Lecture 1: Introduction and Course Overview

MIT 15.401 — Finance Theory I (Prof. Andrew Lo)¶

Video: MIT OCW — Lecture 1: Introduction and Course Overview

Readings: Brealey, Myers, and Allen — Chapters 1–2

This notebook corresponds to Session 1 of Andrew Lo’s Finance Theory I course at MIT Sloan. The lecture sets the stage for the entire course by introducing the motivation behind finance, the key players in the financial system, the fundamental challenges that make finance both difficult and fascinating, a framework for financial analysis, and the six fundamental principles of finance that serve as recurring themes throughout the course.

We complement the theoretical exposition with Python code for hands-on illustrations, visualizations to build intuition, and exercises at the end.

Table of Contents¶

Source

# ============================================================

# Setup: Import libraries used throughout this notebook

# ============================================================

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import matplotlib.ticker as mticker

from IPython.display import display, Markdown

plt.rcParams.update({

'figure.figsize': (10, 5),

'axes.spines.top': False,

'axes.spines.right': False,

'axes.grid': True,

'grid.alpha': 0.3,

'font.size': 12,

'lines.linewidth': 2,

})

print("Libraries loaded successfully.")Libraries loaded successfully.

1. Motivation — Why Finance?¶

Andrew Lo opens the lecture with a simple but powerful equation:

Finance is fundamentally about valuing things — assets, projects, companies, derivatives — and then managing them. Every business activity ultimately reduces to two functions:

Valuation of assets (real/financial, tangible/intangible)

Management of assets (acquiring/selling)

The famous mantra applies: “You cannot manage what you cannot measure.” Valuation is the starting point for management — once value is established, management becomes tractable.

Why Is Finance So Important?¶

Finance touches every aspect of business and personal life. The financial system serves as the circulatory system of the economy: it channels resources from those who have capital to those who need it, enables risk sharing, and facilitates economic growth.

Lo points to legendary figures — Warren Buffett (Berkshire Hathaway), James Simons (Renaissance Technologies), Jack Welch (GE) — as examples of individuals who have mastered the art and science of finance.

The Power of Financial Literacy¶

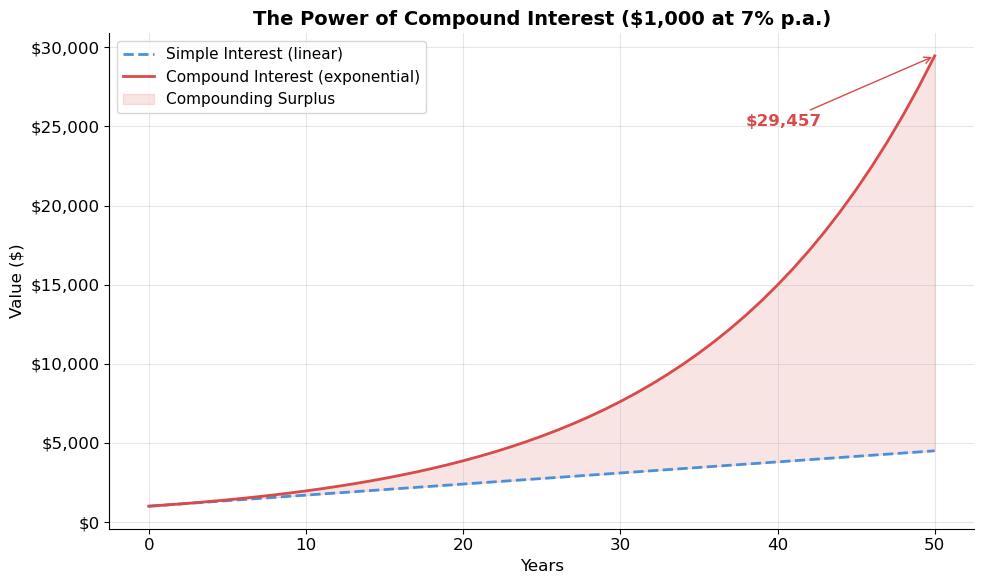

Let’s illustrate the impact of finance with a simple example: the dramatic power of compound interest, which Albert Einstein allegedly called “the most powerful force in the universe.”

Source

# ============================================================

# Illustration: The Power of Compound Interest

# ============================================================

years = np.arange(0, 51)

principal = 1000

rate = 0.07 # 7% annual return

simple_interest = principal * (1 + rate * years)

compound_interest = principal * (1 + rate) ** years

fig, ax = plt.subplots(figsize=(10, 6))

ax.plot(years, simple_interest, label='Simple Interest (linear)', linestyle='--', color='#4a90d9')

ax.plot(years, compound_interest, label='Compound Interest (exponential)', color='#d94a4a')

ax.fill_between(years, simple_interest, compound_interest, alpha=0.15, color='#d94a4a',

label='Compounding Surplus')

ax.set_xlabel('Years')

ax.set_ylabel('Value ($)')

ax.set_title('The Power of Compound Interest ($1,000 at 7% p.a.)', fontsize=14, fontweight='bold')

ax.yaxis.set_major_formatter(mticker.FuncFormatter(lambda x, _: f'${x:,.0f}'))

ax.legend(fontsize=11)

ax.annotate(f'${compound_interest[-1]:,.0f}',

xy=(50, compound_interest[-1]), xytext=(38, compound_interest[-1] * 0.85),

fontsize=12, fontweight='bold', color='#d94a4a',

arrowprops=dict(arrowstyle='->', color='#d94a4a'))

plt.tight_layout()

plt.show()

print(f"After 50 years at 7%:")

print(f" Simple interest: ${simple_interest[-1]:>10,.2f}")

print(f" Compound interest: ${compound_interest[-1]:>10,.2f}")

print(f" Compounding bonus: ${compound_interest[-1] - simple_interest[-1]:>10,.2f}")

After 50 years at 7%:

Simple interest: $ 4,500.00

Compound interest: $ 29,457.03

Compounding bonus: $ 24,957.03

This is a preview of one of the most important concepts in finance: the time value of money. A dollar today is worth more than a dollar tomorrow, and the compounding effect is the engine that drives wealth creation over time. We will formalize this rigorously in Lectures 2–4 on Present Value Relations.

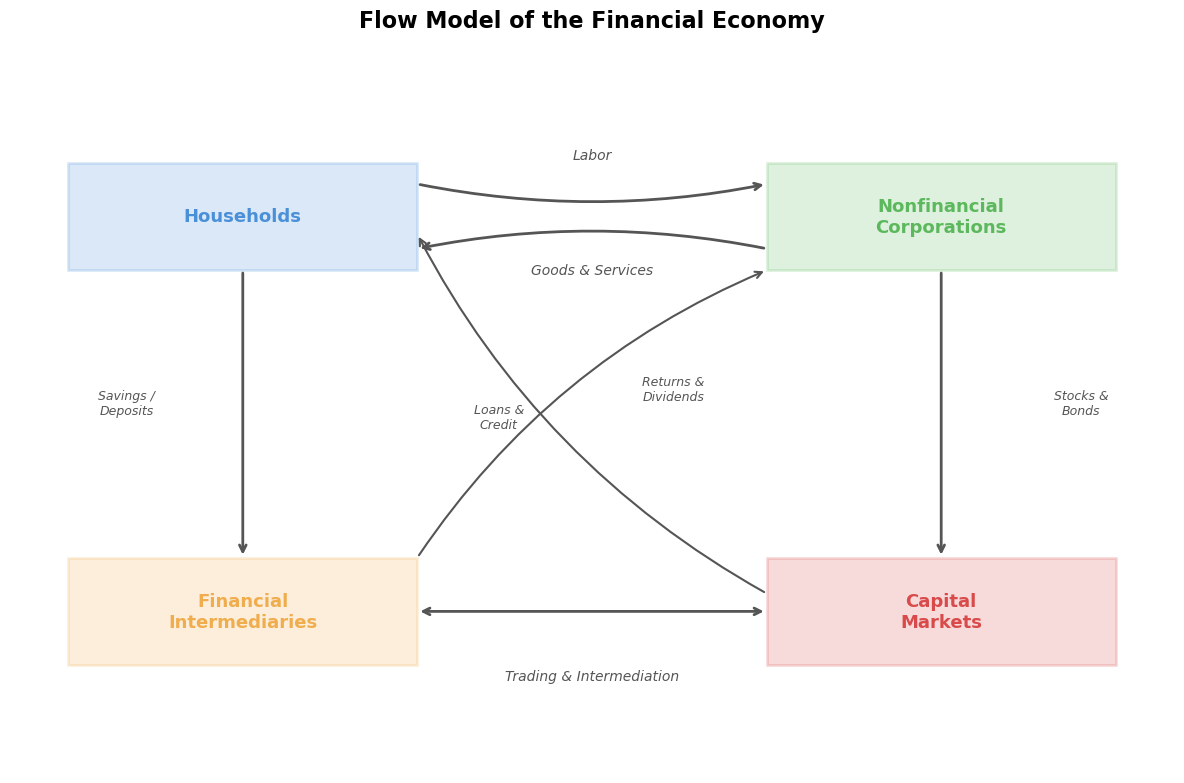

2. Dramatis Personae — The Flow Model of the Economy¶

Lo introduces the key actors in the financial system through a flow model of the economy.

The Circular Flow¶

| Actor | Role |

|---|---|

| Households | Supply labor, consume goods, save and invest |

| Nonfinancial Corporations | Produce goods and services, invest in real assets |

| Financial Intermediaries | Banks, insurance companies, mutual funds — channel capital |

| Capital Markets | Stock markets, bond markets, derivatives markets — price discovery |

Key insight: Financial markets and intermediaries exist to serve a vital economic function — they transfer resources across time and across states of nature (i.e., under uncertainty).

Source

# ============================================================

# Visualization: A Simplified Flow Model of the Economy

# ============================================================

fig, ax = plt.subplots(figsize=(12, 8))

ax.set_xlim(0, 10)

ax.set_ylim(0, 10)

ax.axis('off')

ax.set_title('Flow Model of the Financial Economy', fontsize=16, fontweight='bold', pad=20)

boxes = {

'Households': (0.5, 7, 3, 1.5),

'Nonfinancial\nCorporations': (6.5, 7, 3, 1.5),

'Financial\nIntermediaries': (0.5, 1.5, 3, 1.5),

'Capital\nMarkets': (6.5, 1.5, 3, 1.5),

}

colors = {'Households': '#4a90d9', 'Nonfinancial\nCorporations': '#5cb85c',

'Financial\nIntermediaries': '#f0ad4e', 'Capital\nMarkets': '#d94a4a'}

for name, (x, y, w, h) in boxes.items():

rect = plt.Rectangle((x, y), w, h, linewidth=2, edgecolor=colors[name],

facecolor=colors[name], alpha=0.2, zorder=2)

ax.add_patch(rect)

ax.text(x + w/2, y + h/2, name, ha='center', va='center',

fontsize=13, fontweight='bold', color=colors[name], zorder=3)

arrow_kw = dict(arrowstyle='->', color='#555', lw=2, connectionstyle='arc3,rad=0.1')

ax.annotate('', xy=(6.5, 8.2), xytext=(3.5, 8.2), arrowprops=arrow_kw)

ax.text(5, 8.55, 'Labor', ha='center', fontsize=10, style='italic', color='#555')

ax.annotate('', xy=(3.5, 7.3), xytext=(6.5, 7.3), arrowprops=arrow_kw)

ax.text(5, 6.95, 'Goods & Services', ha='center', fontsize=10, style='italic', color='#555')

ax.annotate('', xy=(2, 3), xytext=(2, 7), arrowprops=dict(arrowstyle='->', color='#555', lw=2))

ax.text(1.0, 5.0, 'Savings /\nDeposits', ha='center', fontsize=9, style='italic', color='#555')

ax.annotate('', xy=(6.5, 7.0), xytext=(3.5, 3.0),

arrowprops=dict(arrowstyle='->', color='#555', lw=1.5, connectionstyle='arc3,rad=-0.15'))

ax.text(4.2, 4.8, 'Loans &\nCredit', ha='center', fontsize=9, style='italic', color='#555')

ax.annotate('', xy=(8, 3), xytext=(8, 7), arrowprops=dict(arrowstyle='->', color='#555', lw=2))

ax.text(9.2, 5.0, 'Stocks &\nBonds', ha='center', fontsize=9, style='italic', color='#555')

ax.annotate('', xy=(3.5, 7.5), xytext=(6.5, 2.5),

arrowprops=dict(arrowstyle='->', color='#555', lw=1.5, connectionstyle='arc3,rad=-0.15'))

ax.text(5.7, 5.2, 'Returns &\nDividends', ha='center', fontsize=9, style='italic', color='#555')

ax.annotate('', xy=(6.5, 2.25), xytext=(3.5, 2.25),

arrowprops=dict(arrowstyle='<->', color='#555', lw=2))

ax.text(5, 1.3, 'Trading & Intermediation', ha='center', fontsize=10, style='italic', color='#555')

plt.tight_layout()

plt.show()

Personal vs. Corporate Financial Decisions¶

Lo emphasizes that the framework applies at both the personal and corporate level:

Personal Financial Decisions: Cash raised from financial institutions → invested in real assets (education, housing) → generated by labor → consumed and reinvested → invested in financial assets. Objective: Maximize lifetime expected utility.

Corporate Financial Decisions: Cash raised from investors (stocks, bonds) → invested in real assets (factories, R&D) → generated from operations → reinvested → returned to investors (dividends, buybacks). Objective: Maximize shareholder value.

A crucial insight: valuation is generally independent of objectives. Whether you want to buy or sell an asset, its value is the same — financial markets perform a price discovery function that aggregates information from all participants.

3. Fundamental Challenges of Finance¶

3.1 The Language of Finance: Accounting¶

Accounting is the language of finance. The three fundamental financial statements form the backbone:

| Statement | What It Tells You | Key Question |

|---|---|---|

| Balance Sheet | What the firm owns and owes at a point in time | What is the firm’s financial position? |

| Income Statement | Revenues, expenses, and profit over a period | Is the firm profitable? |

| Cash Flow Statement | Actual cash inflows and outflows over a period | Does the firm generate cash? |

The fundamental accounting identity:

3.2 Cash Flow vs. Accounting Profit¶

A key theme: cash flow is king. Accounting profit can be manipulated, but cash flows represent actual economic value.

Source

# ============================================================

# Example: Accounting Profit vs. Cash Flow

# ============================================================

data = {

'Item': [

'Revenue (on credit)', 'Cash collected from customers',

'Cost of goods sold', 'Cash paid for inventory',

'Depreciation expense', 'Capital expenditure (cash)',

'', 'ACCOUNTING PROFIT', 'CASH FLOW'

],

'Income Statement': [

100_000, '—', -60_000, '—', -10_000, '—', '', 30_000, '—'

],

'Cash Flow Statement': [

'—', 70_000, '—', -80_000, '—', -50_000, '', '—', -60_000

]

}

df = pd.DataFrame(data)

print("=" * 65)

print("ACCOUNTING PROFIT vs. CASH FLOW — A Cautionary Example")

print("=" * 65)

print(df.to_string(index=False))

print("=" * 65)

print("\nThe firm shows a $30,000 PROFIT on its income statement,")

print("but its actual cash flow is NEGATIVE $60,000!")

print("\n→ This is why finance focuses on CASH FLOWS, not accounting profits.")=================================================================

ACCOUNTING PROFIT vs. CASH FLOW — A Cautionary Example

=================================================================

Item Income Statement Cash Flow Statement

Revenue (on credit) 100000 —

Cash collected from customers — 70000

Cost of goods sold -60000 —

Cash paid for inventory — -80000

Depreciation expense -10000 —

Capital expenditure (cash) — -50000

ACCOUNTING PROFIT 30000 —

CASH FLOW — -60000

=================================================================

The firm shows a $30,000 PROFIT on its income statement,

but its actual cash flow is NEGATIVE $60,000!

→ This is why finance focuses on CASH FLOWS, not accounting profits.

4. The Framework of Financial Analysis¶

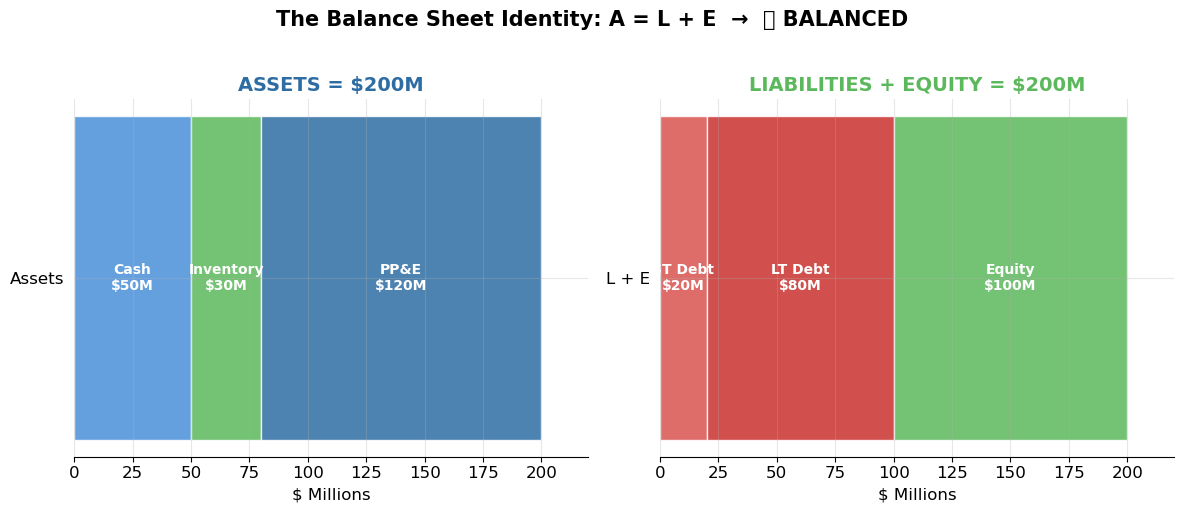

The Balance Sheet — A Snapshot¶

Or equivalently: (the net worth from shareholders’ perspective).

The Income Statement — A Movie¶

The Cash Flow Statement — The Real Story¶

Source

# ============================================================

# Interactive Balance Sheet — Change Parameters and Re-run

# ============================================================

# ▶ MODIFY THESE PARAMETERS AND RE-RUN THE CELL

cash = 50 # Cash ($M)

inventory = 30 # Inventory ($M)

ppe = 120 # Property, Plant & Equipment ($M)

short_term_debt = 20 # Short-term debt ($M)

long_term_debt = 80 # Long-term debt ($M)

# ============================================================

total_assets = cash + inventory + ppe

total_liabilities = short_term_debt + long_term_debt

equity = total_assets - total_liabilities

fig, axes = plt.subplots(1, 2, figsize=(12, 5))

# Assets side

left = 0

for val, label, color in zip([cash, inventory, ppe],

[f'Cash\n${cash}M', f'Inventory\n${inventory}M', f'PP&E\n${ppe}M'],

['#4a90d9', '#5cb85c', '#2e6da4']):

axes[0].barh(['Assets'], [val], left=left, color=color, edgecolor='white', height=0.6, alpha=0.85)

if val > 10:

axes[0].text(left + val/2, 0, label, ha='center', va='center', fontsize=10, color='white', fontweight='bold')

left += val

axes[0].set_title(f'ASSETS = ${total_assets}M', fontsize=14, fontweight='bold', color='#2e6da4')

# Liabilities + Equity side

left = 0

for val, label, color in zip([short_term_debt, long_term_debt, max(equity, 0)],

[f'ST Debt\n${short_term_debt}M', f'LT Debt\n${long_term_debt}M', f'Equity\n${equity}M'],

['#d9534f', '#c9302c', '#5cb85c' if equity >= 0 else '#d9534f']):

axes[1].barh(['L + E'], [val], left=left, color=color, edgecolor='white', height=0.6, alpha=0.85)

if val > 10:

axes[1].text(left + val/2, 0, label, ha='center', va='center', fontsize=10, color='white', fontweight='bold')

left += val

title_color = '#5cb85c' if equity >= 0 else '#d9534f'

axes[1].set_title(f'LIABILITIES + EQUITY = ${total_liabilities + equity}M', fontsize=14, fontweight='bold', color=title_color)

for ax in axes:

ax.spines['left'].set_visible(False)

ax.tick_params(left=False)

ax.set_xlabel('$ Millions')

ax.set_xlim(0, max(total_assets, total_liabilities + max(equity, 0)) * 1.1)

status = "✅ BALANCED" if abs(total_assets - (total_liabilities + equity)) < 0.01 else "❌ ERROR"

fig.suptitle(f'The Balance Sheet Identity: A = L + E → {status}', fontsize=15, fontweight='bold', y=1.02)

if equity < 0:

fig.text(0.5, -0.05, '⚠️ NEGATIVE EQUITY — The firm is technically insolvent!',

ha='center', fontsize=13, color='#d9534f', fontweight='bold')

plt.tight_layout()

plt.show()C:\Users\mjfmourey\AppData\Local\Temp\ipykernel_65876\1014374855.py:55: UserWarning: Glyph 9989 (\N{WHITE HEAVY CHECK MARK}) missing from current font.

plt.tight_layout()

C:\Users\mjfmourey\AppData\Local\anaconda3\Lib\site-packages\IPython\core\pylabtools.py:170: UserWarning: Glyph 9989 (\N{WHITE HEAVY CHECK MARK}) missing from current font.

fig.canvas.print_figure(bytes_io, **kw)

Try it: Change the debt values in the parameter cell above until equity becomes negative — this illustrates insolvency (liabilities exceed assets).

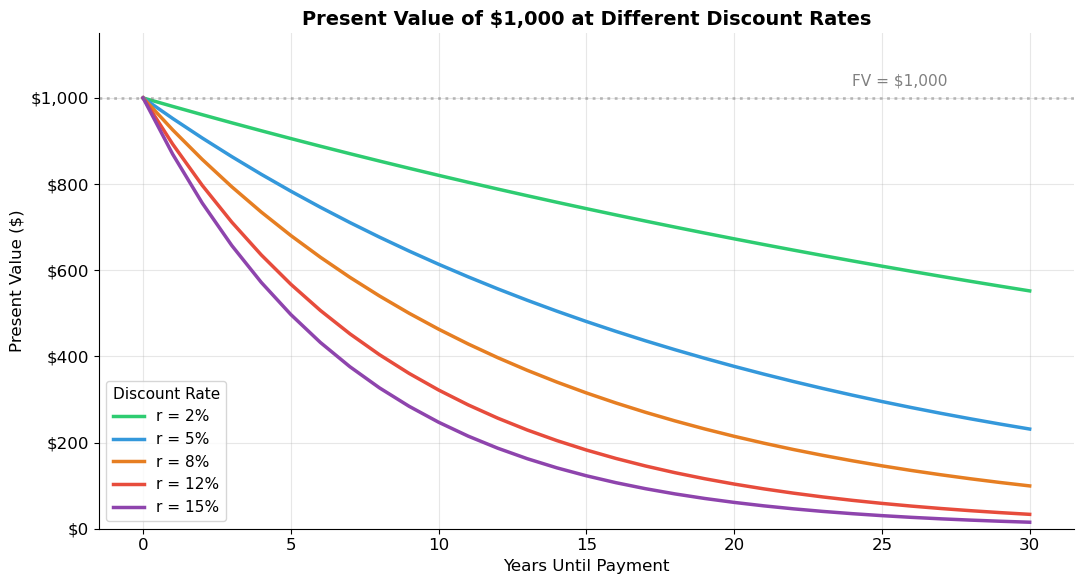

5. The Importance of Time and Risk¶

Lo identifies two factors that make finance particularly challenging:

5.1 Time¶

Cash flows now are fundamentally different from cash flows later. The core question: how do we compare cash flows at different points in time?

5.2 Risk¶

Under perfect certainty, finance theory would be complete. Risk creates significant challenges because future cash flows are uncertain, individuals have different attitudes toward risk, and markets must price risk.

Lo’s approach: (1) Use historical data, (2) Use mathematics.

Source

# ============================================================

# Impact of Discount Rates on Present Value

# ============================================================

# ▶ MODIFY THESE PARAMETERS AND RE-RUN THE CELL

future_value = 1000

max_years = 30

# ============================================================

years = np.arange(0, max_years + 1)

rates = [0.02, 0.05, 0.08, 0.12, 0.15]

colors = ['#2ecc71', '#3498db', '#e67e22', '#e74c3c', '#8e44ad']

fig, ax = plt.subplots(figsize=(11, 6))

for r, color in zip(rates, colors):

pv = future_value / (1 + r) ** years

ax.plot(years, pv, label=f'r = {r:.0%}', color=color, linewidth=2.5)

ax.axhline(y=future_value, color='gray', linestyle=':', alpha=0.5)

ax.text(max_years * 0.8, future_value * 1.03, f'FV = ${future_value:,.0f}', fontsize=11, color='gray')

ax.set_xlabel('Years Until Payment', fontsize=12)

ax.set_ylabel('Present Value ($)', fontsize=12)

ax.set_title(f'Present Value of ${future_value:,.0f} at Different Discount Rates', fontsize=14, fontweight='bold')

ax.yaxis.set_major_formatter(mticker.FuncFormatter(lambda x, _: f'${x:,.0f}'))

ax.legend(title='Discount Rate', fontsize=11, title_fontsize=11)

ax.set_ylim(0, future_value * 1.15)

plt.tight_layout()

plt.show()

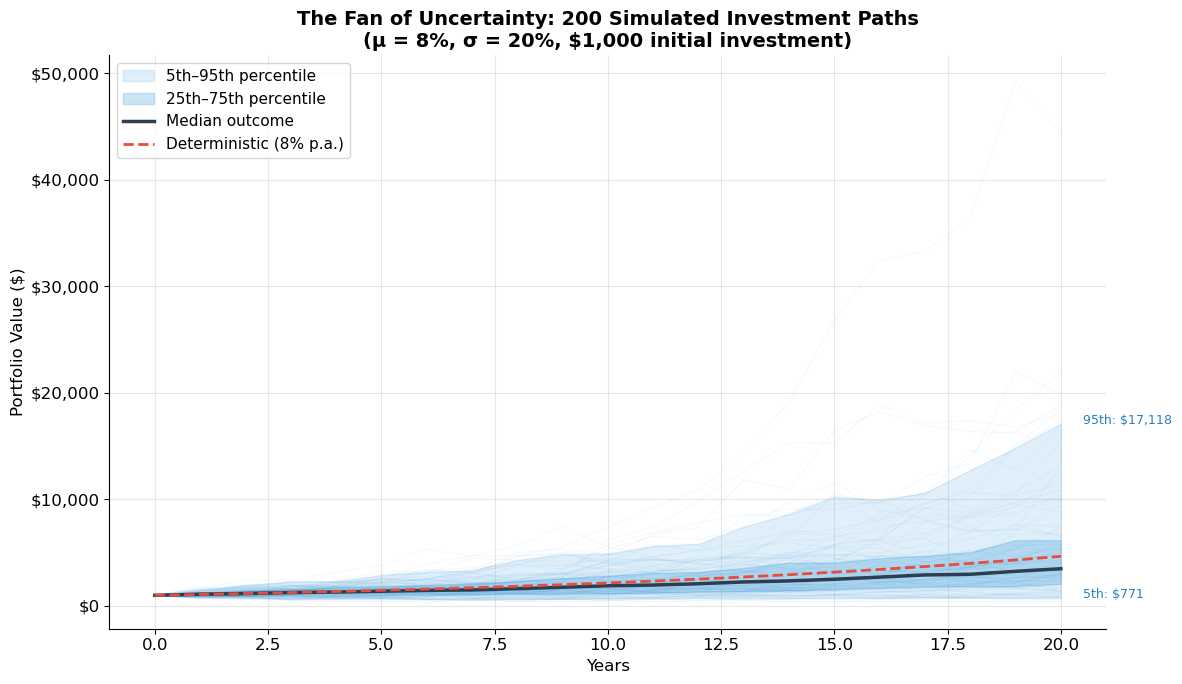

Source

# ============================================================

# Simulation: The Fan of Uncertainty — Random Investment Paths

# ============================================================

np.random.seed(42)

initial = 1000

mu = 0.08 # Expected annual return

sigma = 0.20 # Annual volatility

T = 20 # Time horizon

n_paths = 200 # Number of simulations

years = np.arange(0, T + 1)

log_returns = np.random.normal(mu - 0.5 * sigma**2, sigma, size=(n_paths, T))

log_prices = np.column_stack([np.zeros(n_paths), np.cumsum(log_returns, axis=1)])

paths = initial * np.exp(log_prices)

risk_free_path = initial * (1 + mu) ** years

p5 = np.percentile(paths, 5, axis=0)

p25 = np.percentile(paths, 25, axis=0)

p50 = np.percentile(paths, 50, axis=0)

p75 = np.percentile(paths, 75, axis=0)

p95 = np.percentile(paths, 95, axis=0)

fig, ax = plt.subplots(figsize=(12, 7))

for i in range(min(n_paths, 100)):

ax.plot(years, paths[i], color='#3498db', alpha=0.05, linewidth=0.8)

ax.fill_between(years, p5, p95, alpha=0.15, color='#3498db', label='5th–95th percentile')

ax.fill_between(years, p25, p75, alpha=0.25, color='#3498db', label='25th–75th percentile')

ax.plot(years, p50, color='#2c3e50', linewidth=2.5, label='Median outcome')

ax.plot(years, risk_free_path, color='#e74c3c', linewidth=2, linestyle='--',

label=f'Deterministic ({mu:.0%} p.a.)')

ax.set_xlabel('Years', fontsize=12)

ax.set_ylabel('Portfolio Value ($)', fontsize=12)

ax.set_title(f'The Fan of Uncertainty: {n_paths} Simulated Investment Paths\n'

f'(μ = {mu:.0%}, σ = {sigma:.0%}, $1,000 initial investment)',

fontsize=14, fontweight='bold')

ax.yaxis.set_major_formatter(mticker.FuncFormatter(lambda x, _: f'${x:,.0f}'))

ax.legend(fontsize=11, loc='upper left')

ax.annotate(f'95th: ${p95[-1]:,.0f}', xy=(T, p95[-1]), xytext=(T+0.5, p95[-1]), fontsize=9, color='#2980b9')

ax.annotate(f'5th: ${p5[-1]:,.0f}', xy=(T, p5[-1]), xytext=(T+0.5, p5[-1]), fontsize=9, color='#2980b9')

plt.tight_layout()

plt.show()

final_values = paths[:, -1]

print(f"After {T} years — Distribution of final portfolio values:")

print(f" Mean: ${np.mean(final_values):>10,.0f}")

print(f" Median: ${np.median(final_values):>10,.0f}")

print(f" Std Dev: ${np.std(final_values):>10,.0f}")

print(f" 5th percentile: ${np.percentile(final_values, 5):>10,.0f}")

print(f" 95th percentile: ${np.percentile(final_values, 95):>10,.0f}")

print(f" Probability of loss: {np.mean(final_values < initial):.1%}")

After 20 years — Distribution of final portfolio values:

Mean: $ 5,311

Median: $ 3,497

Std Dev: $ 5,546

5th percentile: $ 771

95th percentile: $ 17,118

Probability of loss: 9.0%

The fan of uncertainty reveals a fundamental truth: as the time horizon increases, the range of possible outcomes widens dramatically. Risk management is essential — it’s not about avoiding risk, but about understanding and managing it.

6. Six Fundamental Principles of Finance¶

These six principles serve as the intellectual backbone of the entire course.

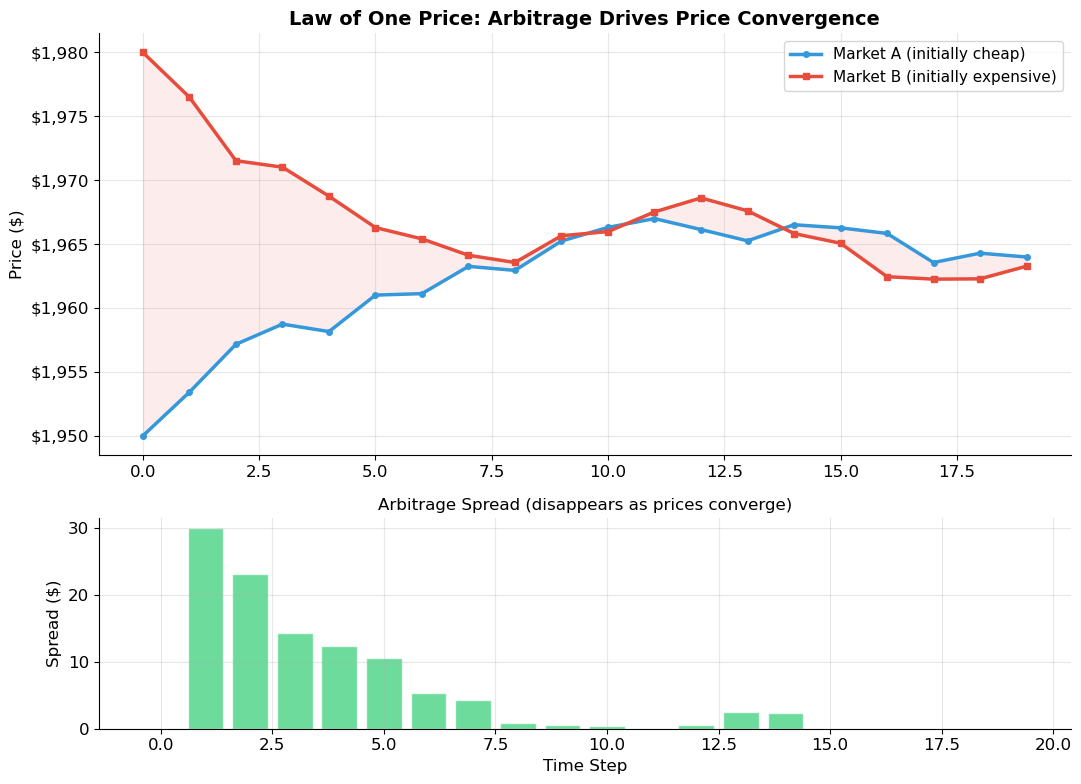

P1: There Is No Such Thing As A Free Lunch¶

The no-arbitrage principle — the most powerful idea in all of finance. An arbitrage is a riskless profit with no investment. In well-functioning markets, arbitrage opportunities are eliminated almost instantaneously.

This principle is the foundation for option pricing (Black-Scholes), fixed-income arbitrage, and most of modern derivatives pricing.

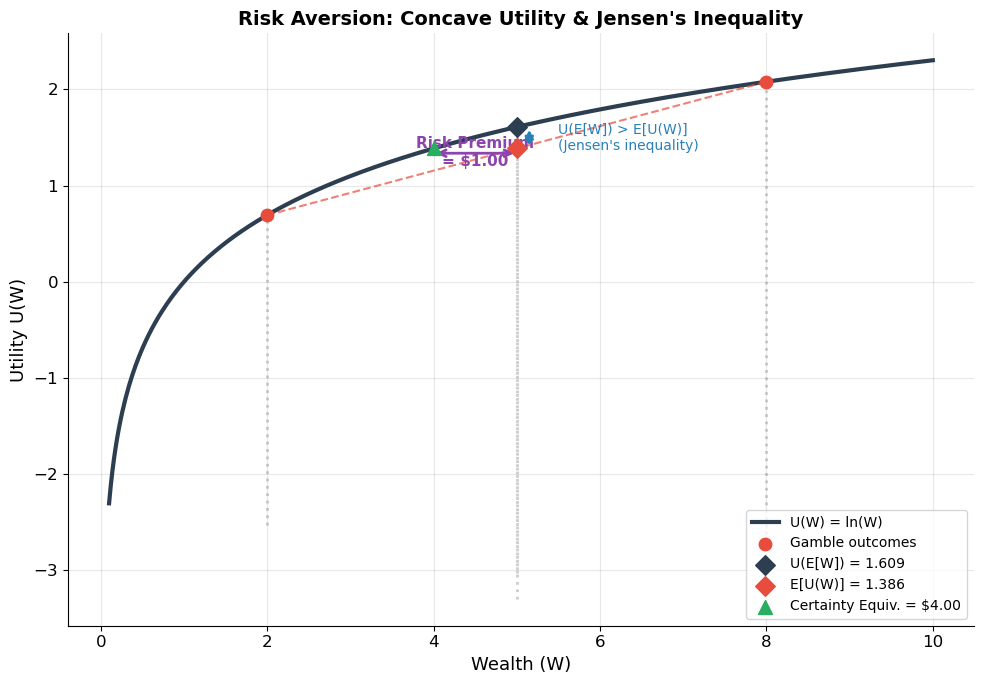

P2: Other Things Equal, Individuals...¶

Prefer more money to less (non-satiation): for

Prefer money now to later (impatience)

Prefer to avoid risk (risk aversion): for concave

P3: All Agents Act To Further Their Own Self-Interest¶

Rational self-interest + competition → efficient outcomes (Adam Smith’s “invisible hand”). But also creates agency problems.

P4: Financial Market Prices Shift to Equalize Supply and Demand¶

Market prices reflect equilibrium — a powerful information aggregation mechanism.

P5: Financial Markets Are Highly Adaptive and Competitive¶

Markets evolve rapidly. Related to the Efficient Market Hypothesis (EMH).

P6: Risk-Sharing and Frictions Are Central to Financial Innovation¶

Every major financial product exists because of the desire to share risk more efficiently and overcome market frictions.

Source

# ============================================================

# Illustration of P1: No-Arbitrage — Price Convergence

# ============================================================

np.random.seed(123)

price_A_init, price_B_init = 1950, 1980

convergence_speed = 0.3

n_steps = 20

price_A, price_B, profit = [price_A_init], [price_B_init], [0]

for t in range(1, n_steps):

spread = price_B[-1] - price_A[-1]

adjustment = spread * convergence_speed

price_A.append(price_A[-1] + adjustment * 0.5 + np.random.normal(0, 1))

price_B.append(price_B[-1] - adjustment * 0.5 + np.random.normal(0, 1))

profit.append(max(spread, 0))

steps = range(n_steps)

fig, (ax1, ax2) = plt.subplots(2, 1, figsize=(11, 8), height_ratios=[2, 1])

ax1.plot(steps, price_A, label='Market A (initially cheap)', color='#3498db', linewidth=2.5, marker='o', markersize=4)

ax1.plot(steps, price_B, label='Market B (initially expensive)', color='#e74c3c', linewidth=2.5, marker='s', markersize=4)

ax1.fill_between(steps, price_A, price_B, alpha=0.1, color='#e74c3c')

ax1.set_ylabel('Price ($)', fontsize=12)

ax1.set_title('Law of One Price: Arbitrage Drives Price Convergence', fontsize=14, fontweight='bold')

ax1.legend(fontsize=11)

ax1.yaxis.set_major_formatter(mticker.FuncFormatter(lambda x, _: f'${x:,.0f}'))

ax2.bar(steps, profit, color='#2ecc71', alpha=0.7, edgecolor='white')

ax2.set_xlabel('Time Step', fontsize=12)

ax2.set_ylabel('Spread ($)', fontsize=12)

ax2.set_title('Arbitrage Spread (disappears as prices converge)', fontsize=12)

plt.tight_layout()

plt.show()

Source

# ============================================================

# Illustration of P2: Risk Aversion via Utility Functions

# ============================================================

W = np.linspace(0.1, 10, 500)

U = np.log(W)

# Gamble: 50% chance of W=2, 50% chance of W=8

W_low, W_high = 2, 8

p = 0.5

E_W = p * W_low + (1 - p) * W_high # Expected wealth = 5

E_U = p * np.log(W_low) + (1 - p) * np.log(W_high) # Expected utility

U_E = np.log(E_W) # Utility of expected wealth

CE = np.exp(E_U) # Certainty equivalent

fig, ax = plt.subplots(figsize=(10, 7))

ax.plot(W, U, color='#2c3e50', linewidth=3, label='U(W) = ln(W)')

ax.plot([W_low, W_high], [np.log(W_low), np.log(W_high)],

color='#e74c3c', linewidth=1.5, linestyle='--', alpha=0.7)

ax.scatter([W_low, W_high], [np.log(W_low), np.log(W_high)],

color='#e74c3c', s=80, zorder=5, label='Gamble outcomes')

ax.scatter([E_W], [U_E], color='#2c3e50', s=100, zorder=5, marker='D',

label=f'U(E[W]) = {U_E:.3f}')

ax.scatter([E_W], [E_U], color='#e74c3c', s=100, zorder=5, marker='D',

label=f'E[U(W)] = {E_U:.3f}')

ax.scatter([CE], [E_U], color='#27ae60', s=100, zorder=5, marker='^',

label=f'Certainty Equiv. = ${CE:.2f}')

ax.annotate('', xy=(CE, E_U - 0.05), xytext=(E_W, E_U - 0.05),

arrowprops=dict(arrowstyle='<->', color='#8e44ad', lw=2))

ax.text((CE + E_W) / 2, E_U - 0.18, f'Risk Premium\n= ${E_W - CE:.2f}',

ha='center', fontsize=11, color='#8e44ad', fontweight='bold')

ax.annotate('', xy=(E_W + 0.15, U_E), xytext=(E_W + 0.15, E_U),

arrowprops=dict(arrowstyle='<->', color='#2980b9', lw=2))

ax.text(E_W + 0.5, (U_E + E_U) / 2, "U(E[W]) > E[U(W)]\n(Jensen's inequality)",

fontsize=10, color='#2980b9', va='center')

for w, u in [(W_low, np.log(W_low)), (W_high, np.log(W_high)), (E_W, U_E), (E_W, E_U)]:

ax.plot([w, w], [ax.get_ylim()[0] if ax.get_ylim()[0] < u else u - 0.5, u], color='gray', linestyle=':', alpha=0.4)

ax.set_xlabel('Wealth (W)', fontsize=13)

ax.set_ylabel('Utility U(W)', fontsize=13)

ax.set_title("Risk Aversion: Concave Utility & Jensen's Inequality", fontsize=14, fontweight='bold')

ax.legend(fontsize=10, loc='lower right')

plt.tight_layout()

plt.show()

print(f"Gamble: 50% chance of ${W_low}, 50% chance of ${W_high}")

print(f"Expected wealth E[W] = ${E_W:.2f}")

print(f"U(E[W]) = {U_E:.4f} (utility of getting E[W] for sure)")

print(f"E[U(W)] = {E_U:.4f} (expected utility of the gamble)")

print(f"Certainty Equivalent CE = ${CE:.2f}")

print(f"Risk Premium = E[W] - CE = ${E_W - CE:.2f}")

print(f"\n→ A risk-averse agent would pay up to ${E_W - CE:.2f} to avoid the gamble.")

Gamble: 50% chance of $2, 50% chance of $8

Expected wealth E[W] = $5.00

U(E[W]) = 1.6094 (utility of getting E[W] for sure)

E[U(W)] = 1.3863 (expected utility of the gamble)

Certainty Equivalent CE = $4.00

Risk Premium = E[W] - CE = $1.00

→ A risk-averse agent would pay up to $1.00 to avoid the gamble.

Understanding Risk Aversion¶

For a risk-averse individual with concave utility, Jensen’s inequality gives us:

The certainty equivalent (CE) is the guaranteed amount giving the same utility as the gamble:

The risk premium is:

This is why risky assets must offer higher expected returns — investors demand compensation for bearing risk.

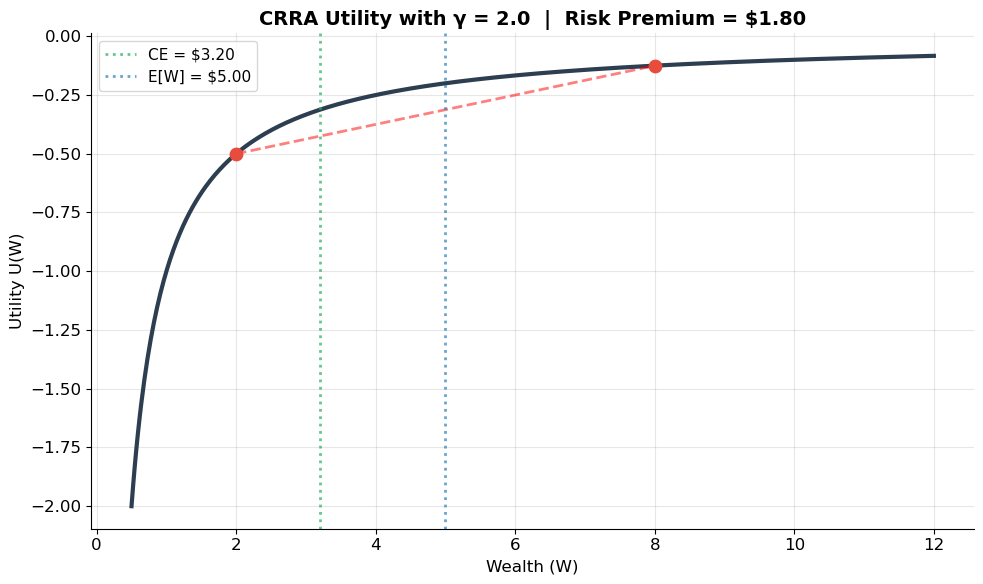

Source

# ============================================================

# Explore Risk Aversion with Different CRRA Parameters

# ============================================================

# ▶ MODIFY gamma AND RE-RUN TO SEE HOW RISK AVERSION CHANGES

gamma = 2.0 # Risk aversion coefficient (try: 0.5, 1, 2, 5, 10)

W_low = 2.0

W_high = 8.0

# ============================================================

W = np.linspace(0.5, 12, 500)

if abs(gamma - 1.0) < 0.01:

U = np.log(W)

u_low, u_high = np.log(W_low), np.log(W_high)

CE = np.exp(0.5 * u_low + 0.5 * u_high)

else:

U = W**(1 - gamma) / (1 - gamma)

u_low = W_low**(1 - gamma) / (1 - gamma)

u_high = W_high**(1 - gamma) / (1 - gamma)

E_U = 0.5 * u_low + 0.5 * u_high

CE = (E_U * (1 - gamma))**(1 / (1 - gamma))

E_W = 0.5 * W_low + 0.5 * W_high

risk_premium = E_W - CE

fig, ax = plt.subplots(figsize=(10, 6))

ax.plot(W, U, color='#2c3e50', linewidth=3)

ax.scatter([W_low, W_high], [u_low, u_high], color='#e74c3c', s=80, zorder=5)

ax.plot([W_low, W_high], [u_low, u_high], 'r--', alpha=0.5)

ax.axvline(CE, color='#27ae60', linestyle=':', alpha=0.7, label=f'CE = ${CE:.2f}')

ax.axvline(E_W, color='#2980b9', linestyle=':', alpha=0.7, label=f'E[W] = ${E_W:.2f}')

ax.set_xlabel('Wealth (W)', fontsize=12)

ax.set_ylabel('Utility U(W)', fontsize=12)

ax.set_title(f'CRRA Utility with γ = {gamma:.1f} | Risk Premium = ${risk_premium:.2f}', fontsize=14, fontweight='bold')

ax.legend(fontsize=11)

plt.tight_layout()

plt.show()

print(f"Try changing gamma to see how risk aversion affects the premium:")

print(f" γ = {gamma:.1f} → Risk Premium = ${risk_premium:.2f}")

Try changing gamma to see how risk aversion affects the premium:

γ = 2.0 → Risk Premium = $1.80

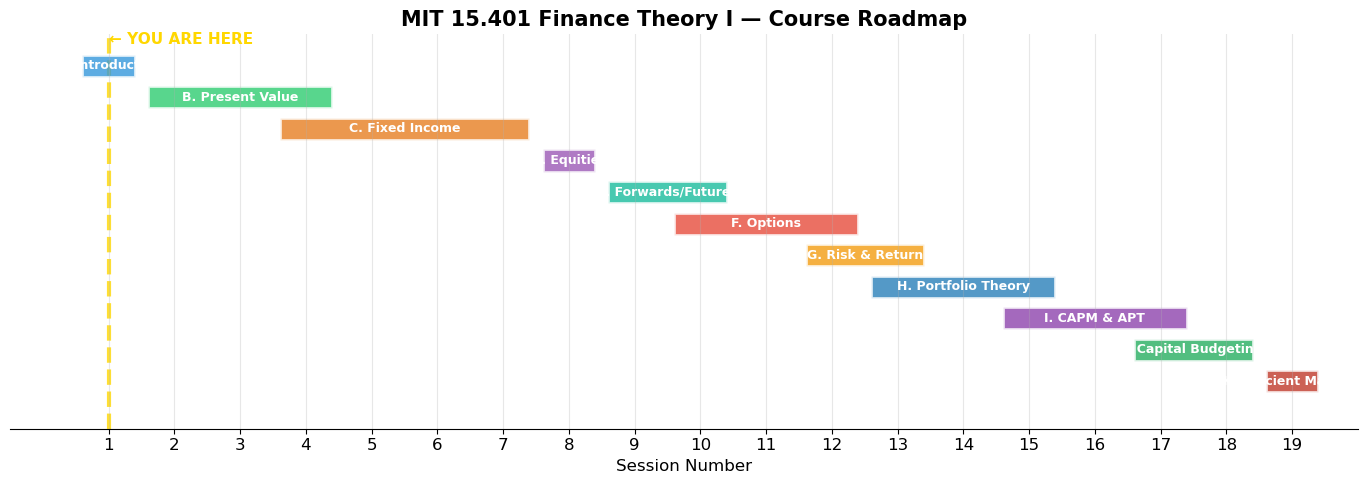

7. Course Overview — The Big Picture¶

Lo organizes the course into four major sections plus a capstone:

A. Introduction¶

Fundamental challenges, framework, six principles, time value of money

B. Valuation¶

NPV, pricing stocks, bonds, futures, forwards, and options

C. Risk¶

Measuring risk, Portfolio Theory (Markowitz), CAPM, APT

D. Corporate Finance¶

Capital budgeting and project finance

Final Lecture: Market Efficiency¶

EMH, behavioral biases, theory vs. practice

Source

# ============================================================

# Course Roadmap Visualization

# ============================================================

sessions = {

'A. Introduction': ([1], '#3498db'),

'B. Present Value': ([2, 3, 4], '#2ecc71'),

'C. Fixed Income': ([4, 5, 6, 7], '#e67e22'),

'D. Equities': ([8], '#9b59b6'),

'E. Forwards/Futures': ([9, 10], '#1abc9c'),

'F. Options': ([10, 11, 12], '#e74c3c'),

'G. Risk & Return': ([12, 13], '#f39c12'),

'H. Portfolio Theory': ([13, 14, 15], '#2980b9'),

'I. CAPM & APT': ([15, 16, 17], '#8e44ad'),

'J. Capital Budgeting':([17, 18], '#27ae60'),

'K. Efficient Markets':([19], '#c0392b'),

}

fig, ax = plt.subplots(figsize=(14, 5))

y_pos = 0

for name, (sess, color) in sessions.items():

start = min(sess) - 0.4

width = max(sess) - min(sess) + 0.8

rect = plt.Rectangle((start, y_pos - 0.35), width, 0.7,

facecolor=color, alpha=0.8, edgecolor='white', linewidth=2)

ax.add_patch(rect)

ax.text(start + width/2, y_pos, name, ha='center', va='center',

fontsize=9, fontweight='bold', color='white')

y_pos -= 1

ax.set_xlim(-0.5, 20)

ax.set_ylim(y_pos - 0.5, 1)

ax.set_xlabel('Session Number', fontsize=12)

ax.set_xticks(range(1, 20))

ax.set_yticks([])

ax.set_title('MIT 15.401 Finance Theory I — Course Roadmap', fontsize=15, fontweight='bold')

ax.spines['left'].set_visible(False)

ax.axvline(x=1, color='gold', linewidth=3, linestyle='--', alpha=0.8, zorder=0)

ax.text(1, 0.7, '← YOU ARE HERE', fontsize=11, fontweight='bold', color='gold')

plt.tight_layout()

plt.show()

“Finance Is One of The Most Difficult Subjects You Will Ever Love!” — Andrew Lo

8. Exercises¶

Exercise 1: The Power of Compounding¶

You invest $5,000 today at 6% annual interest, compounded annually.

(a) What will your investment be worth after 10, 20, and 30 years?

(b) How much of the 30-year final value comes from interest earned on interest (compounding effect vs. simple interest)?

(c) At what annual rate would you need to invest to double your money in exactly 10 years?

(d) Explain the Rule of 72: money doubles in approximately years. For which rates is it most accurate?

Source

# Exercise 1 — Workspace (uncomment and fill in)

# (a)

# principal, rate = 5000, 0.06

# for t in [10, 20, 30]:

# fv = principal * (1 + rate)**t

# print(f"After {t} years: ${fv:,.2f}")

# (b)

# compound_30 = principal * (1 + rate)**30

# simple_30 = principal * (1 + rate * 30)

# print(f"Compounding effect: ${compound_30 - simple_30:,.2f}")

# (c)

# r = 2**(1/10) - 1

# print(f"Required rate: {r:.4%}")

# (d) Test Rule of 72

# for r_pct in [2, 4, 6, 8, 10, 12, 15, 20]:

# approx = 72 / r_pct

# exact = np.log(2) / np.log(1 + r_pct/100)

# print(f"r={r_pct:>2d}%: Rule of 72 = {approx:>5.1f} yrs, Exact = {exact:>5.2f} yrs")Exercise 2: Risk Aversion and Certainty Equivalents¶

Consider an investor with CRRA utility . The investor faces a gamble: 50% chance of $3, 50% chance of $9.

(a) Calculate , , the certainty equivalent, and risk premium for .

(b) Plot the risk premium vs. from 0.1 to 10. What happens at the extremes?

(c) How does a 70/30 probability split (vs. 50/50) affect the risk premium?

Source

# Exercise 2 — Workspace (uncomment and fill in)

# def crra_utility(W, gamma):

# if abs(gamma - 1) < 1e-10:

# return np.log(W)

# return W**(1 - gamma) / (1 - gamma)

# def certainty_equivalent(E_U, gamma):

# if abs(gamma - 1) < 1e-10:

# return np.exp(E_U)

# return (E_U * (1 - gamma))**(1 / (1 - gamma))

# W_low, W_high, p = 3, 9, 0.5

# E_W = p * W_low + (1-p) * W_high

# for gamma in [0.5, 1, 2, 5]:

# E_U = p * crra_utility(W_low, gamma) + (1-p) * crra_utility(W_high, gamma)

# CE = certainty_equivalent(E_U, gamma)

# print(f"γ={gamma}: E[W]=${E_W:.2f}, CE=${CE:.2f}, Risk Premium=${E_W - CE:.2f}")Exercise 3: No-Arbitrage and the Law of One Price¶

Two assets with the following payoffs in one year:

| Asset | Boom | Recession | Price |

|---|---|---|---|

| A | $120 | $80 | $95 |

| B | $60 | $40 | $50 |

(a) Asset A pays exactly twice Asset B in every state. Is there an arbitrage?

(b) Describe the trading strategy and its cash flows.

(c) What happens to prices when many traders exploit this?

(d) With $2 transaction costs per trade, is the arbitrage still profitable?

Source

# Exercise 3 — Workspace (uncomment and fill in)

# (a)

# price_A, price_B = 95, 50

# fair_price_A = 2 * price_B

# print(f"Fair price of A (by LOP): ${fair_price_A}")

# print(f"Actual price: ${price_A}")

# print(f"Mispricing: ${fair_price_A - price_A}")

# (b)

# print("Strategy: Buy 1 unit of A ($95), Sell 2 units of B ($100)")

# print(f" Today: +${2*price_B - price_A}")

# print(f" Boom: ${120 - 2*60}")

# print(f" Recession: ${80 - 2*40}")References¶

Brealey, R.A., Myers, S.C., and Allen, F. Principles of Corporate Finance, Chapters 1–2.

Bernstein, P. (1993). Capital Ideas. New York: Free Press.

Lo, A.W. (1999). “The Three P’s of Total Risk Management.” Financial Analysts Journal, 55, 13–26.

MIT OCW 15.401: Course Homepage

Next lecture: Session 2 — Present Value Relations I, where we formalize the time value of money and develop the machinery of discounted cash flow analysis.