Session 2: ARCH and GARCH Models

Course: Advanced Volatility Modeling¶

Learning Objectives¶

By the end of this session, students will be able to:

Derive and understand the ARCH model and its properties

Extend to GARCH and understand the relationship to ARMA processes

Estimate GARCH models using maximum likelihood

Perform model diagnostics and selection

Generate volatility forecasts

1. The ARCH Model¶

1.1 Motivation¶

From Session 1, we established that financial returns exhibit volatility clustering: large returns tend to be followed by large returns. This means variance is time-varying and predictable.

Engle (1982) introduced the AutoRegressive Conditional Heteroskedasticity (ARCH) model to capture this phenomenon.

1.2 Model Specification¶

Let be the return at time . The ARCH(q) model specifies:

where with , and:

Key insight: Conditional variance depends on past squared shocks.

1.3 Properties of ARCH(q)¶

Conditional distribution:

Unconditional variance (assuming stationarity):

This requires for stationarity.

Unconditional kurtosis for ARCH(1):

This exceeds 3 (excess kurtosis > 0), explaining the heavy tails!

1.4 ARCH(1) as AR(1) in Squared Returns¶

Define (conditional variance “surprise”). Then:

This is an AR(1) process in ! The autocorrelation of squared returns is:

Source

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import scipy.stats as stats

from scipy.optimize import minimize

from scipy.stats import norm, t as student_t

import yfinance as yf

import warnings

warnings.filterwarnings('ignore')

plt.style.use('seaborn-v0_8-whitegrid')

plt.rcParams['figure.figsize'] = (12, 6)

plt.rcParams['font.size'] = 11

np.random.seed(42)Source

def simulate_arch(n, omega, alphas, dist='normal', df=5):

"""

Simulate ARCH(q) process.

Parameters

----------

n : int

Number of observations

omega : float

Constant term (must be positive)

alphas : array-like

ARCH coefficients [alpha_1, ..., alpha_q]

dist : str

'normal' or 't' for standardized innovations

df : int

Degrees of freedom if dist='t'

Returns

-------

eps : np.array

ARCH process

sigma2 : np.array

Conditional variances

"""

q = len(alphas)

eps = np.zeros(n)

sigma2 = np.zeros(n)

# Generate standardized innovations

if dist == 'normal':

z = np.random.standard_normal(n)

else:

z = np.random.standard_t(df, n) / np.sqrt(df / (df - 2)) # Standardize

# Unconditional variance for initialization

uncond_var = omega / (1 - np.sum(alphas))

sigma2[:q] = uncond_var

eps[:q] = np.sqrt(uncond_var) * z[:q]

for t in range(q, n):

sigma2[t] = omega + np.sum(alphas * eps[t-q:t][::-1]**2)

eps[t] = np.sqrt(sigma2[t]) * z[t]

return eps, sigma2

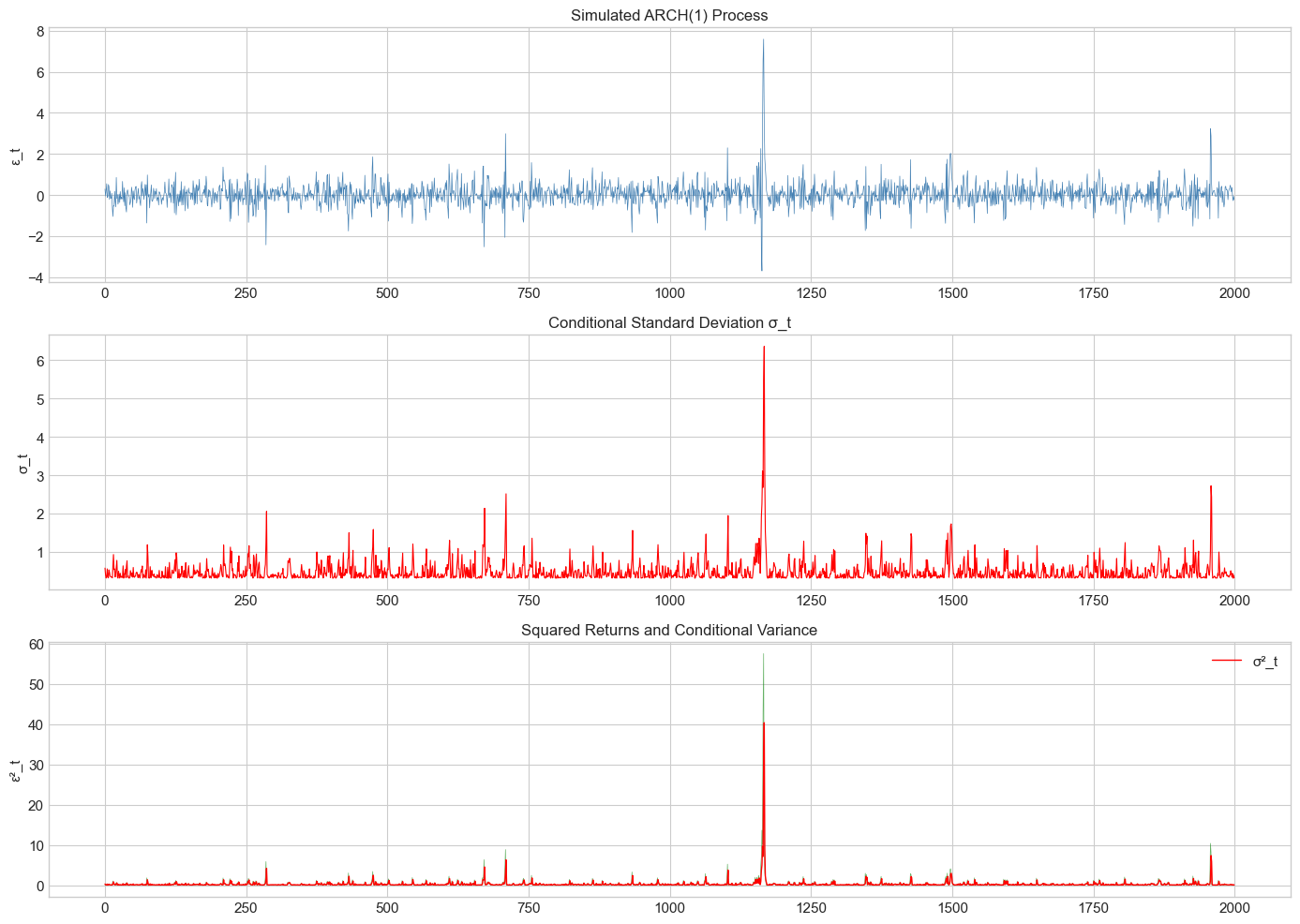

# Simulate ARCH(1) process

n = 2000

omega = 0.1

alpha1 = 0.7

eps_arch, sigma2_arch = simulate_arch(n, omega, [alpha1])

fig, axes = plt.subplots(3, 1, figsize=(14, 10))

axes[0].plot(eps_arch, color='steelblue', linewidth=0.5)

axes[0].set_title('Simulated ARCH(1) Process', fontsize=12)

axes[0].set_ylabel('ε_t')

axes[1].plot(np.sqrt(sigma2_arch), color='red', linewidth=0.8)

axes[1].set_title('Conditional Standard Deviation σ_t', fontsize=12)

axes[1].set_ylabel('σ_t')

axes[2].plot(eps_arch**2, color='green', alpha=0.6, linewidth=0.5)

axes[2].plot(sigma2_arch, color='red', linewidth=1, label='σ²_t')

axes[2].set_title('Squared Returns and Conditional Variance', fontsize=12)

axes[2].set_ylabel('ε²_t')

axes[2].legend()

plt.tight_layout()

plt.show()

2. The GARCH Model¶

2.1 Motivation for GARCH¶

ARCH models require many lags to capture persistent volatility. Bollerslev (1986) introduced the Generalized ARCH (GARCH) model for parsimony.

2.2 GARCH(p,q) Specification¶

The GARCH(1,1) model is:

Interpretation:

: reaction coefficient (sensitivity to recent shocks)

: persistence coefficient (memory of past variance)

: overall persistence

2.3 GARCH as ARMA in Squared Returns¶

Define . Then GARCH(1,1) implies:

This is an ARMA(1,1) process in !

2.4 Stationarity and Persistence¶

Weak stationarity requires:

Unconditional variance:

Volatility half-life: Time for volatility shock to decay by half:

Source

def simulate_garch(n, omega, alphas, betas, dist='normal', df=5):

"""

Simulate GARCH(p,q) process.

Parameters

----------

n : int

Number of observations

omega : float

Constant term

alphas : array-like

ARCH coefficients

betas : array-like

GARCH coefficients

dist : str

Distribution of innovations

df : int

Degrees of freedom for t-distribution

Returns

-------

eps, sigma2 : np.arrays

"""

q = len(alphas)

p = len(betas)

max_lag = max(p, q)

eps = np.zeros(n)

sigma2 = np.zeros(n)

if dist == 'normal':

z = np.random.standard_normal(n)

else:

z = np.random.standard_t(df, n) / np.sqrt(df / (df - 2))

# Unconditional variance

uncond_var = omega / (1 - np.sum(alphas) - np.sum(betas))

sigma2[:max_lag] = uncond_var

eps[:max_lag] = np.sqrt(uncond_var) * z[:max_lag]

for t in range(max_lag, n):

arch_term = np.sum(alphas * eps[t-q:t][::-1]**2) if q > 0 else 0

garch_term = np.sum(betas * sigma2[t-p:t][::-1]) if p > 0 else 0

sigma2[t] = omega + arch_term + garch_term

eps[t] = np.sqrt(sigma2[t]) * z[t]

return eps, sigma2

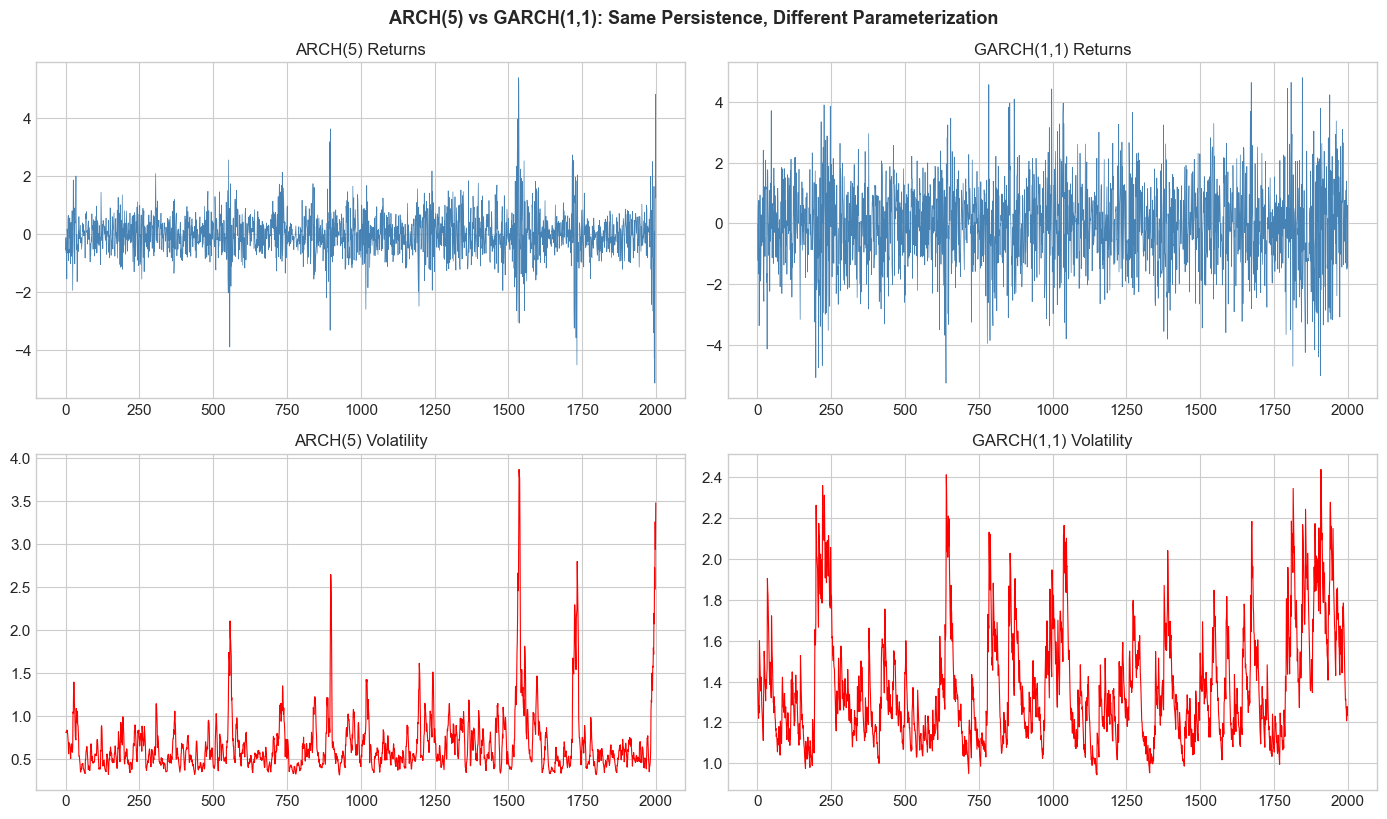

# Compare ARCH(5) vs GARCH(1,1) with similar persistence

n = 2000

# ARCH(5) with persistence ≈ 0.85

alphas_arch5 = np.array([0.20, 0.20, 0.20, 0.15, 0.10]) # sum = 0.85

eps_arch5, sigma2_arch5 = simulate_arch(n, 0.1, alphas_arch5)

# GARCH(1,1) with persistence = 0.85

alpha_garch = 0.10

beta_garch = 0.85

eps_garch, sigma2_garch = simulate_garch(n, 0.1, [alpha_garch], [beta_garch])

fig, axes = plt.subplots(2, 2, figsize=(14, 8))

axes[0,0].plot(eps_arch5, color='steelblue', linewidth=0.5)

axes[0,0].set_title('ARCH(5) Returns', fontsize=12)

axes[0,1].plot(eps_garch, color='steelblue', linewidth=0.5)

axes[0,1].set_title('GARCH(1,1) Returns', fontsize=12)

axes[1,0].plot(np.sqrt(sigma2_arch5), color='red', linewidth=0.8)

axes[1,0].set_title('ARCH(5) Volatility', fontsize=12)

axes[1,1].plot(np.sqrt(sigma2_garch), color='red', linewidth=0.8)

axes[1,1].set_title('GARCH(1,1) Volatility', fontsize=12)

plt.tight_layout()

plt.suptitle('ARCH(5) vs GARCH(1,1): Same Persistence, Different Parameterization',

y=1.02, fontsize=13, fontweight='bold')

plt.show()

print(f"ARCH(5): {len(alphas_arch5)+1} parameters")

print(f"GARCH(1,1): 3 parameters")

print(f"Both have persistence ≈ {np.sum(alphas_arch5):.2f}")

ARCH(5): 6 parameters

GARCH(1,1): 3 parameters

Both have persistence ≈ 0.85

3. Maximum Likelihood Estimation¶

3.1 The Likelihood Function¶

Assuming , the conditional density of is:

The log-likelihood function is:

3.2 Student-t Innovations¶

For heavier tails, use standardized Student-t distribution:

The log-likelihood becomes:

Source

def garch_log_likelihood(params, returns, p=1, q=1, dist='normal'):

"""

Compute negative log-likelihood for GARCH(p,q) model.

Parameters

----------

params : array

[omega, alpha_1,...,alpha_q, beta_1,...,beta_p, (df if t-dist)]

returns : array

Return series (demeaned)

p : int

GARCH order

q : int

ARCH order

dist : str

'normal' or 't'

Returns

-------

float

Negative log-likelihood

"""

T = len(returns)

omega = params[0]

alphas = params[1:1+q]

betas = params[1+q:1+q+p]

if dist == 't':

df = params[-1]

if df <= 2:

return 1e10

# Check parameter constraints

if omega <= 0 or np.any(alphas < 0) or np.any(betas < 0):

return 1e10

if np.sum(alphas) + np.sum(betas) >= 1:

return 1e10

# Initialize variance

sigma2 = np.zeros(T)

sigma2[0] = np.var(returns) # Sample variance as initial

# Compute conditional variances

for t in range(1, T):

sigma2[t] = omega

for i in range(q):

if t - i - 1 >= 0:

sigma2[t] += alphas[i] * returns[t-i-1]**2

for j in range(p):

if t - j - 1 >= 0:

sigma2[t] += betas[j] * sigma2[t-j-1]

# Compute log-likelihood

if dist == 'normal':

ll = -0.5 * np.sum(np.log(2 * np.pi) + np.log(sigma2) + returns**2 / sigma2)

else: # t-distribution

from scipy.special import gammaln

ll = T * (gammaln((df+1)/2) - gammaln(df/2) - 0.5*np.log(np.pi*(df-2)))

ll -= 0.5 * np.sum(np.log(sigma2))

ll -= ((df+1)/2) * np.sum(np.log(1 + returns**2 / ((df-2)*sigma2)))

return -ll # Return negative for minimization

def fit_garch(returns, p=1, q=1, dist='normal'):

"""

Fit GARCH(p,q) model by maximum likelihood.

Returns

-------

dict with 'params', 'sigma2', 'loglik', 'aic', 'bic'

"""

returns = np.asarray(returns)

T = len(returns)

# Initial parameter guesses

var_returns = np.var(returns)

omega_init = var_returns * 0.05

alpha_init = [0.1] * q

beta_init = [0.8 / p] * p

if dist == 'normal':

params_init = [omega_init] + alpha_init + beta_init

else:

params_init = [omega_init] + alpha_init + beta_init + [8.0] # df

# Optimize

result = minimize(

garch_log_likelihood,

params_init,

args=(returns, p, q, dist),

method='Nelder-Mead',

options={'maxiter': 10000}

)

# Refine with BFGS

result = minimize(

garch_log_likelihood,

result.x,

args=(returns, p, q, dist),

method='BFGS',

options={'maxiter': 5000}

)

params = result.x

loglik = -result.fun

# Compute fitted variances

omega = params[0]

alphas = params[1:1+q]

betas = params[1+q:1+q+p]

sigma2 = np.zeros(T)

sigma2[0] = np.var(returns)

for t in range(1, T):

sigma2[t] = omega

for i in range(q):

if t - i - 1 >= 0:

sigma2[t] += alphas[i] * returns[t-i-1]**2

for j in range(p):

if t - j - 1 >= 0:

sigma2[t] += betas[j] * sigma2[t-j-1]

# Information criteria

k = len(params)

aic = -2 * loglik + 2 * k

bic = -2 * loglik + k * np.log(T)

return {

'params': params,

'omega': omega,

'alphas': alphas,

'betas': betas,

'sigma2': sigma2,

'loglik': loglik,

'aic': aic,

'bic': bic,

'persistence': np.sum(alphas) + np.sum(betas)

}Source

# Test on simulated data

true_omega = 0.05

true_alpha = 0.10

true_beta = 0.85

np.random.seed(42)

sim_returns, true_sigma2 = simulate_garch(2000, true_omega, [true_alpha], [true_beta])

# Fit GARCH(1,1)

result = fit_garch(sim_returns, p=1, q=1, dist='normal')

print("GARCH(1,1) Estimation Results (Simulated Data)")

print("="*50)

print(f"\nTrue parameters:")

print(f" ω = {true_omega:.6f}")

print(f" α = {true_alpha:.6f}")

print(f" β = {true_beta:.6f}")

print(f"\nEstimated parameters:")

print(f" ω = {result['omega']:.6f}")

print(f" α = {result['alphas'][0]:.6f}")

print(f" β = {result['betas'][0]:.6f}")

print(f"\nPersistence (α + β): {result['persistence']:.4f}")

print(f"Log-likelihood: {result['loglik']:.2f}")GARCH(1,1) Estimation Results (Simulated Data)

==================================================

True parameters:

ω = 0.050000

α = 0.100000

β = 0.850000

Estimated parameters:

ω = 0.086825

α = 0.100369

β = 0.802914

Persistence (α + β): 0.9033

Log-likelihood: -2682.81

4. Empirical Application: S&P 500¶

Source

# Download S&P 500 data

spy = yf.download('SPY', start='2010-01-01', end='2024-12-31', progress=False)

if isinstance(spy.columns, pd.MultiIndex):

spy.columns = spy.columns.get_level_values(0)

spy['returns'] = np.log(spy['Close'] / spy['Close'].shift(1))

returns = spy['returns'].dropna()

# Demean returns

returns_dm = returns - returns.mean()

print(f"Sample period: {returns.index[0].date()} to {returns.index[-1].date()}")

print(f"Number of observations: {len(returns)}")

print(f"Mean return: {returns.mean()*100:.4f}%")

print(f"Std deviation: {returns.std()*100:.4f}%")

print(f"Annualized volatility: {returns.std()*np.sqrt(252)*100:.2f}%")YF.download() has changed argument auto_adjust default to True

Sample period: 2010-01-05 to 2024-12-30

Number of observations: 3772

Mean return: 0.0510%

Std deviation: 1.0774%

Annualized volatility: 17.10%

Source

# Use arch library for estimation with standard errors

from arch import arch_model

# Fit with arch library (scale returns to percentage for numerical stability)

model = arch_model(returns * 100, vol='Garch', p=1, q=1, dist='Normal')

fitted = model.fit(disp='off')

print("\nGARCH(1,1) Estimation (Normal innovations)")

print("="*50)

print(fitted.summary().tables[1])

GARCH(1,1) Estimation (Normal innovations)

==================================================

Mean Model

==========================================================================

coef std err t P>|t| 95.0% Conf. Int.

--------------------------------------------------------------------------

mu 0.0864 1.216e-02 7.109 1.171e-12 [6.260e-02, 0.110]

==========================================================================

Source

# Compare with Student-t innovations

model_t = arch_model(returns * 100, vol='Garch', p=1, q=1, dist='t')

fitted_t = model_t.fit(disp='off')

print("\nGARCH(1,1) Estimation (Student-t innovations)")

print("="*50)

print(fitted_t.summary().tables[1])

print(f"\n\nModel Comparison:")

print(f"Normal: AIC = {fitted.aic:.2f}, BIC = {fitted.bic:.2f}")

print(f"Student-t: AIC = {fitted_t.aic:.2f}, BIC = {fitted_t.bic:.2f}")

print(f"\nStudent-t degrees of freedom: {fitted_t.params['nu']:.2f}")

GARCH(1,1) Estimation (Student-t innovations)

==================================================

Mean Model

==========================================================================

coef std err t P>|t| 95.0% Conf. Int.

--------------------------------------------------------------------------

mu 0.1023 1.057e-02 9.675 3.834e-22 [8.156e-02, 0.123]

==========================================================================

Model Comparison:

Normal: AIC = 9650.08, BIC = 9675.02

Student-t: AIC = 9433.92, BIC = 9465.10

Student-t degrees of freedom: 5.51

Source

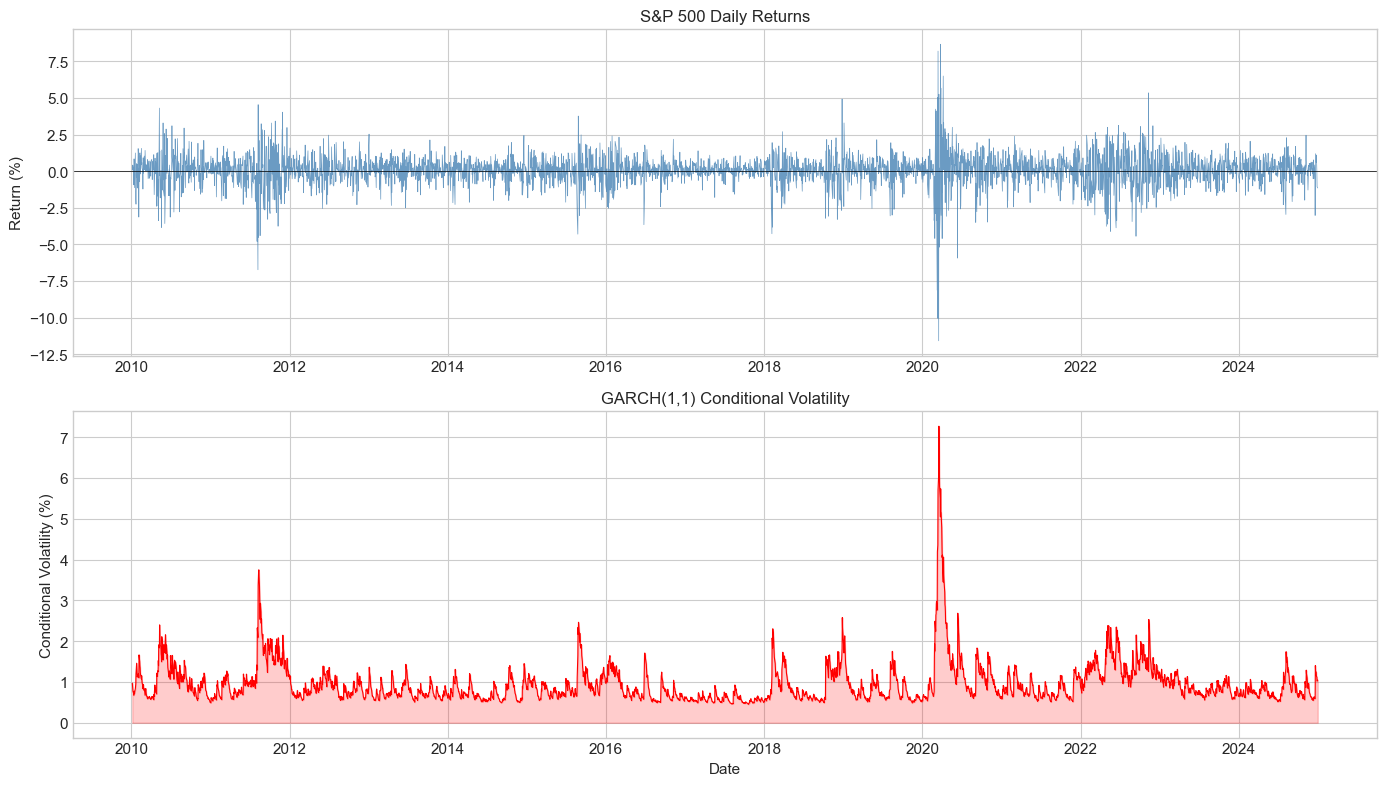

# Plot conditional volatility

fig, axes = plt.subplots(2, 1, figsize=(14, 8))

# Returns

axes[0].plot(returns.index, returns.values * 100, color='steelblue',

linewidth=0.5, alpha=0.8)

axes[0].axhline(0, color='black', linewidth=0.5)

axes[0].set_ylabel('Return (%)')

axes[0].set_title('S&P 500 Daily Returns', fontsize=12)

# Conditional volatility

cond_vol = fitted.conditional_volatility

axes[1].plot(returns.index, cond_vol, color='red', linewidth=0.8)

axes[1].fill_between(returns.index, 0, cond_vol, color='red', alpha=0.2)

axes[1].set_ylabel('Conditional Volatility (%)')

axes[1].set_title('GARCH(1,1) Conditional Volatility', fontsize=12)

axes[1].set_xlabel('Date')

plt.tight_layout()

plt.show()

5. Model Diagnostics¶

5.1 Standardized Residuals¶

If the model is correctly specified, the standardized residuals:

should be i.i.d. with mean 0 and variance 1.

5.2 Diagnostic Tests¶

Ljung-Box test on : Test for remaining autocorrelation in returns

Ljung-Box test on : Test for remaining ARCH effects

Normality test: Jarque-Bera on

Source

from statsmodels.stats.diagnostic import acorr_ljungbox

from scipy.stats import jarque_bera

from statsmodels.graphics.tsaplots import plot_acf

def garch_diagnostics(fitted_model):

"""

Perform diagnostic tests on GARCH residuals.

"""

std_resid = fitted_model.std_resid

print("GARCH Model Diagnostics")

print("="*60)

# Summary statistics of standardized residuals

print("\n1. Standardized Residuals Summary:")

print(f" Mean: {std_resid.mean():.4f} (should be ≈ 0)")

print(f" Std: {std_resid.std():.4f} (should be ≈ 1)")

print(f" Skew: {stats.skew(std_resid):.4f}")

print(f" Kurt: {stats.kurtosis(std_resid):.4f} (excess)")

# Normality test

jb_stat, jb_pval = jarque_bera(std_resid)

print(f"\n2. Jarque-Bera Normality Test:")

print(f" Statistic: {jb_stat:.2f}")

print(f" p-value: {jb_pval:.6f}")

print(f" Result: {'Reject H0 (non-normal)' if jb_pval < 0.05 else 'Fail to reject H0'}")

# Ljung-Box on standardized residuals

lb_resid = acorr_ljungbox(std_resid, lags=[10, 20], return_df=True)

print(f"\n3. Ljung-Box Test on Standardized Residuals:")

print(f" Lag 10: Q = {lb_resid['lb_stat'].iloc[0]:.2f}, p = {lb_resid['lb_pvalue'].iloc[0]:.4f}")

print(f" Lag 20: Q = {lb_resid['lb_stat'].iloc[1]:.2f}, p = {lb_resid['lb_pvalue'].iloc[1]:.4f}")

# Ljung-Box on squared standardized residuals (ARCH effects)

lb_sq = acorr_ljungbox(std_resid**2, lags=[10, 20], return_df=True)

print(f"\n4. Ljung-Box Test on Squared Standardized Residuals:")

print(f" Lag 10: Q = {lb_sq['lb_stat'].iloc[0]:.2f}, p = {lb_sq['lb_pvalue'].iloc[0]:.4f}")

print(f" Lag 20: Q = {lb_sq['lb_stat'].iloc[1]:.2f}, p = {lb_sq['lb_pvalue'].iloc[1]:.4f}")

return std_resid

std_resid = garch_diagnostics(fitted)GARCH Model Diagnostics

============================================================

1. Standardized Residuals Summary:

Mean: -0.0509 (should be ≈ 0)

Std: 0.9986 (should be ≈ 1)

Skew: -0.6267

Kurt: 1.8564 (excess)

2. Jarque-Bera Normality Test:

Statistic: 788.54

p-value: 0.000000

Result: Reject H0 (non-normal)

3. Ljung-Box Test on Standardized Residuals:

Lag 10: Q = 11.65, p = 0.3088

Lag 20: Q = 25.22, p = 0.1930

4. Ljung-Box Test on Squared Standardized Residuals:

Lag 10: Q = 7.41, p = 0.6860

Lag 20: Q = 10.70, p = 0.9537

Source

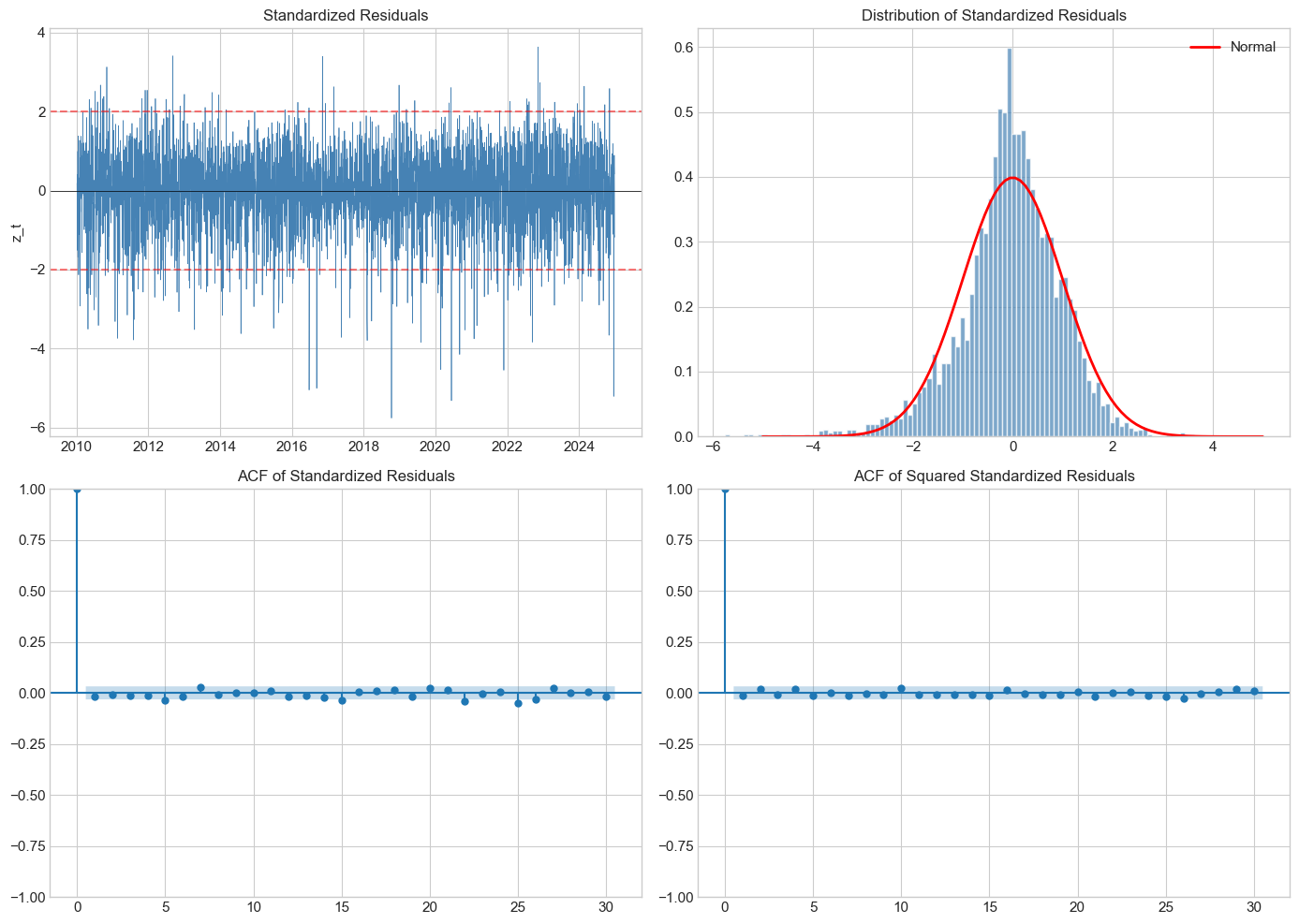

# Visual diagnostics

fig, axes = plt.subplots(2, 2, figsize=(14, 10))

# Time series of standardized residuals

axes[0,0].plot(returns.index, std_resid, color='steelblue', linewidth=0.5)

axes[0,0].axhline(0, color='black', linewidth=0.5)

axes[0,0].axhline(2, color='red', linestyle='--', alpha=0.5)

axes[0,0].axhline(-2, color='red', linestyle='--', alpha=0.5)

axes[0,0].set_title('Standardized Residuals', fontsize=12)

axes[0,0].set_ylabel('z_t')

# Histogram vs Normal

axes[0,1].hist(std_resid, bins=100, density=True, alpha=0.7,

color='steelblue', edgecolor='white')

x = np.linspace(-5, 5, 100)

axes[0,1].plot(x, norm.pdf(x), 'r-', lw=2, label='Normal')

axes[0,1].set_title('Distribution of Standardized Residuals', fontsize=12)

axes[0,1].legend()

# ACF of standardized residuals

plot_acf(std_resid, lags=30, ax=axes[1,0], alpha=0.05)

axes[1,0].set_title('ACF of Standardized Residuals', fontsize=12)

# ACF of squared standardized residuals

plot_acf(std_resid**2, lags=30, ax=axes[1,1], alpha=0.05)

axes[1,1].set_title('ACF of Squared Standardized Residuals', fontsize=12)

plt.tight_layout()

plt.show()

6. Model Selection¶

6.1 Information Criteria¶

Akaike Information Criterion (AIC):

Bayesian Information Criterion (BIC):

where is the number of parameters and is the sample size.

BIC penalizes complexity more heavily and tends to select more parsimonious models.

Source

# Model selection: Compare different GARCH specifications

specifications = [

(1, 1, 'Normal'),

(1, 1, 't'),

(1, 2, 'Normal'),

(1, 2, 't'),

(2, 1, 'Normal'),

(2, 1, 't'),

(2, 2, 'Normal'),

(2, 2, 't'),

]

results = []

for p, q, dist in specifications:

model = arch_model(returns * 100, vol='Garch', p=p, q=q, dist=dist)

fit = model.fit(disp='off')

results.append({

'Model': f'GARCH({p},{q})',

'Distribution': dist,

'Log-Lik': fit.loglikelihood,

'AIC': fit.aic,

'BIC': fit.bic,

'Params': fit.num_params

})

results_df = pd.DataFrame(results)

results_df = results_df.sort_values('BIC')

print("Model Selection Results")

print("="*70)

print(results_df.to_string(index=False))

print(f"\nBest model by BIC: {results_df.iloc[0]['Model']} with {results_df.iloc[0]['Distribution']} innovations")Model Selection Results

======================================================================

Model Distribution Log-Lik AIC BIC Params

GARCH(1,1) t -4711.959934 9433.919868 9465.096671 5

GARCH(2,1) t -4708.599087 9429.198175 9466.610339 6

GARCH(1,2) t -4711.959934 9435.919868 9473.332032 6

GARCH(2,2) t -4708.324808 9430.649616 9474.297140 7

GARCH(1,1) Normal -4821.041592 9650.083185 9675.024628 4

GARCH(2,1) Normal -4819.078583 9648.157167 9679.333970 5

GARCH(1,2) Normal -4821.041593 9652.083185 9683.259988 5

GARCH(2,2) Normal -4818.129509 9648.259018 9685.671182 6

Best model by BIC: GARCH(1,1) with t innovations

7. Volatility Forecasting¶

7.1 Multi-Step Forecasts¶

For GARCH(1,1), the h-step ahead forecast is:

where is the unconditional variance.

As , .

7.2 Forecast Evaluation¶

Since volatility is latent, we need proxies:

Squared returns: (noisy but unbiased)

Realized variance (high-frequency data)

Implied volatility (from options)

Source

# Generate volatility forecasts

forecast_horizon = 22 # 1 month ahead

# Fit model on data up to a point and forecast

train_end = '2023-12-31'

returns_train = returns[returns.index <= train_end]

returns_test = returns[returns.index > train_end]

model = arch_model(returns_train * 100, vol='Garch', p=1, q=1, dist='t')

fitted = model.fit(disp='off')

# Multi-step forecast

forecasts = fitted.forecast(horizon=forecast_horizon, reindex=False)

print("Volatility Forecasts (% per day)")

print("="*40)

print(f"1-day ahead: {np.sqrt(forecasts.variance.iloc[-1, 0]):.4f}%")

print(f"5-day ahead: {np.sqrt(forecasts.variance.iloc[-1, 4]):.4f}%")

print(f"22-day ahead: {np.sqrt(forecasts.variance.iloc[-1, -1]):.4f}%")

# Unconditional volatility

omega = fitted.params['omega']

alpha = fitted.params['alpha[1]']

beta = fitted.params['beta[1]']

uncond_vol = np.sqrt(omega / (1 - alpha - beta))

print(f"\nUnconditional volatility: {uncond_vol:.4f}%")Volatility Forecasts (% per day)

========================================

1-day ahead: 0.6337%

5-day ahead: 0.6960%

22-day ahead: 0.9023%

Unconditional volatility: 1.9216%

Source

# Rolling forecast evaluation

def rolling_forecast_evaluation(returns, window=1000, horizon=1):

"""

Perform rolling 1-step ahead forecasts and compare to realized volatility.

"""

forecasted_vol = []

realized_vol = []

dates = []

returns_array = returns * 100 # Convert to percentage

for t in range(window, len(returns_array) - horizon):

# Fit on rolling window

train = returns_array.iloc[t-window:t]

try:

model = arch_model(train, vol='Garch', p=1, q=1, dist='Normal')

fit = model.fit(disp='off', show_warning=False)

# 1-step forecast

fcast = fit.forecast(horizon=horizon, reindex=False)

forecasted_vol.append(np.sqrt(fcast.variance.iloc[-1, -1]))

# Realized volatility proxy: absolute return

realized_vol.append(np.abs(returns_array.iloc[t + horizon - 1]))

dates.append(returns_array.index[t + horizon - 1])

except:

continue

return pd.DataFrame({

'forecasted': forecasted_vol,

'realized': realized_vol

}, index=dates)

# Run rolling evaluation (subset for speed)

returns_subset = returns['2020-01-01':'2024-12-31']

eval_df = rolling_forecast_evaluation(returns_subset, window=500, horizon=1)

# Compute forecast evaluation metrics

mse = np.mean((eval_df['forecasted'] - eval_df['realized'])**2)

mae = np.mean(np.abs(eval_df['forecasted'] - eval_df['realized']))

corr = eval_df['forecasted'].corr(eval_df['realized'])

print("Forecast Evaluation (1-day ahead)")

print("="*40)

print(f"MSE: {mse:.4f}")

print(f"MAE: {mae:.4f}")

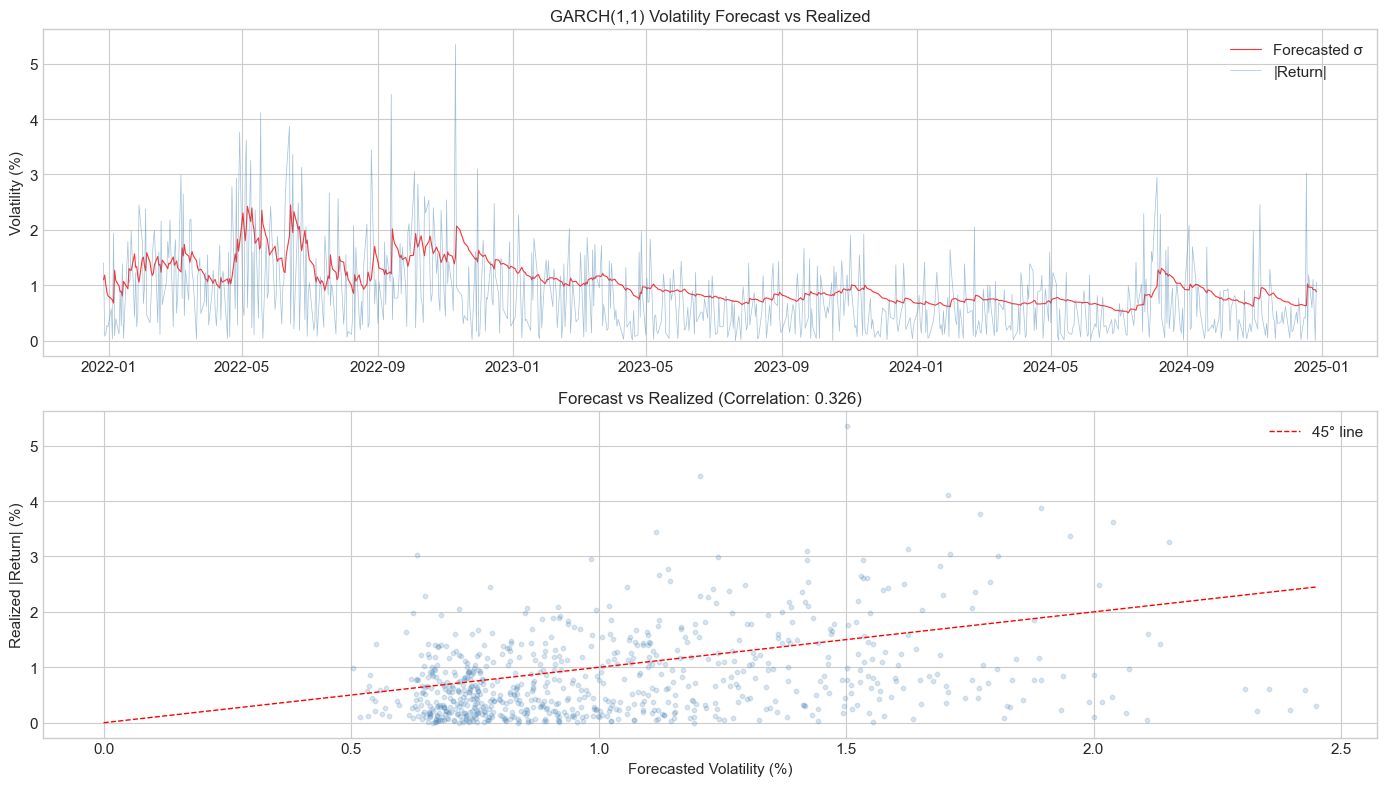

print(f"Correlation: {corr:.4f}")Forecast Evaluation (1-day ahead)

========================================

MSE: 0.5660

MAE: 0.6038

Correlation: 0.3263

Source

# Plot forecast vs realized

fig, axes = plt.subplots(2, 1, figsize=(14, 8))

# Time series comparison

axes[0].plot(eval_df.index, eval_df['forecasted'], color='red',

linewidth=0.8, label='Forecasted σ', alpha=0.8)

axes[0].plot(eval_df.index, eval_df['realized'], color='steelblue',

linewidth=0.5, label='|Return|', alpha=0.5)

axes[0].set_title('GARCH(1,1) Volatility Forecast vs Realized', fontsize=12)

axes[0].set_ylabel('Volatility (%)')

axes[0].legend()

# Scatter plot

axes[1].scatter(eval_df['forecasted'], eval_df['realized'],

alpha=0.2, s=10, color='steelblue')

axes[1].plot([0, eval_df['forecasted'].max()], [0, eval_df['forecasted'].max()],

'r--', linewidth=1, label='45° line')

axes[1].set_xlabel('Forecasted Volatility (%)')

axes[1].set_ylabel('Realized |Return| (%)')

axes[1].set_title(f'Forecast vs Realized (Correlation: {corr:.3f})', fontsize=12)

axes[1].legend()

plt.tight_layout()

plt.show()

8. Integrated GARCH (IGARCH)¶

When , we have the Integrated GARCH model. This implies:

Shocks to volatility persist forever

Unconditional variance is infinite

Volatility forecasts don’t revert to a long-run mean

The EWMA model is a special case: IGARCH(1,1) with no constant:

where and .

Source

# Compare GARCH vs IGARCH forecasts

# Standard GARCH(1,1)

model_garch = arch_model(returns * 100, vol='Garch', p=1, q=1)

fit_garch = model_garch.fit(disp='off')

# EWMA (RiskMetrics) - IGARCH with lambda=0.94

model_ewma = arch_model(returns * 100, vol='EWMA')#, lam=0.94)

fit_ewma = model_ewma.fit(disp='off')

# Generate long-horizon forecasts

horizon = 100

fcast_garch = fit_garch.forecast(horizon=horizon, reindex=False)

fcast_ewma = fit_ewma.forecast(horizon=horizon, reindex=False)

# Plot forecast paths

fig, ax = plt.subplots(figsize=(12, 6))

days = np.arange(1, horizon + 1)

ax.plot(days, np.sqrt(fcast_garch.variance.iloc[-1].values),

'b-', linewidth=2, label='GARCH(1,1)')

ax.plot(days, np.sqrt(fcast_ewma.variance.iloc[-1].values),

'r--', linewidth=2, label='EWMA (λ=0.94)')

# Unconditional volatility

omega = fit_garch.params['omega']

alpha = fit_garch.params['alpha[1]']

beta = fit_garch.params['beta[1]']

uncond_vol = np.sqrt(omega / (1 - alpha - beta))

ax.axhline(uncond_vol, color='blue', linestyle=':', alpha=0.5,

label=f'GARCH unconditional vol: {uncond_vol:.2f}%')

ax.set_xlabel('Forecast Horizon (days)')

ax.set_ylabel('Forecasted Volatility (%)')

ax.set_title('GARCH vs IGARCH (EWMA): Forecast Mean Reversion', fontsize=13)

ax.legend()

plt.tight_layout()

plt.show()

print(f"\nGARCH(1,1) persistence: {alpha + beta:.4f}")

print(f"EWMA persistence: 1.0000 (by construction)")---------------------------------------------------------------------------

ValueError Traceback (most recent call last)

Cell In[41], line 7

4 fit_garch = model_garch.fit(disp='off')

6 # EWMA (RiskMetrics) - IGARCH with lambda=0.94

----> 7 model_ewma = arch_model(returns * 100, vol='EWMA')#, lam=0.94)

8 fit_ewma = model_ewma.fit(disp='off')

10 # Generate long-horizon forecasts

File ~\AppData\Local\anaconda3\Lib\site-packages\arch\univariate\mean.py:2019, in arch_model(y, x, mean, lags, vol, p, o, q, power, dist, hold_back, rescale)

2017 raise ValueError("Unknown model type in mean")

2018 if vol_model not in known_vol:

-> 2019 raise ValueError("Unknown model type in vol")

2020 if dist_name not in known_dist:

2021 raise ValueError("Unknown model type in dist")

ValueError: Unknown model type in vol9. Summary¶

Key Takeaways¶

ARCH models capture volatility clustering by making variance depend on past squared shocks

GARCH extends ARCH with lagged variance terms, providing a parsimonious representation

Estimation is done by maximum likelihood; Student-t innovations typically improve fit

Diagnostics check that standardized residuals are i.i.d.

GARCH(1,1) is often sufficient for daily financial data

Persistence () determines how quickly volatility reverts to its mean

Preview of Session 3¶

GARCH(1,1) has a symmetric news impact: positive and negative shocks of the same magnitude have the same effect on volatility. But we know the leverage effect exists!

Session 3 covers asymmetric GARCH models: EGARCH, GJR-GARCH, TGARCH.

Exercises¶

Exercise 1: Bitcoin GARCH¶

Fit GARCH(1,1) to Bitcoin daily returns. How does the persistence compare to S&P 500? What does this imply about volatility half-life?

Exercise 2: Distribution Choice¶

Compare Normal, Student-t, and Skewed Student-t distributions for S&P 500. Which provides the best fit according to BIC?

Exercise 3: Higher-Order GARCH¶

Estimate GARCH(2,2) for S&P 500. Is the improvement in log-likelihood worth the additional parameters?

Exercise 4: Forecast Evaluation¶

Implement the Mincer-Zarnowitz regression:

Test H0: (unbiased forecasts).

Exercise 5: IGARCH¶

Fit IGARCH(1,1) to S&P 500 and compare forecasts with GARCH(1,1) at horizons of 1, 5, 22, and 66 days.

References¶

Engle, R. F. (1982). Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica, 50(4), 987-1007.

Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31(3), 307-327.

Bollerslev, T., Chou, R. Y., & Kroner, K. F. (1992). ARCH modeling in finance: A review of the theory and empirical evidence. Journal of Econometrics, 52(1-2), 5-59.

Francq, C., & Zakoian, J. M. (2019). GARCH Models: Structure, Statistical Inference and Financial Applications. John Wiley & Sons.