

Short-run component (fast mean reversion):

Key: (long-run persistence) > (short-run persistence)

Source

def simulate_component_garch(n, omega, rho, phi, alpha, beta, seed=None):

"""

Simulate Component GARCH process.

σ²_t = q_t + s_t

q_t = ω + ρ(q_{t-1} - ω) + φ(ε²_{t-1} - σ²_{t-1}) [long-run]

s_t = α(ε²_{t-1} - q_{t-1}) + β s_{t-1} [short-run]

"""

if seed is not None:

np.random.seed(seed)

eps = np.zeros(n)

sigma2 = np.zeros(n)

q = np.zeros(n) # Long-run component

s = np.zeros(n) # Short-run component

z = np.random.standard_normal(n)

# Initialize at unconditional values

q[0] = omega

s[0] = 0

sigma2[0] = q[0] + s[0]

eps[0] = np.sqrt(sigma2[0]) * z[0]

for t in range(1, n):

# Long-run component

q[t] = omega + rho * (q[t-1] - omega) + phi * (eps[t-1]**2 - sigma2[t-1])

# Short-run component

s[t] = alpha * (eps[t-1]**2 - q[t-1]) + beta * s[t-1]

# Total variance

sigma2[t] = max(q[t] + s[t], 1e-8) # Ensure positive

eps[t] = np.sqrt(sigma2[t]) * z[t]

return eps, sigma2, q, s

# Simulate

n = 3000

omega = 1.0

rho = 0.995 # Very persistent long-run

phi = 0.03

alpha = 0.05

beta = 0.90 # Less persistent short-run

eps_comp, sigma2_comp, q_comp, s_comp = simulate_component_garch(

n, omega, rho, phi, alpha, beta, seed=42

)

# Plot

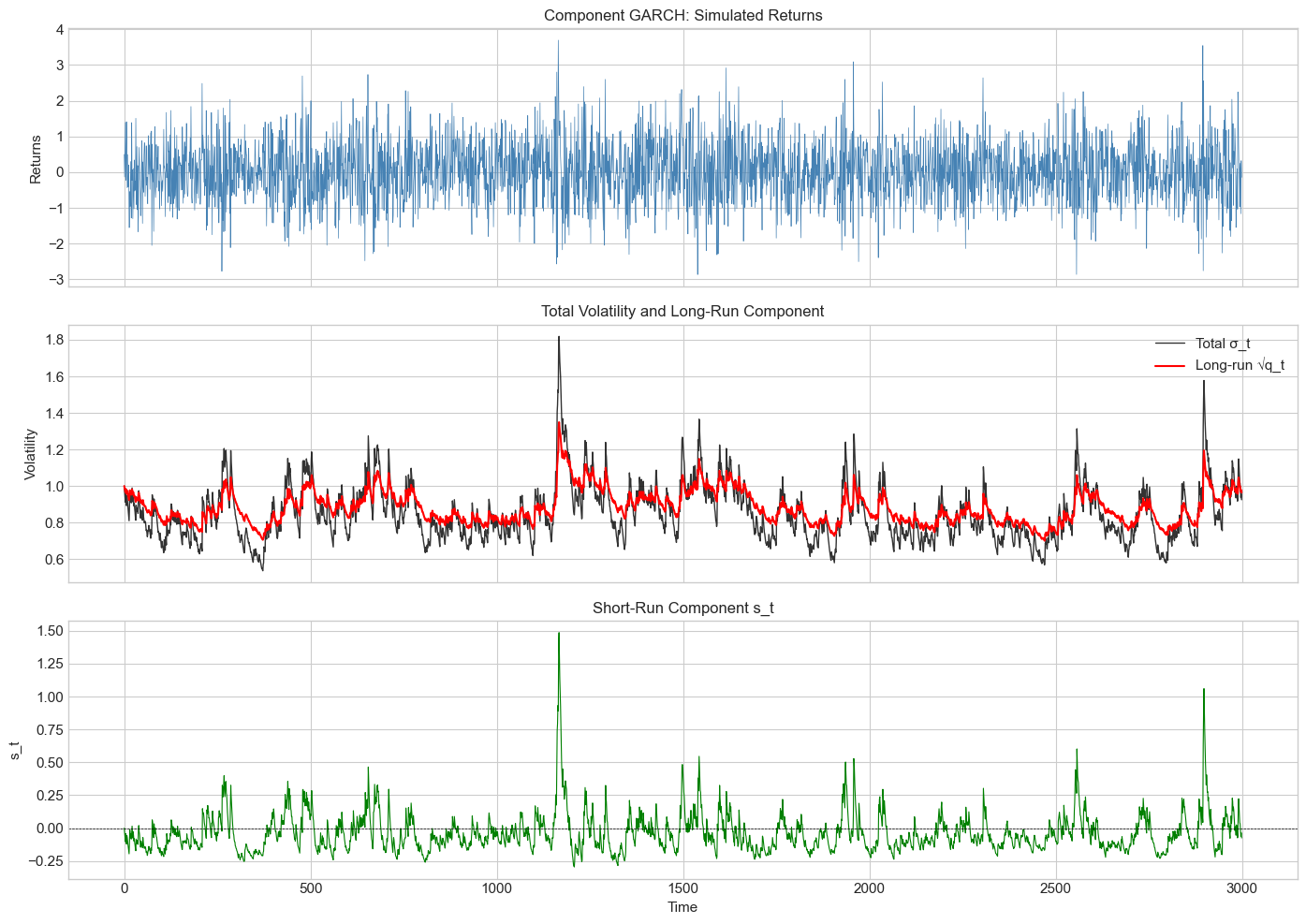

fig, axes = plt.subplots(3, 1, figsize=(14, 10), sharex=True)

axes[0].plot(eps_comp, color='steelblue', linewidth=0.5)

axes[0].set_title('Component GARCH: Simulated Returns', fontsize=12)

axes[0].set_ylabel('Returns')

axes[1].plot(np.sqrt(sigma2_comp), 'k-', linewidth=1, label='Total σ_t', alpha=0.8)

axes[1].plot(np.sqrt(q_comp), 'r-', linewidth=1.5, label='Long-run √q_t')

axes[1].set_title('Total Volatility and Long-Run Component', fontsize=12)

axes[1].set_ylabel('Volatility')

axes[1].legend()

axes[2].plot(s_comp, 'g-', linewidth=0.8)

axes[2].axhline(0, color='black', linestyle='--', linewidth=0.5)

axes[2].set_title('Short-Run Component s_t', fontsize=12)

axes[2].set_ylabel('s_t')

axes[2].set_xlabel('Time')

plt.tight_layout()

plt.show()

print(f"Long-run persistence (ρ): {rho:.3f}")

print(f"Short-run persistence (α+β): {alpha + beta:.3f}")

print(f"\nThe long-run component captures slow trends in volatility.")

Long-run persistence (ρ): 0.995

Short-run persistence (α+β): 0.950

The long-run component captures slow trends in volatility.

Source

# Fit Component GARCH to real data

# Note: arch doesn't have built-in CGARCH, so we use HARCH as approximation

# or fit manually

def fit_component_garch_simple(returns, max_iter=1000):

"""

Fit simplified Component GARCH by MLE.

"""

returns = np.asarray(returns)

T = len(returns)

def neg_loglik(params):

omega, rho, phi, alpha, beta = params

# Constraints

if omega <= 0 or not (0 < rho < 1) or alpha < 0 or beta < 0:

return 1e10

if alpha + beta >= 1:

return 1e10

sigma2 = np.zeros(T)

q = np.zeros(T)

s = np.zeros(T)

q[0] = returns.var()

s[0] = 0

sigma2[0] = q[0]

for t in range(1, T):

q[t] = omega + rho * (q[t-1] - omega) + phi * (returns[t-1]**2 - sigma2[t-1])

s[t] = alpha * (returns[t-1]**2 - q[t-1]) + beta * s[t-1]

sigma2[t] = max(q[t] + s[t], 1e-8)

# Log-likelihood

ll = -0.5 * np.sum(np.log(2*np.pi) + np.log(sigma2) + returns**2/sigma2)

return -ll

# Initial guess

var0 = returns.var()

x0 = [var0 * 0.1, 0.99, 0.01, 0.05, 0.85]

result = minimize(neg_loglik, x0, method='Nelder-Mead',

options={'maxiter': max_iter})

return result

# Fit to S&P 500

cgarch_result = fit_component_garch_simple(returns.values)

print("Component GARCH Estimation Results")

print("="*50)

params = cgarch_result.x

print(f"ω (long-run mean): {params[0]:.4f}")

print(f"ρ (long-run persistence): {params[1]:.4f}")

print(f"φ (long-run news): {params[2]:.4f}")

print(f"α (short-run news): {params[3]:.4f}")

print(f"β (short-run persistence): {params[4]:.4f}")

print(f"\nShort-run persistence (α+β): {params[3] + params[4]:.4f}")

print(f"Log-likelihood: {-cgarch_result.fun:.2f}")Component GARCH Estimation Results

==================================================

ω (long-run mean): 0.2235

ρ (long-run persistence): 1.0000

φ (long-run news): -0.0020

α (short-run news): 0.0903

β (short-run persistence): 0.8965

Short-run persistence (α+β): 0.9868

Log-likelihood: -8679.24

5. Model Comparison and Selection¶

Source

# Comprehensive model comparison

models_to_fit = [

('GARCH(1,1)', {'vol': 'Garch', 'p': 1, 'q': 1}),

('GJR-GARCH(1,1)', {'vol': 'Garch', 'p': 1, 'o': 1, 'q': 1}),

('EGARCH(1,1)', {'vol': 'EGARCH', 'p': 1, 'o': 1, 'q': 1}),

('FIGARCH(1,d,1)', {'vol': 'FIGARCH', 'p': 1, 'q': 1}),

('APARCH(1,1)', {'vol': 'APARCH', 'p': 1, 'o': 1, 'q': 1}),

]

results = []

for name, spec in models_to_fit:

try:

model = arch_model(returns, dist='t', **spec)

fit = model.fit(disp='off')

results.append({

'Model': name,

'Log-Lik': fit.loglikelihood,

'AIC': fit.aic,

'BIC': fit.bic,

'Params': fit.num_params

})

except Exception as e:

print(f"Failed to fit {name}: {e}")

results_df = pd.DataFrame(results).set_index('Model')

results_df = results_df.sort_values('BIC')

print("\nModel Comparison (S&P 500 Daily Returns)")

print("="*70)

print(results_df.round(2))

print(f"\nBest model by BIC: {results_df['BIC'].idxmin()}")

Model Comparison (S&P 500 Daily Returns)

======================================================================

Log-Lik AIC BIC Params

Model

APARCH(1,1) -8354.42 16722.84 16770.06 7

EGARCH(1,1) -8370.72 16753.44 16793.92 6

GJR-GARCH(1,1) -8394.93 16801.86 16842.34 6

FIGARCH(1,d,1) -8476.09 16964.17 17004.65 6

GARCH(1,1) -8499.09 17008.18 17041.91 5

Best model by BIC: APARCH(1,1)

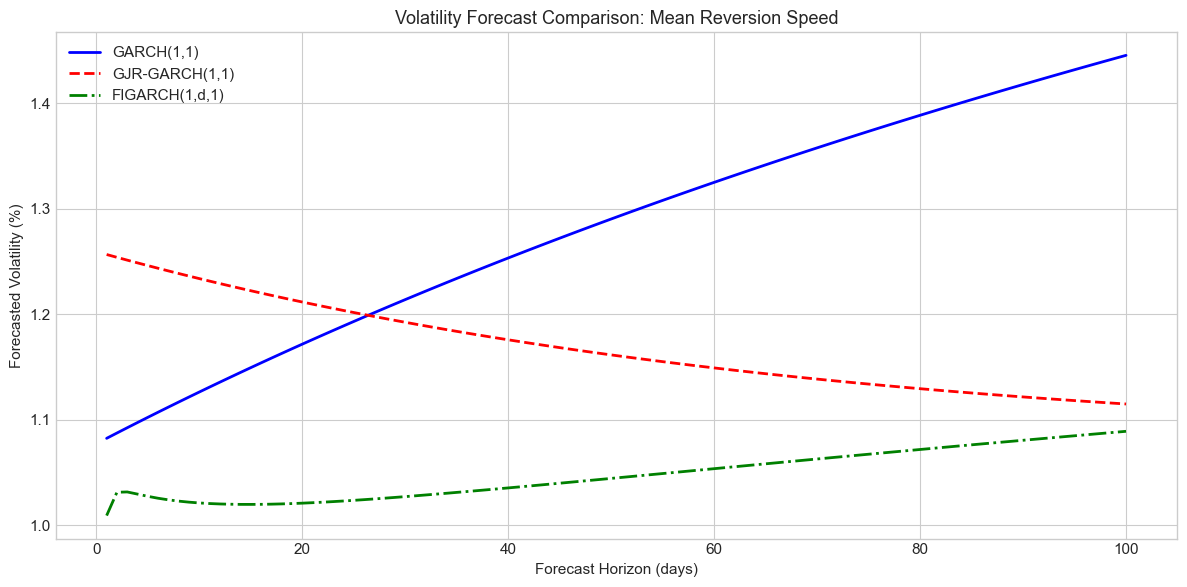

6. Forecasting Comparison¶

Source

# Compare long-horizon forecasts

horizon = 100

# Fit models

fit_garch = arch_model(returns, vol='Garch', p=1, q=1, dist='t').fit(disp='off')

fit_gjr = arch_model(returns, vol='Garch', p=1, o=1, q=1, dist='t').fit(disp='off')

fit_figarch = arch_model(returns, vol='FIGARCH', p=1, q=1, dist='t').fit(disp='off')

# Generate forecasts

fcast_garch = fit_garch.forecast(horizon=horizon, reindex=False)

fcast_gjr = fit_gjr.forecast(horizon=horizon, reindex=False)

fcast_figarch = fit_figarch.forecast(horizon=horizon, reindex=False)

# Plot

fig, ax = plt.subplots(figsize=(12, 6))

days = np.arange(1, horizon + 1)

ax.plot(days, np.sqrt(fcast_garch.variance.iloc[-1].values),

'b-', linewidth=2, label='GARCH(1,1)')

ax.plot(days, np.sqrt(fcast_gjr.variance.iloc[-1].values),

'r--', linewidth=2, label='GJR-GARCH(1,1)')

ax.plot(days, np.sqrt(fcast_figarch.variance.iloc[-1].values),

'g-.', linewidth=2, label='FIGARCH(1,d,1)')

ax.set_xlabel('Forecast Horizon (days)')

ax.set_ylabel('Forecasted Volatility (%)')

ax.set_title('Volatility Forecast Comparison: Mean Reversion Speed', fontsize=13)

ax.legend()

plt.tight_layout()

plt.show()

print("\nKey observation:")

print("FIGARCH forecasts decay more slowly to the long-run mean,")

print("reflecting the long memory property.")

Key observation:

FIGARCH forecasts decay more slowly to the long-run mean,

reflecting the long memory property.

7. Summary¶

Key Takeaways¶

Long memory: Volatility autocorrelations decay hyperbolically (), not exponentially

FIGARCH: Captures long memory via fractional differencing; typical for equities

APARCH: Data-driven power transformation; optimal for many assets (not 2!)

Component GARCH: Separates permanent and transitory volatility components

Model selection: BIC often favors parsimonious models; complex models need careful evaluation

Preview of Session 5¶

Session 5 shifts to Realized Volatility: using high-frequency data to measure volatility directly, rather than as a latent variable.

Exercises¶

Exercise 1: Long Memory Estimation¶

Estimate the fractional differencing parameter for Bitcoin, Gold, and EUR/USD using both GPH and FIGARCH. How do they compare?

Exercise 2: Optimal Power¶

Find the optimal power for maximizing ACF(1) of for cryptocurrencies. Is it different from equities?

Exercise 3: FIEGARCH¶

The arch library supports FIEGARCH (Fractionally Integrated EGARCH). Fit this model to S&P 500 and compare to FIGARCH.

Exercise 4: Component Decomposition¶

Fit Component GARCH to Bitcoin. What are the relative contributions of permanent vs transitory components during major crashes?

Exercise 5: Forecast Evaluation¶

Compare GARCH, GJR-GARCH, FIGARCH, and APARCH forecasts using rolling 1-step-ahead evaluation over 2020-2024. Which model performs best during high vs low volatility periods?

References¶

Baillie, R. T., Bollerslev, T., & Mikkelsen, H. O. (1996). Fractionally integrated generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 74(1), 3-30.

Ding, Z., Granger, C. W., & Engle, R. F. (1993). A long memory property of stock market returns and a new model. Journal of Empirical Finance, 1(1), 83-106.

Engle, R. F., & Lee, G. (1999). A long-run and short-run component model of stock return volatility. Cointegration, Causality, and Forecasting, 475-497.

Andersen, T. G., & Bollerslev, T. (1997). Heterogeneous information arrivals and return volatility dynamics. Journal of Finance, 52(3), 975-1005.