Session 3: Asymmetric GARCH Models

Course: Advanced Volatility Modeling¶

Learning Objectives¶

By the end of this session, students will be able to:

Understand the leverage effect and its economic interpretation

Derive and estimate EGARCH, GJR-GARCH, and TGARCH models

Compare news impact curves across models

Test for asymmetry in volatility response

1. The Leverage Effect¶

1.1 Empirical Evidence¶

Black (1976) documented that stock returns and volatility are negatively correlated:

Negative returns → Increased future volatility

Positive returns → Decreased (or unchanged) future volatility

This asymmetry is called the leverage effect.

1.2 Economic Explanations¶

Leverage hypothesis (Black, 1976; Christie, 1982):

When stock price falls, debt-to-equity ratio rises

Higher leverage → higher risk → higher volatility

Volatility feedback hypothesis (French et al., 1987; Campbell & Hentschel, 1992):

News of higher future volatility raises required return

Stock price must fall immediately to deliver higher expected return

1.3 News Impact Curve¶

The News Impact Curve (NIC) shows how today’s shock affects tomorrow’s variance:

For symmetric GARCH(1,1), the NIC is a parabola centered at zero.

Source

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import scipy.stats as stats

from scipy.optimize import minimize

import yfinance as yf

from arch import arch_model

import warnings

warnings.filterwarnings('ignore')

plt.style.use('seaborn-v0_8-whitegrid')

plt.rcParams['figure.figsize'] = (12, 6)

plt.rcParams['font.size'] = 11

np.random.seed(42)Source

# Download S&P 500 data

spy = yf.download('SPY', start='2010-01-01', end='2024-12-31', progress=False)

if isinstance(spy.columns, pd.MultiIndex):

spy.columns = spy.columns.get_level_values(0)

spy['returns'] = np.log(spy['Close'] / spy['Close'].shift(1))

returns = spy['returns'].dropna() * 100 # Percentage returns

print(f"Sample: {returns.index[0].date()} to {returns.index[-1].date()}")

print(f"Observations: {len(returns)}")YF.download() has changed argument auto_adjust default to True

Sample: 2010-01-05 to 2024-12-30

Observations: 3772

Source

# Empirical evidence of leverage effect

def empirical_leverage_effect(returns, lags=20):

"""

Compute cross-correlation between returns and future squared returns.

Leverage effect implies negative correlation at positive lags.

"""

ret = returns - returns.mean()

sq_ret = ret ** 2

correlations = []

for lag in range(-lags, lags + 1):

if lag < 0:

corr = ret.iloc[-lag:].corr(sq_ret.iloc[:lag])

elif lag > 0:

corr = ret.iloc[:-lag].corr(sq_ret.iloc[lag:])

else:

corr = ret.corr(sq_ret)

correlations.append(corr)

return np.arange(-lags, lags + 1), np.array(correlations)

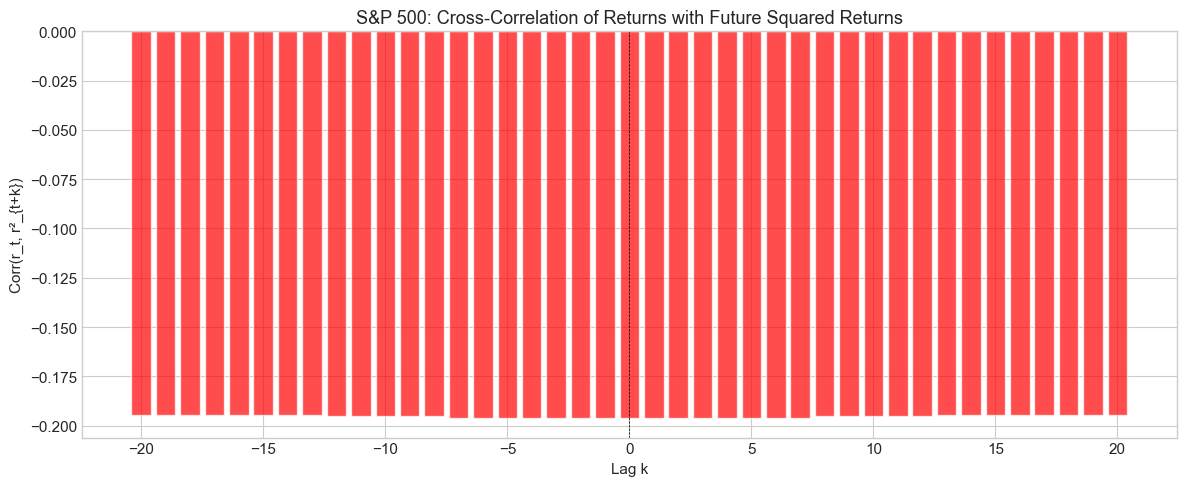

lags, corrs = empirical_leverage_effect(returns)

fig, ax = plt.subplots(figsize=(12, 5))

colors = ['green' if c > 0 else 'red' for c in corrs]

ax.bar(lags, corrs, color=colors, alpha=0.7, edgecolor='white')

ax.axhline(0, color='black', linewidth=0.5)

ax.axvline(0, color='black', linewidth=0.5, linestyle='--')

ax.set_xlabel('Lag k')

ax.set_ylabel('Corr(r_t, r²_{t+k})')

ax.set_title('S&P 500: Cross-Correlation of Returns with Future Squared Returns', fontsize=13)

plt.tight_layout()

plt.show()

print(f"\nCorr(r_t, r²_{{t+1}}): {corrs[lags==1][0]:.4f}")

print(f"Corr(r_t, r²_{{t+5}}): {corrs[lags==5][0]:.4f}")

print("\nNegative values at positive lags confirm the leverage effect.")

Corr(r_t, r²_{t+1}): -0.1962

Corr(r_t, r²_{t+5}): -0.1962

Negative values at positive lags confirm the leverage effect.

2. GJR-GARCH (Glosten-Jagannathan-Runkle)¶

2.1 Model Specification¶

GJR-GARCH(1,1) adds an asymmetric term for negative shocks:

where is an indicator for negative shocks.

Interpretation:

Positive shock (): Impact is

Negative shock (): Impact is

indicates leverage effect

2.2 Stationarity Condition¶

2.3 News Impact Curve¶

Source

def simulate_gjr_garch(n, omega, alpha, gamma, beta, dist='normal', df=5):

"""

Simulate GJR-GARCH(1,1) process.

"""

eps = np.zeros(n)

sigma2 = np.zeros(n)

if dist == 'normal':

z = np.random.standard_normal(n)

else:

z = np.random.standard_t(df, n) / np.sqrt(df / (df - 2))

uncond_var = omega / (1 - alpha - gamma/2 - beta)

sigma2[0] = uncond_var

eps[0] = np.sqrt(sigma2[0]) * z[0]

for t in range(1, n):

indicator = 1 if eps[t-1] < 0 else 0

sigma2[t] = omega + alpha * eps[t-1]**2 + gamma * eps[t-1]**2 * indicator + beta * sigma2[t-1]

eps[t] = np.sqrt(sigma2[t]) * z[t]

return eps, sigma2

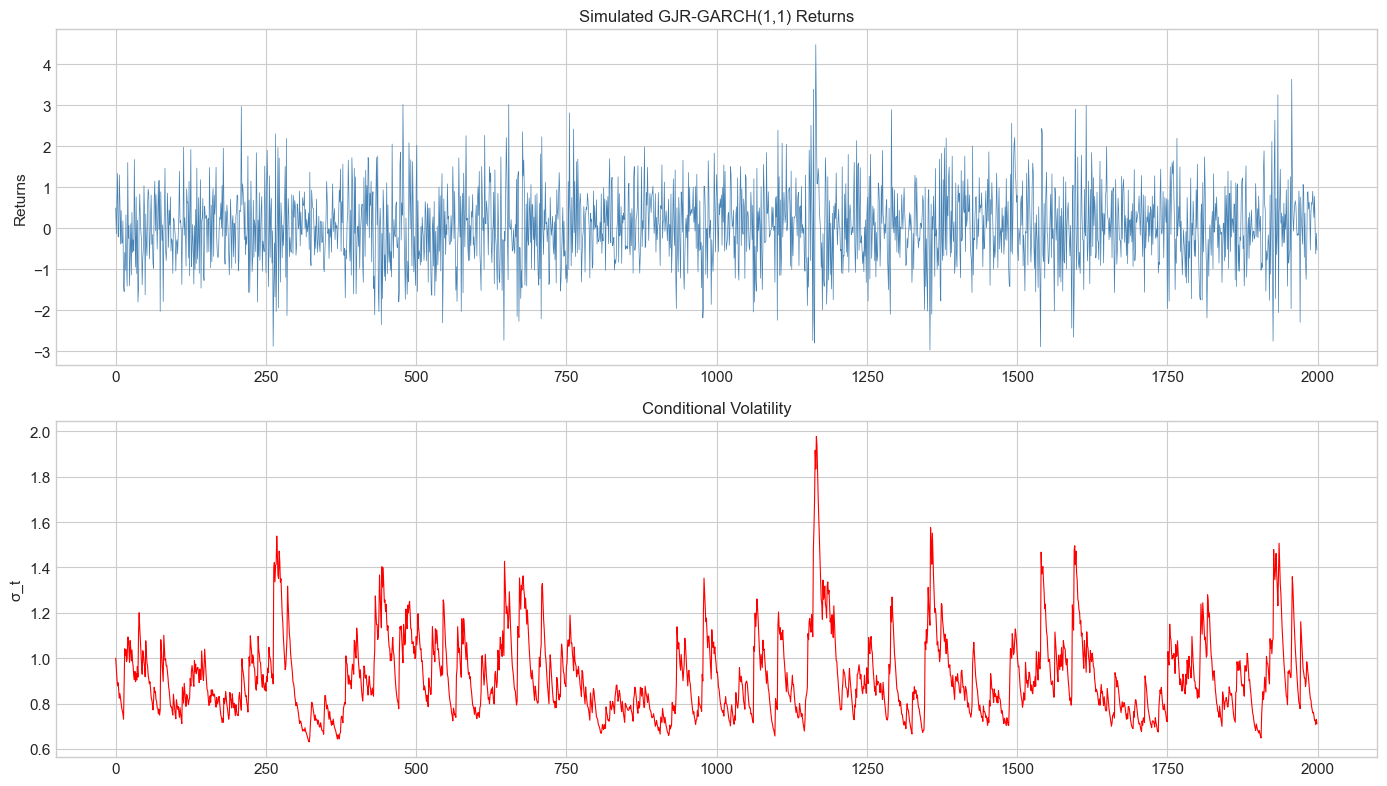

# Simulate GJR-GARCH

n = 2000

omega, alpha, gamma, beta = 0.05, 0.05, 0.10, 0.85

np.random.seed(42)

eps_gjr, sigma2_gjr = simulate_gjr_garch(n, omega, alpha, gamma, beta)

fig, axes = plt.subplots(2, 1, figsize=(14, 8))

axes[0].plot(eps_gjr, color='steelblue', linewidth=0.5)

axes[0].set_title('Simulated GJR-GARCH(1,1) Returns', fontsize=12)

axes[0].set_ylabel('Returns')

axes[1].plot(np.sqrt(sigma2_gjr), color='red', linewidth=0.8)

axes[1].set_title('Conditional Volatility', fontsize=12)

axes[1].set_ylabel('σ_t')

plt.tight_layout()

plt.show()

Source

# Fit GJR-GARCH to S&P 500

model_gjr = arch_model(returns, vol='Garch', p=1, o=1, q=1, dist='t')

fit_gjr = model_gjr.fit(disp='off')

print("GJR-GARCH(1,1) Estimation Results")

print("="*60)

print(fit_gjr.summary())

alpha_hat = fit_gjr.params['alpha[1]']

gamma_hat = fit_gjr.params['gamma[1]']

print(f"\n\nInterpretation:")

print(f"Impact of positive shock: α = {alpha_hat:.4f}")

print(f"Impact of negative shock: α + γ = {alpha_hat + gamma_hat:.4f}")

print(f"Asymmetry ratio: (α + γ)/α = {(alpha_hat + gamma_hat)/max(alpha_hat, 0.001):.2f}")GJR-GARCH(1,1) Estimation Results

============================================================

Constant Mean - GJR-GARCH Model Results

====================================================================================

Dep. Variable: returns R-squared: 0.000

Mean Model: Constant Mean Adj. R-squared: 0.000

Vol Model: GJR-GARCH Log-Likelihood: -4643.32

Distribution: Standardized Student's t AIC: 9298.65

Method: Maximum Likelihood BIC: 9336.06

No. Observations: 3772

Date: Thu, Feb 05 2026 Df Residuals: 3771

Time: 09:32:08 Df Model: 1

Mean Model

============================================================================

coef std err t P>|t| 95.0% Conf. Int.

----------------------------------------------------------------------------

mu 0.0747 1.054e-02 7.091 1.334e-12 [5.406e-02,9.536e-02]

Volatility Model

=============================================================================

coef std err t P>|t| 95.0% Conf. Int.

-----------------------------------------------------------------------------

omega 0.0288 4.634e-03 6.223 4.885e-10 [1.976e-02,3.792e-02]

alpha[1] 2.0125e-12 1.317e-02 1.529e-10 1.000 [-2.580e-02,2.580e-02]

gamma[1] 0.2917 3.587e-02 8.131 4.244e-16 [ 0.221, 0.362]

beta[1] 0.8303 1.690e-02 49.133 0.000 [ 0.797, 0.863]

Distribution

========================================================================

coef std err t P>|t| 95.0% Conf. Int.

------------------------------------------------------------------------

nu 5.8145 0.566 10.264 1.024e-24 [ 4.704, 6.925]

========================================================================

Covariance estimator: robust

Interpretation:

Impact of positive shock: α = 0.0000

Impact of negative shock: α + γ = 0.2917

Asymmetry ratio: (α + γ)/α = 291.69

3. EGARCH (Exponential GARCH)¶

3.1 Model Specification¶

Nelson (1991) proposed EGARCH, which models log-variance:

where and:

3.2 Key Properties¶

Advantages over GJR-GARCH:

No parameter restrictions for positivity (since we model log-variance)

Continuous news impact curve at zero

Log-linear structure facilitates interpretation

Asymmetry: implies leverage effect

Source

# Fit EGARCH to S&P 500

model_egarch = arch_model(returns, vol='EGARCH', p=1, o=1, q=1, dist='t')

fit_egarch = model_egarch.fit(disp='off')

print("EGARCH(1,1) Estimation Results")

print("="*60)

print(fit_egarch.summary())

print(f"\n\nNote: In EGARCH, alpha[1] < 0 indicates leverage effect.")

print(f"alpha[1] = {fit_egarch.params['alpha[1]']:.4f}")EGARCH(1,1) Estimation Results

============================================================

Constant Mean - EGARCH Model Results

====================================================================================

Dep. Variable: returns R-squared: 0.000

Mean Model: Constant Mean Adj. R-squared: 0.000

Vol Model: EGARCH Log-Likelihood: -4630.50

Distribution: Standardized Student's t AIC: 9273.01

Method: Maximum Likelihood BIC: 9310.42

No. Observations: 3772

Date: Thu, Feb 05 2026 Df Residuals: 3771

Time: 09:32:20 Df Model: 1

Mean Model

============================================================================

coef std err t P>|t| 95.0% Conf. Int.

----------------------------------------------------------------------------

mu 0.0694 1.062e-02 6.532 6.508e-11 [4.855e-02,9.018e-02]

Volatility Model

==============================================================================

coef std err t P>|t| 95.0% Conf. Int.

------------------------------------------------------------------------------

omega -9.4307e-03 5.012e-03 -1.882 5.987e-02 [-1.925e-02,3.919e-04]

alpha[1] 0.1876 2.126e-02 8.823 1.115e-18 [ 0.146, 0.229]

gamma[1] -0.1973 1.610e-02 -12.257 1.534e-34 [ -0.229, -0.166]

beta[1] 0.9642 6.178e-03 156.062 0.000 [ 0.952, 0.976]

Distribution

========================================================================

coef std err t P>|t| 95.0% Conf. Int.

------------------------------------------------------------------------

nu 6.0058 0.601 9.989 1.697e-23 [ 4.827, 7.184]

========================================================================

Covariance estimator: robust

Note: In EGARCH, alpha[1] < 0 indicates leverage effect.

alpha[1] = 0.1876

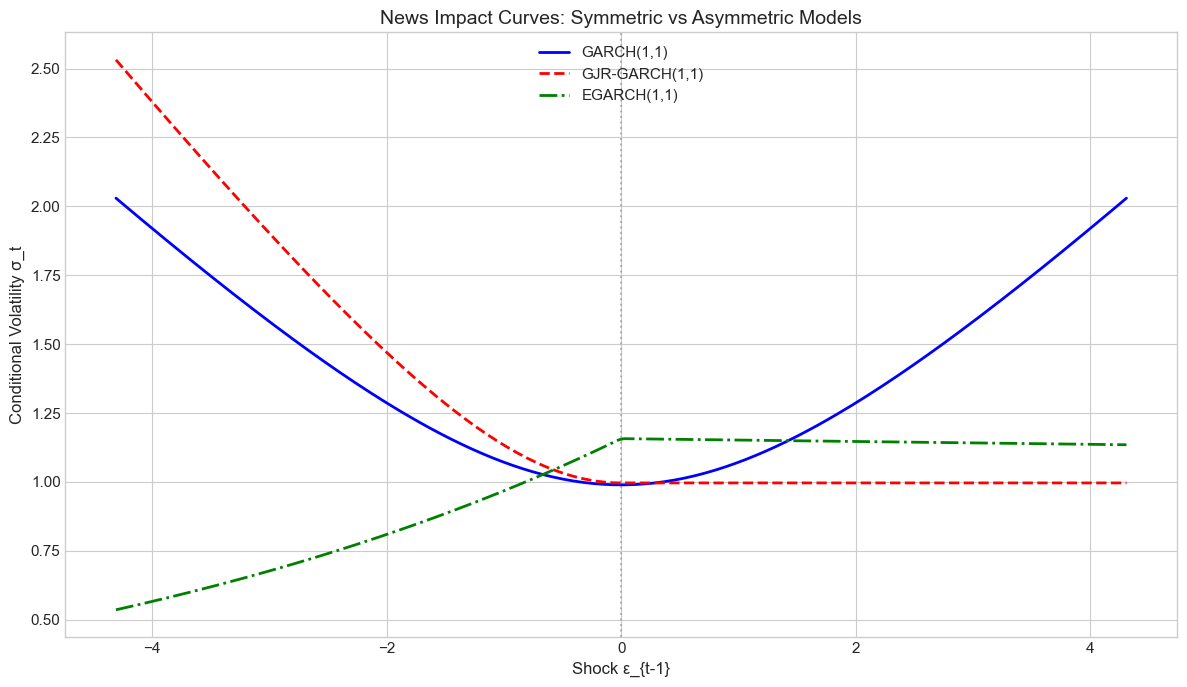

4. News Impact Curves Comparison¶

Source

# Fit symmetric GARCH for comparison

model_garch = arch_model(returns, vol='Garch', p=1, q=1, dist='t')

fit_garch = model_garch.fit(disp='off')

def compute_news_impact_curve(fit, model_type, shock_range, uncond_var):

"""Compute news impact curve for a given model."""

params = fit.params

sample_std = np.sqrt(uncond_var)

shocks = shock_range * sample_std

if model_type == 'GARCH':

omega = params['omega']

alpha = params['alpha[1]']

beta = params['beta[1]']

nic = omega + beta * uncond_var + alpha * shocks**2

elif model_type == 'GJR':

omega = params['omega']

alpha = params['alpha[1]']

gamma = params['gamma[1]']

beta = params['beta[1]']

nic = omega + beta * uncond_var + alpha * shocks**2

nic[shocks < 0] += gamma * shocks[shocks < 0]**2

elif model_type == 'EGARCH':

omega = params['omega']

alpha = params['alpha[1]']

gamma = params['gamma[1]']

beta = params['beta[1]']

z = shocks / sample_std

log_var = omega + beta * np.log(uncond_var) + alpha * z + gamma * (np.abs(z) - np.sqrt(2/np.pi))

nic = np.exp(log_var)

return shocks, nic

# Compute NICs

shock_range = np.linspace(-4, 4, 200)

uncond_var = returns.var()

shocks_g, nic_garch = compute_news_impact_curve(fit_garch, 'GARCH', shock_range, uncond_var)

shocks_j, nic_gjr = compute_news_impact_curve(fit_gjr, 'GJR', shock_range, uncond_var)

shocks_e, nic_egarch = compute_news_impact_curve(fit_egarch, 'EGARCH', shock_range, uncond_var)

# Plot

fig, ax = plt.subplots(figsize=(12, 7))

ax.plot(shocks_g, np.sqrt(nic_garch), 'b-', linewidth=2, label='GARCH(1,1)')

ax.plot(shocks_j, np.sqrt(nic_gjr), 'r--', linewidth=2, label='GJR-GARCH(1,1)')

ax.plot(shocks_e, np.sqrt(nic_egarch), 'g-.', linewidth=2, label='EGARCH(1,1)')

ax.axvline(0, color='gray', linestyle=':', alpha=0.5)

ax.set_xlabel('Shock ε_{t-1}', fontsize=12)

ax.set_ylabel('Conditional Volatility σ_t', fontsize=12)

ax.set_title('News Impact Curves: Symmetric vs Asymmetric Models', fontsize=14)

ax.legend(loc='upper center', fontsize=11)

plt.tight_layout()

plt.show()

print("\nKey observations:")

print("1. GARCH is symmetric (parabola centered at zero)")

print("2. GJR-GARCH has a kink at zero - steeper on the left (negative shocks)")

print("3. EGARCH is smooth and asymmetric")

Key observations:

1. GARCH is symmetric (parabola centered at zero)

2. GJR-GARCH has a kink at zero - steeper on the left (negative shocks)

3. EGARCH is smooth and asymmetric

5. Testing for Asymmetry¶

5.1 Sign Bias Test (Engle & Ng, 1993)¶

Regress squared standardized residuals on sign indicators:

where and .

Sign bias test:

Negative size bias test:

Positive size bias test:

Joint test:

Source

import statsmodels.api as sm

def sign_bias_test(fitted_model):

"""

Perform Engle-Ng sign bias tests for asymmetry.

"""

std_resid = fitted_model.std_resid

resid = fitted_model.resid

# Create variables

z2 = std_resid ** 2

S_neg = (resid < 0).astype(float)

S_pos = 1 - S_neg

# Lag the indicators

df = pd.DataFrame({

'z2': z2,

'S_neg_lag': S_neg.shift(1),

'neg_size': S_neg.shift(1) * resid.shift(1),

'pos_size': S_pos.shift(1) * resid.shift(1)

}).dropna()

# Regression

X = sm.add_constant(df[['S_neg_lag', 'neg_size', 'pos_size']])

y = df['z2']

model = sm.OLS(y, X).fit()

# Individual tests

print("Engle-Ng Sign Bias Tests")

print("="*60)

print(f"\n{'Test':<25} {'Coef':>10} {'t-stat':>10} {'p-value':>10}")

print("-"*60)

tests = [

('Sign Bias', 'S_neg_lag'),

('Negative Size Bias', 'neg_size'),

('Positive Size Bias', 'pos_size')

]

for test_name, var in tests:

coef = model.params[var]

tstat = model.tvalues[var]

pval = model.pvalues[var]

sig = '***' if pval < 0.01 else ('**' if pval < 0.05 else ('*' if pval < 0.1 else ''))

print(f"{test_name:<25} {coef:>10.4f} {tstat:>10.2f} {pval:>10.4f} {sig}")

# Joint test (F-test)

r_matrix = np.eye(4)[1:] # Test all except constant

f_test = model.f_test(r_matrix)

print(f"\n{'Joint Test':<25} {'F-stat':>10} {'':>10} {'p-value':>10}")

print("-"*60)

print(f"{'H0: c1=c2=c3=0':<25} {f_test.fvalue:>10.2f} {'':<10} {f_test.pvalue:>10.4f}")

return model

# Test on symmetric GARCH residuals

print("Testing GARCH(1,1) residuals for asymmetry:")

sb_garch = sign_bias_test(fit_garch)

print("\n" + "="*60)

print("\nTesting GJR-GARCH(1,1) residuals for remaining asymmetry:")

sb_gjr = sign_bias_test(fit_gjr)Testing GARCH(1,1) residuals for asymmetry:

Engle-Ng Sign Bias Tests

============================================================

Test Coef t-stat p-value

------------------------------------------------------------

Sign Bias 0.3460 3.88 0.0001 ***

Negative Size Bias 0.0629 1.20 0.2287

Positive Size Bias -0.0678 -1.03 0.3045

Joint Test F-stat p-value

------------------------------------------------------------

H0: c1=c2=c3=0 9.98 0.0000

============================================================

Testing GJR-GARCH(1,1) residuals for remaining asymmetry:

Engle-Ng Sign Bias Tests

============================================================

Test Coef t-stat p-value

------------------------------------------------------------

Sign Bias 0.3186 3.13 0.0018 ***

Negative Size Bias 0.1583 2.62 0.0089 ***

Positive Size Bias -0.0147 -0.20 0.8436

Joint Test F-stat p-value

------------------------------------------------------------

H0: c1=c2=c3=0 4.94 0.0020

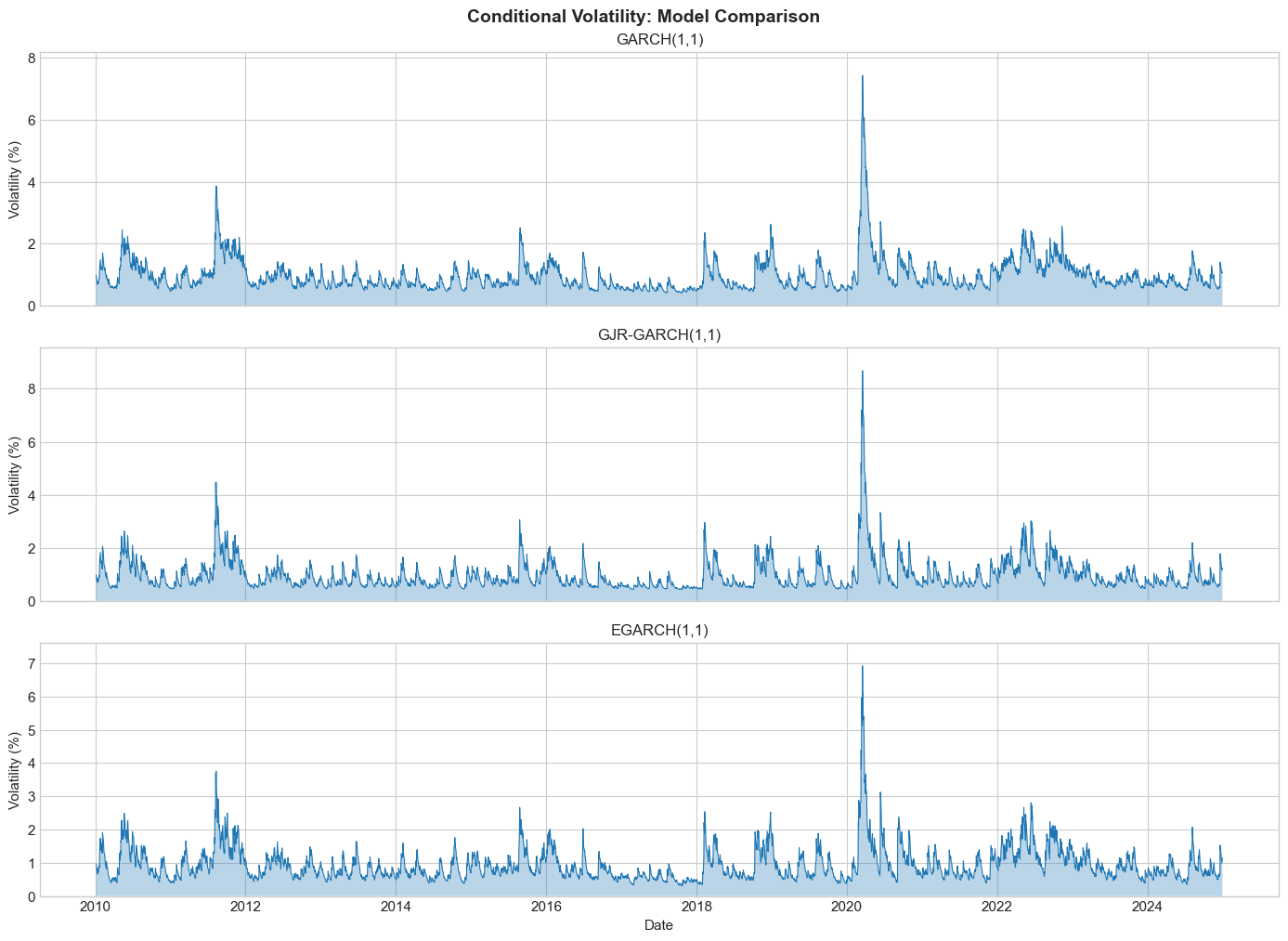

6. Model Comparison¶

Source

# Compare all models

models = {

'GARCH(1,1)': fit_garch,

'GJR-GARCH(1,1)': fit_gjr,

'EGARCH(1,1)': fit_egarch

}

comparison = []

for name, fit in models.items():

comparison.append({

'Model': name,

'Log-Lik': fit.loglikelihood,

'AIC': fit.aic,

'BIC': fit.bic,

'Params': fit.num_params

})

comparison_df = pd.DataFrame(comparison).set_index('Model')

print("Model Comparison")

print("="*60)

print(comparison_df.round(2))

print(f"\nBest model by BIC: {comparison_df['BIC'].idxmin()}")Model Comparison

============================================================

Log-Lik AIC BIC Params

Model

GARCH(1,1) -4711.96 9433.91 9465.09 5

GJR-GARCH(1,1) -4643.32 9298.65 9336.06 6

EGARCH(1,1) -4630.50 9273.01 9310.42 6

Best model by BIC: EGARCH(1,1)

Source

# Plot conditional volatility comparison

fig, axes = plt.subplots(3, 1, figsize=(14, 10), sharex=True)

for ax, (name, fit) in zip(axes, models.items()):

vol = fit.conditional_volatility

ax.plot(vol.index, vol.values, linewidth=0.8, label=name)

ax.fill_between(vol.index, 0, vol.values, alpha=0.3)

ax.set_ylabel('Volatility (%)')

ax.set_title(name, fontsize=12)

ax.set_ylim(0, vol.max() * 1.1)

plt.xlabel('Date')

plt.tight_layout()

plt.suptitle('Conditional Volatility: Model Comparison', y=1.01, fontsize=14, fontweight='bold')

plt.show()

7. Cryptocurrency Application¶

Does the leverage effect exist in cryptocurrency markets?

Source

# Download Bitcoin data

btc = yf.download('BTC-USD', start='2018-01-01', end='2024-12-31', progress=False)

if isinstance(btc.columns, pd.MultiIndex):

btc.columns = btc.columns.get_level_values(0)

btc_returns = (np.log(btc['Close'] / btc['Close'].shift(1)) * 100).dropna()

# Fit models

btc_garch = arch_model(btc_returns, vol='Garch', p=1, q=1, dist='t').fit(disp='off')

btc_gjr = arch_model(btc_returns, vol='Garch', p=1, o=1, q=1, dist='t').fit(disp='off')

print("Bitcoin: GARCH(1,1)")

print(btc_garch.summary())

print("\n\nBitcoin: GJR-GARCH(1,1)")

print(btc_gjr.summary())

btc_gamma = btc_gjr.params['gamma[1]']

print(f"\n\nBitcoin asymmetry parameter γ = {btc_gamma:.4f}")

if btc_gamma > 0:

print("Bitcoin shows leverage effect (surprising for crypto!)")

else:

print("Bitcoin shows inverse leverage effect (common in crypto)")Bitcoin: GARCH(1,1)

Constant Mean - GARCH Model Results

====================================================================================

Dep. Variable: Close R-squared: 0.000

Mean Model: Constant Mean Adj. R-squared: 0.000

Vol Model: GARCH Log-Likelihood: -6402.25

Distribution: Standardized Student's t AIC: 12814.5

Method: Maximum Likelihood BIC: 12843.7

No. Observations: 2555

Date: Thu, Feb 05 2026 Df Residuals: 2554

Time: 09:35:05 Df Model: 1

Mean Model

===========================================================================

coef std err t P>|t| 95.0% Conf. Int.

---------------------------------------------------------------------------

mu 0.0740 4.189e-02 1.767 7.718e-02 [-8.071e-03, 0.156]

Volatility Model

============================================================================

coef std err t P>|t| 95.0% Conf. Int.

----------------------------------------------------------------------------

omega 0.1355 8.336e-02 1.626 0.104 [-2.784e-02, 0.299]

alpha[1] 0.0723 1.091e-02 6.627 3.436e-11 [5.091e-02,9.368e-02]

beta[1] 0.9277 1.334e-02 69.522 0.000 [ 0.902, 0.954]

Distribution

========================================================================

coef std err t P>|t| 95.0% Conf. Int.

------------------------------------------------------------------------

nu 3.1152 0.155 20.057 1.755e-89 [ 2.811, 3.420]

========================================================================

Covariance estimator: robust

Bitcoin: GJR-GARCH(1,1)

Constant Mean - GJR-GARCH Model Results

====================================================================================

Dep. Variable: Close R-squared: 0.000

Mean Model: Constant Mean Adj. R-squared: 0.000

Vol Model: GJR-GARCH Log-Likelihood: -6402.20

Distribution: Standardized Student's t AIC: 12816.4

Method: Maximum Likelihood BIC: 12851.5

No. Observations: 2555

Date: Thu, Feb 05 2026 Df Residuals: 2554

Time: 09:35:05 Df Model: 1

Mean Model

===========================================================================

coef std err t P>|t| 95.0% Conf. Int.

---------------------------------------------------------------------------

mu 0.0749 4.176e-02 1.794 7.274e-02 [-6.910e-03, 0.157]

Volatility Model

==============================================================================

coef std err t P>|t| 95.0% Conf. Int.

------------------------------------------------------------------------------

omega 0.1295 0.100 1.292 0.196 [-6.696e-02, 0.326]

alpha[1] 0.0739 1.130e-02 6.537 6.273e-11 [5.174e-02,9.605e-02]

gamma[1] -5.6362e-03 2.032e-02 -0.277 0.782 [-4.547e-02,3.420e-02]

beta[1] 0.9289 1.652e-02 56.221 0.000 [ 0.897, 0.961]

Distribution

========================================================================

coef std err t P>|t| 95.0% Conf. Int.

------------------------------------------------------------------------

nu 3.1211 0.158 19.770 5.444e-87 [ 2.812, 3.431]

========================================================================

Covariance estimator: robust

Bitcoin asymmetry parameter γ = -0.0056

Bitcoin shows inverse leverage effect (common in crypto)

8. Summary¶

Key Takeaways¶

Leverage effect: Negative shocks increase volatility more than positive shocks (in equities)

GJR-GARCH: Adds asymmetric term ; piecewise parabolic NIC

EGARCH: Models log-variance; smooth asymmetric NIC; no positivity constraints

Testing: Engle-Ng sign bias tests detect asymmetry in GARCH residuals

Crypto: May show inverse leverage effect (positive returns increase volatility)

Preview of Session 4¶

Session 4 covers advanced univariate models: FIGARCH (long memory), APARCH (power transformations), and Component GARCH (short-run vs long-run volatility).

Exercises¶

Exercise 1: Leverage Effect Across Assets¶

Compare the leverage effect (γ parameter) for: S&P 500, Gold, EUR/USD, and VIX. Which assets show the strongest asymmetry?

Exercise 2: TGARCH Implementation¶

Implement TGARCH(1,1) from scratch and compare its NIC to GJR-GARCH.

Exercise 3: Forecast Comparison¶

Compare 22-day ahead volatility forecasts from GARCH, GJR-GARCH, and EGARCH. Which model performs best during the COVID-19 crash?

Exercise 4: Time-Varying Asymmetry¶

Estimate GJR-GARCH on rolling 2-year windows for S&P 500. How does the γ parameter evolve over time?

Exercise 5: Inverse Leverage in Crypto¶

Test multiple cryptocurrencies (ETH, BNB, SOL) for the leverage effect. Is the inverse leverage effect consistent across crypto assets?

References¶

Black, F. (1976). Studies of stock price volatility changes. Proceedings of the 1976 Meetings of the American Statistical Association, 177-181.

Nelson, D. B. (1991). Conditional heteroskedasticity in asset returns: A new approach. Econometrica, 59(2), 347-370.

Glosten, L. R., Jagannathan, R., & Runkle, D. E. (1993). On the relation between the expected value and the volatility of the nominal excess return on stocks. Journal of Finance, 48(5), 1779-1801.

Engle, R. F., & Ng, V. K. (1993). Measuring and testing the impact of news on volatility. Journal of Finance, 48(5), 1749-1778.

Zakoian, J. M. (1994). Threshold heteroskedastic models. Journal of Economic Dynamics and Control, 18(5), 931-955.