Session 1: Introduction to Time Series Analysis

Summer School: Time Series Methods for Finance and Economics¶

Learning Objectives¶

By the end of this session, you will be able to:

Define time series and understand basic notation

Distinguish between stationary and non-stationary processes

Identify and test for stationarity

Understand white noise and random walk processes

Compute and interpret autocorrelation and partial autocorrelation functions

Perform exploratory data analysis on financial time series

Source

# Import required libraries

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

from scipy import stats

from statsmodels.tsa.stattools import adfuller, kpss, acf, pacf

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

import yfinance as yf

import warnings

warnings.filterwarnings('ignore')

# Set style

plt.style.use('seaborn-v0_8-darkgrid')

sns.set_palette("husl")

%matplotlib inline

# Set random seed for reproducibility

np.random.seed(42)1. Time Series Basics and Notation¶

1.1 Definition¶

A time series is a sequence of observations indexed by time:

where:

is the observation at time

is the total number of observations

can represent different time intervals (seconds, days, months, years, etc.)

1.2 Key Characteristics¶

Time series data differs from cross-sectional data in several important ways:

Temporal ordering matters: The sequence is meaningful

Dependence: Observations are typically correlated over time

Trends: Long-run movements in the data

Seasonality: Regular patterns that repeat over fixed periods

Cycles: Irregular fluctuations around the trend

1.3 Common Notation¶

: Mean at time

: Variance at time

: Autocovariance at lag

: Autocorrelation at lag

: Error term or innovation at time

Source

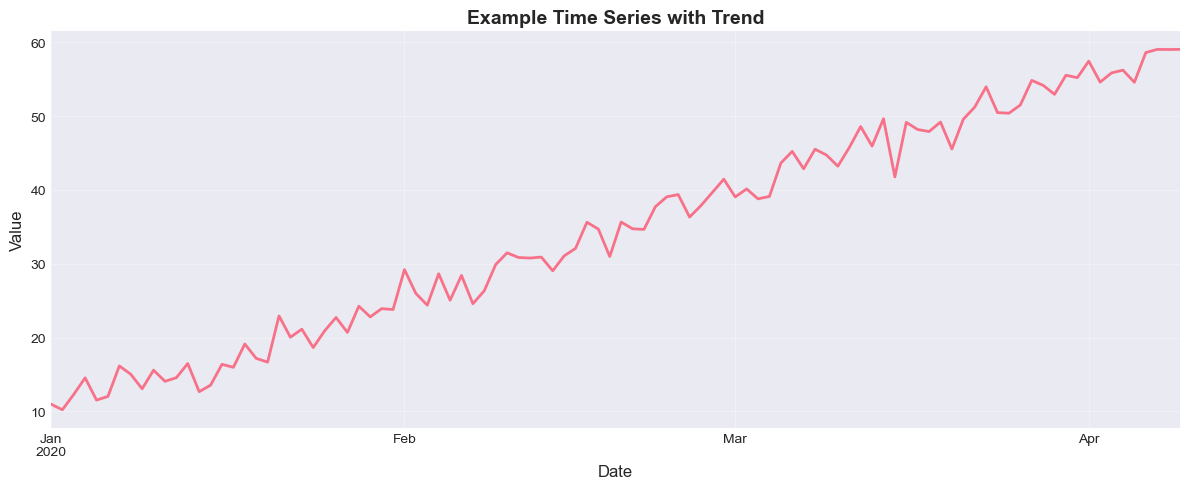

# Example: Generate a simple time series

T = 100

time = np.arange(T)

y = 10 + 0.5 * time + np.random.normal(0, 2, T)

# Create a pandas Series with date index

dates = pd.date_range(start='2020-01-01', periods=T, freq='D')

ts = pd.Series(y, index=dates, name='Value')

# Plot

fig, ax = plt.subplots(figsize=(12, 5))

ts.plot(ax=ax, linewidth=2)

ax.set_title('Example Time Series with Trend', fontsize=14, fontweight='bold')

ax.set_xlabel('Date', fontsize=12)

ax.set_ylabel('Value', fontsize=12)

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print(f"Sample size: {len(ts)}")

print(f"Mean: {ts.mean():.2f}")

print(f"Standard deviation: {ts.std():.2f}")

Sample size: 100

Mean: 34.54

Standard deviation: 14.70

2. Stationarity¶

2.1 Strong (Strict) Stationarity¶

A time series is strictly stationary if the joint distribution of is the same as that of for all and all lags .

Implication: The statistical properties are invariant to shifts in time.

2.2 Weak (Covariance) Stationarity¶

A time series is weakly stationary (or covariance stationary) if:

Constant mean: for all

Constant variance: for all

Autocovariance depends only on lag: for all and lag

2.3 Why Stationarity Matters¶

Most time series models (ARIMA, GARCH, VAR) assume stationarity

Non-stationary series can lead to spurious regression

Forecasting with non-stationary data is problematic

Many statistical properties (ergodicity, law of large numbers) require stationarity

2.4 Common Violations of Stationarity¶

Trend-stationary:

Difference-stationary: (random walk)

Structural breaks: Parameters change at specific points in time

Heteroskedasticity: Variance changes over time

Source

# Generate different types of processes

T = 500

t = np.arange(T)

# 1. Stationary process (AR(1) with |φ| < 1)

phi = 0.7

stationary = np.zeros(T)

epsilon = np.random.normal(0, 1, T)

for i in range(1, T):

stationary[i] = phi * stationary[i-1] + epsilon[i]

# 2. Trend-stationary process

trend_stationary = 10 + 0.05 * t + np.random.normal(0, 1, T)

# 3. Difference-stationary (random walk)

random_walk = np.cumsum(np.random.normal(0, 1, T))

# 4. Random walk with drift

random_walk_drift = np.cumsum(np.random.normal(0.1, 1, T))

# Plot all processes

fig, axes = plt.subplots(2, 2, figsize=(15, 10))

axes[0, 0].plot(stationary, linewidth=1.5)

axes[0, 0].set_title('Stationary Process (AR(1))', fontsize=12, fontweight='bold')

axes[0, 0].axhline(y=0, color='r', linestyle='--', alpha=0.5)

axes[0, 0].grid(True, alpha=0.3)

axes[0, 1].plot(trend_stationary, linewidth=1.5)

axes[0, 1].set_title('Trend-Stationary Process', fontsize=12, fontweight='bold')

axes[0, 1].grid(True, alpha=0.3)

axes[1, 0].plot(random_walk, linewidth=1.5)

axes[1, 0].set_title('Random Walk (Difference-Stationary)', fontsize=12, fontweight='bold')

axes[1, 0].axhline(y=0, color='r', linestyle='--', alpha=0.5)

axes[1, 0].grid(True, alpha=0.3)

axes[1, 1].plot(random_walk_drift, linewidth=1.5)

axes[1, 1].set_title('Random Walk with Drift', fontsize=12, fontweight='bold')

axes[1, 1].grid(True, alpha=0.3)

for ax in axes.flat:

ax.set_xlabel('Time', fontsize=10)

ax.set_ylabel('Value', fontsize=10)

plt.tight_layout()

plt.show()

3. Testing for Stationarity¶

3.1 Augmented Dickey-Fuller (ADF) Test¶

The ADF test checks for the presence of a unit root:

Hypotheses:

: (unit root exists, series is non-stationary)

: (no unit root, series is stationary)

Decision rule: If p-value < 0.05, reject and conclude the series is stationary.

3.2 KPSS Test¶

The KPSS (Kwiatkowski-Phillips-Schmidt-Shin) test has opposite hypotheses:

Hypotheses:

: Series is stationary

: Series has a unit root

Decision rule: If p-value < 0.05, reject and conclude the series is non-stationary.

3.3 Combining Tests¶

Best practice: Use both tests for robustness

| ADF Result | KPSS Result | Conclusion |

|---|---|---|

| Stationary | Stationary | Stationary |

| Non-stationary | Non-stationary | Non-stationary |

| Stationary | Non-stationary | Trend-stationary |

| Non-stationary | Stationary | Difference-stationary |

Source

def test_stationarity(timeseries, name='Series', verbose=True):

"""

Perform ADF and KPSS tests for stationarity.

Parameters:

-----------

timeseries : array-like

The time series to test

name : str

Name of the series for display

verbose : bool

Whether to print detailed results

Returns:

--------

dict : Dictionary containing test results

"""

# ADF Test

adf_result = adfuller(timeseries, autolag='AIC')

adf_statistic = adf_result[0]

adf_pvalue = adf_result[1]

adf_lags = adf_result[2]

adf_critical_values = adf_result[4]

# KPSS Test

kpss_result = kpss(timeseries, regression='ct', nlags='auto')

kpss_statistic = kpss_result[0]

kpss_pvalue = kpss_result[1]

kpss_lags = kpss_result[2]

kpss_critical_values = kpss_result[3]

if verbose:

print(f"\n{'='*60}")

print(f"Stationarity Tests for: {name}")

print(f"{'='*60}")

print("\n1. Augmented Dickey-Fuller Test")

print("-" * 40)

print(f"Test Statistic: {adf_statistic:.4f}")

print(f"P-value: {adf_pvalue:.4f}")

print(f"Lags used: {adf_lags}")

print("Critical Values:")

for key, value in adf_critical_values.items():

print(f" {key}: {value:.4f}")

if adf_pvalue < 0.05:

print("\n✓ ADF: Reject H0 → Series is STATIONARY (at 5% level)")

else:

print("\n✗ ADF: Fail to reject H0 → Series is NON-STATIONARY")

print("\n2. KPSS Test")

print("-" * 40)

print(f"Test Statistic: {kpss_statistic:.4f}")

print(f"P-value: {kpss_pvalue:.4f}")

print(f"Lags used: {kpss_lags}")

print("Critical Values:")

for key, value in kpss_critical_values.items():

print(f" {key}: {value:.4f}")

if kpss_pvalue < 0.05:

print("\n✗ KPSS: Reject H0 → Series is NON-STATIONARY (at 5% level)")

else:

print("\n✓ KPSS: Fail to reject H0 → Series is STATIONARY")

print("\n" + "="*60)

return {

'adf_statistic': adf_statistic,

'adf_pvalue': adf_pvalue,

'adf_is_stationary': adf_pvalue < 0.05,

'kpss_statistic': kpss_statistic,

'kpss_pvalue': kpss_pvalue,

'kpss_is_stationary': kpss_pvalue >= 0.05

}

# Test our generated series

test_stationarity(stationary, name='Stationary AR(1)')

test_stationarity(random_walk, name='Random Walk')

============================================================

Stationarity Tests for: Stationary AR(1)

============================================================

1. Augmented Dickey-Fuller Test

----------------------------------------

Test Statistic: -9.7416

P-value: 0.0000

Lags used: 0

Critical Values:

1%: -3.4435

5%: -2.8673

10%: -2.5699

✓ ADF: Reject H0 → Series is STATIONARY (at 5% level)

2. KPSS Test

----------------------------------------

Test Statistic: 0.0571

P-value: 0.1000

Lags used: 10

Critical Values:

10%: 0.1190

5%: 0.1460

2.5%: 0.1760

1%: 0.2160

✓ KPSS: Fail to reject H0 → Series is STATIONARY

============================================================

============================================================

Stationarity Tests for: Random Walk

============================================================

1. Augmented Dickey-Fuller Test

----------------------------------------

Test Statistic: -1.5175

P-value: 0.5248

Lags used: 0

Critical Values:

1%: -3.4435

5%: -2.8673

10%: -2.5699

✗ ADF: Fail to reject H0 → Series is NON-STATIONARY

2. KPSS Test

----------------------------------------

Test Statistic: 0.5071

P-value: 0.0100

Lags used: 12

Critical Values:

10%: 0.1190

5%: 0.1460

2.5%: 0.1760

1%: 0.2160

✗ KPSS: Reject H0 → Series is NON-STATIONARY (at 5% level)

============================================================

{'adf_statistic': -1.5175165267153008,

'adf_pvalue': 0.5248290551329203,

'adf_is_stationary': False,

'kpss_statistic': 0.5070872812632301,

'kpss_pvalue': 0.01,

'kpss_is_stationary': False}4. White Noise and Random Walks¶

4.1 White Noise¶

A white noise process satisfies:

for all

for all

for all

Properties:

Stationary

Unpredictable (best forecast is zero)

Building block for more complex models

Strong white noise additionally assumes

4.2 Random Walk¶

A random walk is defined as:

where is white noise.

Solution:

Properties:

Non-stationary

(constant)

(increases with time)

First difference is stationary:

Random walk with drift:

where is the drift parameter.

Source

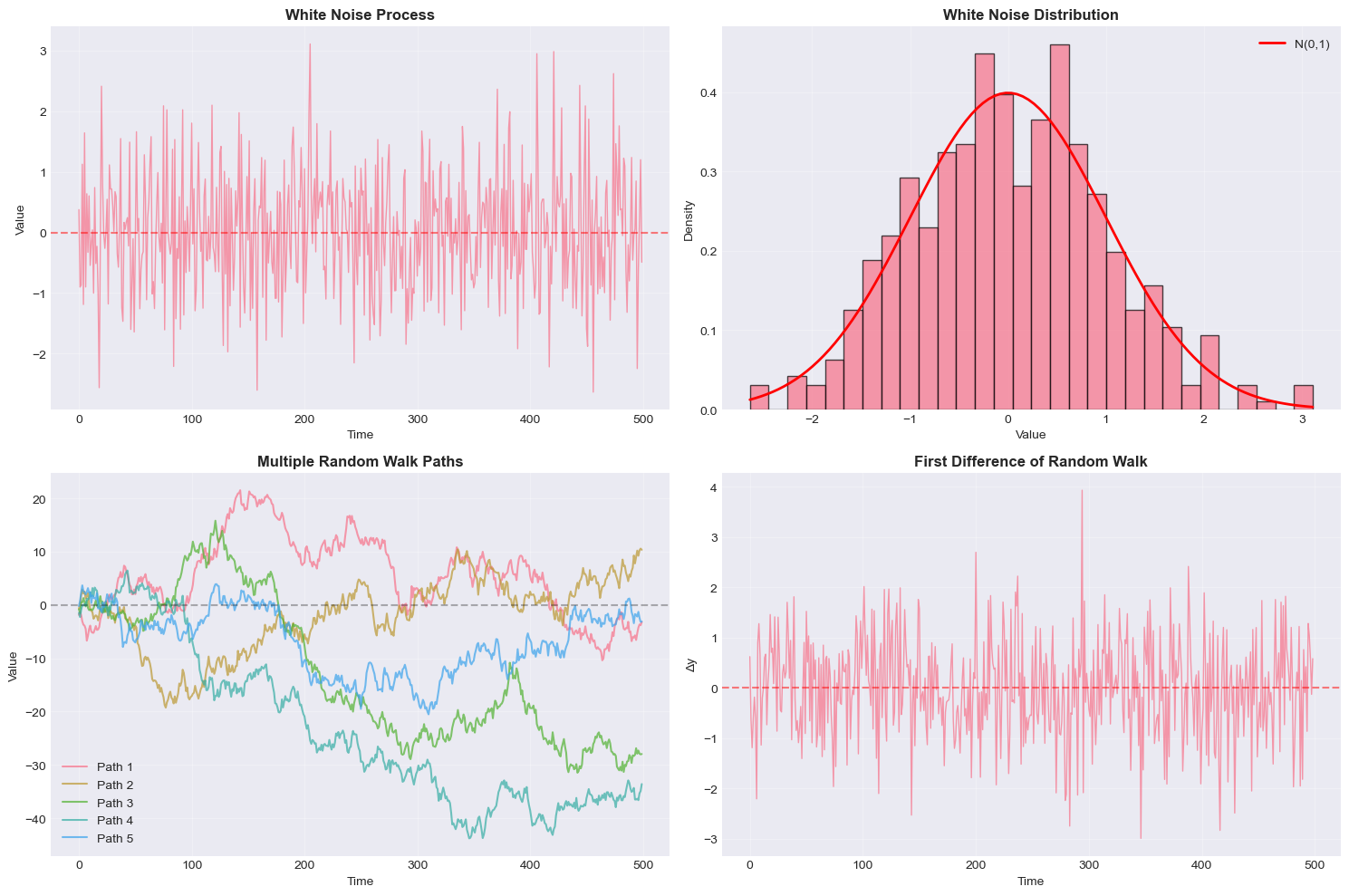

# Generate and analyze white noise

T = 500

white_noise = np.random.normal(0, 1, T)

# Generate multiple random walk paths

n_paths = 5

random_walks = np.zeros((T, n_paths))

for i in range(n_paths):

random_walks[:, i] = np.cumsum(np.random.normal(0, 1, T))

# Plotting

fig, axes = plt.subplots(2, 2, figsize=(15, 10))

# White noise time series

axes[0, 0].plot(white_noise, linewidth=1, alpha=0.7)

axes[0, 0].axhline(y=0, color='r', linestyle='--', alpha=0.5)

axes[0, 0].set_title('White Noise Process', fontsize=12, fontweight='bold')

axes[0, 0].set_xlabel('Time')

axes[0, 0].set_ylabel('Value')

axes[0, 0].grid(True, alpha=0.3)

# White noise histogram

axes[0, 1].hist(white_noise, bins=30, density=True, alpha=0.7, edgecolor='black')

x = np.linspace(white_noise.min(), white_noise.max(), 100)

axes[0, 1].plot(x, stats.norm.pdf(x, 0, 1), 'r-', linewidth=2, label='N(0,1)')

axes[0, 1].set_title('White Noise Distribution', fontsize=12, fontweight='bold')

axes[0, 1].set_xlabel('Value')

axes[0, 1].set_ylabel('Density')

axes[0, 1].legend()

axes[0, 1].grid(True, alpha=0.3)

# Multiple random walk paths

for i in range(n_paths):

axes[1, 0].plot(random_walks[:, i], linewidth=1.5, alpha=0.7, label=f'Path {i+1}')

axes[1, 0].axhline(y=0, color='k', linestyle='--', alpha=0.3)

axes[1, 0].set_title('Multiple Random Walk Paths', fontsize=12, fontweight='bold')

axes[1, 0].set_xlabel('Time')

axes[1, 0].set_ylabel('Value')

axes[1, 0].legend()

axes[1, 0].grid(True, alpha=0.3)

# Random walk first difference (should be white noise)

rw_diff = np.diff(random_walks[:, 0])

axes[1, 1].plot(rw_diff, linewidth=1, alpha=0.7)

axes[1, 1].axhline(y=0, color='r', linestyle='--', alpha=0.5)

axes[1, 1].set_title('First Difference of Random Walk', fontsize=12, fontweight='bold')

axes[1, 1].set_xlabel('Time')

axes[1, 1].set_ylabel('Δy')

axes[1, 1].grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

# Statistical tests

print("\nWhite Noise Statistics:")

print(f"Mean: {white_noise.mean():.4f} (expected: 0)")

print(f"Std Dev: {white_noise.std():.4f} (expected: 1)")

print(f"Skewness: {stats.skew(white_noise):.4f} (expected: 0)")

print(f"Kurtosis: {stats.kurtosis(white_noise):.4f} (expected: 0)")

# Ljung-Box test for white noise

from statsmodels.stats.diagnostic import acorr_ljungbox

lb_result = acorr_ljungbox(white_noise, lags=[10], return_df=True)

print(f"\nLjung-Box Q(10): {lb_result['lb_stat'].values[0]:.4f}")

print(f"P-value: {lb_result['lb_pvalue'].values[0]:.4f}")

if lb_result['lb_pvalue'].values[0] > 0.05:

print("✓ Cannot reject null: Data consistent with white noise")

else:

print("✗ Reject null: Data shows significant autocorrelation")

White Noise Statistics:

Mean: 0.0193 (expected: 0)

Std Dev: 0.9833 (expected: 1)

Skewness: 0.1279 (expected: 0)

Kurtosis: -0.0447 (expected: 0)

Ljung-Box Q(10): 18.7663

P-value: 0.0433

✗ Reject null: Data shows significant autocorrelation

5. Autocorrelation and Partial Autocorrelation¶

5.1 Autocorrelation Function (ACF)¶

The autocorrelation at lag measures the correlation between and :

Sample ACF:

Properties:

(correlation with itself)

For white noise: for all

Standard error (for white noise):

5.2 Partial Autocorrelation Function (PACF)¶

The partial autocorrelation at lag measures the correlation between and after removing the linear influence of .

It answers: “What is the direct correlation between and ?”

Mathematical definition: is the last coefficient in:

5.3 Interpreting ACF and PACF¶

| Process | ACF Pattern | PACF Pattern |

|---|---|---|

| White Noise | All zero | All zero |

| AR(p) | Decays exponentially | Cuts off after lag p |

| MA(q) | Cuts off after lag q | Decays exponentially |

| ARMA(p,q) | Decays exponentially | Decays exponentially |

| Random Walk | Decays slowly | First lag ≈ 1 |

Source

def plot_acf_pacf(timeseries, lags=40, title=''):

"""

Plot ACF and PACF for a time series.

Parameters:

-----------

timeseries : array-like

The time series to analyze

lags : int

Number of lags to display

title : str

Title prefix for the plots

"""

fig, axes = plt.subplots(1, 2, figsize=(15, 4))

# Plot ACF

plot_acf(timeseries, lags=lags, ax=axes[0], alpha=0.05)

axes[0].set_title(f'{title} - Autocorrelation Function (ACF)', fontsize=12, fontweight='bold')

axes[0].set_xlabel('Lag', fontsize=10)

axes[0].set_ylabel('ACF', fontsize=10)

axes[0].grid(True, alpha=0.3)

# Plot PACF

plot_pacf(timeseries, lags=lags, ax=axes[1], alpha=0.05, method='ywm')

axes[1].set_title(f'{title} - Partial Autocorrelation Function (PACF)', fontsize=12, fontweight='bold')

axes[1].set_xlabel('Lag', fontsize=10)

axes[1].set_ylabel('PACF', fontsize=10)

axes[1].grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

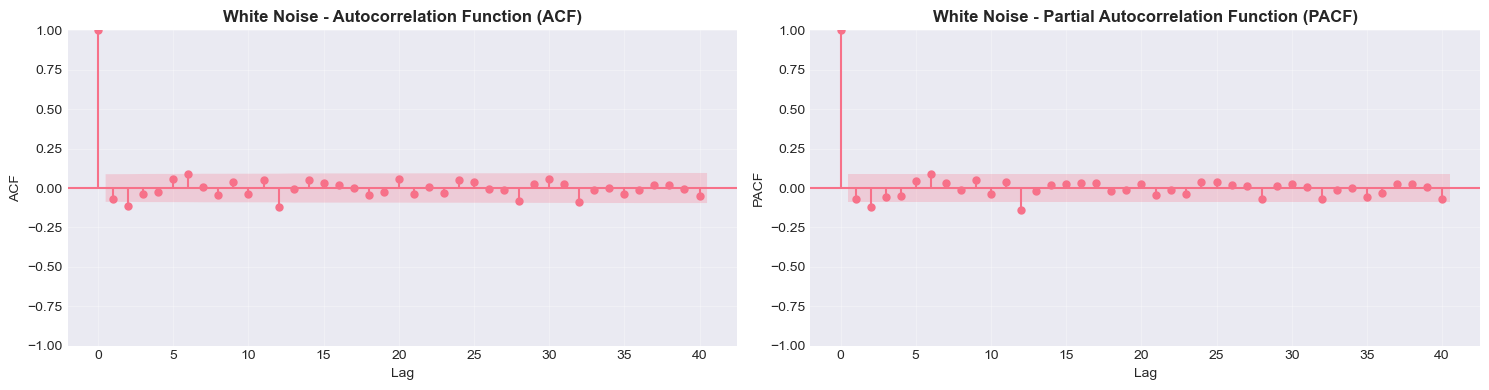

# Analyze white noise

print("White Noise Process")

plot_acf_pacf(white_noise, lags=40, title='White Noise')

# Analyze random walk

print("\nRandom Walk Process")

plot_acf_pacf(random_walks[:, 0], lags=40, title='Random Walk')

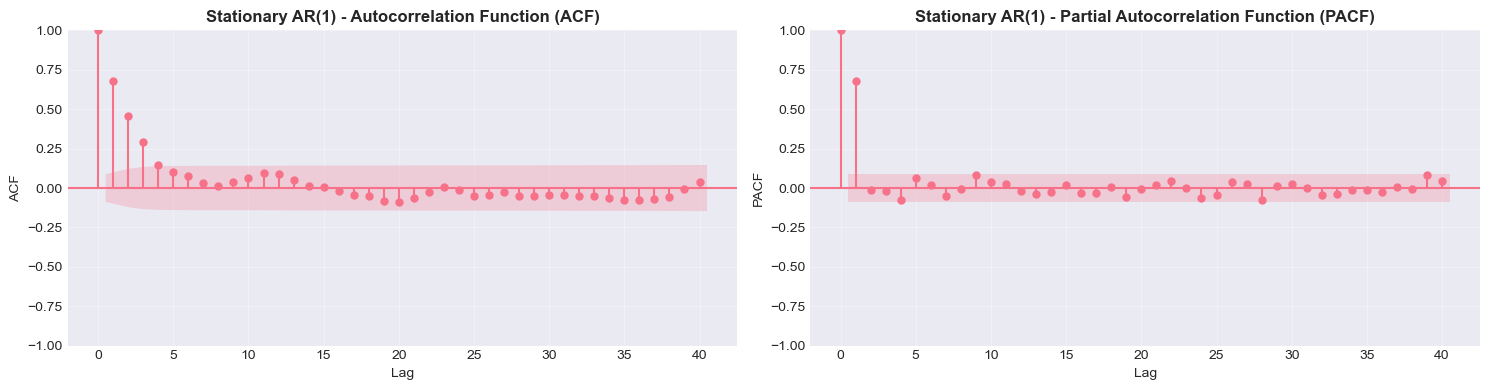

# Analyze stationary AR(1)

print("\nStationary AR(1) Process")

plot_acf_pacf(stationary, lags=40, title='Stationary AR(1)')White Noise Process

Random Walk Process

Stationary AR(1) Process

Source

# Generate and compare different processes

T = 500

# AR(1) process: y_t = 0.8*y_{t-1} + ε_t

ar1 = np.zeros(T)

eps = np.random.normal(0, 1, T)

for i in range(1, T):

ar1[i] = 0.8 * ar1[i-1] + eps[i]

# MA(1) process: y_t = ε_t + 0.8*ε_{t-1}

ma1 = np.zeros(T)

eps = np.random.normal(0, 1, T)

for i in range(1, T):

ma1[i] = eps[i] + 0.8 * eps[i-1]

# Plot time series

fig, axes = plt.subplots(2, 2, figsize=(15, 8))

# AR(1) time series

axes[0, 0].plot(ar1, linewidth=1)

axes[0, 0].set_title('AR(1) Process: $y_t = 0.8y_{t-1} + \epsilon_t$', fontsize=11, fontweight='bold')

axes[0, 0].axhline(y=0, color='r', linestyle='--', alpha=0.5)

axes[0, 0].grid(True, alpha=0.3)

# MA(1) time series

axes[0, 1].plot(ma1, linewidth=1)

axes[0, 1].set_title('MA(1) Process: $y_t = \epsilon_t + 0.8\epsilon_{t-1}$', fontsize=11, fontweight='bold')

axes[0, 1].axhline(y=0, color='r', linestyle='--', alpha=0.5)

axes[0, 1].grid(True, alpha=0.3)

# AR(1) ACF and PACF combined

acf_ar = acf(ar1, nlags=20)

pacf_ar = pacf(ar1, nlags=20, method='ywm')

x = np.arange(len(acf_ar))

axes[1, 0].bar(x - 0.2, acf_ar, width=0.4, label='ACF', alpha=0.7)

axes[1, 0].bar(x + 0.2, pacf_ar, width=0.4, label='PACF', alpha=0.7)

axes[1, 0].axhline(y=0, color='black', linewidth=0.8)

axes[1, 0].axhline(y=1.96/np.sqrt(T), color='blue', linestyle='--', linewidth=1, alpha=0.5)

axes[1, 0].axhline(y=-1.96/np.sqrt(T), color='blue', linestyle='--', linewidth=1, alpha=0.5)

axes[1, 0].set_title('AR(1): ACF decays, PACF cuts off at lag 1', fontsize=11, fontweight='bold')

axes[1, 0].set_xlabel('Lag')

axes[1, 0].legend()

axes[1, 0].grid(True, alpha=0.3)

# MA(1) ACF and PACF combined

acf_ma = acf(ma1, nlags=20)

pacf_ma = pacf(ma1, nlags=20, method='ywm')

axes[1, 1].bar(x - 0.2, acf_ma, width=0.4, label='ACF', alpha=0.7)

axes[1, 1].bar(x + 0.2, pacf_ma, width=0.4, label='PACF', alpha=0.7)

axes[1, 1].axhline(y=0, color='black', linewidth=0.8)

axes[1, 1].axhline(y=1.96/np.sqrt(T), color='blue', linestyle='--', linewidth=1, alpha=0.5)

axes[1, 1].axhline(y=-1.96/np.sqrt(T), color='blue', linestyle='--', linewidth=1, alpha=0.5)

axes[1, 1].set_title('MA(1): ACF cuts off at lag 1, PACF decays', fontsize=11, fontweight='bold')

axes[1, 1].set_xlabel('Lag')

axes[1, 1].legend()

axes[1, 1].grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print("\nKey Observations:")

print("• AR(1): ACF decays exponentially, PACF has significant spike only at lag 1")

print("• MA(1): ACF has significant spike only at lag 1, PACF decays exponentially")

print("• Blue dashed lines show 95% confidence bands (±1.96/√T)")

Key Observations:

• AR(1): ACF decays exponentially, PACF has significant spike only at lag 1

• MA(1): ACF has significant spike only at lag 1, PACF decays exponentially

• Blue dashed lines show 95% confidence bands (±1.96/√T)

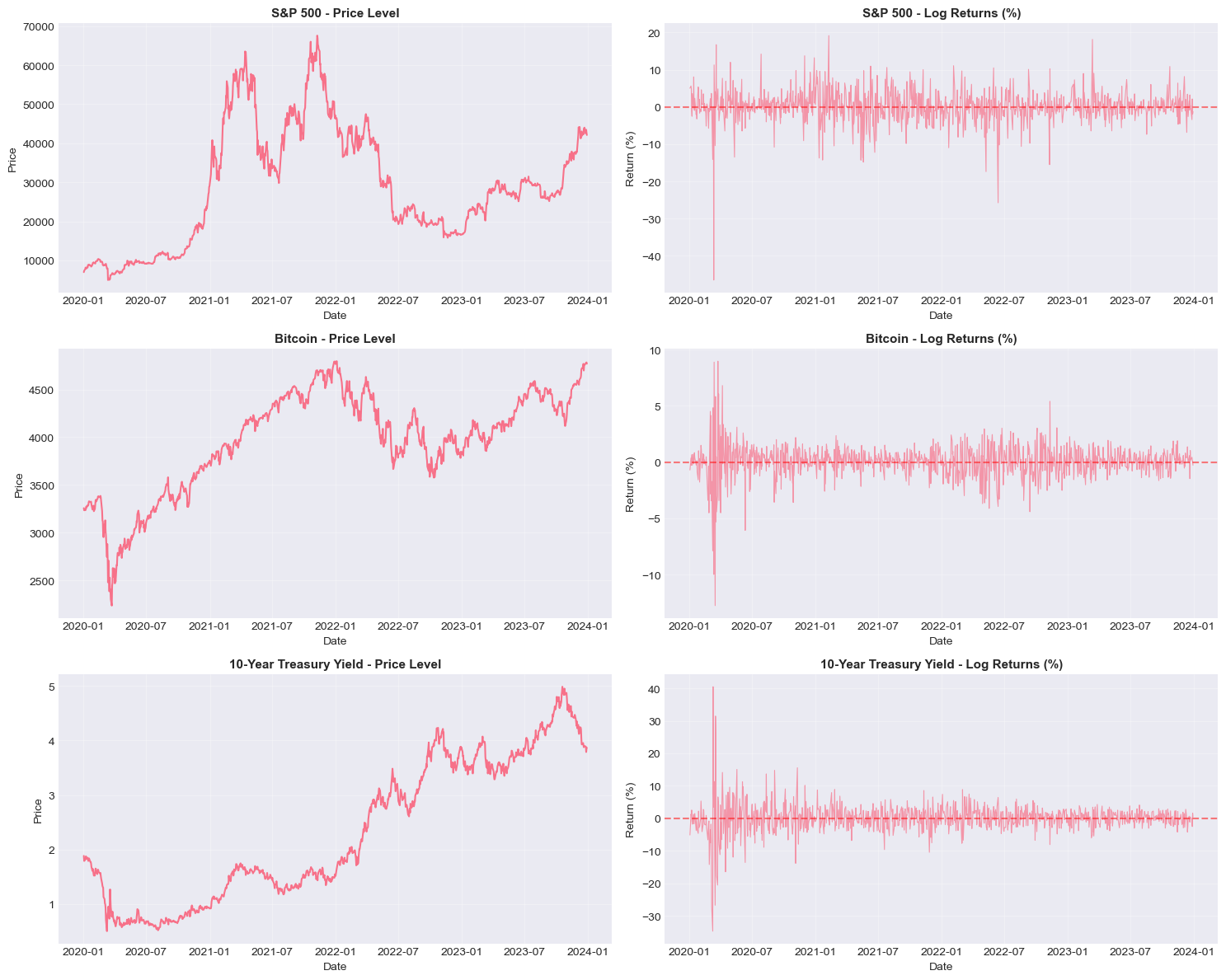

6. Practical Application: Real Financial Data¶

Let’s apply these concepts to real financial time series data.

Source

# Download financial data

print("Downloading financial data...")

# Download S&P 500 and Bitcoin data

tickers = ['^GSPC', 'BTC-USD', '^TNX'] # S&P 500, Bitcoin, 10-Year Treasury

data = yf.download(tickers, start='2020-01-01', end='2024-01-01', progress=False)

# Extract adjusted close prices

prices = data['Close']

prices.columns = ['SP500', 'BTC', 'TNX']

prices = prices.dropna()

# Calculate returns

returns = np.log(prices / prices.shift(1)).dropna() * 100 # Log returns in percentage

print(f"\nData period: {prices.index[0].date()} to {prices.index[-1].date()}")

print(f"Number of observations: {len(prices)}")

print(f"\nAssets: {', '.join(prices.columns)}")Downloading financial data...

Data period: 2020-01-02 to 2023-12-29

Number of observations: 1006

Assets: SP500, BTC, TNX

Source

# Visualize price levels and returns

fig, axes = plt.subplots(3, 2, figsize=(15, 12))

assets = ['SP500', 'BTC', 'TNX']

titles = ['S&P 500', 'Bitcoin', '10-Year Treasury Yield']

for i, (asset, title) in enumerate(zip(assets, titles)):

# Price levels

axes[i, 0].plot(prices.index, prices[asset], linewidth=1.5)

axes[i, 0].set_title(f'{title} - Price Level', fontsize=11, fontweight='bold')

axes[i, 0].set_xlabel('Date')

axes[i, 0].set_ylabel('Price')

axes[i, 0].grid(True, alpha=0.3)

# Returns

axes[i, 1].plot(returns.index, returns[asset], linewidth=0.8, alpha=0.7)

axes[i, 1].axhline(y=0, color='r', linestyle='--', alpha=0.5)

axes[i, 1].set_title(f'{title} - Log Returns (%)', fontsize=11, fontweight='bold')

axes[i, 1].set_xlabel('Date')

axes[i, 1].set_ylabel('Return (%)')

axes[i, 1].grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

Source

# Descriptive statistics

print("\n" + "="*80)

print("DESCRIPTIVE STATISTICS")

print("="*80)

for asset in assets:

print(f"\n{asset}:")

print("-" * 60)

ret = returns[asset].dropna()

print(f"Returns:")

print(f" Mean: {ret.mean():.4f}%")

print(f" Std Dev: {ret.std():.4f}%")

print(f" Min: {ret.min():.4f}%")

print(f" Max: {ret.max():.4f}%")

print(f" Skewness: {stats.skew(ret):.4f}")

print(f" Kurtosis: {stats.kurtosis(ret):.4f}")

# Jarque-Bera test for normality

jb_stat, jb_pval = stats.jarque_bera(ret)

print(f"\n Jarque-Bera test (H0: Normal distribution):")

print(f" Statistic: {jb_stat:.4f}")

print(f" P-value: {jb_pval:.6f}")

if jb_pval < 0.05:

print(f" ✗ Reject normality (at 5% level)")

else:

print(f" ✓ Cannot reject normality")

================================================================================

DESCRIPTIVE STATISTICS

================================================================================

SP500:

------------------------------------------------------------

Returns:

Mean: 0.1787%

Std Dev: 4.2935%

Min: -46.4730%

Max: 19.1527%

Skewness: -1.4686

Kurtosis: 16.5810

Jarque-Bera test (H0: Normal distribution):

Statistic: 11873.8520

P-value: 0.000000

✗ Reject normality (at 5% level)

BTC:

------------------------------------------------------------

Returns:

Mean: 0.0379%

Std Dev: 1.4561%

Min: -12.7652%

Max: 8.9683%

Skewness: -0.7816

Kurtosis: 12.7312

Jarque-Bera test (H0: Normal distribution):

Statistic: 6889.5927

P-value: 0.000000

✗ Reject normality (at 5% level)

TNX:

------------------------------------------------------------

Returns:

Mean: 0.0716%

Std Dev: 4.2557%

Min: -34.7009%

Max: 40.4797%

Skewness: 0.2095

Kurtosis: 20.0543

Jarque-Bera test (H0: Normal distribution):

Statistic: 16848.4709

P-value: 0.000000

✗ Reject normality (at 5% level)

Source

# Test stationarity for prices and returns

print("\n" + "="*80)

print("STATIONARITY TESTS")

print("="*80)

for asset in assets:

print(f"\n{'='*80}")

print(f"Asset: {asset}")

print(f"{'='*80}")

# Test price levels

print("\n[PRICE LEVELS]")

test_stationarity(prices[asset].dropna(), name=f'{asset} Prices', verbose=True)

# Test returns

print("\n[RETURNS]")

test_stationarity(returns[asset].dropna(), name=f'{asset} Returns', verbose=True)

================================================================================

STATIONARITY TESTS

================================================================================

================================================================================

Asset: SP500

================================================================================

[PRICE LEVELS]

============================================================

Stationarity Tests for: SP500 Prices

============================================================

1. Augmented Dickey-Fuller Test

----------------------------------------

Test Statistic: -2.0154

P-value: 0.2798

Lags used: 22

Critical Values:

1%: -3.4370

5%: -2.8645

10%: -2.5683

✗ ADF: Fail to reject H0 → Series is NON-STATIONARY

2. KPSS Test

----------------------------------------

Test Statistic: 0.7671

P-value: 0.0100

Lags used: 19

Critical Values:

10%: 0.1190

5%: 0.1460

2.5%: 0.1760

1%: 0.2160

✗ KPSS: Reject H0 → Series is NON-STATIONARY (at 5% level)

============================================================

[RETURNS]

============================================================

Stationarity Tests for: SP500 Returns

============================================================

1. Augmented Dickey-Fuller Test

----------------------------------------

Test Statistic: -11.1580

P-value: 0.0000

Lags used: 6

Critical Values:

1%: -3.4369

5%: -2.8644

10%: -2.5683

✓ ADF: Reject H0 → Series is STATIONARY (at 5% level)

2. KPSS Test

----------------------------------------

Test Statistic: 0.1447

P-value: 0.0524

Lags used: 6

Critical Values:

10%: 0.1190

5%: 0.1460

2.5%: 0.1760

1%: 0.2160

✓ KPSS: Fail to reject H0 → Series is STATIONARY

============================================================

================================================================================

Asset: BTC

================================================================================

[PRICE LEVELS]

============================================================

Stationarity Tests for: BTC Prices

============================================================

1. Augmented Dickey-Fuller Test

----------------------------------------

Test Statistic: -1.4068

P-value: 0.5790

Lags used: 9

Critical Values:

1%: -3.4369

5%: -2.8644

10%: -2.5683

✗ ADF: Fail to reject H0 → Series is NON-STATIONARY

2. KPSS Test

----------------------------------------

Test Statistic: 0.8059

P-value: 0.0100

Lags used: 19

Critical Values:

10%: 0.1190

5%: 0.1460

2.5%: 0.1760

1%: 0.2160

✗ KPSS: Reject H0 → Series is NON-STATIONARY (at 5% level)

============================================================

[RETURNS]

============================================================

Stationarity Tests for: BTC Returns

============================================================

1. Augmented Dickey-Fuller Test

----------------------------------------

Test Statistic: -9.3706

P-value: 0.0000

Lags used: 8

Critical Values:

1%: -3.4369

5%: -2.8644

10%: -2.5683

✓ ADF: Reject H0 → Series is STATIONARY (at 5% level)

2. KPSS Test

----------------------------------------

Test Statistic: 0.0644

P-value: 0.1000

Lags used: 9

Critical Values:

10%: 0.1190

5%: 0.1460

2.5%: 0.1760

1%: 0.2160

✓ KPSS: Fail to reject H0 → Series is STATIONARY

============================================================

================================================================================

Asset: TNX

================================================================================

[PRICE LEVELS]

============================================================

Stationarity Tests for: TNX Prices

============================================================

1. Augmented Dickey-Fuller Test

----------------------------------------

Test Statistic: -0.2905

P-value: 0.9268

Lags used: 2

Critical Values:

1%: -3.4369

5%: -2.8644

10%: -2.5683

✗ ADF: Fail to reject H0 → Series is NON-STATIONARY

2. KPSS Test

----------------------------------------

Test Statistic: 0.5141

P-value: 0.0100

Lags used: 19

Critical Values:

10%: 0.1190

5%: 0.1460

2.5%: 0.1760

1%: 0.2160

✗ KPSS: Reject H0 → Series is NON-STATIONARY (at 5% level)

============================================================

[RETURNS]

============================================================

Stationarity Tests for: TNX Returns

============================================================

1. Augmented Dickey-Fuller Test

----------------------------------------

Test Statistic: -5.7259

P-value: 0.0000

Lags used: 22

Critical Values:

1%: -3.4370

5%: -2.8645

10%: -2.5683

✓ ADF: Reject H0 → Series is STATIONARY (at 5% level)

2. KPSS Test

----------------------------------------

Test Statistic: 0.1848

P-value: 0.0217

Lags used: 27

Critical Values:

10%: 0.1190

5%: 0.1460

2.5%: 0.1760

1%: 0.2160

✗ KPSS: Reject H0 → Series is NON-STATIONARY (at 5% level)

============================================================

Source

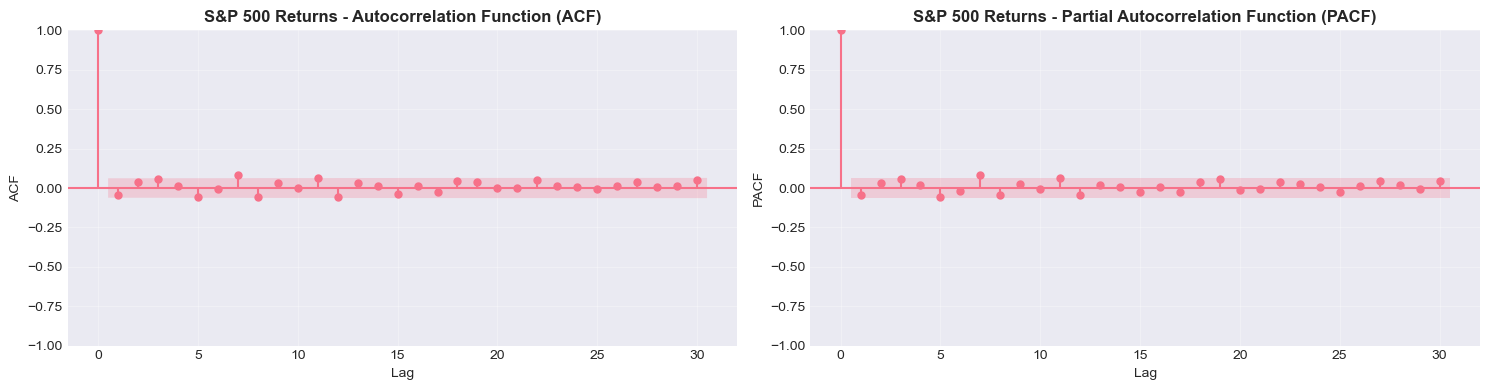

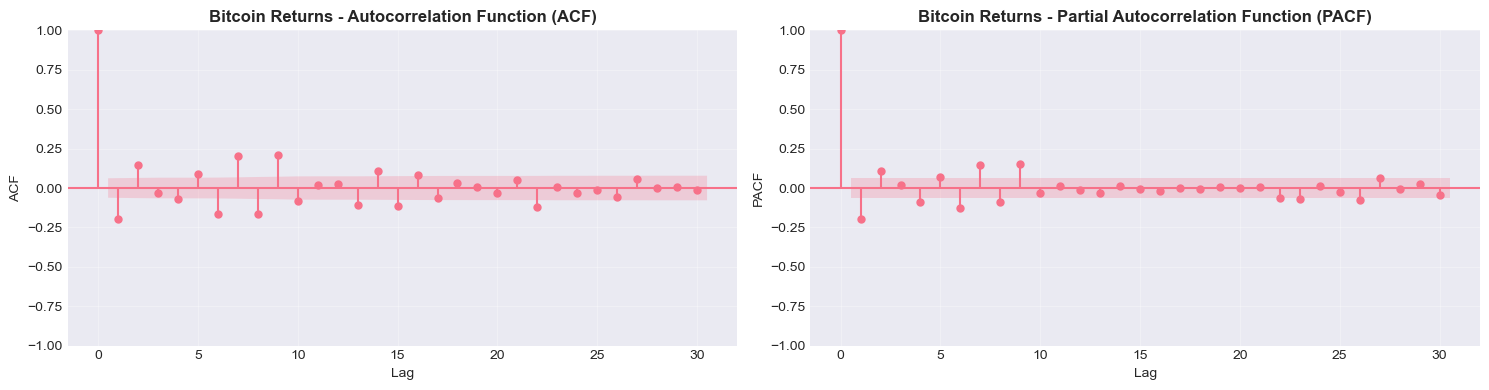

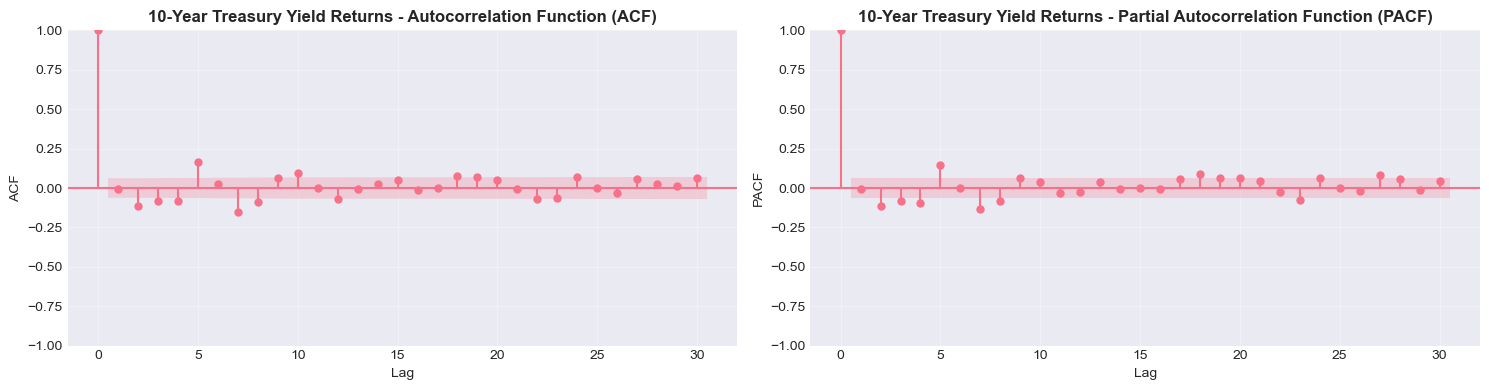

# ACF and PACF for returns

print("\nAutocorrelation Analysis of Returns")

print("="*80)

for asset, title in zip(assets, titles):

print(f"\n{title}")

plot_acf_pacf(returns[asset].dropna(), lags=30, title=f'{title} Returns')

Autocorrelation Analysis of Returns

================================================================================

S&P 500

Bitcoin

10-Year Treasury Yield

Source

# Test for autocorrelation in returns and squared returns

from statsmodels.stats.diagnostic import acorr_ljungbox

print("\nLjung-Box Tests for Autocorrelation")

print("="*80)

for asset, title in zip(assets, titles):

print(f"\n{title}:")

print("-" * 60)

ret = returns[asset].dropna()

ret_sq = ret ** 2

# Test returns

lb_ret = acorr_ljungbox(ret, lags=[10, 20], return_df=True)

print("\nReturns:")

print(lb_ret.to_string())

# Test squared returns (proxy for volatility clustering)

lb_sq = acorr_ljungbox(ret_sq, lags=[10, 20], return_df=True)

print("\nSquared Returns (volatility):")

print(lb_sq.to_string())

if lb_sq['lb_pvalue'].iloc[-1] < 0.05:

print("\n✓ Evidence of volatility clustering (GARCH effects likely)")

else:

print("\n✗ No strong evidence of volatility clustering")

Ljung-Box Tests for Autocorrelation

================================================================================

S&P 500:

------------------------------------------------------------

Returns:

lb_stat lb_pvalue

10 20.309707 0.026456

20 34.351273 0.023844

Squared Returns (volatility):

lb_stat lb_pvalue

10 21.246715 0.019437

20 22.952011 0.291157

✗ No strong evidence of volatility clustering

Bitcoin:

------------------------------------------------------------

Returns:

lb_stat lb_pvalue

10 223.211167 2.272727e-42

20 275.466384 8.015588e-47

Squared Returns (volatility):

lb_stat lb_pvalue

10 1286.284029 3.488940e-270

20 1471.811471 4.437857e-300

✓ Evidence of volatility clustering (GARCH effects likely)

10-Year Treasury Yield:

------------------------------------------------------------

Returns:

lb_stat lb_pvalue

10 99.660254 6.373216e-17

20 121.400995 1.568106e-16

Squared Returns (volatility):

lb_stat lb_pvalue

10 1173.519933 7.412772e-246

20 1222.565773 1.111894e-246

✓ Evidence of volatility clustering (GARCH effects likely)

7. Key Takeaways and Summary¶

Concepts Covered:¶

Time Series Fundamentals

Time series are ordered sequences where temporal dependence matters

Key features: trends, seasonality, cycles, and irregular components

Stationarity

Weak stationarity requires constant mean, variance, and autocovariance

Most time series models assume stationarity

Non-stationary series can often be made stationary through differencing or detrending

Testing for Stationarity

ADF test: H₀ is unit root (non-stationary)

KPSS test: H₀ is stationarity

Use both tests for robustness

White Noise and Random Walks

White noise is stationary and unpredictable

Random walks are non-stationary with variance growing over time

First differencing transforms random walks to white noise

Autocorrelation Analysis

ACF measures total correlation at each lag

PACF measures direct correlation after removing intermediate effects

ACF/PACF patterns help identify appropriate models

Financial Data Characteristics

Price levels are typically non-stationary

Returns are typically stationary but may show autocorrelation

Squared returns often show strong autocorrelation (volatility clustering)

Returns are often non-normal (fat tails, skewness)

Next Session Preview:¶

In Session 2, we will cover:

Classical time series decomposition

Smoothing techniques (moving averages, exponential smoothing)

Trend extraction methods (Hodrick-Prescott filter)

Seasonal adjustment procedures

8. Exercises¶

Exercise 1: Simulation Study¶

Generate 1000 observations from the following processes and compare their ACF/PACF:

AR(2):

MA(2):

ARMA(1,1):

Exercise 2: Real Data Analysis¶

Download data for a different asset (e.g., EUR/USD exchange rate, crude oil prices) and:

Test price levels and returns for stationarity

Examine ACF and PACF

Test for volatility clustering

Compare findings with S&P 500 results

Exercise 3: Differencing¶

For a non-stationary series:

Apply first differencing and test for stationarity

If still non-stationary, apply second differencing

Determine the order of integration (I(0), I(1), or I(2))

Exercise 4: Seasonal Patterns¶

Download monthly economic data (e.g., retail sales, unemployment rate) and:

Plot the series and visually identify seasonal patterns

Calculate ACF and look for seasonal spikes

Discuss implications for modeling

Source

# Space for your solutions to exercises

# Exercise 1:

# Your code here

# Exercise 2:

# Your code here

# Exercise 3:

# Your code here

# Exercise 4:

# Your code hereReferences and Further Reading¶

Textbooks:¶

Hamilton, J.D. (1994). Time Series Analysis. Princeton University Press.

Tsay, R.S. (2010). Analysis of Financial Time Series (3rd ed.). Wiley.

Brockwell, P.J., & Davis, R.A. (2016). Introduction to Time Series and Forecasting (3rd ed.). Springer.

Lütkepohl, H. (2005). New Introduction to Multiple Time Series Analysis. Springer.

Papers:¶

Dickey, D.A., & Fuller, W.A. (1979). Distribution of the estimators for autoregressive time series with a unit root. Journal of the American Statistical Association, 74(366a), 427-431.

Kwiatkowski, D., Phillips, P.C., Schmidt, P., & Shin, Y. (1992). Testing the null hypothesis of stationarity against the alternative of a unit root. Journal of Econometrics, 54(1-3), 159-178.

Python Resources:¶

statsmodels documentation: https://

www .statsmodels .org/ Seabold, S., & Perktold, J. (2010). Statsmodels: Econometric and statistical modeling with Python. Proceedings of the 9th Python in Science Conference.

Instructor Contact: hhs.nl

Office Hours: [Mon-Fri 9am-5pm]