Session 10: Path-Dependent Volatility and Applications

Course: Advanced Volatility Modeling¶

Learning Objectives¶

Understand path-dependent volatility dynamics

Implement volatility targeting and risk parity strategies

Apply volatility models to VaR and Expected Shortfall

Explore volatility in option pricing and the VIX

1. Path-Dependent Volatility¶

1.1 What is Path Dependence?¶

Volatility depends not just on the current state but on the path of past returns:

GARCH: depends on

HAR: Uses daily, weekly, monthly averages of RV

Regime switching: Volatility depends on current regime and transition history

1.2 Signature of Path Dependence¶

At-the-money implied volatility responds to:

Recent realized volatility

Recent returns (leverage effect)

Time since last volatility spike

Source

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from scipy import stats

from arch import arch_model

import yfinance as yf

import warnings

warnings.filterwarnings('ignore')

plt.style.use('seaborn-v0_8-whitegrid')

plt.rcParams['figure.figsize'] = (12, 6)

np.random.seed(42)Source

# Download data

spy = yf.download('SPY', start='2010-01-01', end='2024-12-31', progress=False)

vix = yf.download('^VIX', start='2010-01-01', end='2024-12-31', progress=False)

if isinstance(spy.columns, pd.MultiIndex):

spy.columns = spy.columns.get_level_values(0)

vix.columns = vix.columns.get_level_values(0)

data = pd.DataFrame({

'price': spy['Close'],

'vix': vix['Close']

}).dropna()

data['returns'] = np.log(data['price'] / data['price'].shift(1)) * 100

data['rv_20'] = data['returns'].rolling(20).std() * np.sqrt(252) # Annualized

data = data.dropna()

print(f"Sample: {data.index[0].date()} to {data.index[-1].date()}")YF.download() has changed argument auto_adjust default to True

Sample: 2010-02-02 to 2024-12-30

2. Volatility Targeting¶

2.1 Concept¶

Adjust portfolio exposure inversely to volatility:

where is the target volatility.

2.2 Benefits¶

Constant risk contribution

Reduced drawdowns during crises

More stable Sharpe ratio

Source

def volatility_targeting_strategy(returns, vol_forecast, target_vol=10, max_leverage=2):

"""

Implement volatility targeting strategy.

Parameters

----------

returns : Series

Asset returns

vol_forecast : Series

Volatility forecast (annualized %)

target_vol : float

Target volatility (%)

max_leverage : float

Maximum leverage allowed

"""

# Compute weights

weights = target_vol / vol_forecast

weights = weights.clip(0, max_leverage) # Cap leverage

# Lag weights by 1 day (use yesterday's forecast for today's position)

weights = weights.shift(1)

# Strategy returns

strat_returns = weights * returns

return strat_returns, weights

# Fit GARCH for volatility forecast

garch = arch_model(data['returns'], vol='Garch', p=1, q=1)

garch_fit = garch.fit(disp='off')

vol_forecast = garch_fit.conditional_volatility * np.sqrt(252) # Annualize

# Run strategy

target_vol = 10 # 10% target

strat_returns, weights = volatility_targeting_strategy(

data['returns'], vol_forecast, target_vol=target_vol

)

# Compare

results = pd.DataFrame({

'Buy & Hold': data['returns'],

'Vol Target': strat_returns,

'Weight': weights

}).dropna()

# Cumulative returns

cum_bh = (1 + results['Buy & Hold']/100).cumprod()

cum_vt = (1 + results['Vol Target']/100).cumprod()

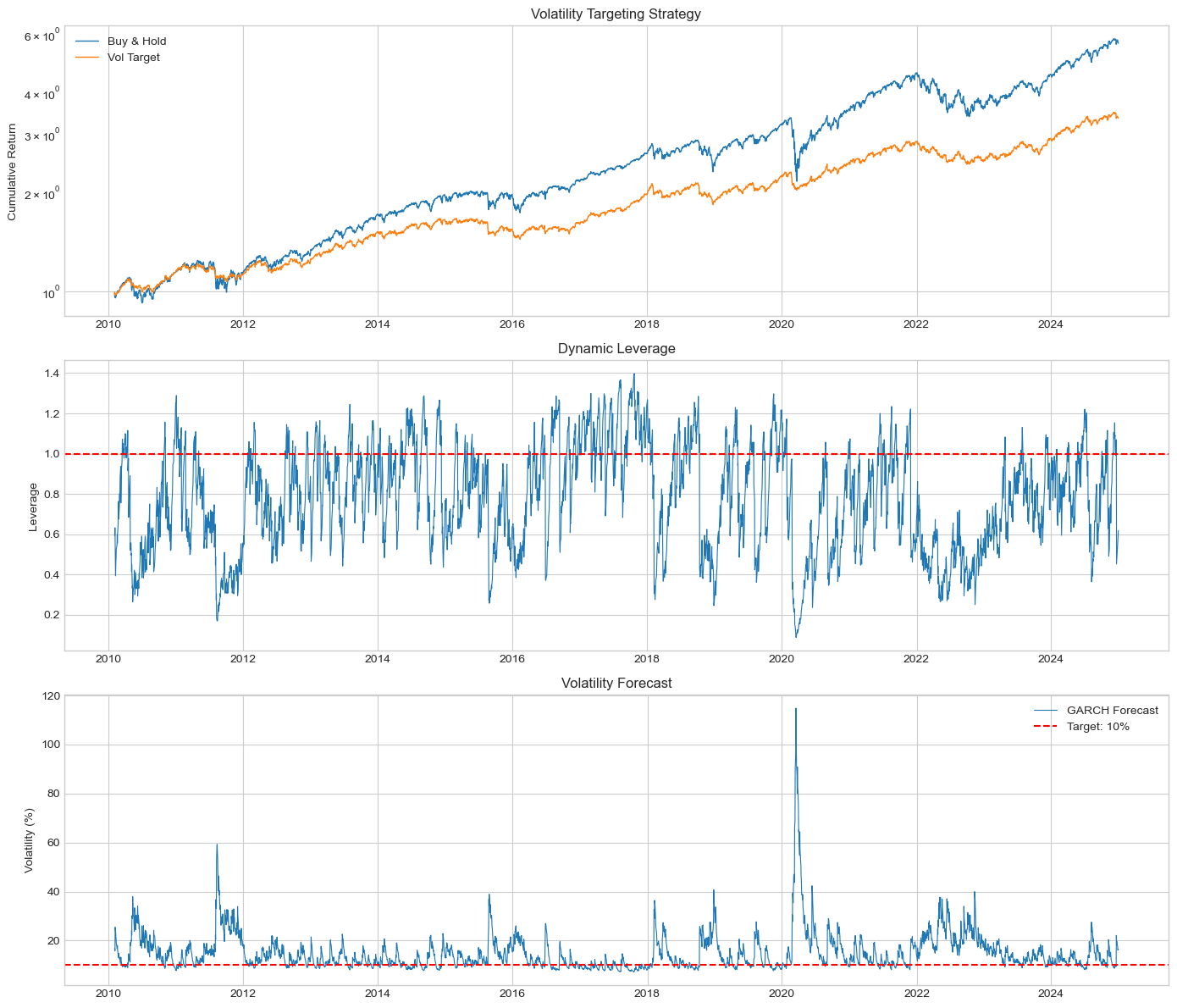

fig, axes = plt.subplots(3, 1, figsize=(14, 12))

axes[0].plot(cum_bh.index, cum_bh, label='Buy & Hold', linewidth=1)

axes[0].plot(cum_vt.index, cum_vt, label='Vol Target', linewidth=1)

axes[0].set_ylabel('Cumulative Return')

axes[0].set_title('Volatility Targeting Strategy')

axes[0].legend()

axes[0].set_yscale('log')

axes[1].plot(results['Weight'].index, results['Weight'], linewidth=0.8)

axes[1].axhline(1, color='red', linestyle='--')

axes[1].set_ylabel('Leverage')

axes[1].set_title('Dynamic Leverage')

axes[2].plot(vol_forecast.index, vol_forecast, label='GARCH Forecast', linewidth=0.8)

axes[2].axhline(target_vol, color='red', linestyle='--', label=f'Target: {target_vol}%')

axes[2].set_ylabel('Volatility (%)')

axes[2].set_title('Volatility Forecast')

axes[2].legend()

plt.tight_layout()

plt.show()

# Performance metrics

def performance_metrics(returns):

ann_ret = returns.mean() * 252

ann_vol = returns.std() * np.sqrt(252)

sharpe = ann_ret / ann_vol

max_dd = (returns.cumsum() - returns.cumsum().cummax()).min()

return ann_ret, ann_vol, sharpe, max_dd

print("\nPerformance Comparison")

print("="*60)

print(f"{'Metric':<20} {'Buy & Hold':>15} {'Vol Target':>15}")

print("-"*60)

bh_metrics = performance_metrics(results['Buy & Hold'])

vt_metrics = performance_metrics(results['Vol Target'])

for metric, bh, vt in zip(['Ann. Return (%)', 'Ann. Volatility (%)', 'Sharpe Ratio', 'Max Drawdown (%)'],

bh_metrics, vt_metrics):

print(f"{metric:<20} {bh:>15.2f} {vt:>15.2f}")

Performance Comparison

============================================================

Metric Buy & Hold Vol Target

------------------------------------------------------------

Ann. Return (%) 13.09 8.63

Ann. Volatility (%) 17.10 10.09

Sharpe Ratio 0.77 0.85

Max Drawdown (%) -41.12 -15.53

3. Value at Risk (VaR) and Expected Shortfall¶

3.1 Definitions¶

Value at Risk at confidence level :

Expected Shortfall (Conditional VaR):

Source

def garch_var_es(returns, alpha=0.01, window=500):

"""

Compute rolling VaR and ES using GARCH.

"""

n = len(returns)

var_list = []

es_list = []

dates = []

for t in range(window, n):

train = returns.iloc[t-window:t]

try:

model = arch_model(train, vol='Garch', p=1, q=1, dist='t')

fit = model.fit(disp='off', show_warning=False)

# 1-day forecast

forecast = fit.forecast(horizon=1, reindex=False)

vol_forecast = np.sqrt(forecast.variance.iloc[-1, 0])

# Degrees of freedom

nu = fit.params.get('nu', 8)

# VaR (Student-t)

var_t = -stats.t.ppf(alpha, nu) * vol_forecast * np.sqrt((nu-2)/nu)

# ES (Student-t)

t_alpha = stats.t.ppf(alpha, nu)

es_t = vol_forecast * np.sqrt((nu-2)/nu) * (

stats.t.pdf(t_alpha, nu) / alpha * (nu + t_alpha**2) / (nu - 1)

)

var_list.append(var_t)

es_list.append(es_t)

dates.append(returns.index[t])

except:

continue

return pd.DataFrame({'VaR': var_list, 'ES': es_list}, index=dates)

# Compute rolling VaR/ES

risk_measures = garch_var_es(data['returns'], alpha=0.01, window=500)

# Align returns

returns_aligned = data['returns'].loc[risk_measures.index]

# Count violations

violations = (returns_aligned < -risk_measures['VaR']).sum()

violation_rate = violations / len(risk_measures) * 100

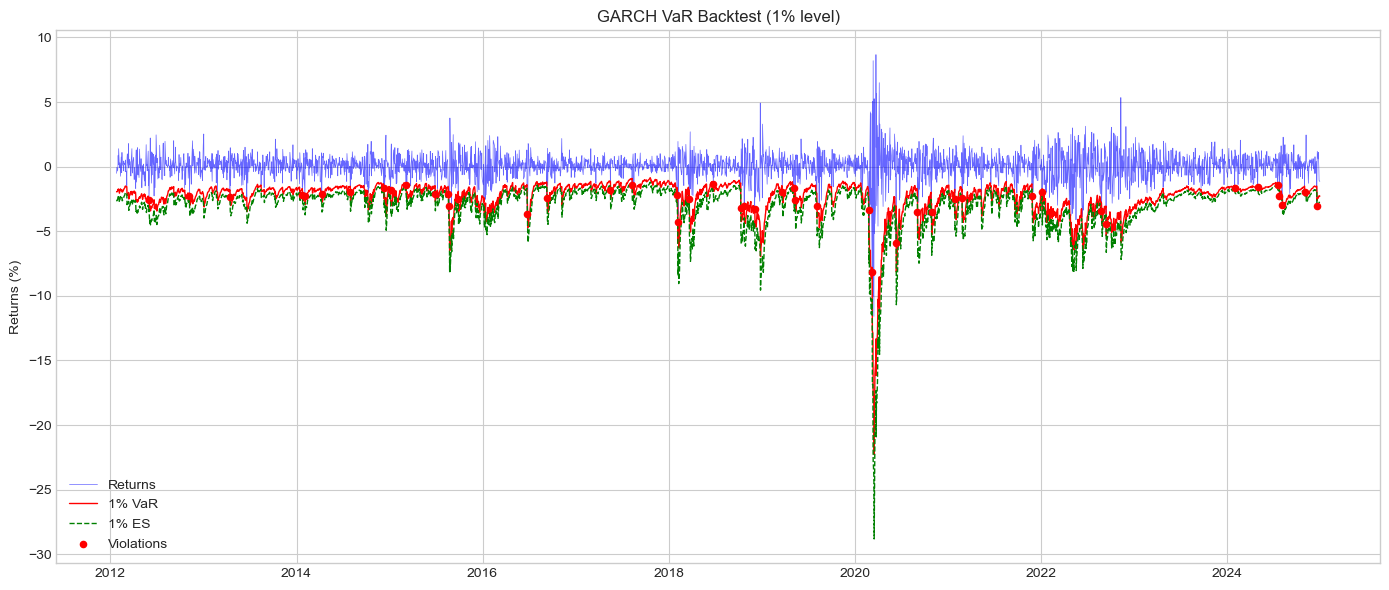

print(f"VaR Backtest (1% level)")

print(f"="*40)

print(f"Expected violations: 1.00%")

print(f"Actual violations: {violation_rate:.2f}%")

print(f"Number of violations: {violations} / {len(risk_measures)}")VaR Backtest (1% level)

========================================

Expected violations: 1.00%

Actual violations: 1.44%

Number of violations: 47 / 3253

Source

# Plot VaR backtest

fig, ax = plt.subplots(figsize=(14, 6))

ax.plot(returns_aligned.index, returns_aligned, 'b-', linewidth=0.5, alpha=0.6, label='Returns')

ax.plot(risk_measures.index, -risk_measures['VaR'], 'r-', linewidth=1, label='1% VaR')

ax.plot(risk_measures.index, -risk_measures['ES'], 'g--', linewidth=1, label='1% ES')

# Mark violations

violations_mask = returns_aligned < -risk_measures['VaR']

ax.scatter(returns_aligned[violations_mask].index,

returns_aligned[violations_mask],

color='red', s=20, zorder=5, label='Violations')

ax.set_ylabel('Returns (%)')

ax.set_title('GARCH VaR Backtest (1% level)')

ax.legend(loc='lower left')

plt.tight_layout()

plt.show()

4. VIX and Implied Volatility¶

4.1 VIX Index¶

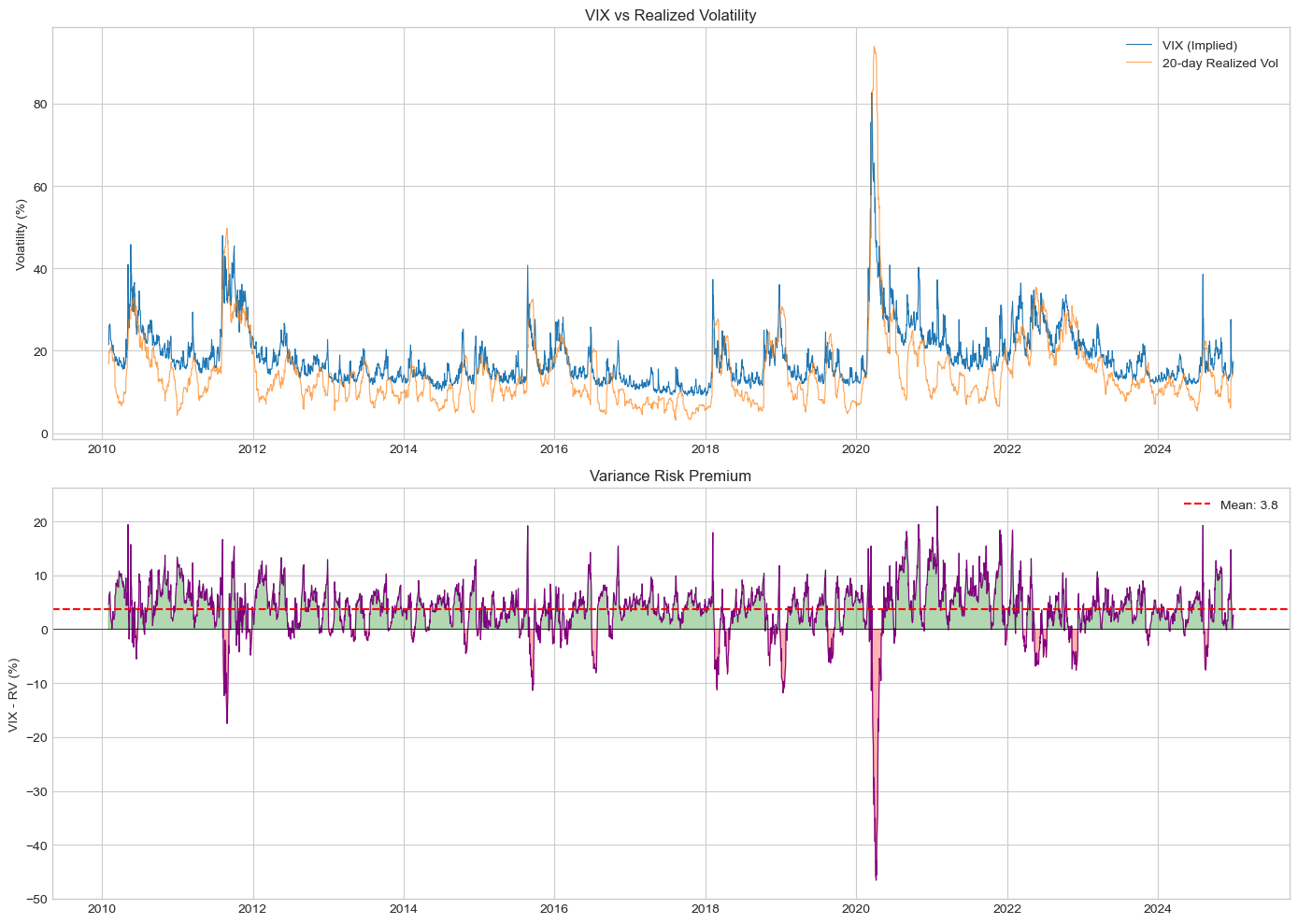

The VIX measures 30-day implied volatility from S&P 500 options:

4.2 VIX-Realized Volatility Spread¶

The Variance Risk Premium (VRP):

On average, VRP > 0: Investors pay a premium for volatility protection.

Source

# VIX vs Realized Volatility

data['rv_30_fwd'] = data['returns'].rolling(22).std().shift(-22) * np.sqrt(252)

fig, axes = plt.subplots(2, 1, figsize=(14, 10))

# Time series

axes[0].plot(data.index, data['vix'], label='VIX (Implied)', linewidth=0.8)

axes[0].plot(data.index, data['rv_20'], label='20-day Realized Vol', linewidth=0.8, alpha=0.7)

axes[0].set_ylabel('Volatility (%)')

axes[0].set_title('VIX vs Realized Volatility')

axes[0].legend()

# Variance Risk Premium

vrp = data['vix'] - data['rv_20']

axes[1].plot(vrp.index, vrp, linewidth=0.8, color='purple')

axes[1].axhline(vrp.mean(), color='red', linestyle='--', label=f'Mean: {vrp.mean():.1f}')

axes[1].axhline(0, color='black', linewidth=0.5)

axes[1].fill_between(vrp.index, 0, vrp, where=vrp>0, alpha=0.3, color='green')

axes[1].fill_between(vrp.index, 0, vrp, where=vrp<0, alpha=0.3, color='red')

axes[1].set_ylabel('VIX - RV (%)')

axes[1].set_title('Variance Risk Premium')

axes[1].legend()

plt.tight_layout()

plt.show()

print(f"\nVariance Risk Premium Statistics:")

print(f"Mean: {vrp.mean():.2f}%")

print(f"% Positive: {(vrp > 0).mean()*100:.1f}%")

print(f"\nOn average, VIX exceeds realized vol by {vrp.mean():.1f} percentage points.")

Variance Risk Premium Statistics:

Mean: 3.76%

% Positive: 85.3%

On average, VIX exceeds realized vol by 3.8 percentage points.

5. Volatility Trading Strategies¶

5.1 Sell Volatility (Variance Swap)¶

Profit from VRP by selling variance:

Short VIX futures / options

Short variance swaps

Short straddles

Source

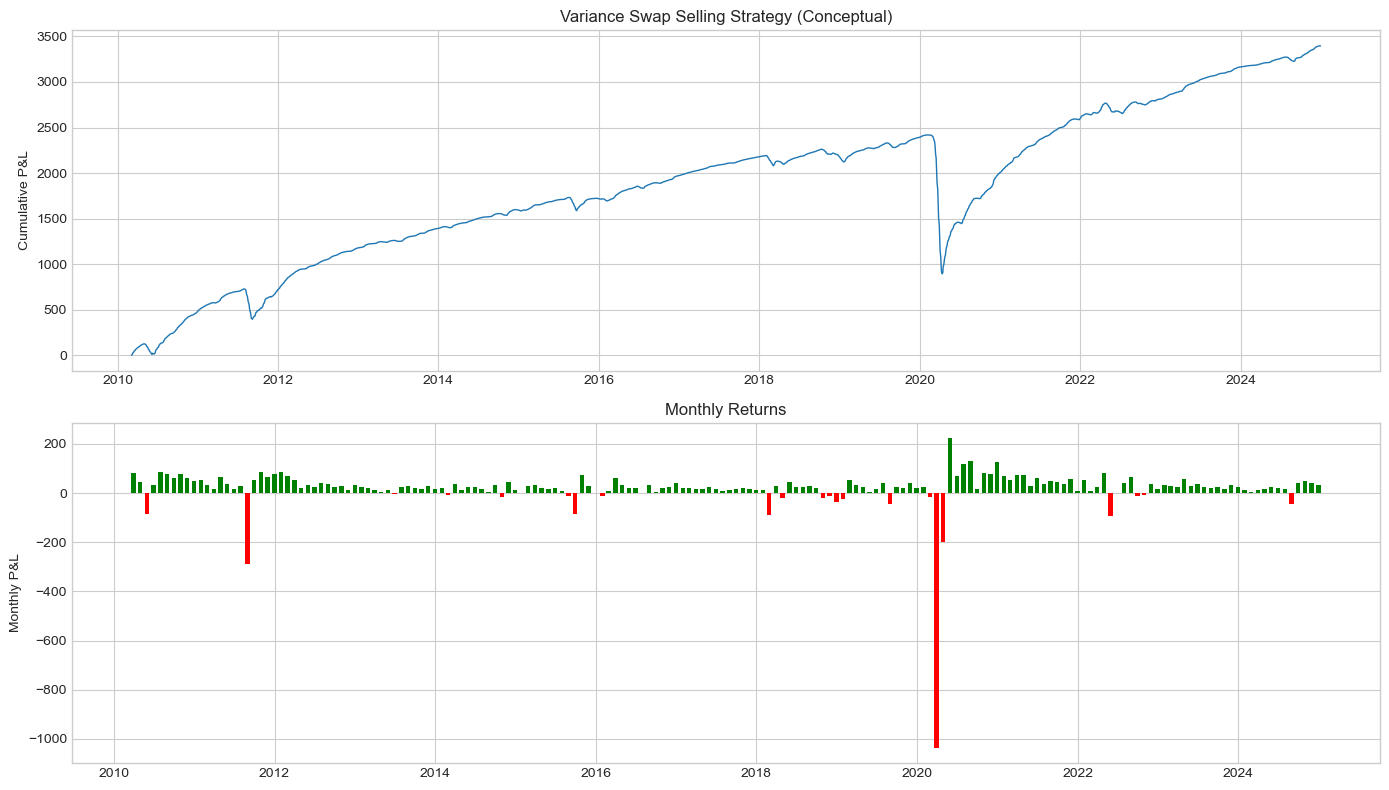

# Simple variance selling strategy (conceptual)

# P&L ≈ VIX² - RV² (for variance swap)

data['vix_lag'] = data['vix'].shift(22) # Entry VIX

data['variance_swap_pnl'] = (data['vix_lag']**2 - data['rv_20']**2) / 100 # Scaled

var_swap_returns = data['variance_swap_pnl'].dropna()

fig, axes = plt.subplots(2, 1, figsize=(14, 8))

# Cumulative P&L

axes[0].plot(var_swap_returns.index, var_swap_returns.cumsum(), linewidth=1)

axes[0].set_ylabel('Cumulative P&L')

axes[0].set_title('Variance Swap Selling Strategy (Conceptual)')

# Monthly returns

monthly_pnl = var_swap_returns.resample('M').sum()

axes[1].bar(monthly_pnl.index, monthly_pnl.values, width=20,

color=['green' if x > 0 else 'red' for x in monthly_pnl.values])

axes[1].set_ylabel('Monthly P&L')

axes[1].set_title('Monthly Returns')

plt.tight_layout()

plt.show()

print("\nVariance Selling Strategy:")

print(f"Win rate: {(var_swap_returns > 0).mean()*100:.1f}%")

print(f"Average daily P&L: {var_swap_returns.mean():.4f}")

print(f"Sharpe ratio: {var_swap_returns.mean() / var_swap_returns.std() * np.sqrt(252):.2f}")

Variance Selling Strategy:

Win rate: 82.8%

Average daily P&L: 0.9099

Sharpe ratio: 2.43

6. Course Summary¶

Key Models Covered¶

| Session | Topic | Key Models |

|---|---|---|

| 1 | Foundations | Stylized facts, simple estimators |

| 2 | GARCH | ARCH, GARCH, IGARCH |

| 3 | Asymmetric | GJR-GARCH, EGARCH, TGARCH |

| 4 | Advanced | FIGARCH, APARCH, Component |

| 5 | Realized | RV, BV, TSRV, Realized Kernel |

| 6 | HAR | HAR-RV, HAR-CJ, HAR-RS |

| 7 | Stochastic | SV, Heston |

| 8 | Rough | fBM, Rough Bergomi |

| 9 | Multivariate | DCC, BEKK |

| 10 | Applications | Vol targeting, VaR, VRP |

Final Exercises¶

Comprehensive Project: Build a complete volatility forecasting system that:

Compares GARCH, HAR, and rough volatility models

Evaluates forecasts using multiple metrics

Applies to portfolio risk management

Cryptocurrency Volatility: Apply all course methods to Bitcoin/Ethereum and document differences from equities

Option Pricing: Implement and compare option prices from Heston vs rough Bergomi

VIX Trading: Design and backtest a VIX-based trading strategy using HAR forecasts

Multivariate Risk: Build a DCC-based risk system for a multi-asset portfolio

References (Course-Wide)¶

Textbooks¶

Tsay, R. S. (2010). Analysis of Financial Time Series. Wiley.

Francq, C., & Zakoian, J. M. (2019). GARCH Models. Wiley.

Gatheral, J. (2006). The Volatility Surface. Wiley.

Key Papers¶

Bollerslev (1986) - GARCH

Nelson (1991) - EGARCH

Engle (2002) - DCC

Corsi (2009) - HAR

Gatheral et al. (2018) - Rough Volatility

Software¶

Python:

arch,statsmodels,scipyR:

rugarch,rmgarch