Session 1: Foundations of Volatility - Stylized Facts and Statistical Properties

Course: Advanced Volatility Modeling¶

Learning Objectives¶

By the end of this session, students will be able to:

Define volatility mathematically and understand its role in financial markets

Identify and empirically verify the stylized facts of financial returns

Understand why simple models (e.g., geometric Brownian motion) fail to capture market dynamics

Motivate the need for sophisticated volatility models

1. Introduction to Volatility¶

1.1 What is Volatility?¶

Volatility measures the dispersion of returns for a given security or market index. In mathematical finance, we distinguish between several concepts:

Historical (Realized) Volatility: The standard deviation of logarithmic returns over a historical period:

where are log-returns and is the sample mean.

Implied Volatility: The volatility parameter extracted from option prices using the Black-Scholes formula (or other pricing models).

Conditional Volatility: The expected volatility at time given information available at time :

where is the information set (sigma-algebra) at time .

1.2 Why Does Volatility Matter?¶

Risk Management: VaR, Expected Shortfall, portfolio optimization

Derivative Pricing: Options are essentially volatility instruments

Asset Allocation: Risk parity, mean-variance optimization

Regulatory Capital: Basel requirements for banks

2. Mathematical Foundations¶

2.1 The Geometric Brownian Motion Benchmark¶

The starting point for financial modeling is often Geometric Brownian Motion (GBM):

where is a standard Brownian motion. By Itô’s lemma, log-prices follow:

This implies that log-returns over interval are:

Key Implications of GBM:

Returns are i.i.d. (independent and identically distributed)

Returns are normally distributed

Volatility is constant over time

We will show that all three assumptions are violated in real data.

2.2 Annualization of Volatility¶

If daily volatility is , then annual volatility is:

assuming 252 trading days per year. This follows from the scaling property of variance:

under the assumption of independent returns.

3. Empirical Analysis: Setting Up¶

Source

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import scipy.stats as stats

from scipy.stats import norm, jarque_bera, kurtosis, skew

import yfinance as yf

import warnings

warnings.filterwarnings('ignore')

# Set plotting style

plt.style.use('seaborn-v0_8-whitegrid')

plt.rcParams['figure.figsize'] = (12, 6)

plt.rcParams['font.size'] = 11Source

# Download data for multiple assets

tickers = {

'SPY': 'S&P 500 ETF',

'BTC-USD': 'Bitcoin',

'EURUSD=X': 'EUR/USD',

'GC=F': 'Gold Futures'

}

start_date = '2015-01-01'

end_date = '2024-12-31'

data = {}

for ticker, name in tickers.items():

df = yf.download(ticker, start=start_date, end=end_date, progress=False)

if len(df) > 0:

# Handle multi-index columns from yfinance

if isinstance(df.columns, pd.MultiIndex):

df.columns = df.columns.get_level_values(0)

data[name] = df['Close'].dropna()

print(f"Data downloaded for: {list(data.keys())}")

for name, series in data.items():

print(f"{name}: {len(series)} observations from {series.index[0].date()} to {series.index[-1].date()}")YF.download() has changed argument auto_adjust default to True

Data downloaded for: ['S&P 500 ETF', 'Bitcoin', 'EUR/USD', 'Gold Futures']

S&P 500 ETF: 2515 observations from 2015-01-02 to 2024-12-30

Bitcoin: 3652 observations from 2015-01-01 to 2024-12-30

EUR/USD: 2605 observations from 2015-01-01 to 2024-12-30

Gold Futures: 2512 observations from 2015-01-02 to 2024-12-30

Source

def compute_returns(prices, method='log'):

"""Compute returns from price series.

Parameters

----------

prices : pd.Series

Price series

method : str

'log' for logarithmic returns, 'simple' for arithmetic returns

Returns

-------

pd.Series

Returns series

"""

if method == 'log':

return np.log(prices / prices.shift(1)).dropna()

else:

return prices.pct_change().dropna()

# Compute log returns for all assets

returns = {name: compute_returns(prices) for name, prices in data.items()}4. Stylized Facts of Financial Returns¶

Financial returns exhibit several robust empirical regularities, often called stylized facts. These patterns are observed across different markets, assets, and time periods.

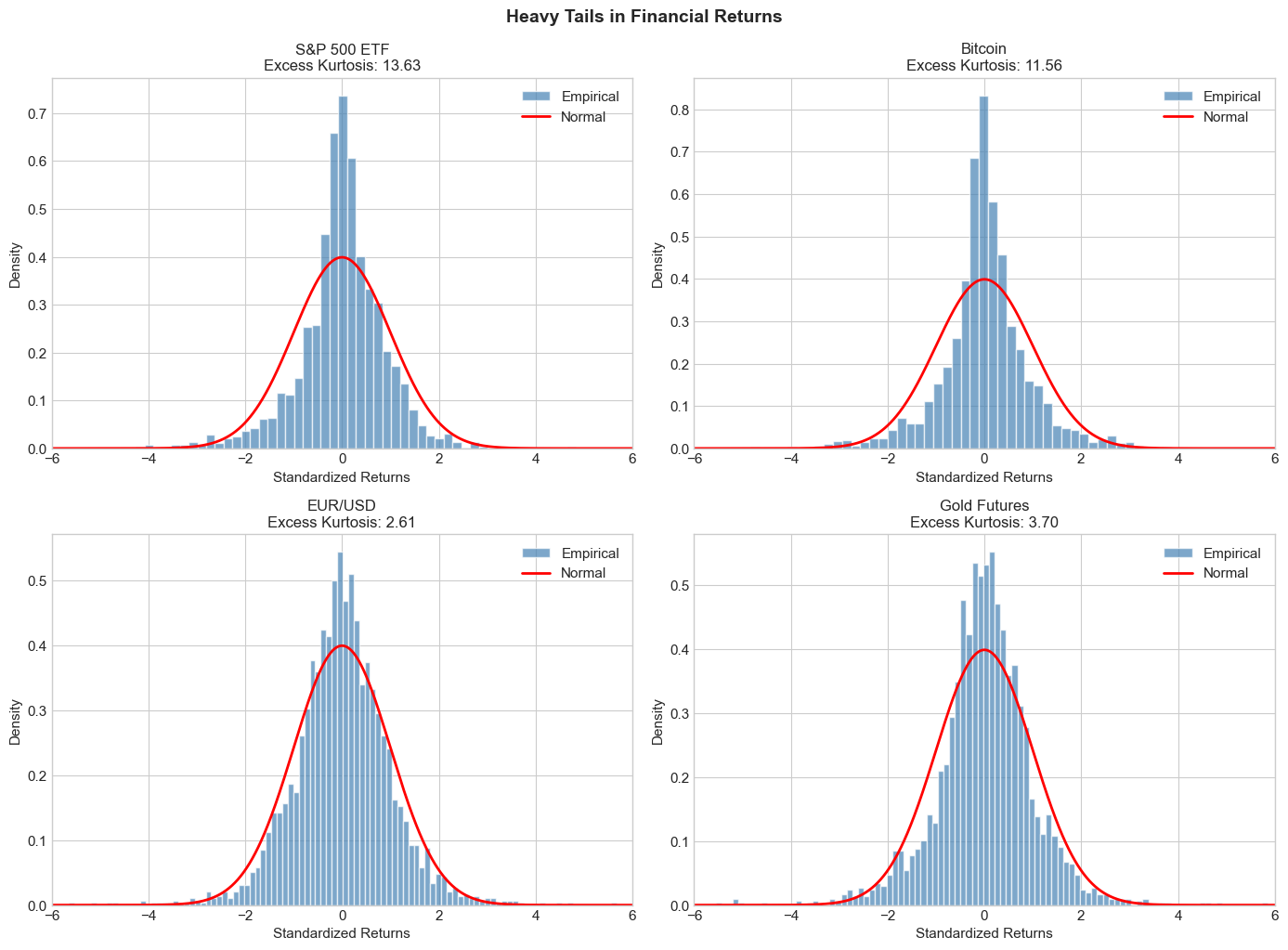

4.1 Stylized Fact 1: Heavy Tails (Leptokurtosis)¶

Financial returns have heavier tails than the normal distribution. This means extreme events occur more frequently than a Gaussian model would predict.

Kurtosis measures the heaviness of tails:

For the normal distribution, . Excess kurtosis is , which is positive for heavy-tailed distributions.

Source

def descriptive_statistics(returns_dict):

"""Compute descriptive statistics for return series."""

stats_list = []

for name, ret in returns_dict.items():

stats_dict = {

'Asset': name,

'N': len(ret),

'Mean (%)': ret.mean() * 100,

'Std Dev (%)': ret.std() * 100,

'Annual Vol (%)': ret.std() * np.sqrt(252) * 100,

'Skewness': skew(ret),

'Excess Kurtosis': kurtosis(ret), # scipy computes excess kurtosis

'Min (%)': ret.min() * 100,

'Max (%)': ret.max() * 100,

'JB Statistic': jarque_bera(ret)[0],

'JB p-value': jarque_bera(ret)[1]

}

stats_list.append(stats_dict)

return pd.DataFrame(stats_list).set_index('Asset').round(4)

stats_df = descriptive_statistics(returns)

print("Descriptive Statistics of Daily Returns")

print("="*60)

stats_dfDescriptive Statistics of Daily Returns

============================================================

Source

# Visual comparison with normal distribution

fig, axes = plt.subplots(2, 2, figsize=(14, 10))

axes = axes.flatten()

for ax, (name, ret) in zip(axes, returns.items()):

# Standardize returns

ret_standardized = (ret - ret.mean()) / ret.std()

# Histogram

ax.hist(ret_standardized, bins=100, density=True, alpha=0.7,

label='Empirical', color='steelblue', edgecolor='white')

# Normal distribution overlay

x = np.linspace(-6, 6, 1000)

ax.plot(x, norm.pdf(x), 'r-', lw=2, label='Normal')

ax.set_title(f'{name}\nExcess Kurtosis: {kurtosis(ret):.2f}', fontsize=12)

ax.set_xlabel('Standardized Returns')

ax.set_ylabel('Density')

ax.legend()

ax.set_xlim(-6, 6)

plt.tight_layout()

plt.suptitle('Heavy Tails in Financial Returns', y=1.02, fontsize=14, fontweight='bold')

plt.show()

Source

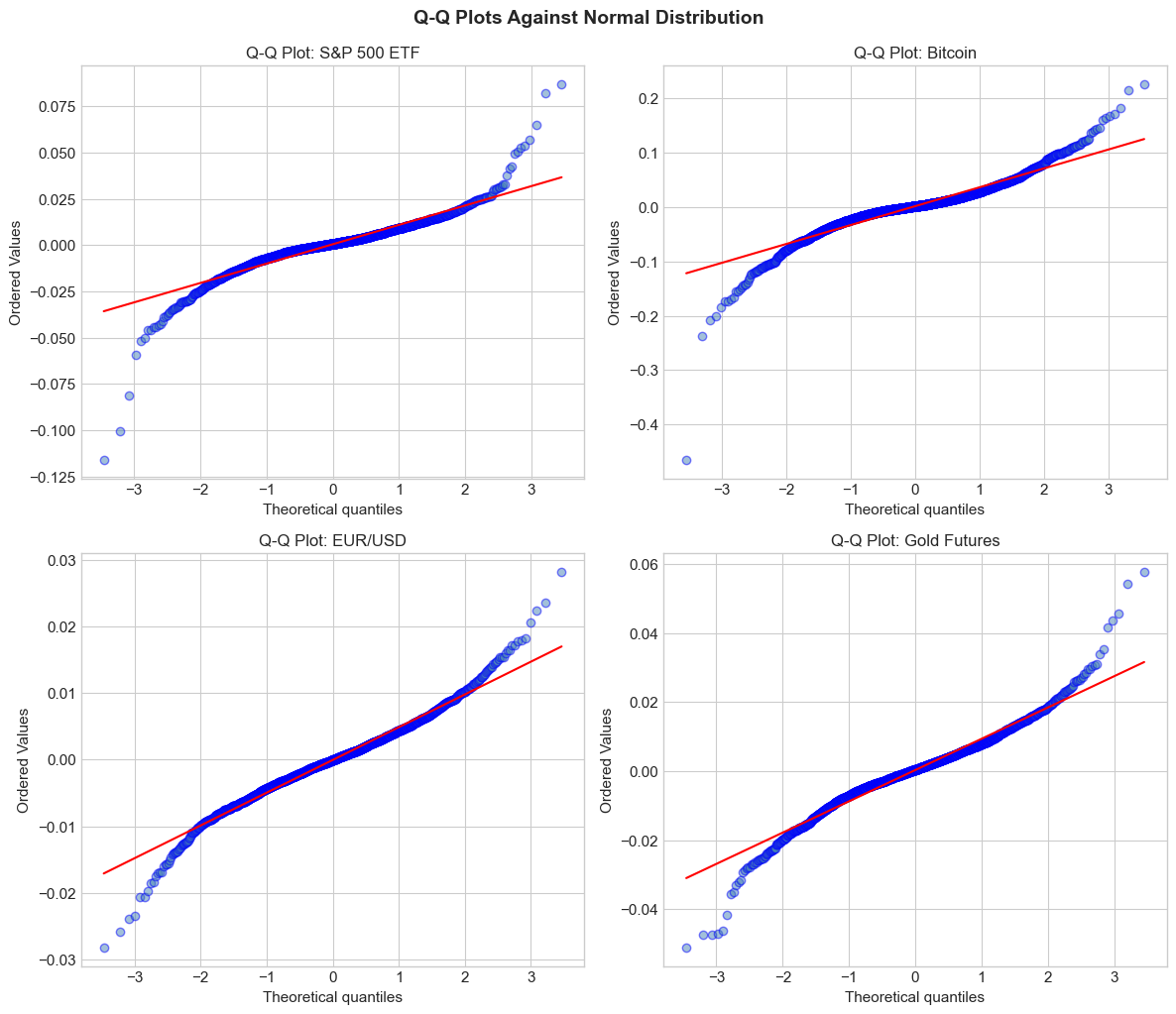

# Q-Q plots for normality assessment

fig, axes = plt.subplots(2, 2, figsize=(12, 10))

axes = axes.flatten()

for ax, (name, ret) in zip(axes, returns.items()):

stats.probplot(ret, dist="norm", plot=ax)

ax.set_title(f'Q-Q Plot: {name}', fontsize=12)

ax.get_lines()[0].set_markerfacecolor('steelblue')

ax.get_lines()[0].set_alpha(0.5)

ax.get_lines()[1].set_color('red')

plt.tight_layout()

plt.suptitle('Q-Q Plots Against Normal Distribution', y=1.02, fontsize=14, fontweight='bold')

plt.show()

print("\nInterpretation: Deviations from the red line, especially in the tails,")

print("indicate departures from normality. S-shaped patterns suggest heavy tails.")

Interpretation: Deviations from the red line, especially in the tails,

indicate departures from normality. S-shaped patterns suggest heavy tails.

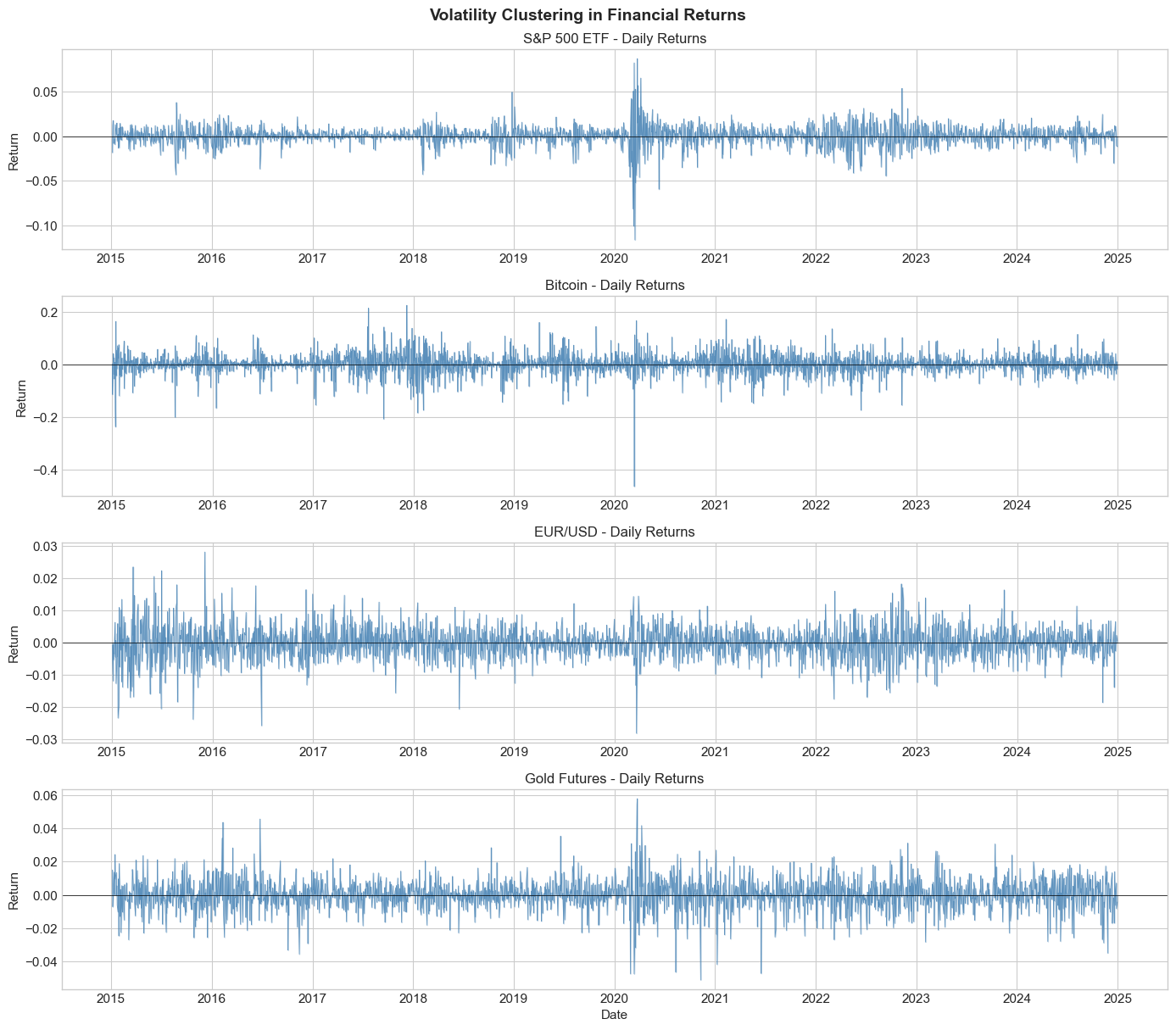

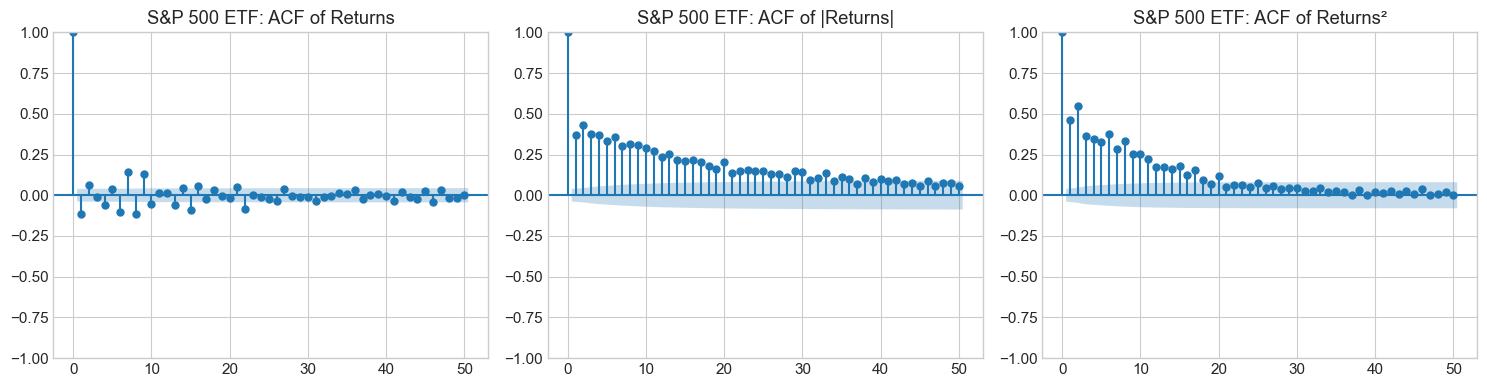

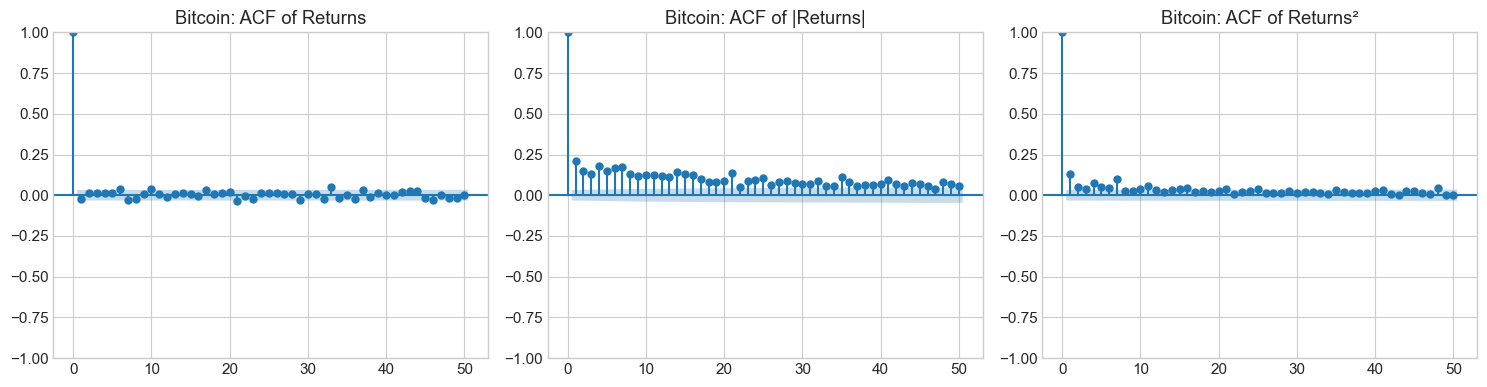

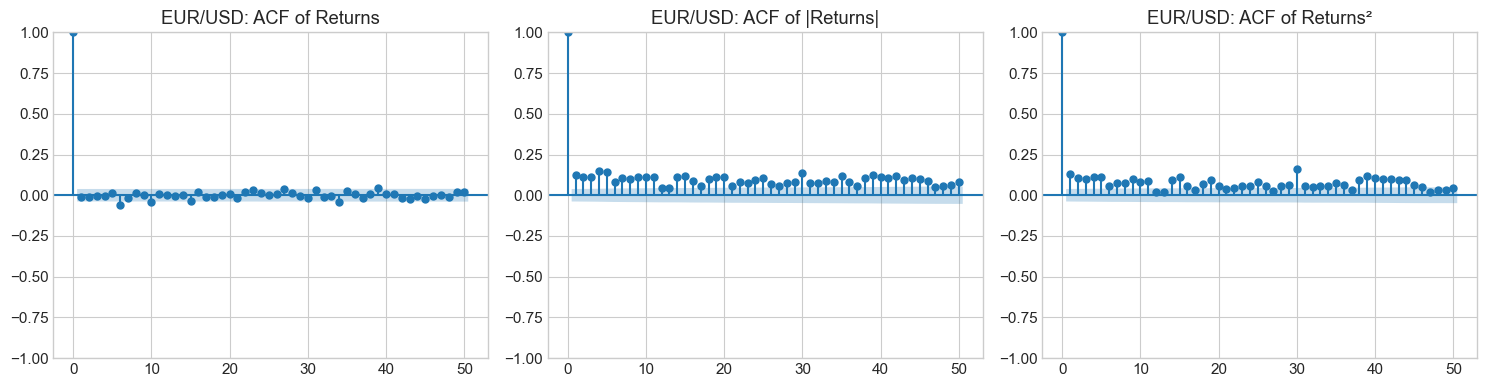

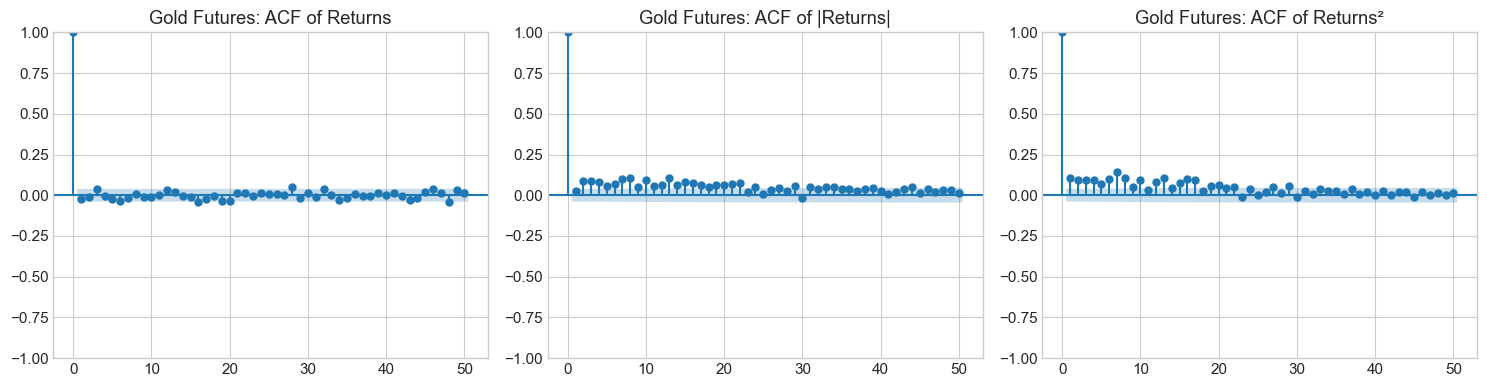

4.2 Stylized Fact 2: Volatility Clustering¶

Large returns (in absolute value) tend to be followed by large returns, and small returns tend to be followed by small returns. This creates periods of high and low volatility.

Mathematically, while returns themselves show little autocorrelation:

Squared or absolute returns show significant positive autocorrelation:

This is the key motivation for GARCH-type models.

Source

# Visualize volatility clustering

fig, axes = plt.subplots(len(returns), 1, figsize=(14, 3*len(returns)))

for ax, (name, ret) in zip(axes, returns.items()):

ax.plot(ret.index, ret.values, color='steelblue', alpha=0.8, linewidth=0.5)

ax.axhline(y=0, color='black', linestyle='-', linewidth=0.5)

ax.fill_between(ret.index, ret.values, 0, alpha=0.3, color='steelblue')

ax.set_title(f'{name} - Daily Returns', fontsize=12)

ax.set_ylabel('Return')

plt.xlabel('Date')

plt.tight_layout()

plt.suptitle('Volatility Clustering in Financial Returns', y=1.01, fontsize=14, fontweight='bold')

plt.show()

Source

from statsmodels.graphics.tsaplots import plot_acf

def plot_acf_comparison(returns_series, name, max_lags=50):

"""Plot ACF of returns vs squared returns."""

fig, axes = plt.subplots(1, 3, figsize=(15, 4))

# ACF of returns

plot_acf(returns_series, lags=max_lags, ax=axes[0], alpha=0.05,

title=f'{name}: ACF of Returns')

# ACF of absolute returns

plot_acf(np.abs(returns_series), lags=max_lags, ax=axes[1], alpha=0.05,

title=f'{name}: ACF of |Returns|')

# ACF of squared returns

plot_acf(returns_series**2, lags=max_lags, ax=axes[2], alpha=0.05,

title=f'{name}: ACF of Returns²')

plt.tight_layout()

plt.show()

for name, ret in returns.items():

plot_acf_comparison(ret, name)

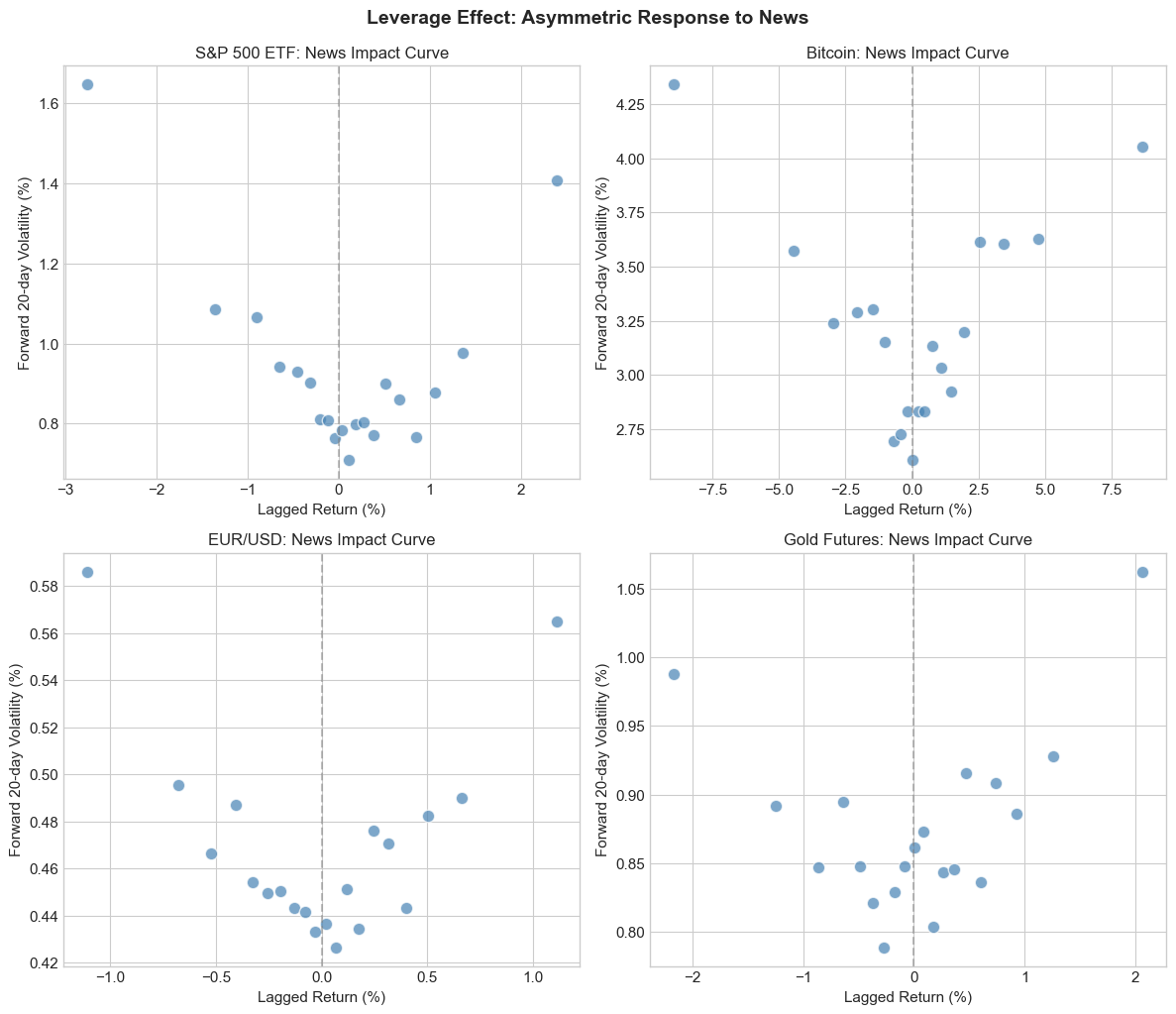

4.3 Stylized Fact 3: Leverage Effect (Asymmetry)¶

Negative returns tend to increase future volatility more than positive returns of the same magnitude. This asymmetry is called the leverage effect (Black, 1976).

The name comes from the corporate finance explanation: when stock prices fall, the firm’s debt-to-equity ratio increases, making the stock riskier.

Mathematically:

This motivates asymmetric GARCH models like EGARCH and GJR-GARCH.

Source

def news_impact_analysis(returns_series, name):

"""Analyze asymmetric impact of positive vs negative returns on future volatility."""

ret = returns_series.copy()

# Create lagged returns and forward realized volatility (20-day)

df = pd.DataFrame({

'return': ret,

'return_lag': ret.shift(1),

'fwd_vol': ret.rolling(window=20).std().shift(-20)

}).dropna()

# Bin lagged returns

df['return_bin'] = pd.qcut(df['return_lag'], q=20, labels=False, duplicates='drop')

# Compute mean forward volatility by bin

grouped = df.groupby('return_bin').agg({

'return_lag': 'mean',

'fwd_vol': 'mean'

}).sort_values('return_lag')

return grouped

fig, axes = plt.subplots(2, 2, figsize=(12, 10))

axes = axes.flatten()

for ax, (name, ret) in zip(axes, returns.items()):

grouped = news_impact_analysis(ret, name)

ax.scatter(grouped['return_lag']*100, grouped['fwd_vol']*100,

s=80, c='steelblue', alpha=0.7, edgecolor='white')

ax.axvline(x=0, color='gray', linestyle='--', alpha=0.5)

ax.set_xlabel('Lagged Return (%)')

ax.set_ylabel('Forward 20-day Volatility (%)')

ax.set_title(f'{name}: News Impact Curve', fontsize=12)

plt.tight_layout()

plt.suptitle('Leverage Effect: Asymmetric Response to News', y=1.02, fontsize=14, fontweight='bold')

plt.show()

print("\nInterpretation: If negative returns (left side) correspond to higher")

print("forward volatility than positive returns, we have evidence of the leverage effect.")

Interpretation: If negative returns (left side) correspond to higher

forward volatility than positive returns, we have evidence of the leverage effect.

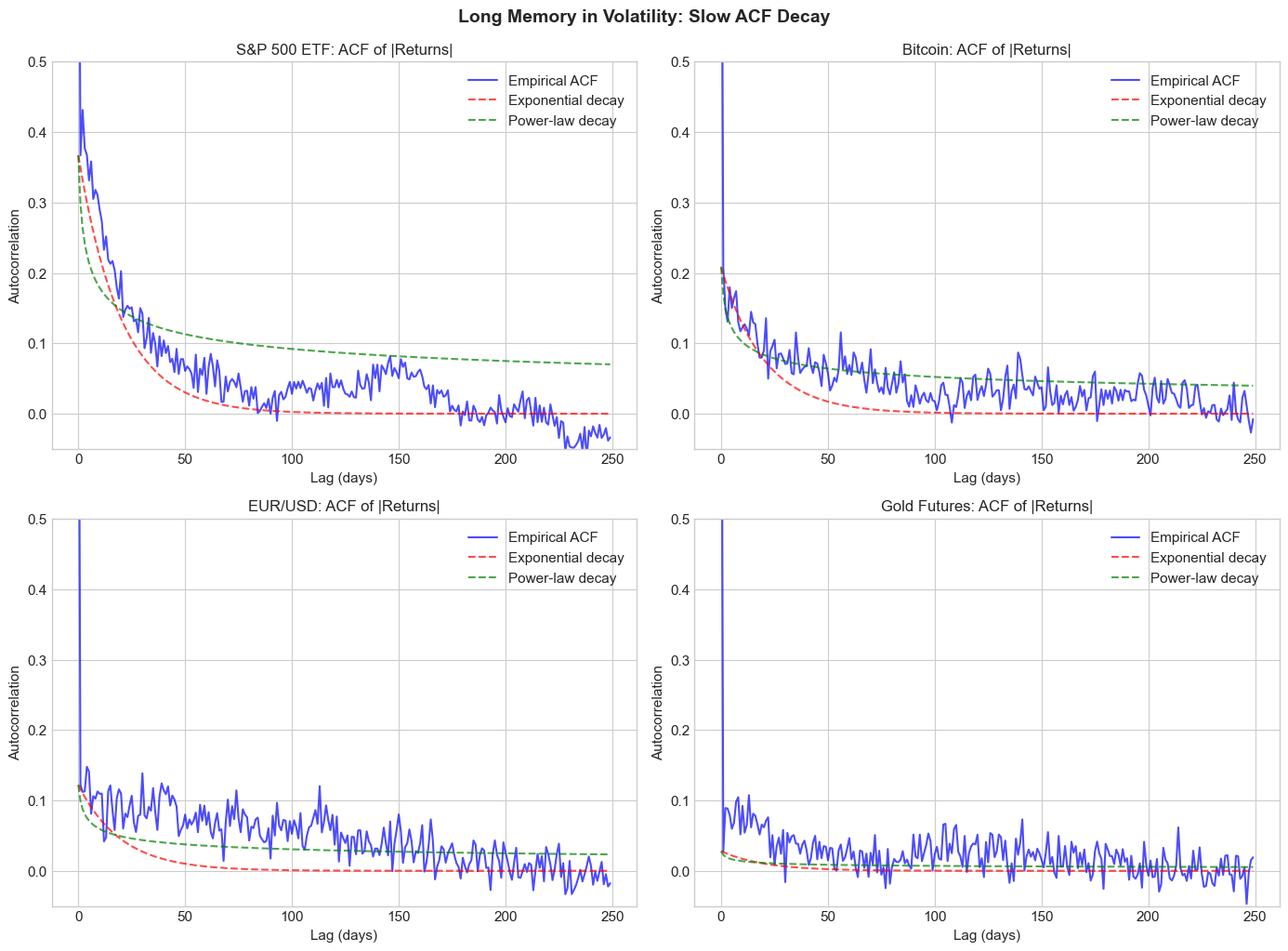

4.4 Stylized Fact 4: Long Memory in Volatility¶

The autocorrelation of squared or absolute returns decays slowly - much slower than exponential decay would predict. This suggests long memory or long-range dependence.

For a long-memory process, the autocorrelation function decays hyperbolically:

where is the fractional differencing parameter.

This motivates FIGARCH and long-memory volatility models, and connects to rough volatility (which we’ll cover later).

Source

def compute_acf(series, max_lag=500):

"""Compute autocorrelation function."""

n = len(series)

mean = series.mean()

var = series.var()

acf = np.zeros(max_lag)

for k in range(max_lag):

acf[k] = np.mean((series.iloc[k:] - mean) * (series.iloc[:-k if k > 0 else n].values - mean)) / var

return acf

# Compare ACF decay patterns

fig, axes = plt.subplots(2, 2, figsize=(14, 10))

axes = axes.flatten()

max_lag = 250

for ax, (name, ret) in zip(axes, returns.items()):

abs_ret = np.abs(ret)

acf_vals = compute_acf(abs_ret, max_lag=max_lag)

lags = np.arange(max_lag)

# Plot ACF

ax.plot(lags, acf_vals, 'b-', alpha=0.7, label='Empirical ACF')

# Fit exponential decay (short memory)

exp_decay = acf_vals[1] * np.exp(-0.05 * lags)

ax.plot(lags, exp_decay, 'r--', alpha=0.7, label='Exponential decay')

# Fit power-law decay (long memory)

power_decay = acf_vals[1] * (lags + 1) ** (-0.3)

ax.plot(lags, power_decay, 'g--', alpha=0.7, label='Power-law decay')

ax.set_xlabel('Lag (days)')

ax.set_ylabel('Autocorrelation')

ax.set_title(f'{name}: ACF of |Returns|', fontsize=12)

ax.legend()

ax.set_ylim(-0.05, 0.5)

plt.tight_layout()

plt.suptitle('Long Memory in Volatility: Slow ACF Decay', y=1.02, fontsize=14, fontweight='bold')

plt.show()

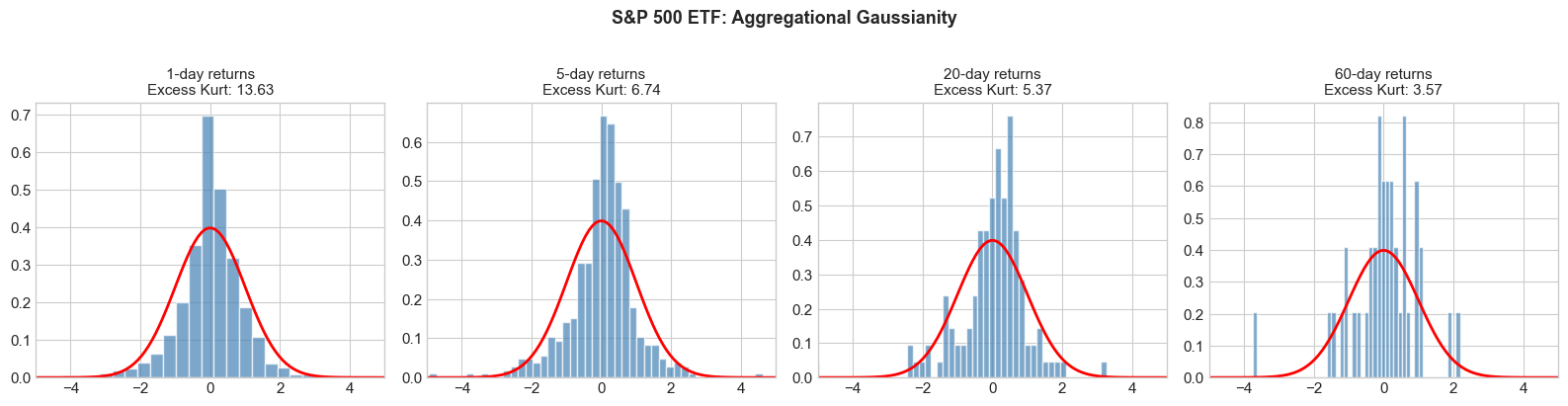

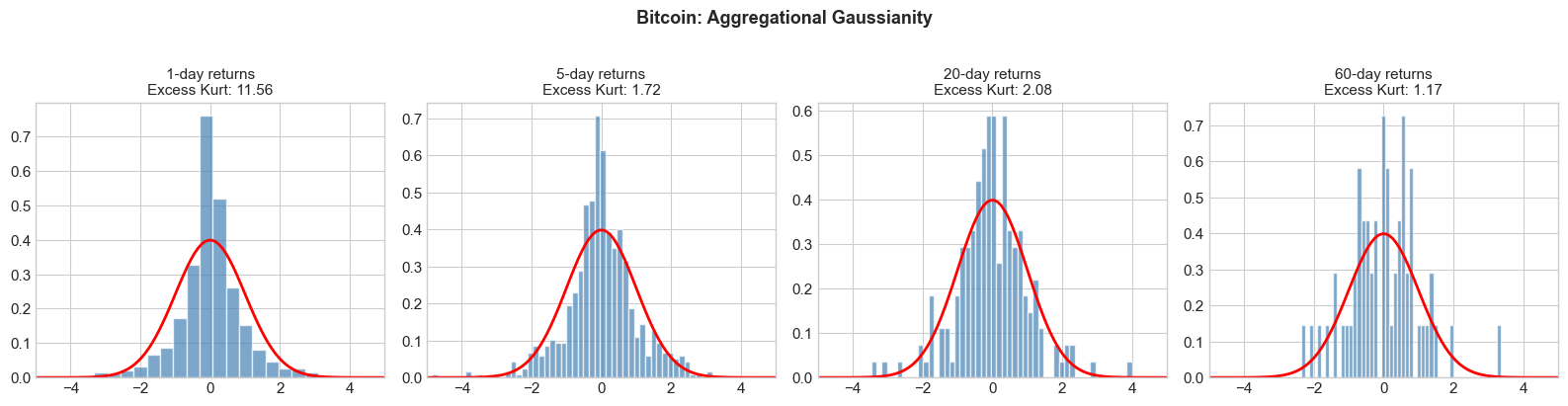

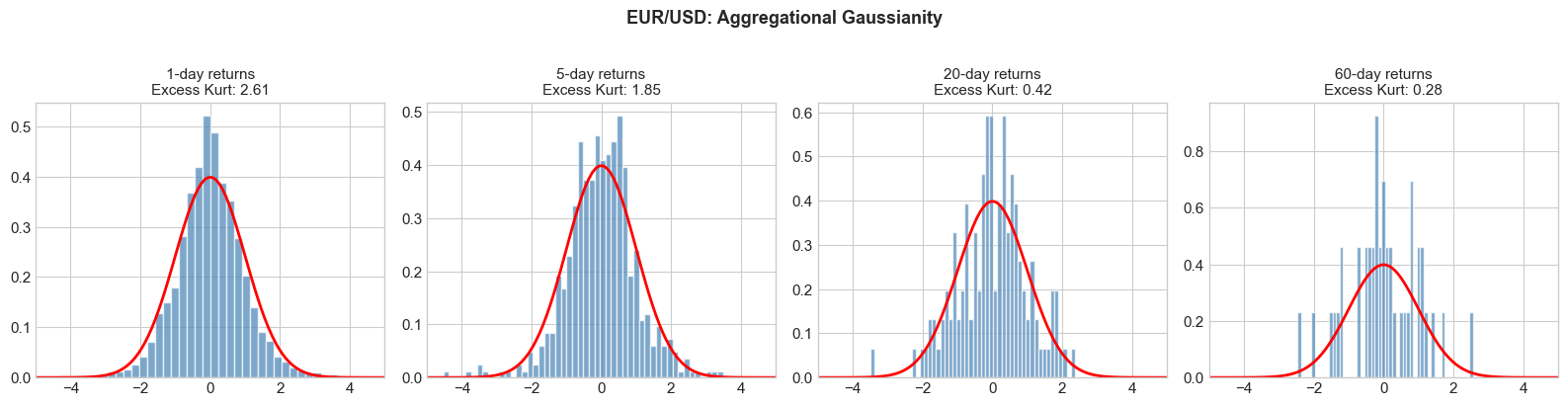

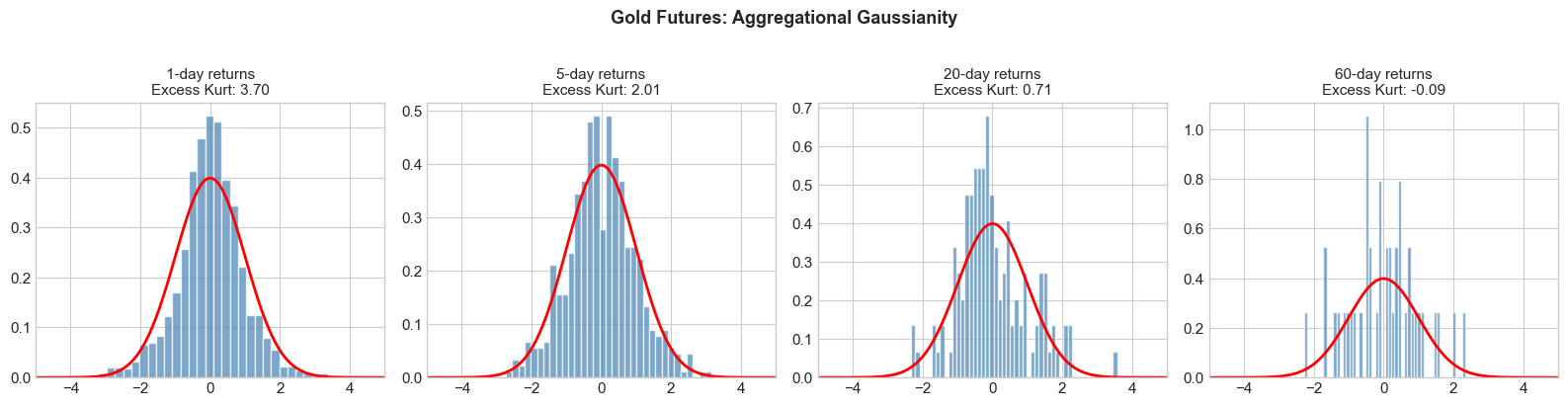

4.5 Stylized Fact 5: Aggregational Gaussianity¶

While daily returns are non-Gaussian, returns over longer horizons (weekly, monthly) tend to become more Gaussian. This is a manifestation of the Central Limit Theorem, but the convergence is slower than for i.i.d. variables due to dependence in volatility.

Source

def aggregational_gaussianity(returns_series, name, horizons=[1, 5, 20, 60]):

"""Show convergence to normality as horizon increases."""

fig, axes = plt.subplots(1, len(horizons), figsize=(4*len(horizons), 4))

for ax, h in zip(axes, horizons):

# Aggregate returns

if h == 1:

agg_ret = returns_series

else:

agg_ret = returns_series.rolling(h).sum().dropna()[::h] # Non-overlapping

# Standardize

agg_std = (agg_ret - agg_ret.mean()) / agg_ret.std()

# Histogram

ax.hist(agg_std, bins=50, density=True, alpha=0.7, color='steelblue', edgecolor='white')

# Normal overlay

x = np.linspace(-5, 5, 100)

ax.plot(x, norm.pdf(x), 'r-', lw=2)

# Excess kurtosis

ek = kurtosis(agg_ret)

ax.set_title(f'{h}-day returns\nExcess Kurt: {ek:.2f}', fontsize=11)

ax.set_xlim(-5, 5)

plt.suptitle(f'{name}: Aggregational Gaussianity', y=1.02, fontsize=13, fontweight='bold')

plt.tight_layout()

plt.show()

for name, ret in returns.items():

aggregational_gaussianity(ret, name)

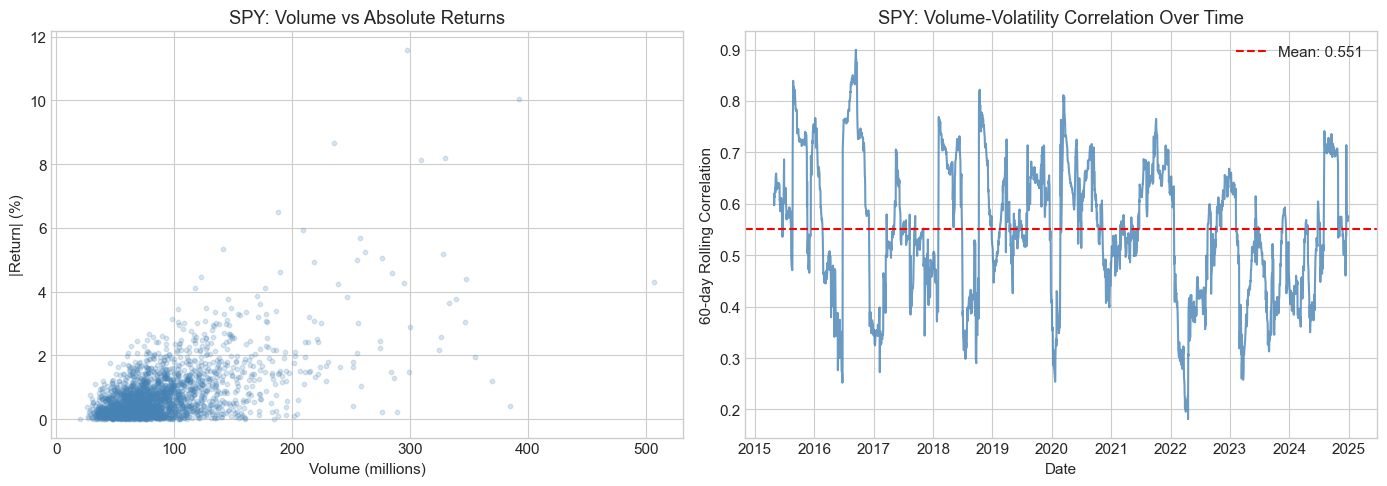

4.6 Stylized Fact 6: Volume-Volatility Correlation¶

Trading volume and volatility are positively correlated. High volatility periods typically coincide with high trading activity.

This is related to the Mixture of Distributions Hypothesis (MDH): both volume and volatility are driven by an underlying information arrival process.

Source

# Analyze volume-volatility relationship for SPY

spy_data = yf.download('SPY', start=start_date, end=end_date, progress=False)

if isinstance(spy_data.columns, pd.MultiIndex):

spy_data.columns = spy_data.columns.get_level_values(0)

spy_data['returns'] = np.log(spy_data['Close'] / spy_data['Close'].shift(1))

spy_data['abs_returns'] = np.abs(spy_data['returns'])

spy_data['volume_ma'] = spy_data['Volume'].rolling(20).mean()

spy_data['vol_20d'] = spy_data['returns'].rolling(20).std()

spy_data = spy_data.dropna()

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

# Scatter plot

axes[0].scatter(spy_data['Volume']/1e6, spy_data['abs_returns']*100,

alpha=0.2, s=10, c='steelblue')

axes[0].set_xlabel('Volume (millions)')

axes[0].set_ylabel('|Return| (%)')

axes[0].set_title('SPY: Volume vs Absolute Returns')

# Correlation over time

rolling_corr = spy_data['Volume'].rolling(60).corr(spy_data['abs_returns'])

axes[1].plot(rolling_corr.index, rolling_corr.values, color='steelblue', alpha=0.8)

axes[1].axhline(y=rolling_corr.mean(), color='red', linestyle='--',

label=f'Mean: {rolling_corr.mean():.3f}')

axes[1].set_xlabel('Date')

axes[1].set_ylabel('60-day Rolling Correlation')

axes[1].set_title('SPY: Volume-Volatility Correlation Over Time')

axes[1].legend()

plt.tight_layout()

plt.show()

print(f"\nOverall correlation between volume and |returns|: {spy_data['Volume'].corr(spy_data['abs_returns']):.4f}")

Overall correlation between volume and |returns|: 0.5870

5. Testing for ARCH Effects¶

Before fitting volatility models, we should formally test whether ARCH effects (conditional heteroskedasticity) are present.

5.1 Engle’s ARCH-LM Test¶

Under the null hypothesis of no ARCH effects, regress squared residuals on their lags:

Test statistic: under

5.2 Ljung-Box Test on Squared Returns¶

Test for autocorrelation in squared returns:

Source

from statsmodels.stats.diagnostic import acorr_ljungbox, het_arch

def test_arch_effects(returns_series, name, lags=10):

"""Test for ARCH effects using multiple tests."""

ret = returns_series.dropna()

# Demean returns

resid = ret - ret.mean()

# ARCH-LM test

arch_test = het_arch(resid, nlags=lags)

# Ljung-Box test on squared returns

lb_test = acorr_ljungbox(resid**2, lags=[lags], return_df=True)

print(f"\n{'='*60}")

print(f"ARCH Effects Tests for {name}")

print(f"{'='*60}")

print(f"\nARCH-LM Test (q={lags}):")

print(f" LM Statistic: {arch_test[0]:.4f}")

print(f" p-value: {arch_test[1]:.6f}")

print(f" Conclusion: {'Reject H0 (ARCH effects present)' if arch_test[1] < 0.05 else 'Fail to reject H0'}")

print(f"\nLjung-Box Test on Squared Returns (m={lags}):")

print(f" Q Statistic: {lb_test['lb_stat'].values[0]:.4f}")

print(f" p-value: {lb_test['lb_pvalue'].values[0]:.6f}")

print(f" Conclusion: {'Reject H0 (autocorrelation in squared returns)' if lb_test['lb_pvalue'].values[0] < 0.05 else 'Fail to reject H0'}")

for name, ret in returns.items():

test_arch_effects(ret, name)

============================================================

ARCH Effects Tests for S&P 500 ETF

============================================================

ARCH-LM Test (q=10):

LM Statistic: 960.3901

p-value: 0.000000

Conclusion: Reject H0 (ARCH effects present)

Ljung-Box Test on Squared Returns (m=10):

Q Statistic: 3328.9704

p-value: 0.000000

Conclusion: Reject H0 (autocorrelation in squared returns)

============================================================

ARCH Effects Tests for Bitcoin

============================================================

ARCH-LM Test (q=10):

LM Statistic: 120.5881

p-value: 0.000000

Conclusion: Reject H0 (ARCH effects present)

Ljung-Box Test on Squared Returns (m=10):

Q Statistic: 159.4009

p-value: 0.000000

Conclusion: Reject H0 (autocorrelation in squared returns)

============================================================

ARCH Effects Tests for EUR/USD

============================================================

ARCH-LM Test (q=10):

LM Statistic: 136.1443

p-value: 0.000000

Conclusion: Reject H0 (ARCH effects present)

Ljung-Box Test on Squared Returns (m=10):

Q Statistic: 248.1804

p-value: 0.000000

Conclusion: Reject H0 (autocorrelation in squared returns)

============================================================

ARCH Effects Tests for Gold Futures

============================================================

ARCH-LM Test (q=10):

LM Statistic: 135.8857

p-value: 0.000000

Conclusion: Reject H0 (ARCH effects present)

Ljung-Box Test on Squared Returns (m=10):

Q Statistic: 238.5584

p-value: 0.000000

Conclusion: Reject H0 (autocorrelation in squared returns)

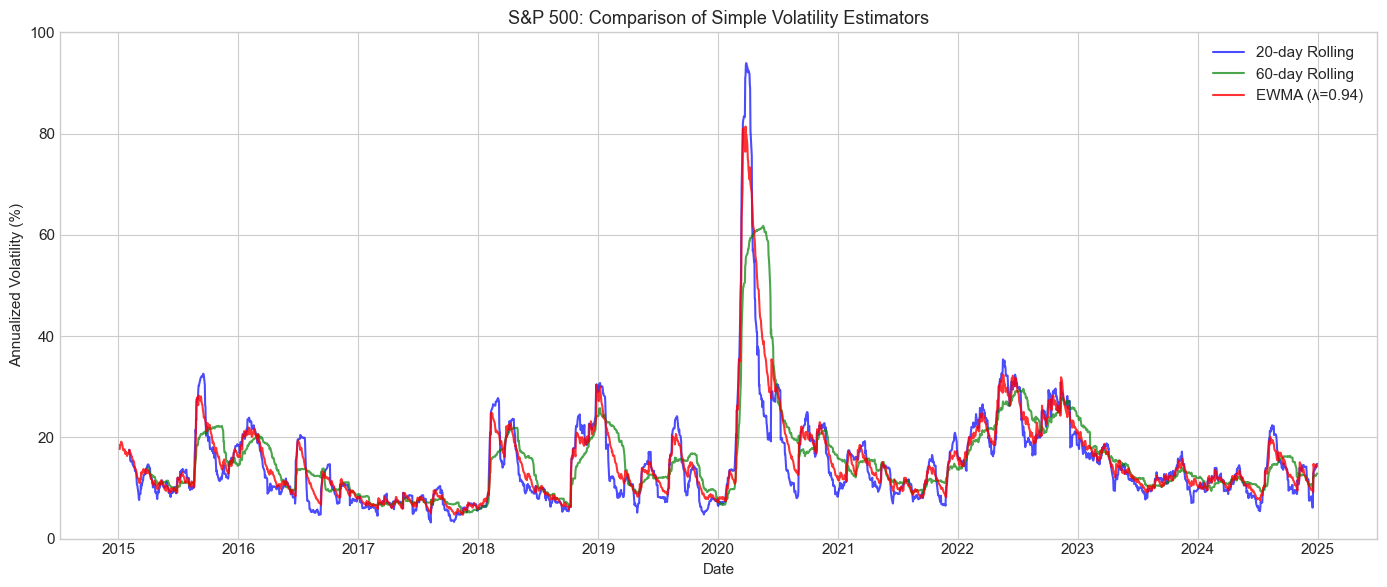

6. Simple Volatility Estimators¶

Before moving to GARCH models, let’s explore simple volatility estimators.

6.1 Rolling Window Volatility¶

The simplest approach: compute standard deviation over a rolling window.

Trade-off: Short windows are noisy; long windows are slow to adapt.

6.2 Exponentially Weighted Moving Average (EWMA)¶

RiskMetrics approach: exponentially declining weights.

where typically (daily) or (monthly).

Equivalent to IGARCH(1,1) without a constant term.

Source

def compute_ewma_volatility(returns, lam=0.94):

"""Compute EWMA volatility (RiskMetrics approach)."""

n = len(returns)

var = np.zeros(n)

# Initialize with sample variance

var[0] = returns.var()

for t in range(1, n):

var[t] = lam * var[t-1] + (1 - lam) * returns.iloc[t-1]**2

return pd.Series(np.sqrt(var), index=returns.index)

# Compare volatility estimators for S&P 500

spy_ret = returns['S&P 500 ETF']

fig, ax = plt.subplots(figsize=(14, 6))

# Rolling windows

for window, color in [(20, 'blue'), (60, 'green')]:

rolling_vol = spy_ret.rolling(window).std() * np.sqrt(252) * 100

ax.plot(rolling_vol.index, rolling_vol.values, label=f'{window}-day Rolling',

color=color, alpha=0.7)

# EWMA

ewma_vol = compute_ewma_volatility(spy_ret, lam=0.94) * np.sqrt(252) * 100

ax.plot(ewma_vol.index, ewma_vol.values, label='EWMA (λ=0.94)',

color='red', alpha=0.8)

ax.set_xlabel('Date')

ax.set_ylabel('Annualized Volatility (%)')

ax.set_title('S&P 500: Comparison of Simple Volatility Estimators', fontsize=13)

ax.legend(loc='upper right')

ax.set_ylim(0, 100)

plt.tight_layout()

plt.show()

7. Summary and Preview¶

Key Takeaways¶

Financial returns violate GBM assumptions: They exhibit heavy tails, volatility clustering, leverage effects, and long memory.

Stylized Facts are universal: These patterns appear across different assets, markets, and time periods.

Volatility is predictable: The autocorrelation in squared returns implies that volatility can be forecasted.

Simple estimators have limitations: Rolling windows and EWMA capture basic dynamics but lack theoretical foundations and statistical optimality.

Course Roadmap¶

| Session | Topic |

|---|---|

| 1 | Foundations and Stylized Facts (today) |

| 2 | ARCH and GARCH Models |

| 3 | Asymmetric GARCH (EGARCH, GJR, TGARCH) |

| 4 | Advanced Univariate Models (FIGARCH, APARCH, Component GARCH) |

| 5 | Realized Volatility and High-Frequency Data |

| 6 | HAR Models and Realized Measures |

| 7 | Stochastic Volatility Models |

| 8 | Rough Volatility |

| 9 | Multivariate Volatility (DCC, BEKK) |

| 10 | Path-Dependent Volatility and Applications |

Exercises¶

Exercise 1: Cryptocurrency Stylized Facts¶

Download data for Ethereum (ETH-USD) and compare its stylized facts to Bitcoin. Do cryptocurrencies exhibit the same patterns as traditional assets?

Exercise 2: Intraday vs Daily¶

Download intraday (hourly) Bitcoin data. How do the stylized facts change at higher frequencies?

Exercise 3: Long Memory Estimation¶

Estimate the fractional differencing parameter for absolute returns using the GPH (Geweke-Porter-Hudak) estimator. What values do you find?

Exercise 4: Rolling Skewness and Kurtosis¶

Compute 252-day rolling skewness and kurtosis for S&P 500 returns. How stable are these higher moments over time?

Exercise 5: EWMA Sensitivity¶

Investigate how EWMA volatility estimates change for different values of λ (0.90, 0.94, 0.97, 0.99). Which value best captures the COVID-19 volatility spike?

References¶

Cont, R. (2001). Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance, 1(2), 223-236.

Bollerslev, T., Engle, R. F., & Nelson, D. B. (1994). ARCH models. Handbook of Econometrics, 4, 2959-3038.

Black, F. (1976). Studies of stock price volatility changes. Proceedings of the 1976 Meetings of the American Statistical Association, 177-181.

JP Morgan/Reuters. (1996). RiskMetrics Technical Document.

Taylor, S. J. (2008). Modelling Financial Time Series. World Scientific.