Lecture 6: Equities — Stock Valuation, the Dividend Discount Model, and Growth Opportunities

MIT 15.401 — Finance Theory I (Prof. Andrew Lo)¶

Video: MIT OCW — Equities

Readings: Brealey, Myers, and Allen — Chapter 4

This session transitions from fixed-income securities (known promised cash flows) to equities (uncertain cash flows). This is a major conceptual leap: unlike bonds, equity cash flows are not contractually fixed — dividends are uncertain in both magnitude and timing, and the terminal price is unknown. Yet the fundamental valuation framework remains the same: price = present value of expected future cash flows.

The workhorse model is the Dividend Discount Model (DDM), which values a stock as the present value of all future dividends. When we add a constant growth assumption, this becomes the Gordon Growth Model — one of the most famous formulas in finance: .

We then connect dividends to earnings through the payout ratio, define growth opportunities, and show how the P/E ratio decomposes into a no-growth component and the present value of growth opportunities (PVGO).

Table of Contents¶

Source

# ============================================================

# Setup

# ============================================================

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import matplotlib.ticker as mticker

from scipy.optimize import brentq

plt.rcParams.update({

'figure.figsize': (10, 5),

'axes.spines.top': False,

'axes.spines.right': False,

'axes.grid': True,

'grid.alpha': 0.3,

'font.size': 12,

'lines.linewidth': 2,

})

print("Libraries loaded successfully.")Libraries loaded successfully.

1. Industry Overview — The Equity Market¶

What Is Common Stock?¶

Common stock represents an ownership position (equity) in a corporation. Key characteristics:

Residual claimant: stockholders get paid after all other obligations (bondholders, employees, taxes). This makes equity riskier than debt — but also gives unlimited upside.

Limited liability: shareholders can lose at most their investment. They are not personally liable for corporate debts.

Voting rights: shareholders elect the board of directors.

Dividends: payouts in cash or stock, at the discretion of the board. Unlike bond coupons, dividends are not contractually guaranteed.

Access to public markets: shares can be bought and sold on exchanges.

Equity vs. Bonds — The Fundamental Distinction¶

| Feature | Bonds | Equities |

|---|---|---|

| Cash flows | Contractually fixed | Uncertain |

| Priority | Senior claim | Residual claim |

| Upside | Capped at face value | Unlimited |

| Downside | Loss if default | Can go to zero |

| Tax treatment | Interest is deductible | Dividends paid from after-tax income |

| Maturity | Finite | Perpetual |

Markets¶

Primary market: IPOs, SEOs, venture capital — companies raise capital by issuing new shares. Secondary market: NYSE, NASDAQ, AMEX — investors trade existing shares among themselves. The secondary market provides liquidity and price discovery.

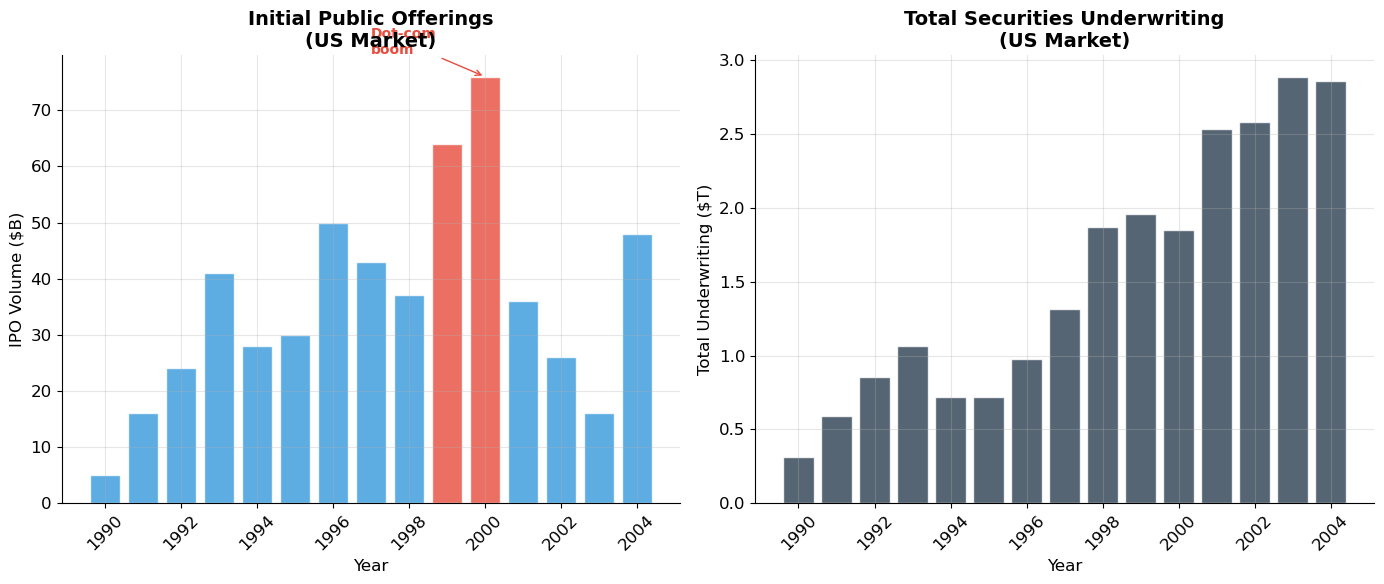

Source

# ============================================================

# Equity Market Scale — IPOs and Market Activity

# ============================================================

# Lo's slide data: IPO volume and total underwriting 1990-2004

years = list(range(1990, 2005))

ipo_volume = [5, 16, 24, 41, 28, 30, 50, 43, 37, 64, 76, 36, 26, 16, 48] # $B

total_underwriting = [312, 587, 856, 1063, 716, 722, 979, 1317, 1868, 1960, 1851, 2535, 2581, 2890, 2859]

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(14, 6))

# IPOs

colors_ipo = ['#e74c3c' if v > 60 else '#3498db' for v in ipo_volume]

ax1.bar(years, ipo_volume, color=colors_ipo, alpha=0.8, edgecolor='white')

ax1.set_xlabel('Year', fontsize=12)

ax1.set_ylabel('IPO Volume ($B)', fontsize=12)

ax1.set_title('Initial Public Offerings\n(US Market)', fontsize=14, fontweight='bold')

ax1.tick_params(axis='x', rotation=45)

# Highlight dot-com boom

ax1.annotate('Dot-com\nboom', xy=(2000, 76), xytext=(1997, 80),

fontsize=10, color='#e74c3c', fontweight='bold',

arrowprops=dict(arrowstyle='->', color='#e74c3c'))

# Total underwriting

ax2.bar(years, [v/1000 for v in total_underwriting], color='#2c3e50', alpha=0.8, edgecolor='white')

ax2.set_xlabel('Year', fontsize=12)

ax2.set_ylabel('Total Underwriting ($T)', fontsize=12)

ax2.set_title('Total Securities Underwriting\n(US Market)', fontsize=14, fontweight='bold')

ax2.tick_params(axis='x', rotation=45)

plt.tight_layout()

plt.show()

2. The Dividend Discount Model (DDM)¶

The Core Idea¶

How should we value a stock? The same way we value any asset: as the present value of its future cash flows. For a stock, the relevant cash flows are dividends.

One-Period Model¶

If you hold a stock for one period, you receive a dividend and sell at price :

But what determines ? The next investor’s expected dividend and resale price:

Multi-Period Model¶

Substituting recursively and pushing the terminal price to infinity:

This is the Dividend Discount Model: the stock price equals the present value of all future dividends, to infinity.

Key Assumptions (for the basic version)¶

Constant discount rate across all periods

Dividends are the only relevant cash flows to equity holders

The terminal price grows slower than the discount rate (ensuring convergence)

Critical insight: Even though any individual investor may hold the stock for a short period and sell it, the price today still equals the PV of all future dividends — because the price the next investor pays is itself based on future dividends.

Source

# ============================================================

# One-Period vs. Multi-Period DDM — Equivalence Demonstration

# ============================================================

def ddm_general(dividends, terminal_price, r):

"""Value a stock from a finite list of dividends plus terminal price."""

T = len(dividends)

pv = sum(D / (1 + r)**t for t, D in enumerate(dividends, 1))

pv += terminal_price / (1 + r)**T

return pv

# Example: constant dividend stream, showing equivalence

r = 0.12

D = 2.00 # constant dividend forever

# Investor 1: holds for 1 year

# P1 = D/r (perpetuity from year 2 onward)

P1 = D / r

P0_1period = ddm_general([D], P1, r)

# Investor 2: holds for 5 years

P5 = D / r # same perpetuity from year 6

P0_5period = ddm_general([D]*5, P5, r)

# Investor 3: holds forever (perpetuity formula)

P0_forever = D / r

print("=" * 60)

print("DDM EQUIVALENCE: Holding Period Doesn't Matter")

print(f"Constant dividend D = ${D:.2f}, discount rate r = {r:.0%}")

print("=" * 60)

print(f"1-year holding period: P₀ = (D₁ + P₁)/(1+r) = ({D} + {P1:.2f})/1.12 = ${P0_1period:.4f}")

print(f"5-year holding period: P₀ = Σ PV(D) + PV(P₅) = ${P0_5period:.4f}")

print(f"Infinite holding: P₀ = D/r = {D}/{r} = ${P0_forever:.4f}")

print(f"\n→ All methods give P₀ = ${D/r:.2f} regardless of holding period ✓")

print(f" The stock price today reflects ALL future dividends, not just")

print(f" the dividends you personally will receive while holding it.")============================================================

DDM EQUIVALENCE: Holding Period Doesn't Matter

Constant dividend D = $2.00, discount rate r = 12%

============================================================

1-year holding period: P₀ = (D₁ + P₁)/(1+r) = (2.0 + 16.67)/1.12 = $16.6667

5-year holding period: P₀ = Σ PV(D) + PV(P₅) = $16.6667

Infinite holding: P₀ = D/r = 2.0/0.12 = $16.6667

→ All methods give P₀ = $16.67 regardless of holding period ✓

The stock price today reflects ALL future dividends, not just

the dividends you personally will receive while holding it.

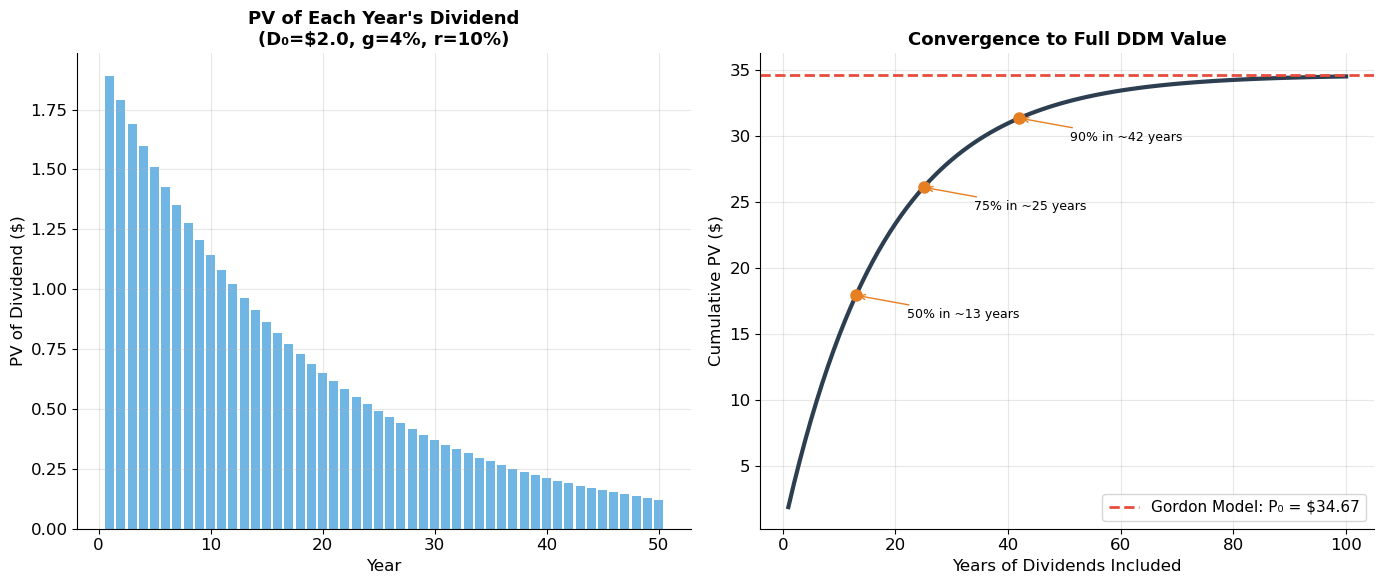

Source

# ============================================================

# DDM Convergence: How Much Value Comes From Near vs. Far Dividends?

# ============================================================

# ▶ MODIFY AND RE-RUN

D = 2.00

r = 0.10

g = 0.04 # growth rate

# ============================================================

# Gordon Growth Model value

P0 = D * (1 + g) / (r - g)

# Cumulative PV of dividends from year 1 to T

T_max = 100

cumulative_pv = np.zeros(T_max)

for t in range(1, T_max + 1):

Dt = D * (1 + g)**t

cumulative_pv[t-1] = cumulative_pv[t-2] + Dt / (1 + r)**t if t > 1 else Dt / (1 + r)

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(14, 6))

# Left: Individual PV contributions

T_show = 50

pvs = [D * (1 + g)**t / (1 + r)**t for t in range(1, T_show + 1)]

ax1.bar(range(1, T_show + 1), pvs, color='#3498db', alpha=0.7, width=0.8)

ax1.set_xlabel('Year', fontsize=12)

ax1.set_ylabel('PV of Dividend ($)', fontsize=12)

ax1.set_title(f'PV of Each Year\'s Dividend\n(D₀=${D}, g={g:.0%}, r={r:.0%})', fontsize=13, fontweight='bold')

# Right: Cumulative

years = np.arange(1, T_max + 1)

ax2.plot(years, cumulative_pv, color='#2c3e50', linewidth=3)

ax2.axhline(y=P0, color='#e74c3c', linewidth=2, linestyle='--', label=f'Gordon Model: P₀ = ${P0:.2f}')

# Milestones

for pct in [0.5, 0.75, 0.9]:

idx = np.searchsorted(cumulative_pv, P0 * pct)

if idx < T_max:

ax2.plot(idx + 1, cumulative_pv[idx], 'o', color='#e67e22', markersize=8, zorder=5)

ax2.annotate(f'{pct:.0%} in ~{idx+1} years', xy=(idx + 1, cumulative_pv[idx]),

xytext=(idx + 10, cumulative_pv[idx] - P0 * 0.05), fontsize=9,

arrowprops=dict(arrowstyle='->', color='#e67e22'))

ax2.set_xlabel('Years of Dividends Included', fontsize=12)

ax2.set_ylabel('Cumulative PV ($)', fontsize=12)

ax2.set_title('Convergence to Full DDM Value', fontsize=13, fontweight='bold')

ax2.legend(fontsize=11)

plt.tight_layout()

plt.show()

for pct in [0.5, 0.75, 0.9, 0.95]:

idx = np.searchsorted(cumulative_pv, P0 * pct) + 1

print(f" {pct:.0%} of value captured in first {idx:>3d} years")

50% of value captured in first 13 years

75% of value captured in first 25 years

90% of value captured in first 42 years

95% of value captured in first 54 years

3. The Gordon Growth Model¶

Derivation¶

If dividends grow at a constant rate forever, with :

The DDM becomes a growing perpetuity (which we derived in Session 2):

This is the Gordon Growth Model (Gordon, 1959) — perhaps the single most important formula in equity valuation.

Lo’s Example (Slide 10)¶

Dividends grow at per year, current dividend , expected return :

The Three Determinants of Stock Price¶

The Gordon model reveals that stock price depends on exactly three things:

(expected next dividend): higher dividends → higher price

(required return / cost of equity): higher risk → lower price

(dividend growth rate): higher growth → higher price

And the model gives a precise formula for how sensitive the price is to each.

Source

# ============================================================

# Gordon Growth Model — Core Calculations

# ============================================================

def gordon_growth_price(D0, r, g):

"""Gordon Growth Model: P0 = D0*(1+g)/(r-g). Requires r > g."""

if r <= g:

return float('inf')

return D0 * (1 + g) / (r - g)

# Lo's example

D0 = 1.00

r = 0.20

g = 0.06

P0 = gordon_growth_price(D0, r, g)

print("=" * 60)

print("GORDON GROWTH MODEL — Lo's Example")

print("=" * 60)

print(f"Current dividend D₀ = ${D0:.2f}")

print(f"Growth rate g = {g:.0%}")

print(f"Required return r = {r:.0%}")

print(f"\nP₀ = D₀(1+g)/(r-g) = ${D0}×{1+g:.2f}/({r:.2f}-{g:.2f}) = ${P0:.2f}")

# Sensitivity table

print(f"\n{'':>8s}", end='')

for g_val in [0.02, 0.04, 0.06, 0.08, 0.10, 0.12]:

print(f"{'g='+f'{g_val:.0%}':>9s}", end='')

print()

print("-" * 62)

for r_val in [0.12, 0.14, 0.16, 0.18, 0.20, 0.25]:

print(f"r={r_val:.0%} ", end='')

for g_val in [0.02, 0.04, 0.06, 0.08, 0.10, 0.12]:

if r_val > g_val:

p = gordon_growth_price(1.0, r_val, g_val)

print(f" ${p:>6.2f}", end='')

else:

print(f" ∞ ", end='')

print()

print("\nKey insight: Price is EXTREMELY sensitive to (r-g).")

print("A small change in growth or discount rate has a massive impact on valuation.")============================================================

GORDON GROWTH MODEL — Lo's Example

============================================================

Current dividend D₀ = $1.00

Growth rate g = 6%

Required return r = 20%

P₀ = D₀(1+g)/(r-g) = $1.0×1.06/(0.20-0.06) = $7.57

g=2% g=4% g=6% g=8% g=10% g=12%

--------------------------------------------------------------

r=12% $ 10.20 $ 13.00 $ 17.67 $ 27.00 $ 55.00 ∞

r=14% $ 8.50 $ 10.40 $ 13.25 $ 18.00 $ 27.50 $ 56.00

r=16% $ 7.29 $ 8.67 $ 10.60 $ 13.50 $ 18.33 $ 28.00

r=18% $ 6.38 $ 7.43 $ 8.83 $ 10.80 $ 13.75 $ 18.67

r=20% $ 5.67 $ 6.50 $ 7.57 $ 9.00 $ 11.00 $ 14.00

r=25% $ 4.43 $ 4.95 $ 5.58 $ 6.35 $ 7.33 $ 8.62

Key insight: Price is EXTREMELY sensitive to (r-g).

A small change in growth or discount rate has a massive impact on valuation.

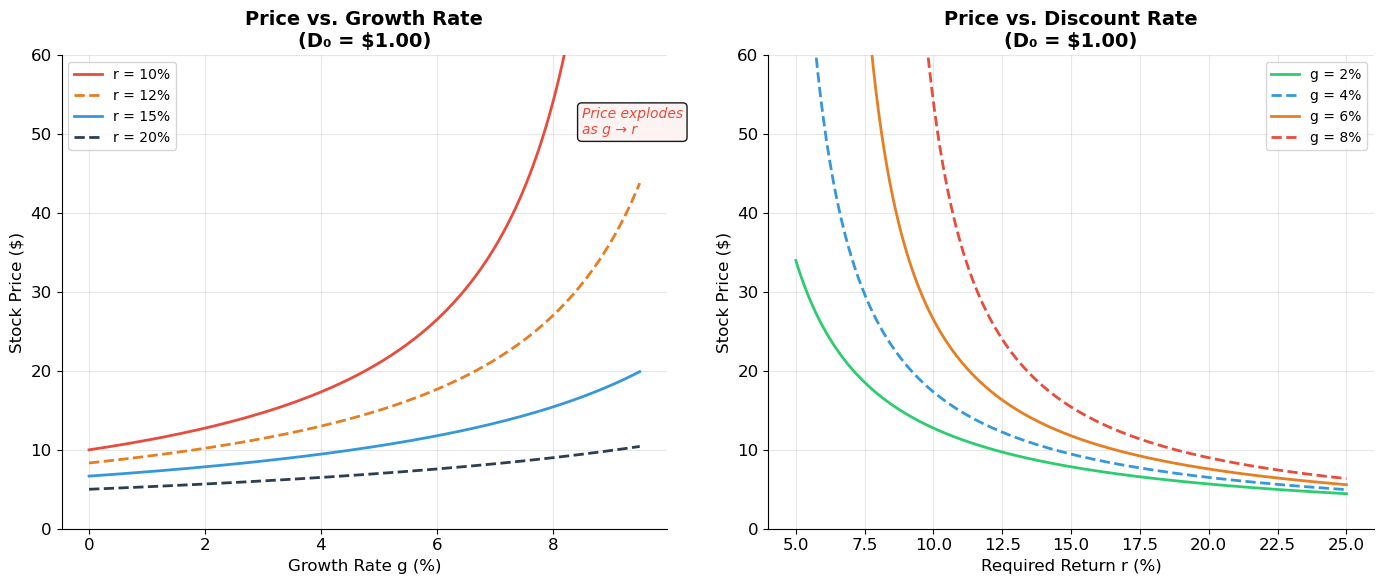

Source

# ============================================================

# Sensitivity Analysis: Price vs. Growth Rate and Discount Rate

# ============================================================

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(14, 6))

# Left: Price vs. growth rate (fixed r)

g_range = np.linspace(0, 0.095, 200)

for r_val, color, ls in [(0.10, '#e74c3c', '-'), (0.12, '#e67e22', '--'),

(0.15, '#3498db', '-'), (0.20, '#2c3e50', '--')]:

prices = [gordon_growth_price(1.0, r_val, g) for g in g_range]

ax1.plot(g_range * 100, prices, color=color, linewidth=2, linestyle=ls,

label=f'r = {r_val:.0%}')

ax1.set_xlabel('Growth Rate g (%)', fontsize=12)

ax1.set_ylabel('Stock Price ($)', fontsize=12)

ax1.set_title('Price vs. Growth Rate\n(D₀ = $1.00)', fontsize=14, fontweight='bold')

ax1.set_ylim(0, 60)

ax1.legend(fontsize=10)

ax1.annotate('Price explodes\nas g → r', xy=(8.5, 50), fontsize=10, color='#e74c3c',

style='italic', bbox=dict(boxstyle='round', facecolor='#fdf2f2', alpha=0.9))

# Right: Price vs. discount rate (fixed g)

r_range = np.linspace(0.05, 0.25, 200)

for g_val, color, ls in [(0.02, '#2ecc71', '-'), (0.04, '#3498db', '--'),

(0.06, '#e67e22', '-'), (0.08, '#e74c3c', '--')]:

prices = [gordon_growth_price(1.0, r, g_val) if r > g_val else np.nan for r in r_range]

ax2.plot(r_range * 100, prices, color=color, linewidth=2, linestyle=ls,

label=f'g = {g_val:.0%}')

ax2.set_xlabel('Required Return r (%)', fontsize=12)

ax2.set_ylabel('Stock Price ($)', fontsize=12)

ax2.set_title('Price vs. Discount Rate\n(D₀ = $1.00)', fontsize=14, fontweight='bold')

ax2.set_ylim(0, 60)

ax2.legend(fontsize=10)

plt.tight_layout()

plt.show()

print("The Gordon model has a singularity at g = r (price → ∞).")

print("In practice, g must be STRICTLY less than r for the model to be valid.")

print("For mature companies, g should not exceed nominal GDP growth (roughly 4-6%).")

The Gordon model has a singularity at g = r (price → ∞).

In practice, g must be STRICTLY less than r for the model to be valid.

For mature companies, g should not exceed nominal GDP growth (roughly 4-6%).

4. Estimating the Cost of Equity from the DDM¶

Rearranging the Gordon Model¶

The Gordon model can be solved for the discount rate (cost of equity):

This decomposition is intuitive: the return to an equity investor comes from two sources:

Dividend yield (): income from dividends

Capital gains (): price appreciation

Lo’s Duke Power Example (Slide 11)¶

In September 1992, Duke Power had:

Dividend yield:

Growth estimates: Value Line (5.0%), IBES (5.5%), historical (4.1%)

Using different growth estimates:

| Source | ≈ | ||

|---|---|---|---|

| Value Line | 5.0% | ~5.5% | ~10.5% |

| IBES | 5.5% | ~5.5% | ~11.0% |

| Historical | 4.1% | ~5.4% | ~9.5% |

The cost of equity for a utility like Duke Power: roughly 10–11%.

Source

# ============================================================

# Cost of Equity Estimation — Duke Power Example

# ============================================================

D0_P0 = 0.052 # current dividend yield

growth_estimates = {

'Value Line': 0.050,

'IBES Consensus': 0.055,

'Historical': 0.041,

}

print("=" * 60)

print("COST OF EQUITY — Duke Power (September 1992)")

print("=" * 60)

print(f"Current dividend yield D₀/P₀ = {D0_P0:.1%}")

print()

print(f"{'Source':>18s} {'g':>8s} {'D₁/P₀':>10s} {'r = D₁/P₀ + g':>15s}")

print("-" * 55)

r_estimates = []

for source, g in growth_estimates.items():

D1_P0 = D0_P0 * (1 + g)

r = D1_P0 + g

r_estimates.append(r)

print(f"{source:>18s} {g:>8.1%} {D1_P0:>10.2%} {r:>15.2%}")

print(f"\nRange of cost of equity estimates: {min(r_estimates):.1%} to {max(r_estimates):.1%}")

print(f"Average: {np.mean(r_estimates):.1%}")

print("\nNote: Duke Power is a regulated utility — low risk, stable dividends.")

print("Its cost of equity is correspondingly modest (~10%) compared to")

print("high-growth tech firms (which might have r = 15-20%).")============================================================

COST OF EQUITY — Duke Power (September 1992)

============================================================

Current dividend yield D₀/P₀ = 5.2%

Source g D₁/P₀ r = D₁/P₀ + g

-------------------------------------------------------

Value Line 5.0% 5.46% 10.46%

IBES Consensus 5.5% 5.49% 10.99%

Historical 4.1% 5.41% 9.51%

Range of cost of equity estimates: 9.5% to 11.0%

Average: 10.3%

Note: Duke Power is a regulated utility — low risk, stable dividends.

Its cost of equity is correspondingly modest (~10%) compared to

high-growth tech firms (which might have r = 15-20%).

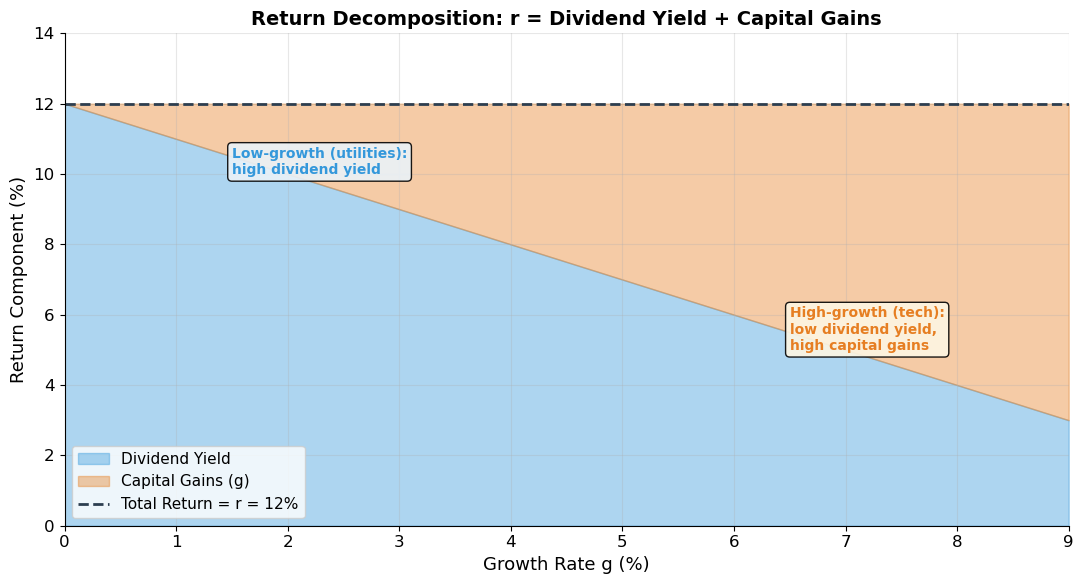

Source

# ============================================================

# Return Decomposition: Dividend Yield vs. Capital Gains

# ============================================================

# Show how return composition changes with growth rate

g_range = np.linspace(0, 0.09, 200)

r_fixed = 0.12

D0 = 1.0

div_yields = np.array([D0 * (1 + g) / gordon_growth_price(D0, r_fixed, g) if r_fixed > g else np.nan for g in g_range])

cap_gains = g_range

fig, ax = plt.subplots(figsize=(11, 6))

ax.fill_between(g_range * 100, 0, div_yields * 100, alpha=0.4, color='#3498db', label='Dividend Yield')

ax.fill_between(g_range * 100, div_yields * 100, (div_yields + cap_gains) * 100,

alpha=0.4, color='#e67e22', label='Capital Gains (g)')

ax.axhline(y=r_fixed * 100, color='#2c3e50', linewidth=2, linestyle='--', label=f'Total Return = r = {r_fixed:.0%}')

ax.set_xlabel('Growth Rate g (%)', fontsize=13)

ax.set_ylabel('Return Component (%)', fontsize=13)

ax.set_title('Return Decomposition: r = Dividend Yield + Capital Gains',

fontsize=14, fontweight='bold')

ax.legend(fontsize=11)

ax.set_ylim(0, 14)

ax.set_xlim(0, 9)

# Annotations

ax.annotate('Low-growth (utilities):\nhigh dividend yield', xy=(1.5, 10), fontsize=10,

color='#3498db', fontweight='bold',

bbox=dict(boxstyle='round', facecolor='#eaf2f8', alpha=0.9))

ax.annotate('High-growth (tech):\nlow dividend yield,\nhigh capital gains', xy=(6.5, 5), fontsize=10,

color='#e67e22', fontweight='bold',

bbox=dict(boxstyle='round', facecolor='#fdf6e3', alpha=0.9))

plt.tight_layout()

plt.show()

print("The total return is always r (by the Gordon model: r = D₁/P₀ + g).")

print("As growth increases, the mix shifts from dividend yield to capital gains.")

print("This is why growth stocks have low dividend yields — it's not a flaw!")

The total return is always r (by the Gordon model: r = D₁/P₀ + g).

As growth increases, the mix shifts from dividend yield to capital gains.

This is why growth stocks have low dividend yields — it's not a flaw!

5. Multi-Stage Growth Models¶

Why Multi-Stage?¶

The constant-growth assumption is unrealistic for many companies. Firms typically pass through distinct phases:

Growth stage: rapid expansion, high profit margins, heavy reinvestment, low dividend payout

Transition stage: competition erodes margins, growth slows, investment opportunities decline

Mature stage: stable growth, high payout ratio, earnings grow at or below GDP rate

Two-Stage DDM¶

The most common variant assumes high growth for years, then stable growth forever:

where the terminal value uses the Gordon model:

Lo’s Example (Slide 12)¶

A company with , grows at for 7 years, then thereafter.

Source

# ============================================================

# Two-Stage Growth DDM

# ============================================================

def two_stage_ddm(D0, r, g_high, T_high, g_low):

"""Two-stage DDM: high growth for T years, then stable growth forever."""

# Phase 1: high-growth dividends

phase1_pv = 0

DT = D0

for t in range(1, T_high + 1):

DT = D0 * (1 + g_high)**t

phase1_pv += DT / (1 + r)**t

# Phase 2: terminal value using Gordon model

D_terminal = DT * (1 + g_low)

P_T = D_terminal / (r - g_low) if r > g_low else float('inf')

phase2_pv = P_T / (1 + r)**T_high

return phase1_pv, phase2_pv, phase1_pv + phase2_pv

# Lo's example

D0 = 1.00

r = 0.20

g_H = 0.06

T = 7

g_L = 0.00

pv1, pv2, P0 = two_stage_ddm(D0, r, g_H, T, g_L)

print("=" * 60)

print("TWO-STAGE DDM — Lo's Example")

print("=" * 60)

print(f"D₀ = ${D0:.2f}, r = {r:.0%}, g_H = {g_H:.0%} (years 1–{T}), g_L = {g_L:.0%} (year {T+1}+)")

print()

# Show dividend timeline

print("Dividend timeline:")

for t in range(1, T + 2):

Dt = D0 * (1 + g_H)**min(t, T)

if t > T:

Dt = D0 * (1 + g_H)**T * (1 + g_L)

phase = "← high growth" if t <= T else "← stable"

print(f" D_{t} = ${Dt:.4f} {phase}")

if t == T + 1:

break

# Terminal price

D_T = D0 * (1 + g_H)**T

P_T = D_T * (1 + g_L) / (r - g_L)

print(f"\nTerminal value at T={T}: P_{T} = D_{T+1}/(r-g_L) = ${D_T*(1+g_L):.4f}/{r-g_L:.2f} = ${P_T:.2f}")

print(f"\nPV of high-growth dividends (years 1–{T}): ${pv1:.4f}")

print(f"PV of terminal value: ${pv2:.4f}")

print(f"Total stock price P₀: ${P0:.4f}")

print(f"\nTerminal value share: {pv2/(pv1+pv2)*100:.1f}% of total value")

# Compare with pure Gordon models

P0_allhigh = gordon_growth_price(D0, r, g_H)

P0_no_growth = D0 * (1 + 0) / (r - 0) # g=0 forever

print(f"\nComparison:")

print(f" If g = {g_H:.0%} forever: P₀ = ${P0_allhigh:.2f}")

print(f" Two-stage model: P₀ = ${P0:.2f}")

print(f" If g = {g_L:.0%} forever: P₀ = ${P0_no_growth:.2f}")============================================================

TWO-STAGE DDM — Lo's Example

============================================================

D₀ = $1.00, r = 20%, g_H = 6% (years 1–7), g_L = 0% (year 8+)

Dividend timeline:

D_1 = $1.0600 ← high growth

D_2 = $1.1236 ← high growth

D_3 = $1.1910 ← high growth

D_4 = $1.2625 ← high growth

D_5 = $1.3382 ← high growth

D_6 = $1.4185 ← high growth

D_7 = $1.5036 ← high growth

D_8 = $1.5036 ← stable

Terminal value at T=7: P_7 = D_8/(r-g_L) = $1.5036/0.20 = $7.52

PV of high-growth dividends (years 1–7): $4.3942

PV of terminal value: $2.0982

Total stock price P₀: $6.4924

Terminal value share: 32.3% of total value

Comparison:

If g = 6% forever: P₀ = $7.57

Two-stage model: P₀ = $6.49

If g = 0% forever: P₀ = $5.00

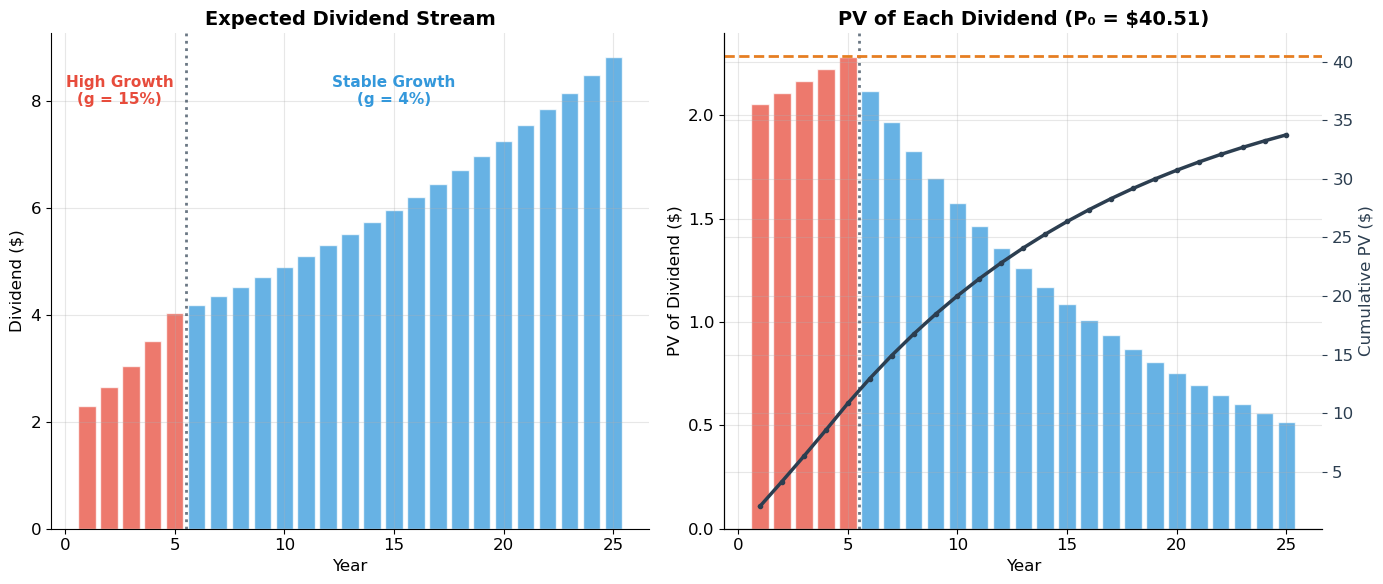

Source

# ============================================================

# Visualization: Two-Stage DDM Cash Flows and Valuation

# ============================================================

# ▶ MODIFY AND RE-RUN

D0 = 2.00

r = 0.12

g_high = 0.15 # high-growth phase

T_high = 5 # years of high growth

g_low = 0.04 # stable growth

# ============================================================

pv1, pv2, P0 = two_stage_ddm(D0, r, g_high, T_high, g_low)

# Build dividend series

T_plot = 25

divs = []

pvs = []

for t in range(1, T_plot + 1):

if t <= T_high:

Dt = D0 * (1 + g_high)**t

else:

Dt = D0 * (1 + g_high)**T_high * (1 + g_low)**(t - T_high)

divs.append(Dt)

pvs.append(Dt / (1 + r)**t)

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(14, 6))

# Left: Dividend timeline

years_plot = range(1, T_plot + 1)

colors_bar = ['#e74c3c' if t <= T_high else '#3498db' for t in years_plot]

ax1.bar(years_plot, divs, color=colors_bar, alpha=0.75, edgecolor='white')

ax1.axvline(x=T_high + 0.5, color='#2c3e50', linewidth=2, linestyle=':', alpha=0.7)

ax1.text(T_high / 2, max(divs) * 0.9, f'High Growth\n(g = {g_high:.0%})',

ha='center', fontsize=11, color='#e74c3c', fontweight='bold')

ax1.text(T_high + (T_plot - T_high) / 2, max(divs) * 0.9, f'Stable Growth\n(g = {g_low:.0%})',

ha='center', fontsize=11, color='#3498db', fontweight='bold')

ax1.set_xlabel('Year', fontsize=12)

ax1.set_ylabel('Dividend ($)', fontsize=12)

ax1.set_title('Expected Dividend Stream', fontsize=14, fontweight='bold')

# Right: PV contributions

ax2.bar(years_plot, pvs, color=colors_bar, alpha=0.75, edgecolor='white')

ax2.axvline(x=T_high + 0.5, color='#2c3e50', linewidth=2, linestyle=':', alpha=0.7)

# Show cumulative reaching total

cumulative = np.cumsum(pvs)

ax2_twin = ax2.twinx()

ax2_twin.plot(years_plot, cumulative, color='#2c3e50', linewidth=2.5, marker='o', markersize=3)

ax2_twin.axhline(y=P0, color='#e67e22', linewidth=2, linestyle='--')

ax2_twin.set_ylabel('Cumulative PV ($)', fontsize=12, color='#2c3e50')

ax2_twin.tick_params(axis='y', colors='#2c3e50')

ax2.set_xlabel('Year', fontsize=12)

ax2.set_ylabel('PV of Dividend ($)', fontsize=12)

ax2.set_title(f'PV of Each Dividend (P₀ = ${P0:.2f})', fontsize=14, fontweight='bold')

plt.tight_layout()

plt.show()

print(f"Two-stage DDM: P₀ = ${P0:.2f}")

print(f" PV of high-growth dividends: ${pv1:.2f} ({pv1/P0*100:.1f}%)")

print(f" PV of terminal value: ${pv2:.2f} ({pv2/P0*100:.1f}%)")

print(f"\nThe terminal value typically dominates — most of a stock's value")

print(f"comes from the LONG-RUN growth phase, not the near-term high growth.")

Two-stage DDM: P₀ = $40.51

PV of high-growth dividends: $10.83 (26.7%)

PV of terminal value: $29.67 (73.3%)

The terminal value typically dominates — most of a stock's value

comes from the LONG-RUN growth phase, not the near-term high growth.

6. EPS, P/E, and the Link to Earnings¶

From Dividends to Earnings¶

In practice, forecasting individual dividends is difficult. Analysts often work with earnings and payout ratios instead.

Key Definitions¶

| Concept | Symbol | Definition |

|---|---|---|

| Earnings per share | EPS | Net income / shares outstanding |

| Payout ratio | DPS / EPS (fraction of earnings paid as dividends) | |

| Plowback (retention) ratio | 1 − (fraction reinvested) | |

| Book value per share | BV | Cumulative retained earnings per share |

| Return on book equity | ROE | EPS / BV |

The Sustainable Growth Rate¶

If a company reinvests fraction of earnings at return ROE:

This is the sustainable growth rate — the rate at which earnings (and dividends) can grow without external financing.

Lo’s Texas Western Example (Slides 14–16)¶

Texas Western (TW) has:

Expected EPS₁ = $1.00, Book Value = $10.00

Plans to grow net book assets by 8% per year (financed by retained earnings)

Discount rate = 10% = ROE

Key ratios:

Plowback ratio:

Payout ratio:

ROE = EPS / BV = 1/10 = 10%

Sustainable growth: ✓

Source

# ============================================================

# Texas Western Example — EPS, Growth, and Valuation

# ============================================================

# Company parameters

EPS1 = 1.00

BV0 = 10.00

g = 0.08

r = 0.10

ROE = EPS1 / BV0 # = 10%

b = BV0 * g / EPS1 # plowback ratio

p = 1 - b # payout ratio

D1 = EPS1 * p # dividend per share

print("=" * 60)

print("TEXAS WESTERN — Lo's Example")

print("=" * 60)

print(f"EPS₁ = ${EPS1:.2f}, BV₀ = ${BV0:.2f}")

print(f"ROE = EPS/BV = {ROE:.0%}")

print(f"Growth rate g = {g:.0%}")

print(f"Plowback ratio b = {b:.2f}")

print(f"Payout ratio p = {p:.2f}")

print(f"DPS₁ = EPS × p = ${D1:.2f}")

print(f"Sustainable growth: b × ROE = {b:.2f} × {ROE:.2f} = {b * ROE:.0%} = g ✓")

# CASE 1: Expand at 8% forever

P0_case1 = D1 / (r - g)

print(f"\nCase 1: Expand at {g:.0%} forever")

print(f" P₀ = D₁/(r-g) = {D1}/{r}-{g} = ${P0_case1:.2f}")

print(f" P/E = {P0_case1/EPS1:.1f}×")

# CASE 2: Growth slows to 4% after year 5

g_high = 0.08

g_low = 0.04

T_trans = 5

# Build explicit year-by-year forecast

print(f"\nCase 2: {g_high:.0%} for {T_trans} years, then {g_low:.0%}")

print(f"\n{'Year':>6s} {'BV_start':>10s} {'EPS':>8s} {'Inv':>8s} {'DPS':>8s} {'b':>6s}")

print("-" * 55)

# Phase 1

BV_t = BV0

EPS_t = EPS1

pv_divs = 0

for t in range(1, T_trans + 1):

EPS_t = BV_t * ROE

inv_t = BV_t * g_high

D_t = EPS_t - inv_t

pv_divs += D_t / (1 + r)**t

b_t = inv_t / EPS_t

print(f"{t:>6d} {BV_t:>10.4f} {EPS_t:>8.4f} {inv_t:>8.4f} {D_t:>8.4f} {b_t:>6.2f}")

BV_t = BV_t * (1 + g_high)

# Terminal value: from year T+1, ROE still 10% but growth drops to 4%

# New plowback: b_new = g_low / ROE

b_new = g_low / ROE

p_new = 1 - b_new

EPS_T1 = BV_t * ROE

D_T1 = EPS_T1 * p_new

P_T = D_T1 / (r - g_low)

pv_terminal = P_T / (1 + r)**T_trans

P0_case2 = pv_divs + pv_terminal

print(f"\nAt year {T_trans+1}: EPS = ${EPS_T1:.4f}, new payout = {p_new:.0%}, DPS = ${D_T1:.4f}")

print(f"Terminal price: P_{T_trans} = ${P_T:.2f}")

print(f"\nPV of dividends (years 1-{T_trans}): ${pv_divs:.2f}")

print(f"PV of terminal value: ${pv_terminal:.2f}")

print(f"Stock price P₀: ${P0_case2:.2f}")

print(f"P/E = {P0_case2/EPS1:.1f}×")

print(f"\n→ BOTH cases give P₀ = ${P0_case1:.2f}! Why?")

print(f" Because ROE = r = {ROE:.0%}. When the firm earns EXACTLY its cost of")

print(f" capital on new investments, growth adds NO value.")

print(f" Price = EPS₁/r = ${EPS1/r:.2f} regardless of growth strategy.")============================================================

TEXAS WESTERN — Lo's Example

============================================================

EPS₁ = $1.00, BV₀ = $10.00

ROE = EPS/BV = 10%

Growth rate g = 8%

Plowback ratio b = 0.80

Payout ratio p = 0.20

DPS₁ = EPS × p = $0.20

Sustainable growth: b × ROE = 0.80 × 0.10 = 8% = g ✓

Case 1: Expand at 8% forever

P₀ = D₁/(r-g) = 0.19999999999999996/0.1-0.08 = $10.00

P/E = 10.0×

Case 2: 8% for 5 years, then 4%

Year BV_start EPS Inv DPS b

-------------------------------------------------------

1 10.0000 1.0000 0.8000 0.2000 0.80

2 10.8000 1.0800 0.8640 0.2160 0.80

3 11.6640 1.1664 0.9331 0.2333 0.80

4 12.5971 1.2597 1.0078 0.2519 0.80

5 13.6049 1.3605 1.0884 0.2721 0.80

At year 6: EPS = $1.4693, new payout = 60%, DPS = $0.8816

Terminal price: P_5 = $14.69

PV of dividends (years 1-5): $0.88

PV of terminal value: $9.12

Stock price P₀: $10.00

P/E = 10.0×

→ BOTH cases give P₀ = $10.00! Why?

Because ROE = r = 10%. When the firm earns EXACTLY its cost of

capital on new investments, growth adds NO value.

Price = EPS₁/r = $10.00 regardless of growth strategy.

7. Growth Opportunities and Growth Stocks¶

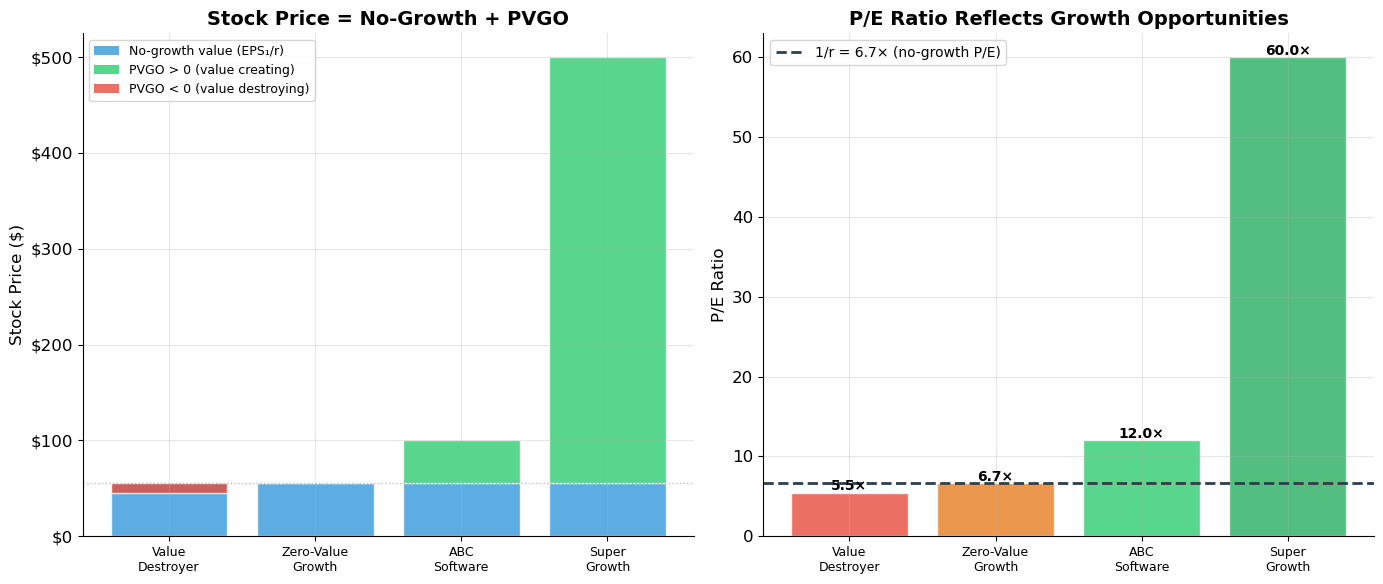

The PVGO Decomposition¶

Lo shows that any stock price can be decomposed into two components:

No-growth value (): the price if the firm distributed all earnings as dividends — no reinvestment, no growth

PVGO (Present Value of Growth Opportunities): the additional value created by reinvesting at returns above the cost of capital

When Does Growth Create Value?¶

Growth is valuable only when ROE > r — that is, when the firm can reinvest at a rate of return that exceeds what investors require.

If ROE = : PVGO = 0, and (the Texas Western result!)

If ROE < : PVGO < 0, and growth actually destroys value. The firm would be worth more if it stopped investing and paid out all earnings.

What Is a “Growth Stock”?¶

A growth stock is NOT merely a stock with growing EPS, growing dividends, or growing assets. It is a stock of a company with access to investments earning more than the cost of capital (ROE > ), so PVGO > 0.

Counterintuitively:

A stock with fast-growing EPS might NOT be a growth stock (if ROE < )

A stock with slow-growing EPS MIGHT be a growth stock (if ROE > )

The P/E Ratio and PVGO¶

Dividing both sides by :

This explains why high P/E ratios indicate growth stocks: P/E > 1/r implies PVGO > 0.

Source

# ============================================================

# Lo's ABC Software Example — PVGO Decomposition

# ============================================================

# From slide 18

EPS1_abc = 8.33

p_abc = 0.6 # payout ratio

ROE_abc = 0.25 # return on equity

r_abc = 0.15 # cost of capital

b_abc = 1 - p_abc # plowback ratio = 0.4

g_abc = b_abc * ROE_abc # sustainable growth = 10%

D1_abc = EPS1_abc * p_abc

print("=" * 65)

print("ABC SOFTWARE — Growth Opportunities (Lo's Example)")

print("=" * 65)

print(f"EPS₁ = ${EPS1_abc:.2f}, payout = {p_abc:.0%}, ROE = {ROE_abc:.0%}, r = {r_abc:.0%}")

print(f"Plowback b = {b_abc:.1f}, g = b × ROE = {b_abc:.1f} × {ROE_abc:.0%} = {g_abc:.0%}")

print(f"D₁ = EPS × p = ${D1_abc:.2f}")

# No-growth value

P0_nogrowth = EPS1_abc / r_abc

print(f"\nNo-growth value: EPS₁/r = ${EPS1_abc:.2f}/{r_abc:.2f} = ${P0_nogrowth:.2f}")

# Growth value

P0_growth = D1_abc / (r_abc - g_abc)

print(f"Growth value: D₁/(r-g) = ${D1_abc:.2f}/({r_abc:.2f}-{g_abc:.2f}) = ${P0_growth:.2f}")

PVGO = P0_growth - P0_nogrowth

print(f"\nPVGO = P₀(growth) - P₀(no-growth) = ${P0_growth:.2f} - ${P0_nogrowth:.2f} = ${PVGO:.2f}")

print(f"PVGO share: {PVGO/P0_growth*100:.1f}% of stock price")

# Verify PVGO via NPV of growth investments

# At t=1: invest b*EPS = 0.4*8.33 = 3.33 at ROE=25% → perpetual CF of 0.25*3.33 = 0.83

inv_1 = b_abc * EPS1_abc

cf_from_inv1 = ROE_abc * inv_1

NPV_1 = -inv_1 + cf_from_inv1 / r_abc # NPV at t=1

# PVGO = NPV_1 / (r - g) as a growing perpetuity

PVGO_check = NPV_1 / (r_abc - g_abc)

print(f"\nVerification via NPV of growth investments:")

print(f" Year 1 investment: ${inv_1:.2f} at ROE={ROE_abc:.0%}")

print(f" Perpetual CF from investment: ${cf_from_inv1:.2f}/year")

print(f" NPV at t=1: -${inv_1:.2f} + ${cf_from_inv1:.2f}/{r_abc:.2f} = ${NPV_1:.2f}")

print(f" PVGO = NPV₁/(r-g) = ${NPV_1:.2f}/({r_abc:.2f}-{g_abc:.2f}) = ${PVGO_check:.2f} ✓")=================================================================

ABC SOFTWARE — Growth Opportunities (Lo's Example)

=================================================================

EPS₁ = $8.33, payout = 60%, ROE = 25%, r = 15%

Plowback b = 0.4, g = b × ROE = 0.4 × 25% = 10%

D₁ = EPS × p = $5.00

No-growth value: EPS₁/r = $8.33/0.15 = $55.53

Growth value: D₁/(r-g) = $5.00/(0.15-0.10) = $99.96

PVGO = P₀(growth) - P₀(no-growth) = $99.96 - $55.53 = $44.43

PVGO share: 44.4% of stock price

Verification via NPV of growth investments:

Year 1 investment: $3.33 at ROE=25%

Perpetual CF from investment: $0.83/year

NPV at t=1: -$3.33 + $0.83/0.15 = $2.22

PVGO = NPV₁/(r-g) = $2.22/(0.15-0.10) = $44.43 ✓

Source

# ============================================================

# PVGO Decomposition — Visualization

# ============================================================

def pvgo_decomposition(EPS1, r, ROE, b):

"""Compute price, no-growth value, and PVGO."""

g = b * ROE

D1 = EPS1 * (1 - b)

if r <= g:

return float('inf'), EPS1/r, float('inf'), g

P0 = D1 / (r - g)

P_nogrowth = EPS1 / r

PVGO = P0 - P_nogrowth

return P0, P_nogrowth, PVGO, g

# Compare firms with different ROE

firms = [

('Value Destroyer', 8.33, 0.15, 0.10, 0.4), # ROE < r

('Zero-Value Growth', 8.33, 0.15, 0.15, 0.4), # ROE = r

('ABC Software', 8.33, 0.15, 0.25, 0.4), # ROE > r

('Super Growth', 8.33, 0.15, 0.35, 0.4), # ROE >> r

]

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(14, 6))

names = []

no_growth_vals = []

pvgo_vals = []

pe_ratios = []

print("=" * 80)

print("PVGO DECOMPOSITION ACROSS FIRMS (all: EPS₁=$8.33, r=15%, b=0.4)")

print("=" * 80)

print(f"{'Firm':>20s} {'ROE':>6s} {'g':>6s} {'P₀':>8s} {'EPS/r':>8s} {'PVGO':>8s} {'P/E':>6s} {'PVGO%':>7s}")

print("-" * 80)

for name, eps, r, roe, b in firms:

P0, P_ng, pvgo, g = pvgo_decomposition(eps, r, roe, b)

pe = P0 / eps

names.append(name.replace(' ', '\n'))

no_growth_vals.append(P_ng)

pvgo_vals.append(pvgo)

pe_ratios.append(pe)

print(f"{name:>20s} {roe:>6.0%} {g:>6.0%} ${P0:>7.2f} ${P_ng:>7.2f} ${pvgo:>+7.2f} {pe:>6.1f} {pvgo/P0*100:>6.1f}%")

# Left: Stacked bar chart

x = np.arange(len(names))

ax1.bar(x, no_growth_vals, color='#3498db', alpha=0.8, label='No-growth (EPS₁/r)', edgecolor='white')

for i, pv in enumerate(pvgo_vals):

color = '#2ecc71' if pv >= 0 else '#e74c3c'

ax1.bar(x[i], pv, bottom=no_growth_vals[i], color=color, alpha=0.8, edgecolor='white')

# Custom legend

from matplotlib.patches import Patch

legend_elements = [Patch(facecolor='#3498db', alpha=0.8, label='No-growth value (EPS₁/r)'),

Patch(facecolor='#2ecc71', alpha=0.8, label='PVGO > 0 (value creating)'),

Patch(facecolor='#e74c3c', alpha=0.8, label='PVGO < 0 (value destroying)')]

ax1.legend(handles=legend_elements, fontsize=9, loc='upper left')

ax1.set_xticks(x)

ax1.set_xticklabels(names, fontsize=9)

ax1.set_ylabel('Stock Price ($)', fontsize=12)

ax1.set_title('Stock Price = No-Growth + PVGO', fontsize=14, fontweight='bold')

ax1.axhline(y=no_growth_vals[0], color='gray', linewidth=1, linestyle=':', alpha=0.5)

ax1.yaxis.set_major_formatter(mticker.FuncFormatter(lambda x, _: f'${x:.0f}'))

# Right: P/E ratio

colors_pe = ['#e74c3c', '#e67e22', '#2ecc71', '#27ae60']

ax2.bar(x, pe_ratios, color=colors_pe, alpha=0.8, edgecolor='white')

ax2.axhline(y=1/0.15, color='#2c3e50', linewidth=2, linestyle='--',

label=f'1/r = {1/0.15:.1f}× (no-growth P/E)')

ax2.set_xticks(x)

ax2.set_xticklabels(names, fontsize=9)

ax2.set_ylabel('P/E Ratio', fontsize=12)

ax2.set_title('P/E Ratio Reflects Growth Opportunities', fontsize=14, fontweight='bold')

ax2.legend(fontsize=10)

for i, pe in enumerate(pe_ratios):

ax2.text(i, pe + 0.3, f'{pe:.1f}×', ha='center', fontsize=10, fontweight='bold')

plt.tight_layout()

plt.show()================================================================================

PVGO DECOMPOSITION ACROSS FIRMS (all: EPS₁=$8.33, r=15%, b=0.4)

================================================================================

Firm ROE g P₀ EPS/r PVGO P/E PVGO%

--------------------------------------------------------------------------------

Value Destroyer 10% 4% $ 45.44 $ 55.53 $ -10.10 5.5 -22.2%

Zero-Value Growth 15% 6% $ 55.53 $ 55.53 $ +0.00 6.7 0.0%

ABC Software 25% 10% $ 99.96 $ 55.53 $ +44.43 12.0 44.4%

Super Growth 35% 14% $ 499.80 $ 55.53 $+444.27 60.0 88.9%

Source

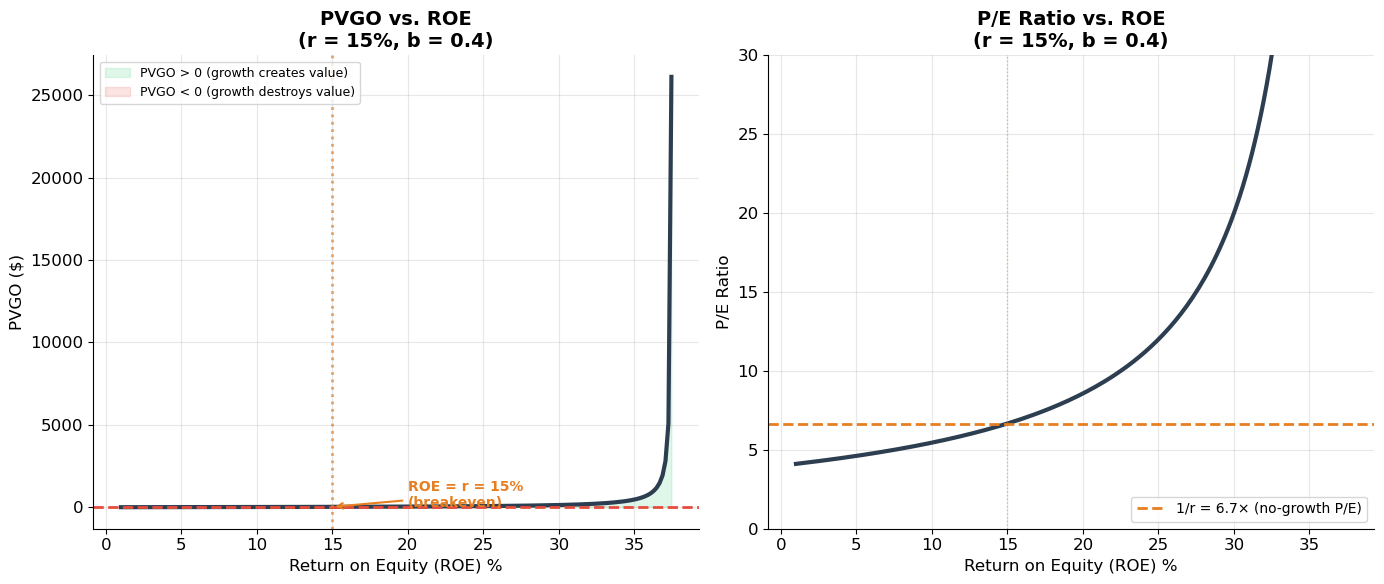

# ============================================================

# When Does Growth Create/Destroy Value? — ROE vs. r

# ============================================================

EPS1 = 8.33

r = 0.15

b = 0.4

ROE_range = np.linspace(0.01, 0.40, 200)

prices = []

pvgos = []

pes = []

for roe in ROE_range:

g = b * roe

if r > g:

D1 = EPS1 * (1 - b)

P0 = D1 / (r - g)

pvgo = P0 - EPS1/r

prices.append(P0)

pvgos.append(pvgo)

pes.append(P0/EPS1)

else:

prices.append(np.nan)

pvgos.append(np.nan)

pes.append(np.nan)

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(14, 6))

# Left: PVGO vs ROE

ax1.plot(ROE_range * 100, pvgos, color='#2c3e50', linewidth=3)

ax1.axhline(y=0, color='#e74c3c', linewidth=2, linestyle='--')

ax1.axvline(x=r * 100, color='#e67e22', linewidth=2, linestyle=':', alpha=0.7)

ax1.fill_between(ROE_range * 100, 0, pvgos, where=np.array(pvgos) > 0,

alpha=0.15, color='#2ecc71', label='PVGO > 0 (growth creates value)')

ax1.fill_between(ROE_range * 100, 0, pvgos, where=np.array(pvgos) < 0,

alpha=0.15, color='#e74c3c', label='PVGO < 0 (growth destroys value)')

ax1.annotate(f'ROE = r = {r:.0%}\n(breakeven)', xy=(r*100, 0), xytext=(r*100 + 5, -15),

fontsize=10, color='#e67e22', fontweight='bold',

arrowprops=dict(arrowstyle='->', color='#e67e22', lw=1.5))

ax1.set_xlabel('Return on Equity (ROE) %', fontsize=12)

ax1.set_ylabel('PVGO ($)', fontsize=12)

ax1.set_title('PVGO vs. ROE\n(r = 15%, b = 0.4)', fontsize=14, fontweight='bold')

ax1.legend(fontsize=9)

# Right: P/E vs ROE

ax2.plot(ROE_range * 100, pes, color='#2c3e50', linewidth=3)

ax2.axhline(y=1/r, color='#e67e22', linewidth=2, linestyle='--', label=f'1/r = {1/r:.1f}× (no-growth P/E)')

ax2.axvline(x=r * 100, color='#e67e22', linewidth=1, linestyle=':', alpha=0.5)

ax2.set_xlabel('Return on Equity (ROE) %', fontsize=12)

ax2.set_ylabel('P/E Ratio', fontsize=12)

ax2.set_title('P/E Ratio vs. ROE\n(r = 15%, b = 0.4)', fontsize=14, fontweight='bold')

ax2.legend(fontsize=10)

ax2.set_ylim(0, 30)

plt.tight_layout()

plt.show()

print("Critical insight:")

print("• ROE > r: Growth creates value → PVGO > 0 → P/E > 1/r (growth stock)")

print("• ROE = r: Growth is value-neutral → PVGO = 0 → P/E = 1/r")

print("• ROE < r: Growth DESTROYS value → PVGO < 0 → P/E < 1/r")

print("\nA 'growth stock' is defined by ROE > r, NOT by growing EPS!")

Critical insight:

• ROE > r: Growth creates value → PVGO > 0 → P/E > 1/r (growth stock)

• ROE = r: Growth is value-neutral → PVGO = 0 → P/E = 1/r

• ROE < r: Growth DESTROYS value → PVGO < 0 → P/E < 1/r

A 'growth stock' is defined by ROE > r, NOT by growing EPS!

8. Exercises¶

Exercise 1: Gordon Growth Model¶

A utility company just paid a dividend of $3.50 per share. Dividends are expected to grow at 3% per year indefinitely.

(a) If the required return is 9%, what is the stock price?

(b) If the stock is currently trading at $65, what cost of equity is the market implying?

(c) If management announces it will increase the growth rate to 5% by reducing the payout ratio, but the required return also increases to 11% due to higher risk, what happens to the stock price? Is the growth strategy value-creating?

(d) The CEO claims “our stock is undervalued because the market doesn’t understand our growth.” If the current price is $55 and r = 9%, what growth rate is the market implying? Is the CEO’s claim plausible if ROE = 12%?

Source

# Exercise 1 — Workspace

# D0 = 3.50; g = 0.03; r = 0.09

#

# (a) P0 = D0*(1+g)/(r-g) = 3.50*1.03/(0.09-0.03)

# P0 = ?

#

# (b) Trading at $65: r = D1/P0 + g = 3.50*1.03/65 + 0.03

# r = ?

#

# (c) New g=0.05, new r=0.11

# P0_new = 3.50*(1.05)/(0.11-0.05)

# Compare with original

#

# (d) 55 = 3.50*(1+g)/(0.09-g) → solve for g

# from scipy.optimize import brentq

# g_implied = brentq(lambda g: 3.50*(1+g)/(0.09-g) - 55, 0, 0.089)

# print(f"Implied g = {g_implied:.2%}")Exercise 2: Two-Stage Growth Model¶

TechCorp has just paid a dividend of $1.20. Analysts expect 20% dividend growth for the next 5 years, followed by 4% growth forever. The cost of equity is 14%.

(a) Compute the stock price using the two-stage DDM.

(b) What fraction of the stock’s value comes from the terminal value? Why is this fraction typically so large?

(c) If the market prices the stock at $35, what stable growth rate is being implied (keeping all else equal)? Use numerical methods.

(d) Run a sensitivity analysis: how does the stock price change as varies from 2% to 6% and as varies from 12% to 16%? Present your results as a table.

Source

# Exercise 2 — Workspace

# D0, r, g_H, T, g_L = 1.20, 0.14, 0.20, 5, 0.04

#

# (a)

# pv1, pv2, P0 = two_stage_ddm(D0, r, g_H, T, g_L)

# print(f"P₀ = ${P0:.2f}")

#

# (b)

# print(f"Terminal value share: {pv2/(pv1+pv2)*100:.1f}%")

#

# (c) Find g_L such that P0 = 35

# g_implied = brentq(lambda g: two_stage_ddm(D0, r, g_H, T, g)[2] - 35, 0, 0.139)

# print(f"Implied g_L = {g_implied:.2%}")Exercise 3: PVGO and Growth Stocks¶

MegaCorp has: EPS₁ = $5.00, payout ratio = 50%, ROE = 18%, cost of equity = 12%.

(a) Compute the sustainable growth rate, dividend, stock price, and P/E ratio.

(b) Decompose the stock price into no-growth value and PVGO. What fraction of value comes from growth opportunities?

(c) A competitor, SteadyCorp, has the same EPS and cost of equity but ROE = 12% (equal to ). It also retains 50%. Compute SteadyCorp’s price, PVGO, and P/E. What happens if SteadyCorp increases retention to 80%?

(d) A value investor argues: “I only buy stocks with P/E < 10. High P/E stocks are overpriced.” Using the PVGO framework, explain why this rule might cause the investor to miss excellent opportunities. When might the rule be correct?

Source

# Exercise 3 — Workspace

# EPS1, p, ROE, r = 5.00, 0.50, 0.18, 0.12

# b = 1 - p

# g = b * ROE

# D1 = EPS1 * p

# P0 = D1 / (r - g)

# P_nogrowth = EPS1 / r

# PVGO = P0 - P_nogrowth

# PE = P0 / EPS1

#

# print(f"g = {g:.2%}, D₁ = ${D1:.2f}")

# print(f"P₀ = ${P0:.2f}, P/E = {PE:.1f}×")

# print(f"No-growth: ${P_nogrowth:.2f}, PVGO: ${PVGO:.2f} ({PVGO/P0*100:.1f}%)")Key Takeaways — Session 6¶

The DDM values a stock as the present value of all future dividends: . The holding period doesn’t matter — the price reflects the infinite dividend stream.

The Gordon Growth Model is the workhorse of equity valuation. It requires and is extremely sensitive to the spread .

Cost of equity can be estimated from the DDM: (dividend yield + growth). Returns decompose into income (dividends) and capital gains (growth).

Multi-stage models handle firms transitioning from high to stable growth. The terminal value (stable phase) typically dominates, accounting for 60–80% of total value.

Sustainable growth . The link between dividends and earnings is through the payout ratio.

Stock price = No-growth value + PVGO. Growth creates value only when ROE > . A true “growth stock” is defined by having PVGO > 0, not by having fast-growing EPS.

P/E ratio = + PVGO/EPS. High P/E signals growth opportunities. P/E equals only when the firm earns exactly its cost of capital on new investments.

References¶

Brealey, R.A., Myers, S.C., and Allen, F. Principles of Corporate Finance, Chapter 4.

MIT OCW 15.401: Equities

Gordon, M.J. (1959). “Dividends, Earnings, and Stock Prices.” Review of Economics and Statistics, 41(2), 99–105.

Harris, L. (2002). Trading and Exchanges: Market Microstructure for Practitioners. Oxford University Press.

Malkiel, B. (1996). A Random Walk Down Wall Street. W.W. Norton.

Next: Session 7 — Forward and Futures Contracts — forward pricing, cost of carry, futures markets, and hedging applications.