Session 1: Foundations of Event Studies

Event Studies in Finance and Economics - Summer School¶

Learning Objectives¶

By the end of this session, you will be able to:

Explain the economic logic underlying event study methodology

Identify the key components of an event study design

Distinguish between different types of corporate and economic events

Implement a basic event study for a single firm and event

Interpret abnormal returns in economic terms

1. Introduction: What is an Event Study?¶

An event study is an empirical methodology used to assess the impact of a specific event on the value of a firm (or more generally, on asset prices). The fundamental premise is elegantly simple: if markets are efficient, the impact of an event will be reflected immediately in asset prices.

The Core Insight¶

Consider a firm that announces unexpected positive earnings. Under the efficient market hypothesis, this new information should be rapidly incorporated into the stock price. The event study methodology allows us to:

Isolate the price change attributable to the specific event

Quantify the economic magnitude of the event’s impact

Test hypotheses about how markets process information

Why Event Studies Matter¶

Event studies serve multiple purposes in financial economics:

Market Efficiency Tests: Do prices adjust quickly and correctly to new information?

Corporate Finance: What is the wealth effect of corporate decisions (M&A, dividends, capital structure)?

Policy Analysis: How do regulatory changes or policy announcements affect asset values?

Legal Applications: Quantifying damages in securities litigation

2. Historical Development¶

The Pioneering Studies¶

The event study methodology emerged from two seminal papers in the late 1960s:

Ball and Brown (1968) - “An Empirical Evaluation of Accounting Income Numbers”

Examined whether accounting earnings convey useful information to investors

Found that stock prices adjust in the direction of earnings surprises

Demonstrated that most adjustment occurs before the announcement (anticipation)

Fama, Fisher, Jensen, and Roll (1969) - “The Adjustment of Stock Prices to New Information”

Studied stock splits and their information content

Introduced the market model for estimating normal returns

Established the template that most subsequent event studies follow

Evolution of the Methodology¶

| Decade | Key Developments |

|---|---|

| 1970s | Standardization of methodology; focus on market efficiency |

| 1980s | Refinements in statistical testing (Patell, Brown-Warner) |

| 1990s | Long-horizon event studies; concerns about specification |

| 2000s | Cross-sectional analysis; robust inference methods |

| 2010s+ | High-frequency studies; machine learning applications |

3. The Anatomy of an Event Study¶

Timeline Structure¶

Every event study involves a carefully defined timeline:

Estimation Window Event Window Post-Event Window

|------------------------| |----------| |----------------|

T₀ T₁ τ₁ τ τ₂ T₂ T₃

|<----- L₁ days ------->| |<-- L₂ -->| |<---- L₃ ----->|Where:

τ = Event date (day 0)

Estimation window [T₀, T₁]: Used to estimate the “normal” relationship between stock and market returns

Event window [τ₁, τ₂]: Period over which we measure the event’s impact (often [-1, +1] or [-5, +5])

Post-event window [T₂, T₃]: Optional; used for long-horizon studies

Key Design Choices¶

Event Definition: What constitutes the event? When exactly did it occur?

Event Window Length: Should we look at just day 0, or include surrounding days?

Estimation Window Length: Typically 120-250 trading days

Gap Between Windows: Often a small gap is left to prevent event contamination

4. The Mathematical Framework¶

Defining Abnormal Returns¶

The abnormal return is the difference between the actual return and the “normal” (expected) return:

Where:

= Abnormal return of firm on day

= Actual return of firm on day

= Expected (normal) return given conditioning information

The Market Model¶

The most common model for normal returns is the market model:

Where:

= Return on the market portfolio

= Firm-specific parameters estimated from the estimation window

The expected return during the event window is then:

And the abnormal return:

Cumulative Abnormal Returns (CAR)¶

To capture the total effect over an event window, we sum abnormal returns:

For example, captures the cumulative abnormal return from one day before to one day after the event.

Aggregating Across Firms¶

For a sample of events, the average abnormal return is:

And the cumulative average abnormal return:

5. Types of Events¶

Firm-Specific Events¶

| Category | Examples |

|---|---|

| Earnings | Quarterly announcements, earnings surprises, guidance |

| Corporate Actions | Stock splits, dividends, share repurchases |

| M&A | Merger announcements, tender offers, hostile bids |

| Financing | Equity issuance, debt offerings, credit rating changes |

| Governance | CEO changes, board appointments, activist involvement |

| Legal/Regulatory | Lawsuits, FDA approvals, patent grants |

Market-Wide Events¶

| Category | Examples |

|---|---|

| Monetary Policy | Interest rate decisions, QE announcements |

| Fiscal Policy | Tax changes, stimulus packages |

| Regulation | New rules, deregulation, sanctions |

| Political | Elections, referendums, geopolitical events |

| Macroeconomic | Employment reports, GDP releases, inflation data |

Anticipated vs. Unanticipated Events¶

A crucial distinction:

Anticipated events (e.g., scheduled earnings announcements): Markets may partially price in expectations before the event

Unanticipated events (e.g., sudden CEO death): Full impact should occur at announcement

For anticipated events, the abnormal return reflects the surprise component only.

6. Practical Implementation¶

Let’s now implement a basic event study step by step. We’ll analyze Apple’s stock response to its iPhone 15 announcement in September 2023.

Source

# Import required libraries

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

from scipy import stats

import yfinance as yf

from datetime import datetime, timedelta

import warnings

warnings.filterwarnings('ignore')

# Set plotting style

plt.style.use('seaborn-v0_8-whitegrid')

sns.set_palette("husl")

print("Libraries loaded successfully!")Libraries loaded successfully!

Step 1: Define the Event and Parameters¶

Source

# Event Study Parameters

TICKER = 'AAPL' # Apple Inc.

MARKET_INDEX = '^GSPC' # S&P 500 as market proxy

EVENT_DATE = '2023-09-12' # iPhone 15 announcement date

# Window specifications (in trading days)

ESTIMATION_WINDOW = 120 # Days in estimation window

GAP = 10 # Gap between estimation and event window

EVENT_WINDOW_PRE = 5 # Days before event

EVENT_WINDOW_POST = 5 # Days after event

print(f"Event Study Configuration:")

print(f" Stock: {TICKER}")

print(f" Market Index: {MARKET_INDEX}")

print(f" Event Date: {EVENT_DATE}")

print(f" Estimation Window: {ESTIMATION_WINDOW} trading days")

print(f" Event Window: [{-EVENT_WINDOW_PRE}, +{EVENT_WINDOW_POST}]")Event Study Configuration:

Stock: AAPL

Market Index: ^GSPC

Event Date: 2023-09-12

Estimation Window: 120 trading days

Event Window: [-5, +5]

Step 2: Download Price Data¶

Source

def download_data(ticker, market, event_date, est_window, gap, pre, post):

"""

Download stock and market data for event study.

Parameters:

-----------

ticker : str

Stock ticker symbol

market : str

Market index ticker

event_date : str

Event date in 'YYYY-MM-DD' format

est_window : int

Length of estimation window in trading days

gap : int

Gap between estimation and event window

pre : int

Days before event in event window

post : int

Days after event in event window

Returns:

--------

pd.DataFrame with columns ['stock_ret', 'market_ret', 'event_time']

"""

# Calculate date range (add buffer for weekends/holidays)

event_dt = pd.to_datetime(event_date)

start_date = event_dt - timedelta(days=int((est_window + gap + pre) * 1.5))

end_date = event_dt + timedelta(days=int(post * 2))

# Download data

stock_data = yf.download(ticker, start=start_date, end=end_date, progress=False)

market_data = yf.download(market, start=start_date, end=end_date, progress=False)

# Calculate returns

df = pd.DataFrame({

'stock_price': stock_data['Close'].squeeze(),

'market_price': market_data['Close'].squeeze()

})

df['stock_ret'] = df['stock_price'].pct_change()

df['market_ret'] = df['market_price'].pct_change()

df = df.dropna()

# Find event date in the data (might be adjusted if not a trading day)

if event_dt not in df.index:

# Find nearest trading day

idx = df.index.get_indexer([event_dt], method='nearest')[0]

event_dt = df.index[idx]

print(f" Note: Event date adjusted to nearest trading day: {event_dt.date()}")

# Create event time index

event_idx = df.index.get_loc(event_dt)

df['event_time'] = range(-event_idx, len(df) - event_idx)

return df, event_dt

# Download data

data, actual_event_date = download_data(

TICKER, MARKET_INDEX, EVENT_DATE,

ESTIMATION_WINDOW, GAP, EVENT_WINDOW_PRE, EVENT_WINDOW_POST

)

print(f"\nData downloaded: {len(data)} trading days")

print(f"Date range: {data.index[0].date()} to {data.index[-1].date()}")

data.head()YF.download() has changed argument auto_adjust default to True

Data downloaded: 146 trading days

Date range: 2023-02-23 to 2023-09-21

Step 3: Define Windows¶

Source

def define_windows(df, est_window, gap, pre, post):

"""

Split data into estimation and event windows.

Returns:

--------

estimation_data, event_data : pd.DataFrame

"""

# Estimation window: ends 'gap' days before event window starts

est_end = -(gap + pre)

est_start = est_end - est_window

# Event window

evt_start = -pre

evt_end = post

estimation_data = df[(df['event_time'] >= est_start) & (df['event_time'] < est_end)].copy()

event_data = df[(df['event_time'] >= evt_start) & (df['event_time'] <= evt_end)].copy()

print(f"Estimation Window:")

print(f" Event time: [{est_start}, {est_end})")

print(f" Dates: {estimation_data.index[0].date()} to {estimation_data.index[-1].date()}")

print(f" Observations: {len(estimation_data)}")

print(f"\nEvent Window:")

print(f" Event time: [{evt_start}, {evt_end}]")

print(f" Dates: {event_data.index[0].date()} to {event_data.index[-1].date()}")

print(f" Observations: {len(event_data)}")

return estimation_data, event_data

estimation_data, event_data = define_windows(

data, ESTIMATION_WINDOW, GAP, EVENT_WINDOW_PRE, EVENT_WINDOW_POST

)Estimation Window:

Event time: [-135, -15)

Dates: 2023-02-28 to 2023-08-18

Observations: 120

Event Window:

Event time: [-5, 5]

Dates: 2023-09-05 to 2023-09-19

Observations: 11

Step 4: Estimate the Market Model¶

Source

def estimate_market_model(estimation_data):

"""

Estimate market model parameters using OLS.

R_i,t = alpha + beta * R_m,t + epsilon_t

Returns:

--------

dict with 'alpha', 'beta', 'sigma', 'r_squared'

"""

y = estimation_data['stock_ret'].values

x = estimation_data['market_ret'].values

# Add constant for alpha

X = np.column_stack([np.ones(len(x)), x])

# OLS estimation

beta_hat = np.linalg.lstsq(X, y, rcond=None)[0]

alpha = beta_hat[0]

beta = beta_hat[1]

# Residuals and standard error

y_pred = alpha + beta * x

residuals = y - y_pred

sigma = np.std(residuals, ddof=2) # Adjust for 2 parameters

# R-squared

ss_res = np.sum(residuals**2)

ss_tot = np.sum((y - np.mean(y))**2)

r_squared = 1 - ss_res / ss_tot

return {

'alpha': alpha,

'beta': beta,

'sigma': sigma,

'r_squared': r_squared,

'residuals': residuals

}

# Estimate model

model = estimate_market_model(estimation_data)

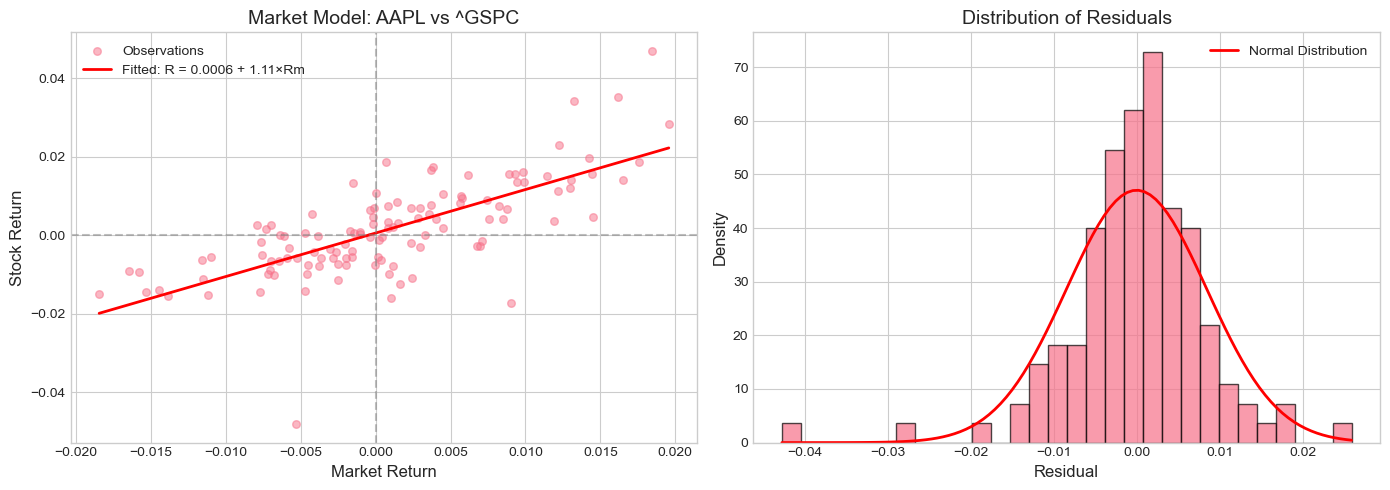

print("Market Model Estimation Results:")

print(f" α (alpha) = {model['alpha']:.6f}")

print(f" β (beta) = {model['beta']:.4f}")

print(f" σ (sigma) = {model['sigma']:.6f}")

print(f" R² = {model['r_squared']:.4f}")

print(f"\nInterpretation:")

print(f" - Beta of {model['beta']:.2f} indicates the stock is ", end="")

if model['beta'] > 1:

print(f"more volatile than the market")

elif model['beta'] < 1:

print(f"less volatile than the market")

else:

print(f"as volatile as the market")Market Model Estimation Results:

α (alpha) = 0.000582

β (beta) = 1.1072

σ (sigma) = 0.008476

R² = 0.5215

Interpretation:

- Beta of 1.11 indicates the stock is more volatile than the market

Source

# Visualize the market model fit

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

# Scatter plot with regression line

ax1 = axes[0]

ax1.scatter(estimation_data['market_ret'], estimation_data['stock_ret'],

alpha=0.5, s=30, label='Observations')

x_line = np.linspace(estimation_data['market_ret'].min(), estimation_data['market_ret'].max(), 100)

y_line = model['alpha'] + model['beta'] * x_line

ax1.plot(x_line, y_line, 'r-', linewidth=2, label=f'Fitted: R = {model["alpha"]:.4f} + {model["beta"]:.2f}×Rm')

ax1.axhline(y=0, color='gray', linestyle='--', alpha=0.5)

ax1.axvline(x=0, color='gray', linestyle='--', alpha=0.5)

ax1.set_xlabel('Market Return', fontsize=12)

ax1.set_ylabel('Stock Return', fontsize=12)

ax1.set_title(f'Market Model: {TICKER} vs {MARKET_INDEX}', fontsize=14)

ax1.legend()

# Residual distribution

ax2 = axes[1]

ax2.hist(model['residuals'], bins=30, density=True, alpha=0.7, edgecolor='black')

# Overlay normal distribution

x_norm = np.linspace(model['residuals'].min(), model['residuals'].max(), 100)

y_norm = stats.norm.pdf(x_norm, 0, model['sigma'])

ax2.plot(x_norm, y_norm, 'r-', linewidth=2, label='Normal Distribution')

ax2.set_xlabel('Residual', fontsize=12)

ax2.set_ylabel('Density', fontsize=12)

ax2.set_title('Distribution of Residuals', fontsize=14)

ax2.legend()

plt.tight_layout()

plt.show()

Step 5: Calculate Abnormal Returns¶

Source

def calculate_abnormal_returns(event_data, model):

"""

Calculate abnormal returns during the event window.

AR_t = R_t - (alpha + beta * R_m,t)

Returns:

--------

pd.DataFrame with abnormal returns and related statistics

"""

result = event_data.copy()

# Expected (normal) returns

result['expected_ret'] = model['alpha'] + model['beta'] * result['market_ret']

# Abnormal returns

result['AR'] = result['stock_ret'] - result['expected_ret']

# Cumulative abnormal return (from start of event window)

result['CAR'] = result['AR'].cumsum()

return result

# Calculate abnormal returns

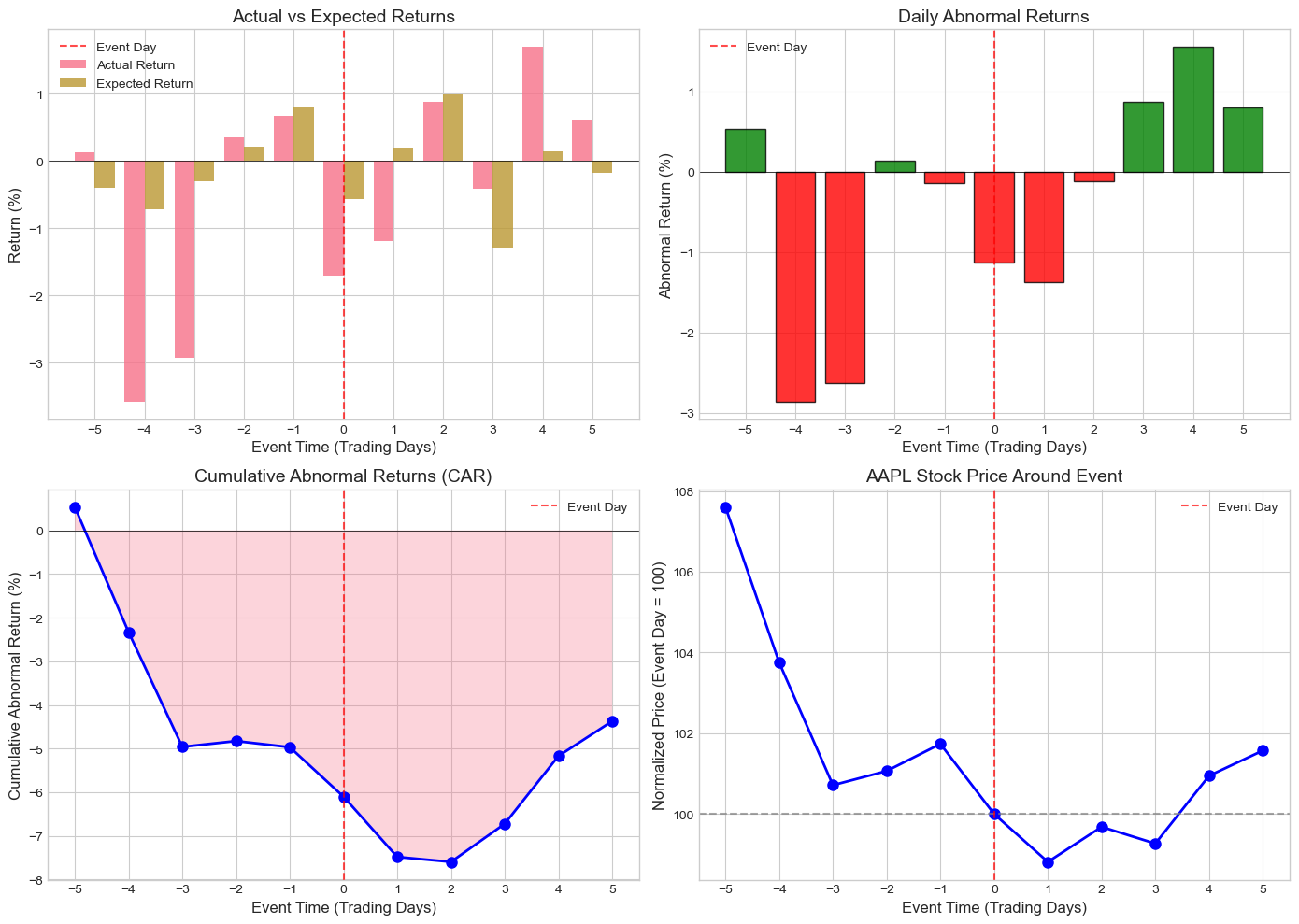

event_results = calculate_abnormal_returns(event_data, model)

# Display results

display_cols = ['event_time', 'stock_ret', 'market_ret', 'expected_ret', 'AR', 'CAR']

print("Event Window Results:")

print("="*80)

event_results_display = event_results[display_cols].copy()

event_results_display.index = event_results_display.index.strftime('%Y-%m-%d')

# Format as percentages

for col in ['stock_ret', 'market_ret', 'expected_ret', 'AR', 'CAR']:

event_results_display[col] = event_results_display[col].apply(lambda x: f"{x*100:.2f}%")

print(event_results_display.to_string())Event Window Results:

================================================================================

event_time stock_ret market_ret expected_ret AR CAR

Date

2023-09-05 -5 0.13% -0.42% -0.41% 0.53% 0.53%

2023-09-06 -4 -3.58% -0.70% -0.71% -2.87% -2.33%

2023-09-07 -3 -2.92% -0.32% -0.30% -2.63% -4.96%

2023-09-08 -2 0.35% 0.14% 0.22% 0.13% -4.83%

2023-09-11 -1 0.66% 0.67% 0.80% -0.14% -4.97%

2023-09-12 0 -1.71% -0.57% -0.57% -1.13% -6.10%

2023-09-13 1 -1.19% 0.12% 0.20% -1.38% -7.48%

2023-09-14 2 0.88% 0.84% 0.99% -0.11% -7.60%

2023-09-15 3 -0.42% -1.22% -1.29% 0.87% -6.72%

2023-09-18 4 1.69% 0.07% 0.14% 1.55% -5.17%

2023-09-19 5 0.62% -0.22% -0.18% 0.80% -4.37%

Step 6: Visualize Results¶

Source

fig, axes = plt.subplots(2, 2, figsize=(14, 10))

event_time = event_results['event_time'].values

# Plot 1: Actual vs Expected Returns

ax1 = axes[0, 0]

ax1.bar(event_time - 0.2, event_results['stock_ret']*100, 0.4, label='Actual Return', alpha=0.8)

ax1.bar(event_time + 0.2, event_results['expected_ret']*100, 0.4, label='Expected Return', alpha=0.8)

ax1.axhline(y=0, color='black', linestyle='-', linewidth=0.5)

ax1.axvline(x=0, color='red', linestyle='--', alpha=0.7, label='Event Day')

ax1.set_xlabel('Event Time (Trading Days)', fontsize=12)

ax1.set_ylabel('Return (%)', fontsize=12)

ax1.set_title('Actual vs Expected Returns', fontsize=14)

ax1.legend()

ax1.set_xticks(event_time)

# Plot 2: Abnormal Returns

ax2 = axes[0, 1]

colors = ['green' if ar >= 0 else 'red' for ar in event_results['AR']]

ax2.bar(event_time, event_results['AR']*100, color=colors, alpha=0.8, edgecolor='black')

ax2.axhline(y=0, color='black', linestyle='-', linewidth=0.5)

ax2.axvline(x=0, color='red', linestyle='--', alpha=0.7, label='Event Day')

ax2.set_xlabel('Event Time (Trading Days)', fontsize=12)

ax2.set_ylabel('Abnormal Return (%)', fontsize=12)

ax2.set_title('Daily Abnormal Returns', fontsize=14)

ax2.legend()

ax2.set_xticks(event_time)

# Plot 3: Cumulative Abnormal Returns

ax3 = axes[1, 0]

ax3.plot(event_time, event_results['CAR']*100, 'b-o', linewidth=2, markersize=8)

ax3.fill_between(event_time, 0, event_results['CAR']*100, alpha=0.3)

ax3.axhline(y=0, color='black', linestyle='-', linewidth=0.5)

ax3.axvline(x=0, color='red', linestyle='--', alpha=0.7, label='Event Day')

ax3.set_xlabel('Event Time (Trading Days)', fontsize=12)

ax3.set_ylabel('Cumulative Abnormal Return (%)', fontsize=12)

ax3.set_title('Cumulative Abnormal Returns (CAR)', fontsize=14)

ax3.legend()

ax3.set_xticks(event_time)

# Plot 4: Stock Price Around Event

ax4 = axes[1, 1]

# Normalize price to 100 at event day

event_idx = event_results[event_results['event_time'] == 0].index[0]

base_price = event_results.loc[event_idx, 'stock_price']

normalized_price = (event_results['stock_price'] / base_price) * 100

ax4.plot(event_time, normalized_price, 'b-o', linewidth=2, markersize=8)

ax4.axhline(y=100, color='gray', linestyle='--', alpha=0.7)

ax4.axvline(x=0, color='red', linestyle='--', alpha=0.7, label='Event Day')

ax4.set_xlabel('Event Time (Trading Days)', fontsize=12)

ax4.set_ylabel('Normalized Price (Event Day = 100)', fontsize=12)

ax4.set_title(f'{TICKER} Stock Price Around Event', fontsize=14)

ax4.legend()

ax4.set_xticks(event_time)

plt.tight_layout()

plt.show()

Step 7: Statistical Testing (Preview)¶

For a single event, we can perform a simple t-test to assess whether abnormal returns are statistically significant. More sophisticated tests will be covered in Sessions 4 and 5.

Source

def simple_significance_test(event_results, model, windows=None):

"""

Perform simple t-test for abnormal returns.

Under the null hypothesis of no abnormal returns:

t = AR / sigma ~ t(T-2)

For CAR:

t = CAR / (sigma * sqrt(L)) where L is the window length

"""

sigma = model['sigma']

if windows is None:

windows = [(-1, 1), (0, 0), (-5, 5)]

print("Statistical Significance Tests")

print("="*60)

results = []

for w_start, w_end in windows:

mask = (event_results['event_time'] >= w_start) & (event_results['event_time'] <= w_end)

window_data = event_results[mask]

car = window_data['AR'].sum()

window_length = len(window_data)

# Standard error of CAR (assuming independence)

se_car = sigma * np.sqrt(window_length)

# t-statistic

t_stat = car / se_car

# p-value (two-tailed)

p_value = 2 * (1 - stats.t.cdf(abs(t_stat), df=ESTIMATION_WINDOW-2))

print(f"\nWindow [{w_start:+d}, {w_end:+d}]:")

print(f" CAR = {car*100:+.2f}%")

print(f" Std.Err = {se_car*100:.2f}%")

print(f" t-stat = {t_stat:.3f}")

print(f" p-value = {p_value:.4f}", end="")

if p_value < 0.01:

print(" ***")

elif p_value < 0.05:

print(" **")

elif p_value < 0.10:

print(" *")

else:

print("")

results.append({

'window': f"[{w_start:+d}, {w_end:+d}]",

'CAR': car,

't_stat': t_stat,

'p_value': p_value

})

print("\n" + "="*60)

print("Significance levels: *** p<0.01, ** p<0.05, * p<0.10")

return pd.DataFrame(results)

# Run significance tests

test_results = simple_significance_test(

event_results, model,

windows=[(-1, 1), (0, 0), (-5, 5), (-2, 2)]

)Statistical Significance Tests

============================================================

Window [-1, +1]:

CAR = -2.66%

Std.Err = 1.47%

t-stat = -1.808

p-value = 0.0731 *

Window [+0, +0]:

CAR = -1.13%

Std.Err = 0.85%

t-stat = -1.337

p-value = 0.1837

Window [-5, +5]:

CAR = -4.37%

Std.Err = 2.81%

t-stat = -1.555

p-value = 0.1226

Window [-2, +2]:

CAR = -2.64%

Std.Err = 1.90%

t-stat = -1.391

p-value = 0.1670

============================================================

Significance levels: *** p<0.01, ** p<0.05, * p<0.10

7. Interpretation and Caveats¶

Interpreting the Results¶

The abnormal return captures the component of the stock’s return that cannot be explained by general market movements. A positive (negative) abnormal return suggests the event created (destroyed) shareholder value.

Important considerations:

Single-firm limitation: With only one event, we cannot separate the event effect from firm-specific noise. Multi-firm samples (covered in Sessions 4-5) provide more robust inference.

Event window choice: Different windows may yield different conclusions. The choice should be guided by:

How quickly information is incorporated (shorter for efficient markets)

Whether the event was anticipated (longer window to capture pre-announcement drift)

Industry norms and prior research

Confounding events: Other news during the event window can contaminate our estimates.

Market model assumptions: The market model assumes a stable relationship between stock and market returns, which may not hold.

8. Exercises¶

Exercise 1: Different Event¶

Modify the code to study a different corporate event (e.g., an earnings announcement, M&A deal, or CEO change). Document your findings.

Exercise 2: Alternative Normal Return Model¶

Implement the constant mean return model:

Compare results with the market model.

Exercise 3: Sensitivity Analysis¶

Examine how your results change when you:

Vary the estimation window length (60, 120, 250 days)

Use different event windows ([-1,+1], [-3,+3], [-10,+10])

Change the market index (S&P 500, NASDAQ, sector ETF)

Source

# Exercise 2 Solution Template: Constant Mean Return Model

def estimate_constant_mean_model(estimation_data):

"""

Estimate constant mean return model.

E[R_i,t] = mean(R_i) during estimation period

"""

y = estimation_data['stock_ret'].values

mean_return = np.mean(y)

residuals = y - mean_return

sigma = np.std(residuals, ddof=1)

return {

'mean_return': mean_return,

'sigma': sigma,

'residuals': residuals

}

def calculate_ar_constant_mean(event_data, model):

"""

Calculate abnormal returns using constant mean model.

"""

result = event_data.copy()

result['expected_ret'] = model['mean_return']

result['AR'] = result['stock_ret'] - result['expected_ret']

result['CAR'] = result['AR'].cumsum()

return result

# Your code here to estimate and compare models

# ...9. Summary¶

In this session, we covered:

The Logic of Event Studies: Using market efficiency to isolate event impacts

Historical Context: The foundational work of Ball & Brown (1968) and FFJR (1969)

Timeline Structure: Estimation window, event window, and their relationship

The Market Model: Estimating normal returns as a function of market returns

Abnormal Returns: AR and CAR as measures of event impact

Basic Implementation: A complete single-event study workflow

Coming Up Next¶

Session 2: The Market Model and Normal Return Estimation will explore:

Alternative models for expected returns (CAPM, Fama-French, Carhart)

Parameter estimation techniques

Model selection and specification tests

Handling estimation issues (thin trading, non-synchronous trading)

10. References¶

Foundational Papers¶

Ball, R., & Brown, P. (1968). An empirical evaluation of accounting income numbers. Journal of Accounting Research, 6(2), 159-178.

Fama, E. F., Fisher, L., Jensen, M. C., & Roll, R. (1969). The adjustment of stock prices to new information. International Economic Review, 10(1), 1-21.

Methodological References¶

Brown, S. J., & Warner, J. B. (1985). Using daily stock returns: The case of event studies. Journal of Financial Economics, 14(1), 3-31.

MacKinlay, A. C. (1997). Event studies in economics and finance. Journal of Economic Literature, 35(1), 13-39.

Kothari, S. P., & Warner, J. B. (2007). Econometrics of event studies. Handbook of Corporate Finance, 1, 3-36.

Textbooks¶

Campbell, J. Y., Lo, A. W., & MacKinlay, A. C. (1997). The Econometrics of Financial Markets. Princeton University Press. Chapter 4.